- Beverages

- RTD Alcoholic Beverages Market

RTD Alcoholic Beverages Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

RTD Alcoholic Beverages Market by Product (Hard Seltzers, Canned Cocktails, Flavored Malt Beverages (FMBs), Hard Ciders, Hard Kombucha, and Alcopops), Base Type (Spirit-Based RTDs, Malt-Based RTDs, Wine-Based RTDs, and Beer-Based RTDs), Alcohol Content (Low Alcohol (1%-7%), Medium Alcohol (4%-8%), and High Alcohol (>7%)), Packaging Type (Cans, Bottles, Tetra Packs, and Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Liquor Stores, Online Retail, and Others), and Regional Analysis from 2026 to 2033

RTD Alcoholic Beverages Market Share and Trend Analysis

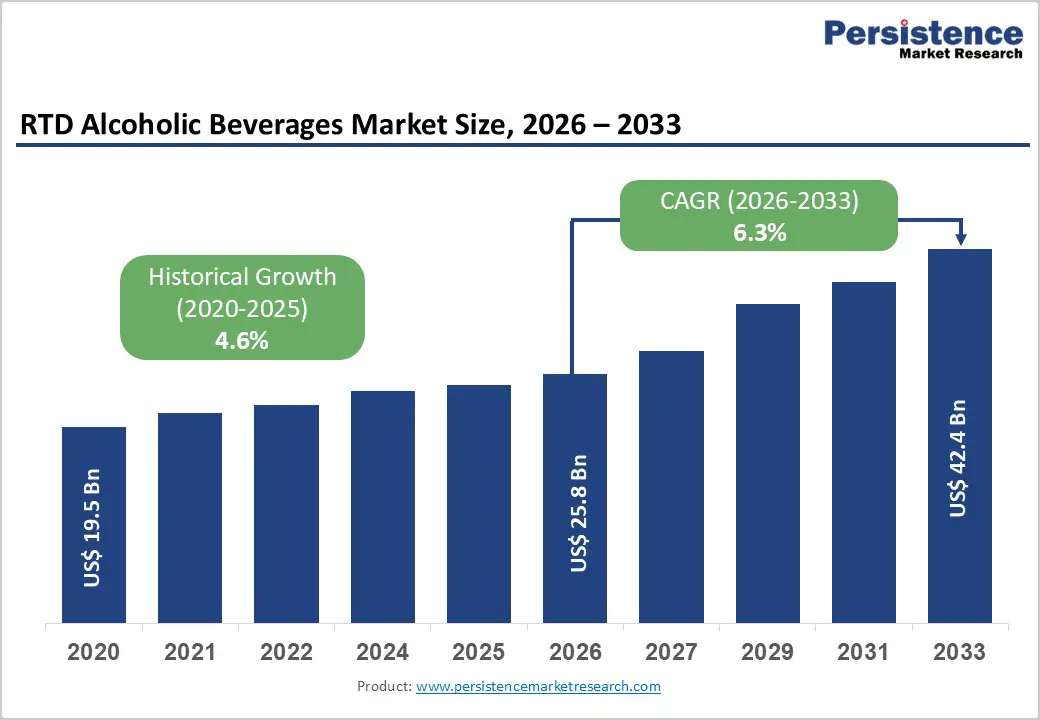

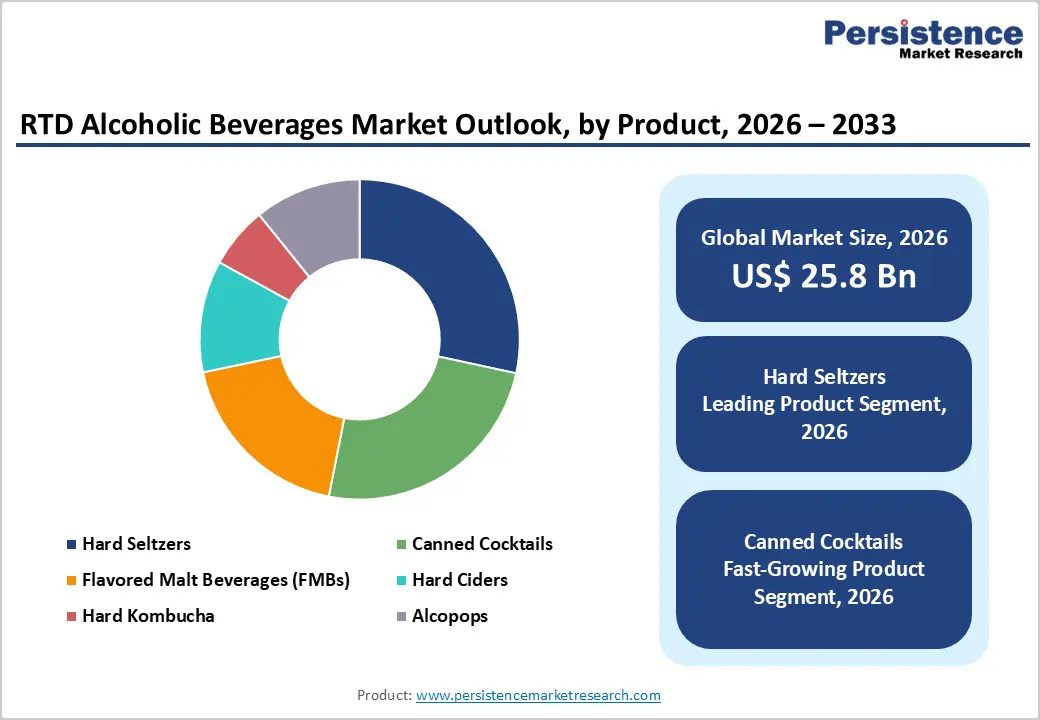

The global RTD alcoholic beverages market size is estimated to grow from US$ 25.8 Bn in 2026 to US$ 42.4 Bn by 2033. The market is projected to record a CAGR of 6.3% during the forecast period from 2026 to 2033.

Global demand for ready-to-drink (RTD) alcoholic beverages is expanding steadily as consumers increasingly shift toward convenient, ready-to-consume formats that combine taste, portability, and premium experiences. Products