- Plastics, Polymers & Resins

- Polyester Fiber Market

Polyester Fiber Market Size, Share, and Growth Forecast, 2026 – 2033

Polyester Fiber Market by Product Type (Polyester Staple Fiber (PSF), Polyester Filament Yarn (PFY)), Application (Carpets and Rugs, Apparel, Others), and Regional Analysis for 2026 – 2033

Polyester Fiber Market Size and Trends Analysis

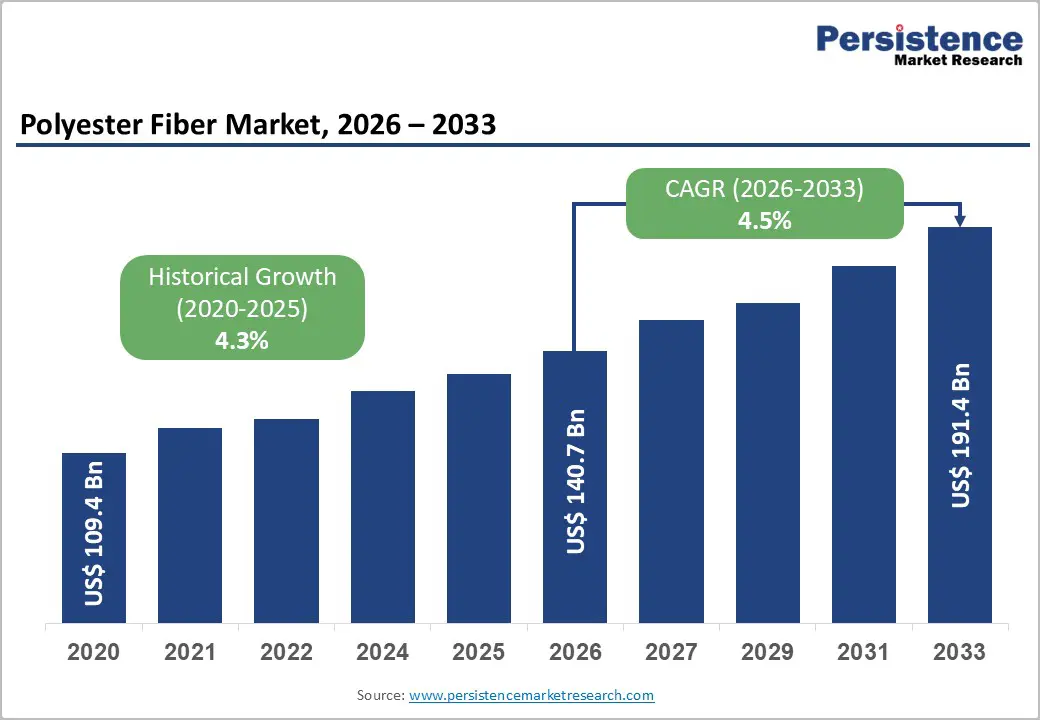

The global polyester fiber market size is likely to be valued at US$140.7 billion in 2026 and is expected to reach US$191.4 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by robust and sustained demand from the textile and apparel sectors, owing to polyester's durability, affordability, wrinkle resistance, and versatility.

The material's increasing use in non-woven fabrics, household textiles, automotive interiors, and industrial applications is contributing to this expansion. Factors such as rapid urbanization, population growth, and rising disposable incomes in emerging markets continue to boost consumption. The growing adoption of recycled polyester (rPET) also aligns with sustainability goals. Moreover, ongoing advancements in fiber technology, including high-tenacity, flame-retardant, and moisture-wicking polyester varieties, are expanding its application in performance apparel and technical textiles.

