- Plastics, Polymers & Resins

- Polyester Resin Dispersion Market

Polyester Resin Dispersion Market Size, Share, and Growth Forecast, 2026 - 2033

Polyester Resin Dispersion Market by Product Type (Thermosetting, Thermoplastic), Resin Category (Saturated, Unsaturated), Application (Coatings, Adhesives, Sealants), and Regional Analysis 2026 - 2033

Polyester Resin Dispersion Market Size and Trends Analysis

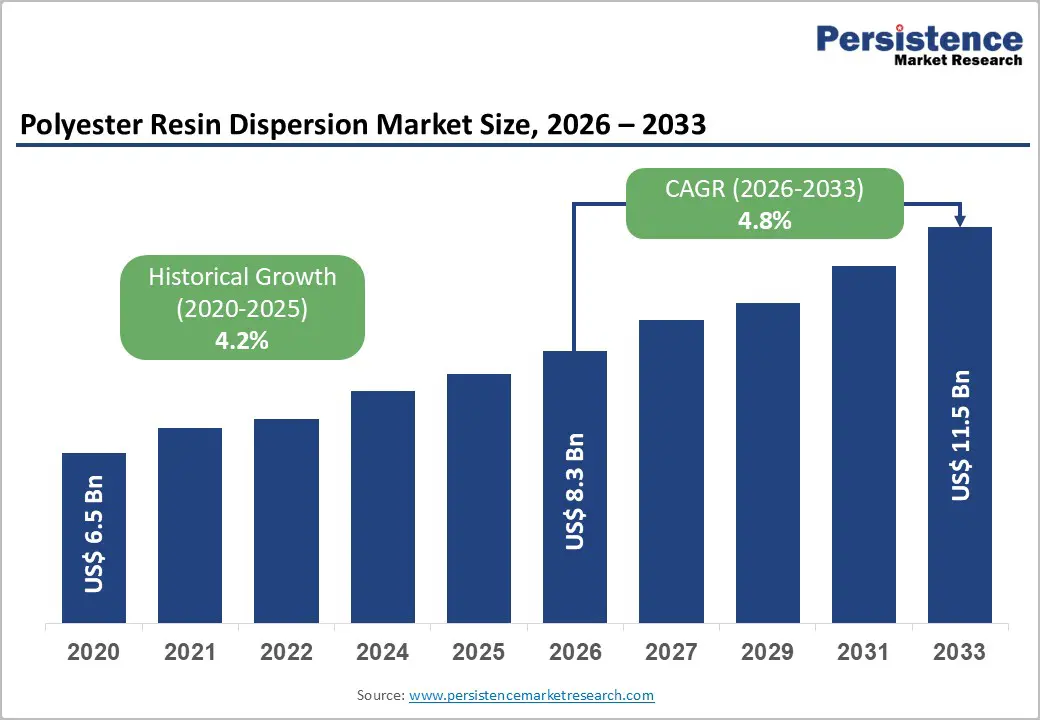

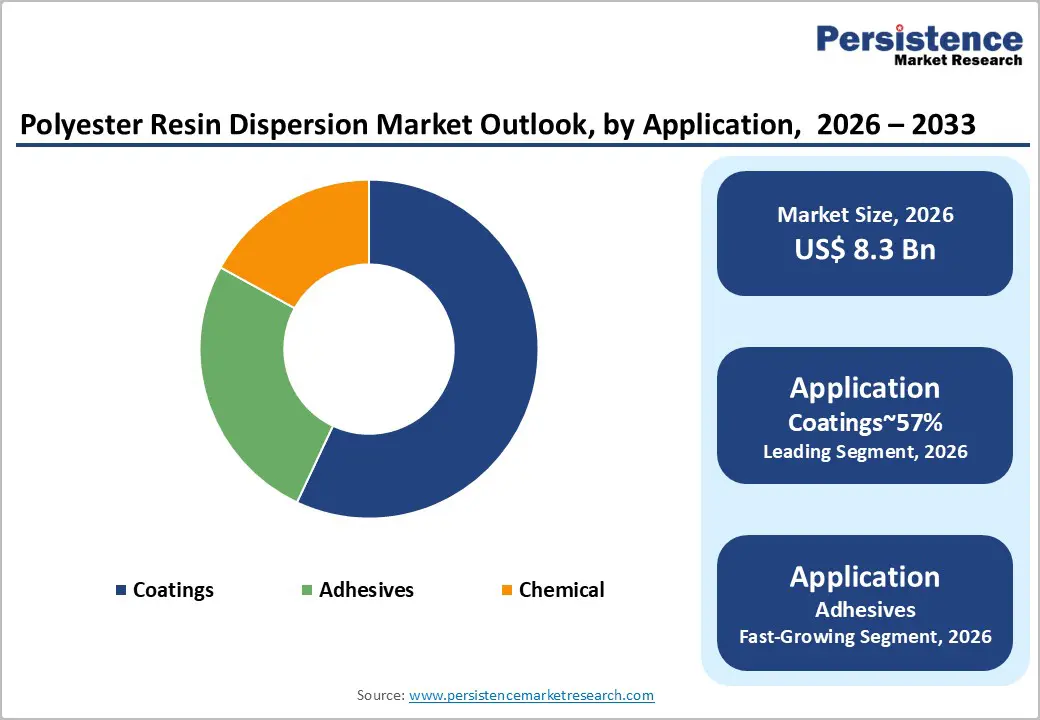

The global polyester resin dispersion market size is likely to be valued at US$8.3 billion in 2026 and is expected to reach US$11.5 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by the rapid transition from solvent-borne to water-borne systems to comply with stringent VOC emission standards.

