- Plastics, Polymers & Resins

- Polyester Medical Films Market

Polyester Medical Films Market Size, Share, and Growth Forecast 2025 - 2032

Polyester Medical Films Market by Film Thickness (<100 Microns, 100 Microns - 300 Microns, >300 Microns), Application (Diagnostic Strips, Medical Tapes and Adhesives, Transdermal Therapeutic Systems (TTS), Biosensors, Labelling, Other), and Regional Analysis for 2025 - 2032

Polyester Medical Films Market Share and Trend Analysis

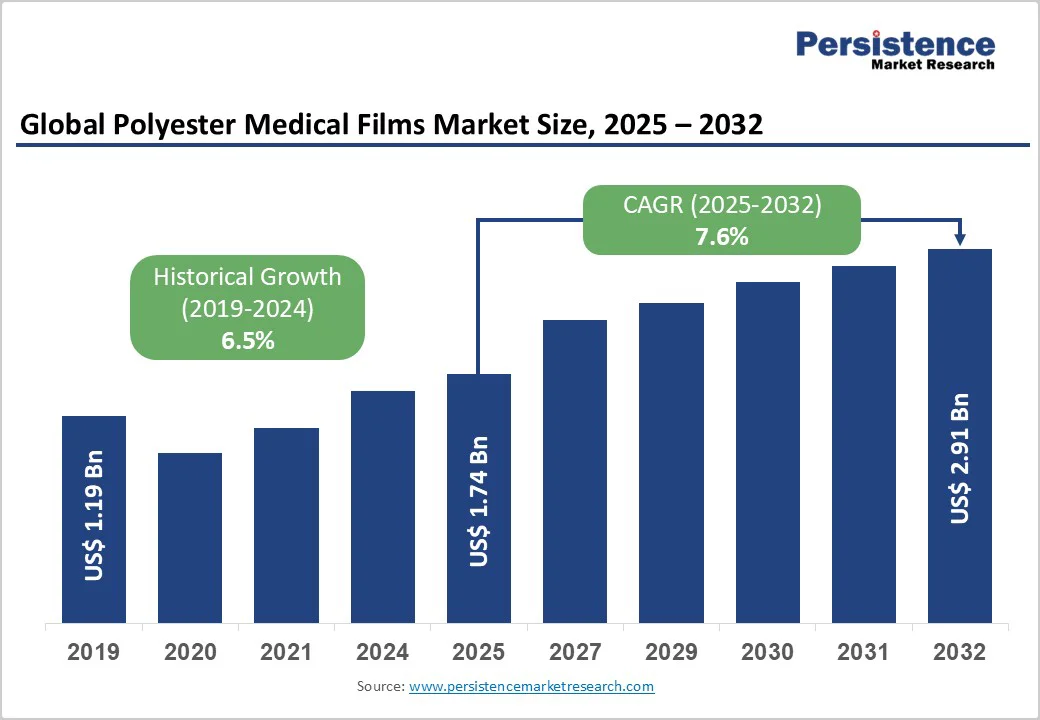

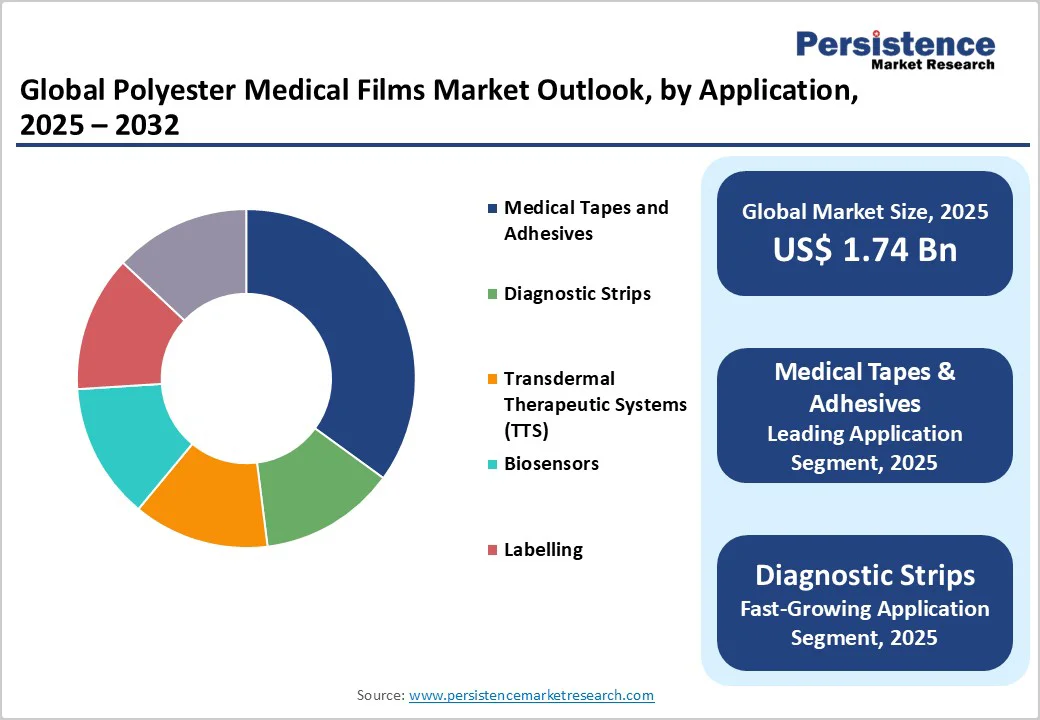

The global polyester medical films market size is likely to be valued at US$ 1.7 billion in 2025, and is projected to reach US$ 2.9 billion by 2032, growing at a CAGR of 7.6% during the forecast period 2025 - 2032. The primary driver of this growth is the escalating demand for advanced medical devices and packaging solutions amid rising chronic disease prevalence worldwide.

Supporting this, global healthcare investments have surged, with the World Health Organization (WHO) reporting that chronic conditions, or noncommunicable diseases (NCDs) killed around 43 million people globally in 2021. These numbers have necessitated the development of biocompatible materials such as polyester films for diagnostics and drug delivery.