Key Industry Highlights:

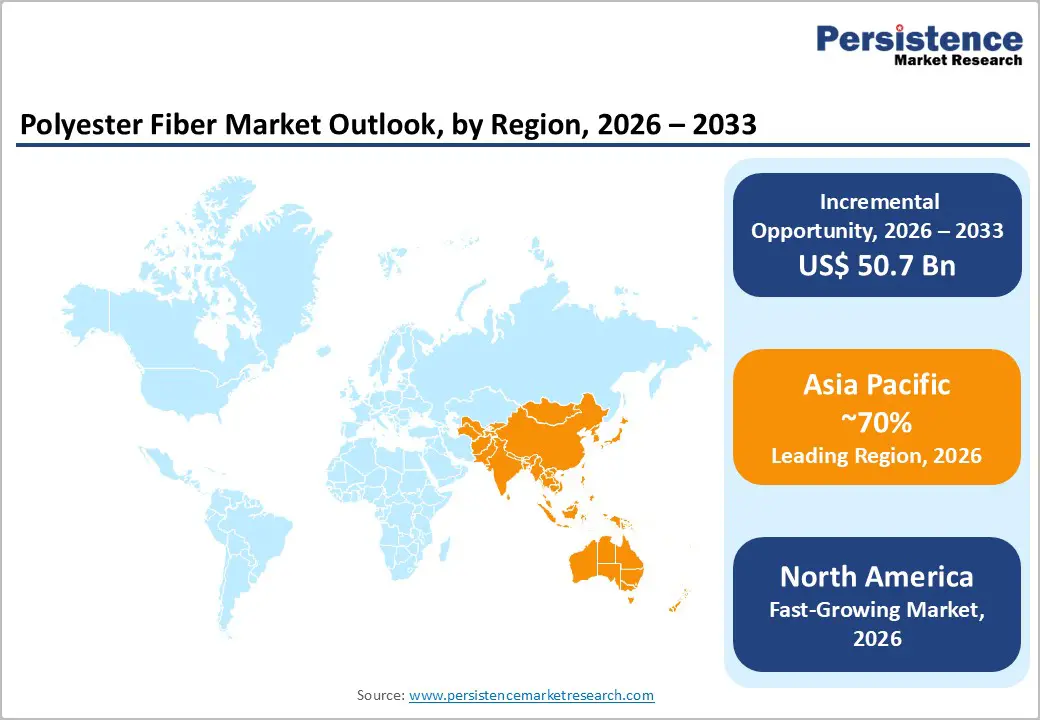

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 70% in 2026, driven by large-scale production capacity in China and India, cost-efficient manufacturing, strong apparel demand, and increasing investments in recycling and capacity expansion.

- Fastest-growing Region: North America is likely to be the fastest-growing region in polyester fibers in 2026, supported by high-value applications, technical textiles, automotive demand, and a strong focus on recycled content and innovation.

- Leading Product Type: Polyester staple fiber (PSF) is projected to represent the leading product type in 2026, accounting for 60% of the revenue share, driven by its widespread use in apparel, home textiles, and non-woven fabrics.