such as hard seltzers, canned cocktails, and flavored malt beverages are gaining strong traction due to their ease of consumption and growing alignment with modern lifestyles.

Consumers are moving away from traditional spirits and beer toward lighter, flavored, and lower-calorie alternatives that fit social and on-the-go occasions. Innovation in flavor profiles, including fruit blends, botanicals, and low-sugar formulations, is enhancing product appeal across diverse consumer groups. In parallel, premiumization trends are encouraging manufacturers to introduce spirit-based RTDs that replicate bar-quality cocktails. Expanding retail penetration, especially across supermarkets and online platforms, is improving product accessibility. Continuous advancements in packaging, formulation, and branding strategies are further strengthening global market expansion, particularly across younger demographics and urban populations.

Key Industry Highlights

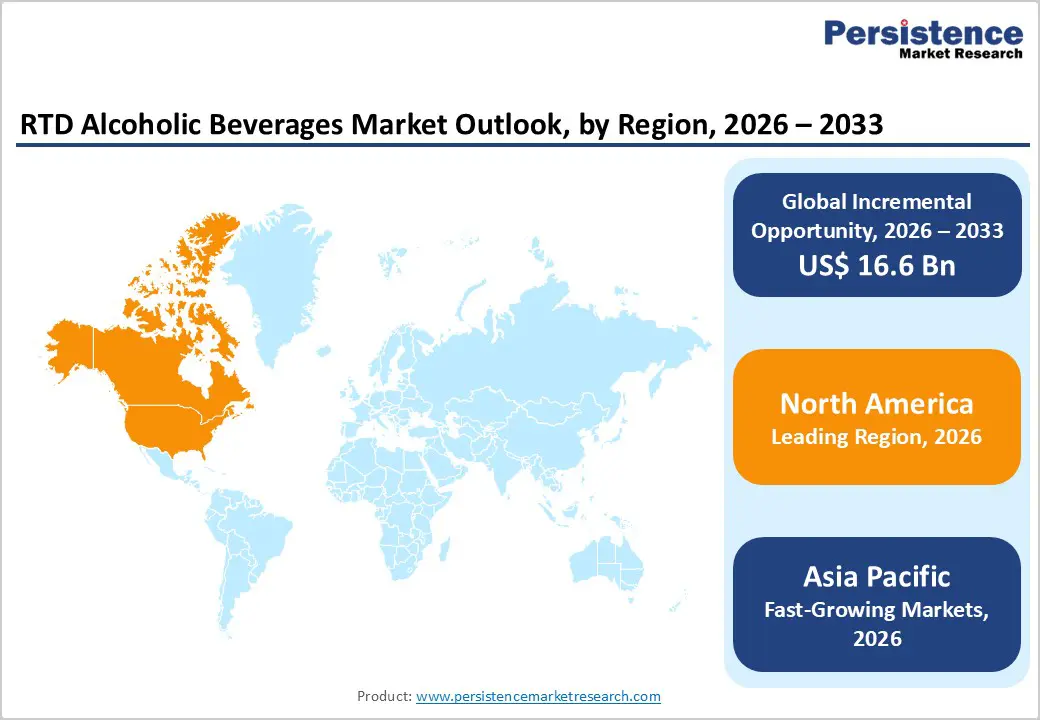

- Leading Region: North America dominates with 46.7%, supported by strong consumer adoption of RTDs, established beverage infrastructure, high disposable income, and continuous product innovation.