Key Industry Highlights

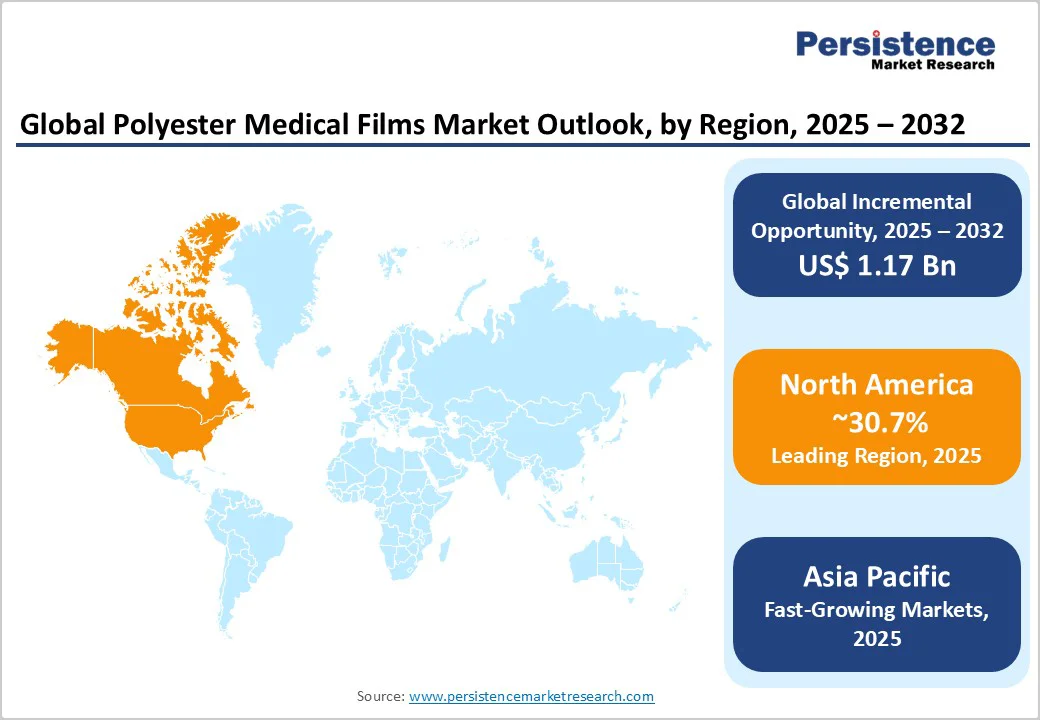

- Regional Leader: North America is slated to lead the market with around 30.7% in 2025, due to advanced healthcare infrastructure of the U.S. and high volume of surgeries in the region.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing regional market during 2025 - 2032, driven by manufacturing hubs in China and India, with surging healthcare investments fueling the demand for cost-effective films.

- Leading Application: Medical tapes and adhesives are likely to dominate the market share in 2025, leveraging polyester's adhesion for wound care in chronic disease management.

- Fastest-growing Application: Biosensors represent the fastest-growing application segment, propelled by wearable tech advancements and real-time monitoring needs in digital health.

- Growth Opportunities: Advancements in biodegradable polyesters offer key opportunities, aligning with sustainability policies to tap into eco-friendly medical packaging demands.

| Key Insights | Details |

|---|---|

| Polyester Medical Films Size (2025E) | US$ 1.7 Bn |

| Market Value Forecast (2032F) | US$ 2.9 Bn |

| Projected Growth CAGR (2025 - 2032) | 7.6% |

| Historical Market Growth (2019-2024) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Chronic Diseases

The increasing incidence of chronic conditions such as diabetes and obesity is a major driver for the polyester medical films market growth, as these films are integral to diagnostic tools and therapeutic systems. For example, according to the Organisation for Economic Co-operation and Development (OECD), chronic conditions such as cancer and diabetes are the leading causes of death across OECD countries.

Polyester films, particularly Mylar® PET, offer exceptional optical clarity, durability, and chemical stability, making them ideal substrates for diagnostic strips used in blood glucose monitoring, pregnancy tests, and infectious disease detection. As a result, healthcare providers heavily rely on these films to meet the needs of patients suffering from chronic diseases, especially the elderly.

Innovations in medical technology, particularly in tissue engineering and flexible electronics, propel the adoption of polyester medical films due to their superior mechanical properties and adaptability. These advancements have enabled the development of smart packaging with embedded sensors, improving drug delivery efficiency and traceability in pharmaceuticals.

For instance, enhanced barrier properties in films prevent contamination, aligning with rising investments in preventive healthcare. This technological evolution not only boosts product performance but also supports the integration of polyester in emerging applications like 3D-printed medical devices, ensuring long-term market vitality.

Increasingly Stringent Regulatory Requirements

Stringent regulatory frameworks pose significant barriers to the polyester medical films market expansion, as compliance with biocompatibility and safety standards demands extensive testing and certification.

Bodies such as the U.S. Food and Drug Administration (FDA) enforce rigorous guidelines under 21 CFR Part 820, which can delay product launches and increase costs significantly for manufacturers. These regulations aim to mitigate risks of adverse reactions, but they limit innovation speed, particularly for novel film formulations.

Furthermore, environmental concerns and inefficient recycling processes are also hindering market growth, as the non-biodegradable nature of polyester draws scrutiny amid global sustainability pushes. The European Union (EU)'s Single-Use Plastics Directive mandates reduced plastic use, impacting medical packaging and potentially increasing costs for compliant alternatives.

