- Home Appliances

- Laptop Cooling Pad Market

Laptop Cooling Pad Market Size, Share, and Growth Forecast, 2025 - 2032

Laptop Cooling Pad Market By Product Type (Active Cooling Pad, Passive Cooling Pad, Others), Material Type (Metal, Plastic, Others), Distribution Channel, and Regional Analysis for 2025 - 2032

Laptop Cooling Pad Market Size and Trends Analysis

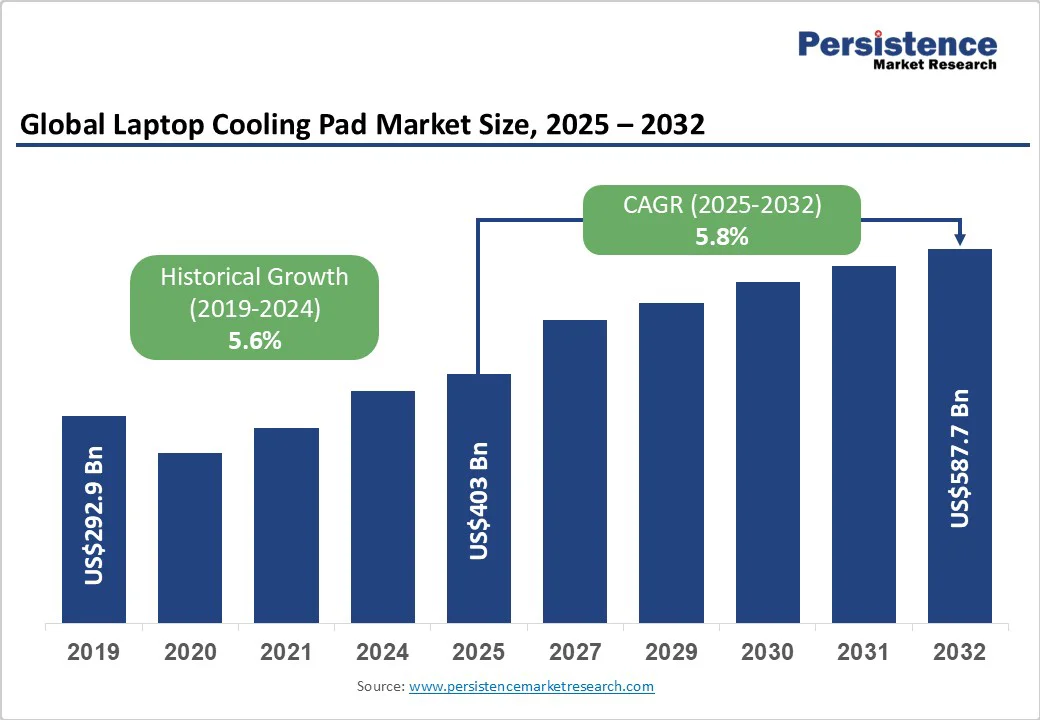

The global laptop cooling pad market size is likely to be valued at US$403 Million in 2025 and is expected to reach US$587.7 Million by 2032, growing at a CAGR of 5.8% during the forecast period from 2025 to 2032, driven by an expanding base of high-performance laptops (such as gaming and creator-class devices), increased adoption of accessories due to remote work trends, and improved e-commerce distribution, which lowers barriers related to pricing and availability.

Product innovation, multi-fan arrays, hybrid ergonomic stands, and telemetry have shifted consumer preference toward premium, higher-average selling price stock keeping units (ASP SKUs). The market consists of a few strong global brands operating in premium channels, alongside a broad range of regional and private-label manufacturers competing primarily on price.