The expanding footprint of the automotive and construction industries in emerging economies is also fueling the demand for high-performance, eco-friendly coating solutions. Technological innovations in hybrid resin formulations are also providing enhanced durability, positioning these dispersions as a critical component in sustainable industrial manufacturing.

Key Industry Highlights:

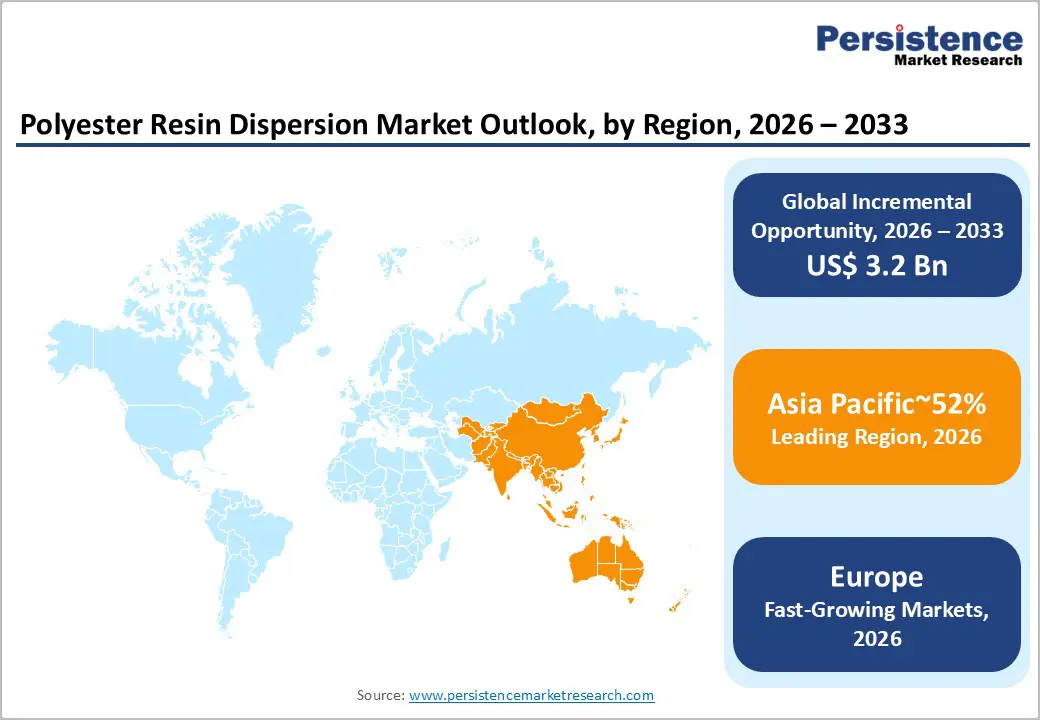

- Leading Region: Asia Pacific is projected to lead, accounting 52% of the global market share in 2026, due to large-scale manufacturing hubs in China, India, and Japan, and technology adoption in waterborne and thermosetting dispersions.

- Fastest-growing Region: Europe is anticipated to grow the fastest due to industrial innovation clusters, Green Deal regulatory support, and rising adoption across automotive, aerospace, and construction sectors.