Current recycling rates for medical-grade polyesters are low due to contamination risks during healthcare applications, leading to higher waste volumes. This inefficiency exacerbates regulatory pressures, as seen in bans on certain plastics in packaging, forcing manufacturers to invest in costly modifications.

Expansion in Biosensor Technologies

The rapid growth in biosensor technologies presents a key opportunity for market participants, as polyester medical films serve as flexible substrates for wearable and implantable devices.

With the biosensor market projected to expand significantly due to demand for real-time health monitoring, polyesters' electrical insulation and biocompatibility enable integration in glucose monitors and cardiac sensors. In Asia Pacific, manufacturing hubs such as China and India offer cost advantages, with investments in healthcare infrastructure exceeding US$ 100 billion annually, creating a huge demand for advanced films.

The shift toward sustainable materials opens even more opportunities in the polyester medical films market, with tunable biodegradable polyesters addressing environmental regulations and eco-conscious healthcare trends. Polyesters such as polylactic acid are gaining traction for implants and packaging, supported by the European Commission's Green Deal, which targets 50% plastic recycling by 2030 and incentivizes bio-based alternatives.

Similarly, in North America, the U.S. Environmental Protection Agency (EPA) reports rising demand for recyclable medical films, with sustainability considerations driving of procurement decisions in hospitals. News from industry leaders highlights investments in low-impact production, such as reduced energy processes, enhancing market appeal amid global plastic waste concerns exceeding 400 million tons yearly.

Category-wise Analysis

Film Thickness Insights

The <100 Microns segment is likely to lead in 2025, commanding approximately 45% of the polyester medical films market revenue share owing to its suitability for flexible, thin applications requiring high precision and conformability. These ultra-thin films excel in diagnostic strips and biosensors, where minimal thickness ensures optimal sensor response and patient comfort without compromising durability.

This dominance is further justified by the rising demand for wearable devices, where thin polyesters provide essential electrical insulation and biocompatibility. As minimally invasive technologies advance, the segment's versatility continues to drive its leadership, aligning with the broader medical tapes market trends for lightweight materials.

Application Insights

Medical tapes and adhesives are set to dominate in 2025, holding about 35% of the market share, on account of the critical role they play in wound care and secure device attachment. These films offer superior adhesion and tear resistance, essential for sterile dressings that prevent infections in millions of surgical procedures globally each year.

Their moisture-resistant properties ensure longevity in high-humidity environments, making them indispensable for hospital settings. Justification stems from biocompatibility standards met under ISO 10993, enabling safe skin contact and reducing allergic reactions compared to alternatives.

Regional Insights

North America Polyester Medical Films Market Trends

North America leads the polyester medical films market share in 2025, driven by the advanced healthcare ecosystem and high volume of surgical innovations in the U.S. The FDA's rigorous compliance requirements for medical device materials, including biocompatibility testing for cytotoxicity, sensitization, systemic toxicity, and hemocompatibility under 21 CFR 878.5000, drive demand for high-quality, well-documented polyester film grades that meet Class II medical device standards.

Innovation in the region thrives through R&D hubs such as those in Massachusetts, where collaborations between universities and firms advance tissue engineering applications. Recent developments, including enhanced barrier films, align with the push for infection prevention, as evidenced by rising minimally invasive surgery rates. This ecosystem positions North America as a pioneer in adopting next-generation polyesters.

Europe Polyester Medical Films Market Trends

The Europe polyester medical films market is expected to exhibit strong performance, particularly in Germany, the U.K., France, and Spain, underpinned by harmonized regulations via the EU Medical Device Regulation (MDR). These policies standardize biocompatibility testing, facilitating cross-border trade and boosting adoption in pharmaceutical packaging. In Germany, the focus on precision manufacturing supports films for biosensors, with the country's € 50 billion annual medtech exports highlighting its influence.