Key Industry Highlights

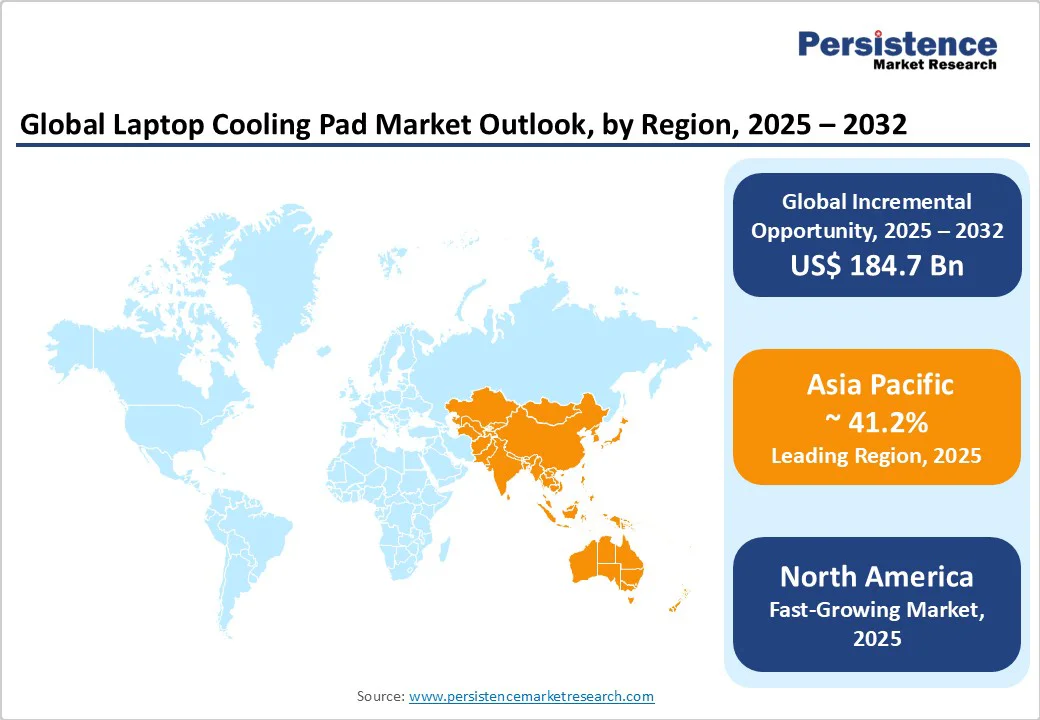

- Leading Region: Asia Pacific commands approximately 41.2% of the global market share (2025), driven by high laptop penetration, strong local manufacturing capacity in China and Japan, and the rapid expansion of gaming and e-learning ecosystems.

- Fastest-growing Region: North America, fueled by premium product adoption in the U.S., expansion of remote work setups, and technological advancements such as smart and noise-optimized cooling solutions.

- Investment Plans: Major brands including Cooler Master, DeepCool, and Thermaltake are investing in localized production units, ergonomic innovation, and eco-friendly materials, with regional expansions into India, Germany, and the U.S. The 2024–2032 investment cycle emphasizes AI-controlled fan systems and recycled composite materials, aligning with ESG goals.

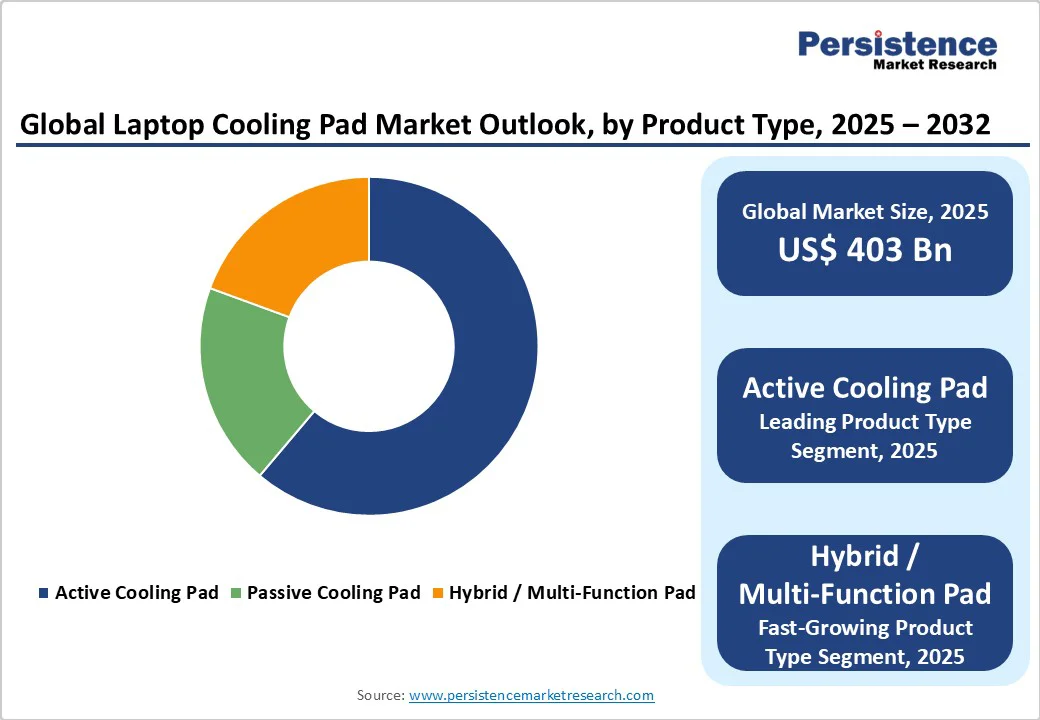

- Dominant Product Type: Active cooling pads hold approximately 62.4% of the market share in 2025, led by gamer-focused designs integrating multi-fan arrays, RGB lighting, and adjustable RPM control systems.