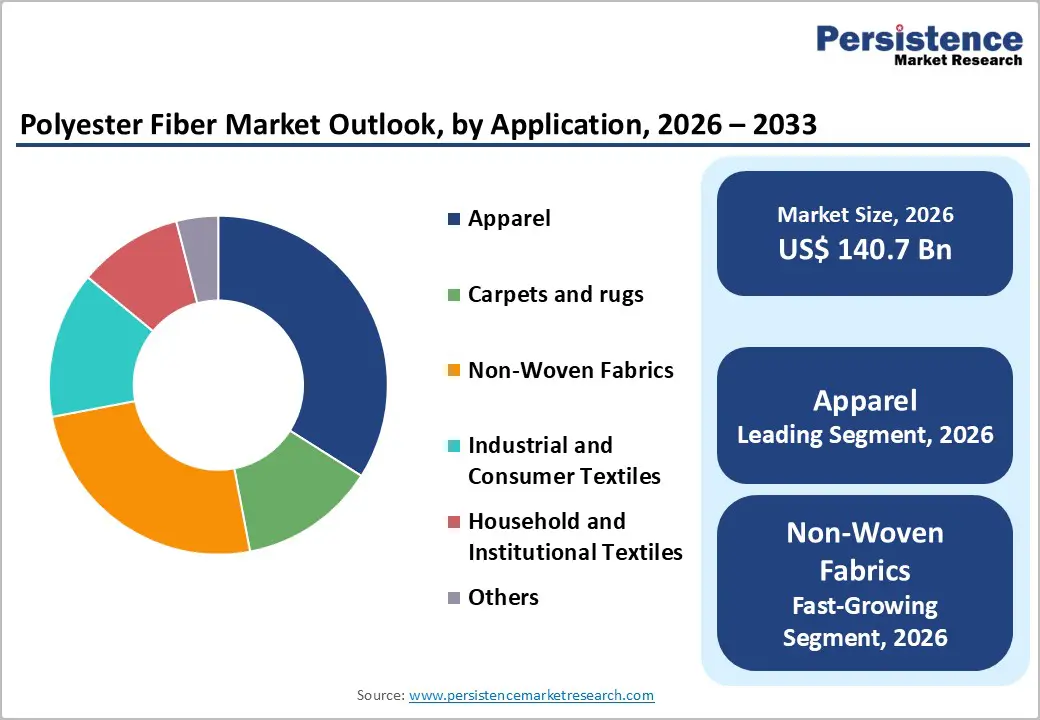

- Leading Application: The apparel segment is anticipated to be the leading application type, accounting for over 40% of the revenue share in 2026, supported by polyester’s durability, affordability, and popularity in fast fashion and sportswear.

| Key Insights | Details |

|---|---|

| Polyester Fiber Market Size (2026E) | US$ 140.7 Bn |

| Market Value Forecast (2033F) | US$ 191.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion in Textile and Apparel Demand

Polyester durability, wrinkle resistance, and cost-effectiveness make it the preferred choice for fast fashion, active wear, and mass-market clothing. Rising urbanization, population growth, and increasing disposable incomes in emerging economies are fueling higher consumption, particularly in China, India, and Southeast Asia. The ability to blend polyester with natural fibers such as cotton enhances fabric versatility, meeting evolving consumer preferences. The expansion of organized retail and e-commerce platforms also supports consistent demand, ensuring long-term growth for polyester fibers in apparel production.

The trend toward performance fabrics and sportswear has amplified polyester usage. Consumers increasingly prefer lightweight, quick-drying, and stretchable clothing, which polyester fibers efficiently provide. Innovations in yarn engineering, such as high-tenacity fibers, improve strength and elasticity, enhancing their appeal across casual, formal, and functional apparel segments. Globalization of fashion trends accelerates market penetration in emerging regions. Polyester's adaptability to various textile finishes and dyeing techniques strengthens its competitiveness. These factors create a self-reinforcing cycle of demand, ensuring polyester fibers remain a cornerstone of the textile and apparel industry.

Growth in Non-Woven and Industrial Applications

Non-woven fabrics for hygiene products, medical disposables, automotive interiors, and filtration materials increasingly utilize polyester due to its durability, tensile strength, and cost-effectiveness. The rise in healthcare awareness, automotive production, and industrial manufacturing has accelerated the adoption of polyester non-woven. In industrial textiles, polyester is preferred for ropes, geotextiles, conveyor belts, and filtration media. Its resistance to moisture, abrasion, and chemicals ensures reliability in demanding environments. Consequently, non-woven and industrial applications are becoming critical growth engines for polyester fibers.

The automotive sector, in particular, is increasing polyester adoption through seat covers, airbags, and insulation materials, aligning with lightweighting and fuel efficiency goals. Industrial uses in packaging, protective clothing, and construction textiles expand market opportunities. The shift toward hygiene and medical safety drives non-woven demand for masks, wipes, and disposable garments. This diversification reduces reliance on apparel alone and stabilizes revenues amid seasonal or fashion-related fluctuations. With increasing manufacturing capacities in Asia Pacific, these factors support sustained growth, reinforcing polyester fibers’ strategic importance across non-woven and industrial sectors.

Barrier Analysis - Environmental and Regulatory Concerns

Being a synthetic polymer derived from petrochemicals, polyester production contributes to carbon emissions and microplastic pollution. Governments and environmental bodies in North America, Europe, and parts of Asia are enforcing stricter regulations on synthetic fiber production, usage, and disposal. These policies may increase production costs and compliance requirements. Consumers’ growing preference for sustainable and eco-friendly textiles challenges conventional polyester. Rising awareness of microplastic contamination in water bodies has sparked industry-wide scrutiny, compelling manufacturers to adopt cleaner processes and consider recycled alternatives, which may require additional investment.