European regulatory frameworks, including the Packaging and Packaging Waste Directive (94/62/EC) and EN 868 series standards for terminally sterilized medical device packaging, establish stringent requirements for material biocompatibility, sterility maintenance, and environmental sustainability.

Strategic initiatives by companies such as Coveme SpA and Futamura Chemical Co., Ltd. in developing eco-friendly film alternatives position Europe as a leader in sustainable medical packaging innovation, aligning with the EU’s circular economy objectives and carbon neutrality commitments.

Asia Pacific Polyester Medical Films Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing regional market for polyester medical films, propelled by manufacturing advantages in China, Japan, India, and ASEAN countries. China's expansive production capacities, supported by over US$ 100 billion in healthcare investments, enable cost-effective scaling for diagnostic applications. India's pharmaceutical hub status drives demand for films in labeling and adhesives, with exports growing at 10% annually.

Growth dynamics are fueled by urbanization and rising per capita income, increasing access to advanced medical devices. In Japan, technological prowess in biosensors leverages polyester's properties for the needs of an aging population, as 65% of its residents are over 50. The market in ASEAN benefits from supply chain efficiencies, with recent policy incentives for medtech attracting foreign investments. This regional momentum positions the Asia Pacific for exponential expansion.

Competitive Landscape

The global polyester medical films market structure is moderately fragmented, with a modest hold of Tier-1 companies, while numerous mid-tier players compete through specialization. Expansion strategies emphasize R&D investments, such as developing biocompatible variants to meet regulatory demands.

Leaders differentiate via superior barrier properties and sustainability, like recyclable formulations. Emerging models focus on partnerships for custom solutions, enhancing supply chain resilience amid global healthcare demands. This structure encourages innovation while allowing niche entrants in high-growth segments such as biosensors.

Key Industry Developments

- In October 2025, Selenis introduced a new medical-grade polyester film designed to be fully recyclable, addressing growing environmental concerns in healthcare packaging. This innovative film maintains necessary medical-grade performance characteristics such as biocompatibility and sterilization compatibility while meeting recycling standards to reduce plastic waste. This solution supports the circular economy by enabling easy reintegration of medical polyester waste into production cycles without compromising material quality or safety.

- In June 2025, Dhunseri Poly Films invested INR 1000 crore to establish two new polyester film manufacturing units in the Panagarh Industrial Park, West Bengal. The expansion includes a greenfield facility for producing BoPET (biaxially oriented polyethylene terephthalate) and another for BOPP (biaxially oriented polypropylene) films, both widely used in packaging. This move supports Dhunseri’s growth strategy in the high-demand plastics packaging sector.

- In May 2025, Pelsan Tekstil announced plans to build a manufacturing plant in the United States dedicated to producing breathable films used in hygiene and medical products. The new facility aims to meet increasing demand for high-performance, breathable materials that provide comfort while maintaining barrier protection. This strategic expansion will enhance Pelsan Tekstil’s global production capacity and market presence, supporting growth in the healthcare and hygiene sectors.

Companies Covered in Polyester Medical Films Market

- Toray Industries, Inc.

- Tekra Corporation

- Mitsubishi Chemicals Holdings Corporation

- DuPont

- 3M

- Cosmo Films Limited

- Filmquest Group Inc.

- Grafix Plastics

- DUNMORE Corporation

- Flex Films USA Inc.

- Coveme spa

- Tekni-Plex

- FUTAMURA CHEMICAL CO., LTD.

- Merck KGaA

- Uflex Limited

- Amcor plc

Frequently Asked Questions

The global polyester medical films market is projected to reach US$ 1.7 billion in 2025.

Rising prevalence of chronic diseases and medical technology advancements, including tissue engineering, are driving the market.

The market is poised to witness a CAGR of 7.6% from 2025 to 2032.

Expansion in biosensor technologies offers significant potential, leveraging polyester's flexibility for wearable health monitoring devices.

Toray Industries, 3M, and DuPont are some of the leading players in this market.