- Leading Product Type: Thermosetting is expected to lead, accounting for approximately 66% share in 2026 through high industrial adoption, production throughput, quality, and applications in coatings and composite solutions.

- Leading Application: Coatings are projected to dominate for simplicity, cost efficiency, adoption, and functional use across key sectors, holding approximately 57% share in 2026.

| Key Insights | Details |

|---|---|

|

Polyester Resin Dispersion Market Size (2026E) |

US$8.3 Bn |

|

Market Value Forecast (2033F) |

US$11.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of the Electric Vehicle (EV) and Automotive Sector

The automotive sector’s structural shift toward electrification is reconfiguring material demand across coating value chains. Battery housings and power electronics require coatings delivering electrical insulation and thermal management stability. Polyester resin dispersions align with these specifications through strong substrate adhesion and electrolyte resistance. Their compatibility with metal and composite assemblies supports multi-material battery architectures. Regulatory emphasis on vehicle safety and fire performance further elevates functional coating requirements. As electrified platforms scale, OEM procurement frameworks increasingly prioritize performance-certified dispersion systems. This transition embeds specialty resin demand within evolving automotive material standards.

Rising electric vehicle output intensifies upstream demand for high-performance dispersion chemistries. Regional manufacturing hubs accelerate localized sourcing of automotive-grade coating intermediates. Supply chains adapt toward waterborne systems aligned with tightening emission compliance frameworks. This favors polyester dispersion technologies with lower volatile organic compound profiles. Value addition shifts toward formulation expertise and application-specific performance optimization. Margin structures increasingly reflect certification costs and advanced raw material inputs. Consequently, electrification structurally reinforces polyester resin dispersion consumption across automotive coatings.

Urbanization and Infrastructure Expansion Stimulate Protective Materials Demand

Accelerating urbanization is intensifying structural demand for advanced construction materials globally. Expanding infrastructure pipelines elevate requirements for durable coatings and sealants. Polyester resin dispersions provide chemical resistance and substrate compatibility in harsh environments. Their film-forming stability enhances long-term structural protection across civil assets. Regulatory tightening around building safety and environmental compliance reinforces waterborne dispersion adoption. Large-scale infrastructure investments in Asia Pacific strengthen regional consumption patterns. This dynamic embeds resin dispersions within construction-grade performance specifications.

Increased construction throughput expands downstream coatings and sealants integration. Developers prioritize lifecycle durability to moderate recurring maintenance expenditure burdens. Polyester dispersion systems support extended service intervals under aggressive weather exposure. Infrastructure modernization programs stimulate bulk procurement of compliant protective formulations. Environmental policy frameworks accelerate substitution away from solvent-intensive chemistries. Raw material sourcing and formulation efficiency influence margin resilience for suppliers. As urban density intensifies, demand stability improves across construction-linked resin applications.

Barrier Analysis – Competition from Bio-Based Resin Alternatives

The increasing adoption of bio-based resins is creating structural pressure on polyester resin dispersions. These alternatives offer superior sustainability credentials, including a lower carbon footprint and renewable feedstock utilization. Regulatory frameworks, particularly under the EU Green Deal, incentivize bio-resin incorporation in coatings and adhesives. Compliance requirements impose additional formulation and certification costs, reducing price competitiveness for conventional polyester dispersions. Customer procurement policies increasingly favor environmentally aligned chemistries, reshaping purchasing patterns across industrial and construction applications. This dynamic slows penetration of traditional dispersions in markets where green mandates are strictly enforced.

Cost premiums associated with bio-resin integration directly constrain broader polyester adoption. Premium pricing pressures limit uptake in price-sensitive segments such as adhesives and mid-tier coatings. Performance differentiation challenges arise when sustainability-driven choices override conventional material advantages such as chemical resistance and substrate adhesion. Investment in compliance, sourcing, and formulation adaptation further compresses supplier margins. Conventional polyester resin dispersions eventually face heightened substitution risk, reducing volumetric growth and reshaping competitive dynamics in regulated regions.

Technical Performance Limitations in Extreme Conditions

Water-borne polyester resin dispersions exhibit inherent technical constraints under extreme environmental conditions. Shelf-life stability can degrade during prolonged storage, while repeated freeze-thaw cycles compromise emulsion integrity. High-humidity environments further slow curing kinetics, reducing film formation uniformity and adhesion performance. These limitations restrict application in demanding marine, offshore, and industrial sectors where operational reliability is critical. Solvent-based alternatives continue to provide superior mechanical and chemical resilience, maintaining preference in heavy-duty coating and sealant projects.