- Fastest-Growing Region: Asia Pacific is witnessing rapid growth driven by urbanization, increasing disposable incomes, expanding retail networks, and rising acceptance of Western drinking habits.

- Leading Product Segment: Hard seltzers account for the largest share at 28.4%, primarily due to their low-calorie positioning, refreshing taste, and broad appeal among health-conscious consumers.

- Fastest-Growing Product Segment: Canned cocktails are expanding at a faster pace as demand rises for premium, spirit-based, ready-to-serve beverages offering convenience and quality.

- Leading Alcohol Content Segment: Low alcohol (1%-7%) leads with 41.6%, supported by increasing preference for light, sessionable drinks suited for casual and social consumption.

- Fastest-Growing Alcohol Content Segment: Medium alcohol (4%-8%) is gaining momentum as consumers seek a balance between flavor intensity and moderate alcohol strength in RTD formats.

| Key Insights | Details |

| RTD Alcoholic Beverages Market Size (2026E) | US$ 25.8 Bn |

| Market Value Forecast (2033F) | US$ 42.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6 % |

Market Dynamics

Driver - Rising Demand for Convenient, Premium, and Ready-to-Consume Alcoholic Options

Shifting consumer lifestyles and evolving drinking preferences are significantly accelerating demand for ready-to-drink alcoholic beverages across global markets. Increasing urbanization, busy schedules, and the growing preference for convenience-oriented consumption have positioned RTDs as a practical alternative to traditional alcoholic drinks that require preparation or mixing. Consumers, particularly millennials and Gen Z, are actively seeking portable, single-serve formats that align with on-the-go and social drinking occasions such as outdoor events, house parties, and casual gatherings.

Additionally, premiumization trends are reshaping product development strategies, with manufacturers introducing high-quality, spirit-based RTDs that replicate bar-quality cocktails. Flavor innovation remains a key growth lever, with companies expanding portfolios to include exotic fruits, botanical infusions, and low-sugar formulations. Additionally, rising health awareness is influencing demand for low-calorie, low-alcohol, and clean-label beverages, encouraging brands to reformulate products with natural ingredients and transparent labeling. Strong retail penetration, aggressive marketing campaigns, and celebrity-backed product launches are further boosting category visibility. As consumer demand continues to shift toward convenience, variety, and premium experiences, RTD alcoholic beverages are witnessing sustained global traction.

Restraints - Regulatory Complexities and Supply Chain Cost Pressures

The industry faces considerable challenges arising from complex regulatory frameworks and fluctuating input costs, which can impact production and distribution efficiency. Alcoholic beverages are subject to stringent regulations across different countries, including restrictions on alcohol content, labeling requirements, advertising limitations, and taxation policies. These regulatory variations often create barriers for global players attempting to standardize products or expand into new markets, resulting in longer approval timelines and increased compliance costs.

In addition to regulatory constraints, supply chain volatility presents a significant concern. Key inputs such as base alcohol (spirits, malt, or wine), flavoring agents, sweeteners, and packaging materials like aluminum cans and glass bottles are susceptible to price fluctuations driven by global commodity trends and logistical disruptions. The rising cost of sustainable packaging solutions further adds to operational expenses. Maintaining product consistency across large-scale production while managing diverse flavor profiles also increases manufacturing complexity. Moreover, competition from traditional alcoholic beverages and emerging low/no-alcohol alternatives can limit market expansion in certain regions. Retail pricing pressures and margin constraints may also impact smaller manufacturers. Collectively, these factors create operational inefficiencies and cost burdens that may restrain rapid market growth despite strong consumer demand.

Opportunity - Expansion into Premium, Functional, and Emerging Market Segments

Significant growth potential lies in the expansion of premium, health-oriented, and region-specific RTD offerings, supported by evolving consumer expectations and untapped markets. The premium segment, particularly spirit-based canned cocktails, is gaining momentum as consumers increasingly seek high-quality, bar-like experiences in convenient formats. Brands are capitalizing on this trend by launching craft-inspired products, incorporating premium spirits, and emphasizing authentic cocktail recipes. Another key opportunity is the development of functional and better-for-you alcoholic beverages. Products featuring low sugar, organic ingredients, natural flavors, and added functional benefits such as electrolytes or botanical extracts are attracting health-conscious consumers. The rise of moderation trends is also encouraging innovation in low- and no-alcohol RTDs, opening new consumer segments. Emerging markets across Asia Pacific, Latin America, and parts of Africa present strong expansion opportunities due to rising disposable incomes, urbanization, and increasing acceptance of western drinking habits. Digital transformation and e-commerce platforms are further enabling direct-to-consumer distribution, enhancing accessibility and brand engagement. Additionally, strategic collaborations, celebrity endorsements, and localized flavor innovations are helping companies strengthen market penetration. As product innovation and geographic expansion continue, the RTD category is well-positioned for long-term growth.