Environmental concerns also affect public perception and brand positioning. Fashion brands are increasingly emphasizing sustainability, pressuring suppliers to reduce virgin polyester usage and integrate recycled content. Extended producer responsibility (EPR) regulations, waste management mandates, and water treatment norms add operational complexity. Non-compliance risks fines, reputational damage, or restricted market access. Environmental and regulatory constraints act as both operational and strategic hurdles, slowing growth compared to potential market demand. Companies must innovate in recycling, biodegradable alternatives, and low-impact production technologies to align with evolving environmental standards while maintaining competitiveness.

Competition from Alternative Fibers and Substitutes

Polyester fibers face growing competition from alternative synthetic fibers, natural fibers, and emerging bio-based materials. Cotton, viscose, nylon, and other synthetics offer eco-friendly or performance-based advantages that attract both manufacturers and consumers. Bio-based and biodegradable fibers are gaining attention due to environmental concerns, potentially reducing polyester’s market share. Price fluctuations in raw materials also make polyester vulnerable compared to low-cost alternatives. This intensifies market competition, compelling polyester producers to innovate or diversify product offerings to maintain relevance in both apparel and technical textile applications.

Substitutes also appeal to premium fashion segments that emphasize sustainability and comfort. Blended fabrics combining natural fibers with recycled synthetics are increasingly preferred. Technical textiles, such as moisture-wicking and high-strength fabrics, are sometimes dominated by nylon, aramid, or polypropylene fibers due to specific performance requirements. Polyester manufacturers face both pricing and performance pressures. Investment in advanced fibers, functional finishes, and recycled content becomes necessary to counteract these threats.

Opportunity Analysis - Technological Advancements in Recycling

Recycled polyester (rPET) derived from post-consumer PET bottles or textile waste reduces environmental impact, aligns with sustainability trends, and meets increasing regulatory requirements. Manufacturers are investing in chemical and mechanical recycling technologies to produce high-quality fibers comparable to virgin polyester. rPET adoption is growing in apparel, home textiles, and non-woven applications. Recycling not only addresses waste management concerns but also attracts eco-conscious consumers, enabling brands to position products as sustainable while maintaining cost competitiveness.

Chemical recycling innovations, such as depolymerization and purification, allow polyester fibers to be regenerated without quality loss, enabling closed-loop circularity. Mechanical recycling, though limited in fiber length, complements large-scale production for less critical applications. Adoption of recycled polyester (rPET) also benefits manufacturers by stabilizing raw material costs against crude oil price volatility. Partnerships between brands, recyclers, and fiber producers facilitate steady rPET supply and market penetration.

Diversification into Technical Textiles

Technical textiles, including automotive fabrics, industrial textiles, geotextiles, protective clothing, and filtration media, require high-performance fibers with superior strength, durability, and specialized properties. Polyester adaptability and high tensile strength make it ideal for these applications. Manufacturers can leverage this diversification to reduce dependence on apparel markets, which are subject to seasonal trends and fashion cycles. Expansion into technical textiles allows for higher value-addition, long-term contracts, and market penetration, especially in industrially advanced regions such as North America, Europe, and Asia Pacific.

The technical textiles sector also benefits from increased urbanization, infrastructure development, and automotive production worldwide. Polyester fibers can be engineered to meet specific requirements, including flame retardancy, UV resistance, and moisture management, enhancing their suitability for industrial and safety applications. Collaboration with automotive and construction companies accelerates adoption in high-performance applications. Governments encourage technical textile adoption through infrastructure and protective clothing standards.

Category-wise Analysis

Product Type Insights

Polyester staple fibers (PSF) are expected to lead, accounting for approximately 60% of revenue share in 2026, driven by their versatility, durability, and cost-effectiveness, making them ideal for high-volume applications in apparel, home textiles, and non-woven fabrics. PSF can be easily blended with natural fibers such as cotton, wool, or viscose, enhancing fabric softness, breathability, and performance while reducing production costs. Its extensive use in spun yarns supports applications across mass-market clothing and household textiles such as bed linens, curtains, and upholstery. For example, Reliance Industries Limited in India, which produces PSF extensively for domestic and export markets, supplies high-quality fibers for apparel brands and home furnishing manufacturers.