Such performance gaps constrain dispersion adoption in specialized high-stress environments. The technical deficiencies also influence formulation and logistics decisions. Manufacturers must invest in stabilizers, cold-chain handling, and accelerated curing additives to mitigate environmental sensitivity. Despite improvements, residual risk remains for coating failure under extreme conditions, limiting market confidence. Cost structures rise due to additional material inputs and handling protocols, creating margin pressure. As a result, high-performance industrial applications continue to favor solvent-based chemistries, reinforcing competitive barriers for water-borne polyester resin dispersions.

Opportunity Analysis – Technological Convergence in Composites

The integration of UV-curable polyester resin dispersions is expanding applications across high-performance composite markets. Radiation-cured technologies provide rapid film formation, precise crosslinking, and high electrical insulation, enabling their use in advanced electronics and lightweight aerospace components. These dispersions meet stringent thermal and mechanical requirements while supporting faster production cycles compared to conventional curing methods. Strategic partnerships accelerate technology adoption, addressing unmet material performance needs in sectors where weight reduction and operational reliability are critical. This convergence strengthens the role of specialty dispersions within composite manufacturing and functional coatings.

Industry adoption is reinforced by regulatory and process efficiencies, including reduced energy consumption and lower volatile organic compound emissions. Formulation development focuses on balancing curing speed, substrate compatibility, and end-use durability. Supply chain alignment with composite fabricators and electronics manufacturers supports scalable deployment. As aerospace and electronics sectors increasingly demand lightweight, high-performance materials, UV and radiation-curable polyester dispersions capture structurally growing application opportunities, integrating technology evolution with market expansion dynamics.

Sustainable Formulation Innovations

Policy-driven incentives are structurally enhancing the market for environmentally compliant polyester resin dispersions. Frameworks such as the US Inflation Reduction Act allocate substantial funding to support green material adoption across industrial and construction sectors. Waterborne thermosetting dispersions benefit from these policies, enabling reduced volatile organic compound emissions and alignment with evolving environmental standards. Bio-derived feedstocks further improve regulatory compliance and sustainability profiles, positioning formulations to meet both corporate ESG goals and sector-specific chemical performance requirements. This policy environment catalyzes broader adoption of renewable and low-emission dispersion technologies.

Formulation innovations focus on integrating bio-based polyols and diacids while maintaining thermal, mechanical, and adhesion performance. Transitioning to waterborne systems addresses VOC restrictions without compromising application versatility across coatings, adhesives, and sealants. Cost and margin considerations reflect the balance between green feedstock sourcing and performance optimization. Collectively, these dynamics establish a structurally scalable opportunity for sustainable polyester dispersions in regulated and environmentally conscious markets.

Category-wise Analysis

Product Type Insights

Thermosetting is anticipated to dominate, accounting for approximately 66% share in 2026, underpinned by their entrenched role in high-performance coatings and composite applications across automotive, construction, and industrial machinery segments. Adoption remains anchored by superior thermal stability, chemical resistance, and cross-linking durability, with manufacturers prioritizing operational reliability and long-term performance in high-volume OEM environments. Ongoing platform evolution, including UV-curable and waterborne thermosetting formulations, continues to reinforce replacement cycles and utilization intensity. Key brands such as BASF, Arkema, and Dow Chemicals, and their portfolio ecosystems, provide validated high-performance solutions, locking in enterprise workflows and sustaining premium adoption.

Thermoplastic is expected to be the fastest-growing segment, driven by emerging demand for recyclable and re-processable materials across packaging, consumer electronics, and adhesives applications. Growth is being catalyzed by technological advancements enabling intricate processing, flexible bonding, and lightweight component integration, which materially improve production efficiency and material circularity. Accelerating adoption is supported by formulation innovations and compatibility with sustainable production workflows, lowering operational friction for first-time industrial adopters. Brands such as Evonik, Arkema, and Allnex are introducing new thermoplastic platforms to capture early-cycle demand and embed switching advantages. Flexibility and sustainability increasingly dictate procurement strategies; thermoplastic dispersions are poised to outpace the overall market.