- Leading Material Type: Metal cooling pads represent about 52.2% of total market revenue in 2025, attributed to superior thermal conductivity, durability, and widespread adoption in premium laptop accessories.

| Key Insights | Details |

|---|---|

|

Laptop Cooling Pad Market Size (2025E) |

US$403 Mn |

|

Market Value Forecast (2032F) |

US$587.7 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of High-Performance Laptop Segments and Thermal Requirements

The steady rise in gaming laptops, mobile workstations, and high-TDP consumer laptops has created a persistent need for supplemental cooling to avoid thermal throttling and to extend component life. As CPU and GPU power envelopes increased, users, especially gamers and creative professionals, have been more likely to purchase auxiliary cooling solutions. This structural demand underpins steady market expansion and supports higher ASPs for active and hybrid pads that demonstrably mitigate temperature rise.

E-Commerce Proliferation and Improved Market Access

Online marketplaces and direct-to-consumer channels have broadened distribution reach for both established brands and small OEMs. Lower distribution friction and faster product launches enable more SKUs to reach global buyers, expanding the addressable market. Online customer reviews and independent performance tests have also accelerated product discovery and purchase conversion, particularly in developed e-commerce markets.

Product Innovation and Feature Convergence

Manufacturers have migrated from basic fan-only pads to integrated solutions that combine active cooling with ergonomic stands, USB hubs, battery pass-throughs, and software fan control. These value-added features justify premium pricing tiers and foster brand differentiation. As a result, the premium segment grows faster than commodity low-end pads.

Commoditization and Margin Pressure at the Low End

A large share of unit volume is produced by low-cost manufacturers supplying sub-US$20 pads. This commoditization compresses margins across the industry, limits reinvestment in R&D, and raises price sensitivity among many buyer cohorts. For firms focused on scale, margin erosion constrains long-term innovation capability.

Variable Product Efficacy and Customer Skepticism

Independent testing highlights wide variance in real-world cooling performance across models. Many mass-market pads provide only marginal thermal benefit for modern laptop chassis with different venting designs. Where end users perceive limited effectiveness, purchase frequency and willingness to pay decline. Vendors must therefore substantiate thermal gains through third-party testing and clear performance benchmarks to maintain consumer trust.

Premiumization and Higher-Value Product Tiers

Premium multi-fan aluminum pads with firmware control and ergonomic design represent a clear growth opportunity. If premium share expands modestly, manufacturers can capture significant incremental revenue, as premium ASPs materially exceed commodity levels. Brands able to demonstrate thermal performance, quiet operation, and durable construction will capture disproportionate value.

Geographic Expansion in Asia Pacific and India

Asia Pacific combines the largest laptop installed base, expanding gaming and creator communities, and strong local manufacturing. Targeted localization, country-specific marketing, local warranties, and optimized logistics can convert volume potential into market share. India in particular represents a high-volume growth market for both budget and mid-tier SKUs as remote work and gaming adoption grow.

B2B Channels and OEM Co-Branding

Bundling cooling pads with laptop purchases, offering accessory attachments as part of corporate procurement packages, and forming OEM co-branding partnerships provide stable sales channels and reduce direct customer acquisition costs. Capturing a modest share of enterprise refresh cycles or OEM bundle programs can create recurring revenue and higher lifetime value.

Category-wise Analysis

Product Type Analysis

Active cooling pads, equipped with integrated fans, represent the dominant product type, accounting for over 62.4% of the global market value in 2025. Their popularity stems from their superior heat dissipation capability and compatibility with performance laptops used by gamers, video editors, and data scientists. Models featuring multi-fan arrays (typically 2 to 6 fans) and adjustable RPM controls are most prevalent. Brands such as Cooler Master (U3 Plus) and Thermaltake (Massive Series) lead this segment, offering enhanced airflow design, customizable RGB lighting, and noise-optimized bearings. The rising trend of gaming tournaments, particularly across Asia Pacific and North America, is further sustaining demand for these high-performance cooling systems. With more consumers owning high-TDP laptops exceeding 90 W, the need for active thermal management continues to grow.