Polyester filament yarn (PFY) is likely to represent the fastest-growing segment, supported by its superior tensile strength, smooth texture, and suitability for continuous filament applications in both apparel and industrial textiles. PFY enables high-speed weaving and knitting, supporting production efficiency and premium fabric quality. The segment is particularly gaining traction in technical textile applications, such as automotive seat covers, industrial belting, and geotextiles, where durability and performance are critical. For example, Toray Industries Inc. leverages PFY in high-performance fabrics for both sportswear and automotive interiors, demonstrating its functional advantages over staple fibers.

Application Insights

Apparel is projected to lead the market, capturing around 40% of the revenue share in 2026, supported by its durability, affordability, wrinkle resistance, and versatility, making it a preferred fiber for fast fashion, sportswear, casual wear, and uniforms. Polyester’s ability to blend with cotton and other natural fibers enhances fabric aesthetics, comfort, and performance, meeting the demands of consumers for versatile clothing. For example, Indorama Ventures supplies polyester fibers to fashion brands that produce sportswear and mass-market clothing. The segment benefits from rising disposable incomes, urbanization, and growing demand in emerging economies, particularly in Asia Pacific.

Non-woven fabrics are expected to experience rapid growth in 2026, driven by rising demand in the hygiene, medical, and automotive sectors. This segment benefits from polyester's durability, lightweight nature, and versatility in specialized manufacturing processes. Disposable hygiene products such as surgical masks, wipes, and diapers rely on polyester non-woven fabrics for their strength and absorbency. Similarly, the automotive industry and filtration materials use these fibers for their performance and long-lasting qualities. For instance, Far Eastern New Century Corporation manufactures polyester non-woven fabrics for medical and industrial applications, catering to the increasing demand in Asia and North America.

Regional Insights

North America Polyester Fiber Market Trends

North America is likely to be the fastest-growing region, driven by strong demand for high-performance and sustainable textile solutions. The region’s established textile and manufacturing infrastructure supports significant polyester consumption across apparel, home furnishings, and industrial segments, with the U.S. accounting for a large portion of regional usage. There is a clear shift toward recycled polyester (rPET) as brands and manufacturers respond to sustainability trends and regulatory emphasis on circular economy models. Consumer preference for eco-friendly products is driving expanded integration of rPET in everyday fabrics, from casual wear to technical garments.

In North America, the use of polyester is growing across applications such as filtration, insulation, and composite materials, driving demand. A notable example is Unifi’s REPREVE recycled polyester initiative, which showcases how local manufacturers are leveraging sustainability while staying relevant in the industry. Unifi transforms post-consumer PET bottles into high-quality polyester yarn, which is then used by major brands such as Nike and Patagonia. This demonstrates the commercial success of recycled fibers in mainstream textile products. This trend highlights North America’s increasing investments in advanced recycling technologies and specialized polyester variants that align with evolving consumer demands for both performance and environmental responsibility.

Europe Polyester Fiber Market Trends

Europe is likely to be a significant market, due to stringent regulatory frameworks and growing consumer demand for eco-friendly textiles. Manufacturers are increasingly focusing on recycled polyester (rPET) integration to align with the European Union’s-circular economy action plan and extended producer responsibility mandates, which require brands and producers to reduce waste and enhance recyclability. European consumers are more environmentally conscious compared with other regions, propelling demand for sustainably produced fabrics in fashion, home furnishings, and automotive interiors.

Demand from automotive and industrial applications for durable, lightweight, and functional polyester fibers continues to grow, while fashion brands reinforce sustainability pledges through increased adoption of recycled content in apparel production. For example, corporate adaptation to these trends is Ahlstrom-Munksjö Oyj, a Finland-based fiber and nonwoven materials provider that emphasizes sustainable fiber solutions across Europe and beyond. Ahlstrom’s focus on renewable and recycled inputs highlights how European companies are integrating circularity into polyester fiber production and associated non-woven applications, including filters, automotive fabrics, and technical textiles.