Application Insights

Coatings are expected to lead, accounting for approximately 57% share in 2026, underpinned by its entrenched role in architectural, automotive, and industrial applications. Adoption remains anchored by high-strength formulations, durability, and film-forming reliability, with manufacturers prioritizing volume efficiency and long-term substrate protection across high-demand sectors. Ongoing platform evolution, including waterborne and UV-curable coating systems, continues to reinforce replacement cycles and utilization intensity. Key brands such as PPG, Sherwin-Williams, and AkzoNobel, and their product ecosystems, provide validated high-performance solutions, locking in enterprise workflows and sustaining premium adoption. This combination of mature supply chains, consistent demand, and performance reliability solidifies the coatings segment’s dominance within structured deployment models.

Adhesives are projected to be the fastest-growing segment, driven by emerging demand for lightweight, high-strength bonding across automotive, aerospace, and electronics assembly applications. Growth is being catalyzed by technological advancements enabling flexible, durable, and chemically resistant adhesive formulations, which materially improve fuel efficiency and production efficiency. Accelerating adoption is supported by process integration, advanced application tools, and formulation innovations, lowering operational friction for first-time adopters. Brands such as 3M, H.B. Fuller, and Sika are introducing new polyester-based adhesive platforms to capture early-cycle demand and embed switching advantages. As lightweighting and multi-material assembly increasingly dictate industrial practices, adhesive dispersions are poised to outpace overall market growth over the forecast period.

Regional Insights

Asia Pacific Polyester Resin Dispersion Market Trends

Asia Pacific is anticipated to remain the dominating region, accounting for approximately 52% of the global share in 2026, supported by a structurally deep manufacturing ecosystem spanning China, India, Japan, and ASEAN countries. Adoption is anchored by large-scale urbanization, government-led infrastructure expansion, and cost-efficient production models, with enterprises prioritizing high-throughput operations and waterborne coating technologies. Technological evolution toward low-VOC dispersions, coupled with advanced formulation capabilities, reinforces regional demand intensity and platform utilization. The combination of competitive industrial networks, scalable manufacturing capacity, and policy-aligned infrastructure investments sustains Asia Pacific’s dominance, enabling rapid deployment of thermosetting and thermoplastic dispersions across coatings, adhesives, and sealant applications while embedding enterprise workflow advantages for leading suppliers.

China serves as the regional anchor, shaping momentum through accelerated industrial expansion, regulatory enforcement, and investment inflows. National initiatives such as the “New Infrastructure” plan and stringent VOC compliance audits drive widespread adoption of waterborne dispersions in automotive, construction, and industrial coatings. Supplier strategies emphasize localized formulation innovation, joint ventures, and integration of thermoplastic and high-performance thermosetting platforms to meet evolving application needs. Forward-looking deployment is expected to intensify as urbanization, manufacturing scaling, and infrastructure modernization programs expand, solidifying China’s role in anchoring Asia Pacific’s market leadership while reinforcing technology adoption across the regional industrial ecosystem.

Europe Polyester Resin Dispersion Market Trends

Europe is expected to register the fastest growth trajectory, driven by innovation-intensive industrial clusters and rising adoption in automotive, aerospace, and construction applications. Adoption is catalyzed by the transition to high-performance waterborne and UV-curable dispersions, aligned with sustainability and carbon-neutrality mandates under the European Green Deal. Technological evolution in thermosetting and bio-based resin formulations, coupled with advanced application capabilities such as powder coatings and precision curing, materially enhances performance, throughput, and operational efficiency. The competitive landscape remains moderately fragmented, with top players including BASF, Evonik, and Covestro advancing platform adoption and reinforcing early-cycle market capture.

Germany anchors regional momentum by driving industrial-scale deployment of high-tech polyester dispersions through concentrated R&D investments, automotive and aerospace production, and infrastructure modernization programs. Supplier strategies focus on localized production, UV- and waterborne technology adoption, and integration of bio-based dispersions to meet emerging carbon reduction targets. Forward-looking deployment is expected to intensify as Germany sustains output expansion, technology adoption, and industrial scaling, reinforcing Europe’s position as the primary growth engine for advanced polyester resin dispersions.

North America Polyester Resin Dispersion Market Trends

North America is expected to remain a mature and structurally stable market, underpinned by a strong industrial base, advanced regulatory oversight, and established specialty chemical infrastructure. Adoption is anchored in high-value applications, including medical-grade adhesives, electronics coatings, and automotive topcoats, with enterprises prioritizing operational reliability, compliance readiness, and material performance. Technology evolution toward waterborne dispersions and low-VOC formulations continues to reinforce replacement cycles and workflow integration, while consolidated supplier networks ensure predictable supply and scale economics. The combination of mature manufacturing, regulatory alignment, and enterprise-grade platform adoption sustains the region’s market stability and high-value orientation.