The hybrid cooling pad segment is projected to record the fastest CAGR between 2025 and 2032, reflecting a market shift toward multifunctional accessories. These products combine active cooling mechanisms with ergonomic elevation stands, integrated USB hubs, and even wireless charging ports. Hybrid pads appeal strongly to professionals and digital nomads seeking multi-utility setups for long-duration laptop use. For instance, Havit’s RGB Cooling Stand and TopMate C12 models integrate fan speed controls and USB passthroughs, supporting both performance and workspace organization.

Material Type Analysis

Metal-based cooling pads, primarily made from aluminum alloys, dominate the market with an estimated 52.2% revenue share in 2025. Aluminum offers superior thermal conductivity, significantly improving heat transfer efficiency compared with ABS plastic alternatives. Its durability, corrosion resistance, and premium aesthetic make it the material of choice for gaming and workstation-grade cooling pads. Leading manufacturers such as Zalman, DeepCool, and Cooler Master continue to use CNC-machined aluminum grids that maximize airflow while ensuring rigidity. For example, Cooler Master’s Notepal X150 features a full aluminum mesh surface coupled with 160 mm fans, effectively reducing laptop surface temperatures by 5-10°C.

The composite and eco-material segment is the fastest-growing segment, driven by the integration of thermally conductive polymers, carbon fiber blends, and recycled materials. This reflects a broader industry shift toward sustainable electronics manufacturing, spurred by environmental compliance initiatives such as the EU’s Circular Economy Action Plan and EPEAT standards. Brands are experimenting with bioplastics and graphene-infused composites to achieve comparable heat dissipation performance with lower environmental impact. For instance, startups in Japan and Germany have developed recycled ABS-polycarbonate cooling frames that reduce product weight by 20-25%. Such materials not only improve transport efficiency but also cater to eco-conscious consumers and organizations implementing green procurement policies.

Regional Insights

Asia Pacific Laptop Cooling Pad Market Trends - Manufacturing Powerhouse with eSports-Driven Growth

Asia Pacific is the largest regional market, holding approximately 41.2% of market share, reflecting its position as a global hub for laptop manufacturing and component sourcing. The region’s market leadership is attributed to the strong consumer base in China, India, Japan, and the ASEAN countries, where rising disposable income and digital adoption fuel consistent demand. China accounts for the highest production and domestic consumption, supported by a robust local manufacturing ecosystem in Guangdong and Zhejiang provinces, while India shows the fastest growth in shipments driven by affordable pricing and expanding digital education programs.

Japan and South Korea dominate the premium category, with consumers valuing high-performance, feature-rich cooling pads for gaming and creative workloads. Several macroeconomic trends underpin Asia Pacific’s growth. The region is witnessing a boom in eSports participation, with China’s gamer population exceeding 700 million, creating consistent demand for laptop accessories. Similarly, the expansion of remote work and online learning has made thermal accessories essential for device longevity in high-temperature climates. Local manufacturing advantages, including access to aluminum fabrication and fan motor components, enable competitive pricing and scalability.

Regulatory frameworks vary across countries: China enforces CCC product safety certification, while India’s Production Linked Incentive (PLI) scheme incentivizes local assembly of computer peripherals. These policies enhance regional manufacturing competitiveness and attract foreign investment.

North America Laptop Cooling Pad Market Trends - Premium Gaming Demand & Innovation-Driven Cooling Solutions

North America represents the fastest-growing market for laptop cooling pads due to high consumer purchasing power, mature e-commerce infrastructure, and strong demand for performance-oriented accessories. The U.S. dominates the regional landscape, contributing the majority of revenue due to its premium SKU adoption and innovation-driven product offerings. The ASP in the U.S. market remains among the highest globally, reflecting a strong preference for branded and feature-rich cooling solutions. Canada follows with steady growth supported by the expanding remote work culture and rising health awareness related to ergonomic workstation setups.

Growth across North America is largely driven by the gaming ecosystem, where laptops with high thermal loads have become common among both casual and professional gamers. According to the Entertainment Software Association (ESA), more than 210 million Americans play video games regularly, sustaining strong demand for cooling accessories. The work-from-home model has also intensified accessory adoption, as professionals seek devices that enhance laptop longevity and comfort during extended usage.