Asia Pacific Polyester Fiber Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 70% in 2026, driven by rapid industrialization, large-scale textile production, and strong consumption growth in countries such as China and India. Polyester fibers are widely used in apparel, home textiles, and industrial applications due to their durability, versatility, and cost-effectiveness. China’s integrated production capacity and robust textile export sector bolster its leadership, while India’s expanding domestic market and government support for synthetic fiber manufacturing amplify regional demand.

Technological advancements in fiber manufacturing and automation also contribute to improved quality and production efficiency, enhancing competitiveness. For example, Indorama Ventures Public Company Limited, a major Asia Pacific producer that has expanded into sustainable polyester fiber supply chains by participating in multi-company initiatives to use renewable, bio-based, and CO2-derived materials in fiber production. This reflects the broader trend of integrating sustainability into polyester manufacturing, as downstream apparel brands seek lower-impact solutions without sacrificing performance.

Competitive Landscape

The global polyester fiber market exhibits a moderately fragmented structure, driven by the presence of numerous regional and international manufacturers competing on production capacity, product quality, price, and sustainability credentials. Major producers are spread across Asia, Europe, and the Americas, with China’s manufacturers alone accounting for a substantial portion of output thanks to integrated operations and cost advantages. Despite the large number of active firms, a handful of companies stand out due to their extensive production networks and broad distribution channels.

With key leaders including Indorama Ventures Public Company Limited, Reliance Industries Limited, Toray Industries Inc., Sinopec Yizheng Chemical Fibre Limited Liability Company, and Alpek Polyester, the competitive landscape is shaped by strategic initiatives that enhance market position. Companies compete through product innovation, such as the development of recycled and high-performance fibers, sustainability initiatives to meet environmental regulations, and strategic partnerships or acquisitions to secure raw material supply and enter new geographies.

Key Industry Developments:

- In October 2025, Toray Industries launched its Toray Premium GOUSEN select series, featuring four high-performance fibers: GIGADULL (for opacity, sun protection, and sweat stain resistance), SPRINGFIT (eco-friendly stretch fiber), QUUP (enhancing comfort), and Light gram (ultra-fine, lightweight nylon). As Japan’s sole producer of polyester, nylon, and acrylic, Toray aims to expand global marketing of these advanced fibers, showcasing Japan's tech leadership in textiles.

- In July 2025, Loop Industries unveiled Twist™, a circular polyester resin made entirely from textile waste. Using patented depolymerization technology, Twist™ turns polyester waste into virgin-quality resin, free from dyes and contaminants. The process ensures full traceability and supports the fashion industry's shift toward a circular economy.

- In December 2025, KIPAS Textiles launched fibR-e, a recycling platform to address polyester waste and enable circularity in fashion. The platform converts post-consumer garments with 70%+ polyester into GRS-certified rTEX Chips, which are then turned into yarns and fibers for new collections. Using patented molecular recycling, fibR-e ensures repeated, quality-preserving recycling without microplastic generation.

Companies Covered in Polyester Fiber Market

- Reliance Industries Limited

- Indorama Ventures Public Company Limited

- Toray Industries Inc.

- Sinopec Yizheng Chemical Fibre Limited Liability Company

- Green Group S.A.

- Alpek Polyester

- Zhejiang Hengyi Group Co., Ltd

- Nan Ya Plastics Corporation

- Far Eastern New Century Corporation

- Green Group SA

- Sarla Performance Fibers Limited

- Märkische Faser GmbH

- Tongkun Holding Group

- Huvis Corp.

- Teijin Limited

Frequently Asked Questions

The global polyester fibers market is projected to reach US$140.7 billion in 2026.

The polyester fibers market is driven by strong demand from the textile and apparel industry due to polyester’s durability, affordability, and versatility.

The polyester fiber market is expected to grow at a CAGR of 4.5% from 2026 to 2033.

Key market opportunities in polyester fibers lie in technological advancements in recycling and diversification into technical and high-performance textiles.

Reliance Industries Limited, Indorama Ventures Public Company Limited, Toray Industries Inc., and Sinopec Yizheng Chemical Fibre are the leading players.