Category-wise Analysis

By Product Insights

Hard seltzers are expected to retain their leading position in the global RTD alcoholic beverages market in 2026, accounting for 28.4% of total revenue. Their dominance is driven by increasing consumer inclination toward light, refreshing, and low-calorie alcoholic drinks that align with evolving health-conscious lifestyles. These beverages typically feature simple ingredient profiles, appealing to clean-label trends while offering convenient, ready-to-consume formats. The segment benefits from continuous flavor innovation, including fruit-infused and exotic variants, which attract younger demographics. Additionally, strong branding, aggressive marketing, and wide availability across retail channels have enhanced product visibility. Manufacturers are also focusing on expanding premium hard seltzer portfolios and improving carbonation quality to enhance the drinking experience. As consumers increasingly seek alternatives to traditional beer and spirits, hard seltzers continue to gain traction, reinforcing their leadership across global markets.

By Alcohol Content Insights

The low alcohol segment (1%-7%) is projected to hold the largest share of the RTD alcoholic beverages market in 2026, contributing 41.6% of overall revenue. Growth is largely fueled by shifting consumer behavior toward moderation, wellness, and mindful drinking habits. Low-ABV beverages offer a balanced combination of flavor and reduced alcohol intensity, making them suitable for social and extended consumption occasions. Increasing awareness around health and calorie intake is encouraging consumers to opt for lighter alcoholic options without compromising taste. Beverage companies are actively introducing innovative formulations with natural flavors, reduced sugar content, and functional ingredients to cater to this demand. Furthermore, regulatory support for lower alcohol products in several regions is facilitating wider market penetration.

By Distribution Channel Insights

Supermarkets and hypermarkets are anticipated to account for the largest share of the RTD alcoholic beverages market in 2026, capturing 38.5% of total revenue. Their leadership is attributed to strong shelf visibility, extensive product assortments, and the ability to attract high footfall across diverse consumer groups. These retail formats enable consumers to compare multiple brands, flavors, and price points in a single location, supporting informed purchasing decisions. Large retail chains also benefit from established supply chain networks, ensuring consistent product availability and efficient inventory management. Promotional activities such as discounts, bundled offers, and in-store displays further enhance sales volumes. Additionally, the expansion of organized retail infrastructure, particularly in emerging economies, is strengthening the reach of RTD alcoholic beverages. As consumers increasingly prefer convenient one-stop shopping experiences, supermarkets and hypermarkets continue to dominate distribution dynamics.

Regional Insights

North America RTD Alcoholic Beverages Market Trends

North America is projected to maintain its position as the largest regional market in 2026, accounting for 46.7% of global revenue, with the United States representing the primary growth engine. The region’s leadership is supported by a highly mature alcoholic beverage industry, strong consumer acceptance of innovative drink formats, and rapid adoption of premium ready-to-drink offerings. Consumers across the U.S. and Canada are increasingly shifting toward convenient, portable beverages that align with busy lifestyles and social consumption patterns. This has significantly boosted demand for hard seltzers, canned cocktails, and spirit-based RTDs.

Moreover, the presence of major beverage manufacturers and well-established distribution networks enables rapid commercialization of new products. Companies are continuously investing in product diversification, focusing on unique flavor combinations, low-calorie formulations, and premium packaging formats. E-commerce and direct-to-consumer channels are also gaining traction, complementing traditional retail. Favorable regulatory frameworks and high disposable incomes further support market expansion. Additionally, strong marketing campaigns and brand loyalty play a critical role in sustaining consumer engagement. These combined factors continue to reinforce North America’s dominance in the global RTD alcoholic beverages landscape.

Europe RTD Alcoholic Beverages Market Trends

Europe represents a mature yet steadily evolving market for RTD alcoholic beverages, supported by established drinking culture and increasing demand for premium and low-alcohol products. Countries such as the United Kingdom, Germany, and France are key contributors, driven by strong consumption of flavored and spirit-based RTDs. The region is witnessing a notable shift toward premiumization, with consumers increasingly favoring high-quality ingredients, authentic flavors, and craft-inspired beverages.