Regulatory oversight is stringent; compliance with UL and CSA safety certifications, along with clear warranty and labeling standards, is mandatory for large-scale retail and online distribution. Recent investments focus on silent fan technology, USB-C power integration, and direct-to-consumer marketing strategies. For example, Cooler Master introduced its “Notepal Flex” series in 2024, featuring adaptive thermal sensors, while U.S.-based startup Opolar expanded its direct online retail presence with upgraded high-RPM cooling stands. The U.S. continues to be the region’s innovation hub, attracting investments in smart accessories and IoT-enabled cooling devices that provide real-time temperature monitoring and AI-based fan control.

Europe Laptop Cooling Pad Market Trends - Eco-Friendly Designs & Ergonomic Compliance in Focus

Europe maintains a substantial market position, with a focus on ergonomic design, sustainability, and regulatory compliance. The region accounts for a meaningful share of the global laptop cooling pad market, driven by strong demand in Germany, the U.K., France, and Spain. Germany leads the region in both unit sales and value contribution, supported by a thriving gaming culture, a large base of creative professionals, and a preference for locally certified, durable accessories.

The U.K. also contributes significantly through online retail channels and commercial sales to hybrid workers, while France and Spain exhibit accelerating e-commerce-driven accessory adoption. Growth in Europe is sustained by stringent ergonomic standards and environmental awareness. Consumers increasingly prefer cooling pads designed with eco-friendly materials, energy-efficient fans, and recyclable packaging.

The region’s regulatory framework, governed by CE marking, RoHS, and WEEE directives, requires manufacturers to comply with product safety, restricted substances, and recyclability mandates. These regulations have led to greater investments in eco-design initiatives, closed-loop recycling programs, and partnerships with certified European retailers. For instance, Trust International (Netherlands) and Speedlink (Germany) have launched sustainable cooling pads using recycled plastics, while Zalman expanded its European distribution network with RoHS-compliant product lines in 2024.

Competitive Landscape

The global laptop cooling pad market is moderately fragmented. A small set of established global brands exert influence in premium channels while numerous regional OEMs and private-label suppliers command large unit volumes at the low end. No single vendor controls a dominant global share; market power concentrates in the premium segment among brand incumbents.

Dominant strategic themes include product differentiation through premium features, cost leadership at the low end, and market expansion via e-commerce and OEM partnerships. Leading players blend brand strength, R&D investment, and distribution scale to sustain ASPs while smaller suppliers compete on price and private-label contracts.

Key Industry Developments

- In January 2025, MSI unveiled its Titan 18 HX Dragon Edition Norse Myth gaming laptop at CES 2025. This high-end device features an illuminated touchpad, Intel's Core Arrow Lake processor, and Nvidia's RTX 50-series GPU, built specifically for extreme gaming performance. While the focus is on the laptop itself, such high-performance devices often necessitate advanced cooling solutions, influencing the demand for high-end cooling pads.

- In August 2025, Targus introduced the Targus Lap Chill Mat as a budget-friendly, quiet, and lightweight option for students. Priced under US$30, it offers portability and effective cooling, catering to everyday use and light gaming.

- In April 2025, Portronics launched two new portable fans in India: the ClipCool Portable Rechargeable Fan and the CoolCube Portable Desktop Fan, starting at INR 1,149 (US$13.84). These compact and travel-friendly fans offer efficient cooling solutions for users on the go, expanding the brand's consumer electronics portfolio.

Companies Covered in Laptop Cooling Pad Market

- Cooler Master

- Thermaltake Technology

- Targus

- Logitech

- GIGABYTE/AORUS

- Zalman Tech

- HAVIT

- Antec

- Belkin

- NZXT

- Zebronics

- Portronics

- DeepCool

- Trust International

- Elecom

- TopMate

- Opolar

- Fantech

- Kolink

- Endgame Gear

Frequently Asked Questions

The laptop cooling pad market size is estimated at US$403 Million in 2025.

The laptop cooling pad market is projected to reach US$361.2 Million by 2032.

Key trends are the rising demand for gaming laptops and high-performance computing devices, and growth in remote work and e-learning, increasing accessory adoption.

The active cooling pads segment is the market leader, accounting for approximately 63% of the market value in 2025, due to superior heat dissipation and strong adoption among gamers and professionals.

The laptop cooling pad market is expected to decline slightly at a CAGR of 5.8% from 2025 to 2032.

Major players include Cooler Master, Thermaltake Technology, Targus, Zalman Tech, and HAVIT.