The U.S. serves as the regional anchor, shaping market momentum through automotive production, semiconductor manufacturing incentives, and environmental regulation. National initiatives such as “Buy American” provisions and EPA VOC compliance programs drive adoption of ultra-pure and waterborne polyester dispersions, particularly in EV and electronics applications. Supplier strategies emphasize localized production, R&D investments, and high-performance thermosetting and thermoplastic platform deployment. Forward-looking demand is expected to remain resilient as automotive lightweighting, green technology adoption, and industrial innovation continue to reinforce North America’s mature and high-value positioning in the global market.

Competitive Landscape

The polyester resin dispersion market is moderately consolidated, with the top five players, including Allnex, BASF, and Arkema, controlling approximately 40–45% of total revenue, reflecting a balance between global platform dominance and regional specialization. Leading companies influence technology standards through waterborne and thermosetting innovations, shaping procurement preferences and enabling adoption in high-volume coating applications, while establishing credibility in regulatory compliance and performance consistency across industrial workflows. Competitive positioning is characterized by horizontal and vertical differentiation, with multinational corporations focusing on high-volume coatings, and regional or specialized suppliers addressing niche adhesives and sealant segments. Leaders leverage innovation in waterborne dispersions, platform integration, and technical support services to maintain adoption across diverse end-use industries.

Key Industry Developments:

- In February 2026, Arkema showcased Elium® recyclable thermoplastic resins at JEC World 2026 for boat hull circularity. Demonstrates a shift toward "circular composites" where polyester-like performance is met with full recyclability for the marine and wind sectors.

- In January 2026, Covestro highlighted Decovery® CQ 8411, a 30% bio-based binder for low-VOC wall paints. This water-based binder eliminates the need for additional co-solvents, directly addressing consumer demand for improved indoor air quality and sustainability.

- In August 2025, Allnex launched SETALUX® 57-1612, a versatile acrylic resin for 2.1 VOC industrial coatings. Offers a "toolbox" solution for manufacturers to meet strict VOC regulations while maintaining fast-dry performance in industrial settings.

Companies Covered in Polyester Resin Dispersion Market

- Covestro AG

- Allnex GMBH

- BASF SE

- Arkema S.A.

- Mitsubishi Chemical Group

- DIC Corporation

- Eternal Materials Co. Ltd.

- LG Chem

- Dow Chemical

- Eastman Chemical Company

- PPG Industries

- Huntsman

- Hexion

- Ashland

- Solvay

- DSM

Frequently Asked Questions

The global polyester resin dispersion market is projected to be valued at US$8.3 billion in 2026 and is expected to reach US$11.5 billion by 2033, driven by the transition from solvent-borne to water-borne systems, increasing adoption in automotive, construction, and industrial coatings, and the rising demand for sustainable and high-performance resin formulations.

The shift toward electric vehicles is reshaping material requirements across coatings and adhesives, with polyester dispersions providing strong substrate adhesion, thermal stability, and electrolyte resistance for battery housings, power electronics, and lightweight multi-material assemblies, enabling OEMs to meet stringent safety and performance standards while supporting electrification initiatives.

The polyester resin dispersion market is forecast to grow at a CAGR of 4.8% from 2026 to 2033, reflecting sustained demand from automotive electrification, infrastructure expansion, and regulatory-driven adoption of waterborne and low-VOC coating technologies.

Asia Pacific is the leading regional market, accounting for approximately 52% share, anchored by large-scale manufacturing in China, India, and Japan, rapid urbanization, infrastructure expansion, and high adoption of waterborne and thermosetting dispersion technologies across coatings, adhesives, and sealants.

The polyester resin dispersion market is moderately consolidated, with key players including BASF SE, Arkema S.A., Allnex GMBH, Covestro AG, Mitsubishi Chemical Group, DIC Corporation, Eternal Materials Co. Ltd., LG Chem, Dow Chemical, Eastman Chemical Company, PPG Industries, Huntsman, Hexion, Ashland, Solvay, and DSM. These companies compete through technology innovation, waterborne and thermosetting platform leadership, and integration into high-volume industrial and construction applications.