Furthermore, growing inclination toward low-ABV and non-alcoholic alternatives is also shaping market dynamics, reflecting broader health and wellness trends. Packaging innovation, particularly the shift toward sustainable and portable can formats, is further influencing purchasing behavior. Additionally, regulatory frameworks promoting transparency and clean-label products enhance consumer trust and adoption. Seasonal consumption patterns, especially in Southern Europe, also contribute to demand for refreshing RTD options such as cocktails and sangrias. While growth remains moderate compared to emerging regions, continuous product innovation and evolving consumer preferences ensure stable expansion across the European market.

Asia Pacific RTD Alcoholic Beverages Market Trends

Asia Pacific is expected to be the fastest-growing region in the RTD alcoholic beverages market, driven by rapid urbanization, rising disposable incomes, and expanding young consumer demographics. Countries such as China, India, Japan, and South Korea are witnessing increased adoption of RTD products, particularly among millennials and first-time drinkers seeking convenient and approachable alcoholic options.

The regional market growth is strongly supported by changing lifestyles, westernization of consumption habits, and increasing penetration of modern retail and e-commerce platforms. Low-alcohol and fruit-flavored RTDs are especially popular, offering an accessible entry point into alcohol consumption. Additionally, innovation in localized flavors and smaller packaging formats enhances affordability and consumer appeal. Urban convenience stores and online delivery platforms are playing a crucial role in improving product accessibility. With a large population base, rising experimentation with new beverage formats, and increasing investments by global and regional players, Asia Pacific continues to emerge as the most dynamic and high-growth market globally.

Competitive Landscape

The global RTD alcoholic beverages market is highly competitive, with strong participation from Anheuser-Busch InBev SA/NV, Diageo plc, Pernod Ricard SA, Suntory Holdings Limited, and Molson Coors Beverage Company. These companies leverage strong brand portfolios, large-scale production capabilities, and extensive global distribution networks to strengthen their market presence while enhancing product innovation, flavor diversification, and premium positioning of RTD offerings.

Growing demand for convenient, low-alcohol, and premium beverages is accelerating product innovation. Manufacturers are focusing on expanding canned cocktail portfolios, improving flavor formulations, strengthening regulatory compliance, and forming strategic collaborations while increasing R&D investments to develop functional, low-sugar, and premium RTD beverages.

Key Industry Developments:

- In March 2026, Molson Coors Beverage Company strengthened its RTD portfolio through a strategic deal involving Monaco Cocktails. The move enhances its presence in the fast-growing canned cocktail segment and broadens its premium product offerings. This expansion supports the company’s strategy to capture rising consumer demand for convenient, spirit-based ready-to-drink beverages.

- In March 2026, Jack Daniel’s & Coca-Cola launched a new 330ml can format across its RTD range in the UK to align with growing demand for premium ready-to-drink beverages. The updated sleek packaging improves shelf visibility and merchandising efficiency, particularly in convenience and impulse channels. Additionally, the new format enhances sustainability by reducing material usage while optimizing transport and storage.

- In November 2025, PepsiCo and Varun Beverages Limited planned their entry into India’s alcoholic beverages market by exploring the launch of ready-to-drink (RTD) products. The initiative focuses on tapping into the fast-growing premium and low-alcohol RTD segment, driven by evolving consumer preferences and rising demand for convenient beverage formats.

Companies Covered in RTD Alcoholic Beverages Market

- Anheuser-Busch InBev SA/NV

- Diageo plc

- Pernod Ricard SA

- Suntory Holdings Limited

- Molson Coors Beverage Company

- Brown-Forman Corporation

- Asahi Group Holdings, Ltd.

- Davide Campari-Milano N.V.

- Mark Anthony Group of Companies

- Sazerac Company, Inc.

- Constellation Brands, Inc.

- The Boston Beer Company, Inc.

- Bacardi Limited

- Au Vodka Ltd

- Two Chicks Drinks, LLC

- Others

Frequently Asked Questions

The global RTD alcoholic beverages market is projected to be valued at US$ 25.8 Bn in 2026.

Rising disposable incomes, premiumization trends, and growing demand for convenient formats like RTDs are driving the global alcoholic beverages market.

The global RTD alcoholic beverages market is poised to witness a CAGR of 6.3 % between 2026 and 2033.

Expansion of low/no-alcohol products, craft innovations, and emerging market penetration offer key growth opportunities in the global alcoholic beverages market.

Anheuser-Busch InBev SA/NV, Diageo plc, Pernod Ricard SA, Suntory Holdings Limited, and Molson Coors Beverage Company are some of the key players in the alcoholic beverages market.