- Display Technologies

- Image Intensifier Market

Image Intensifier Market Size, Share, and Growth Forecast, 2025 - 2032

Image Intensifier Market by System Location (Driver’s Seat and Dashboard), by Component (Sensors, Software and Hardware), by Application Outlook (Pulse Rate, Blood Sugar Level, Blood Pressure and Misc.), by End Use (Passenger Car, LCV and HCV) and Regional Analysis for 2025 - 2032

Image Intensifier Market Size and Trends Analysis

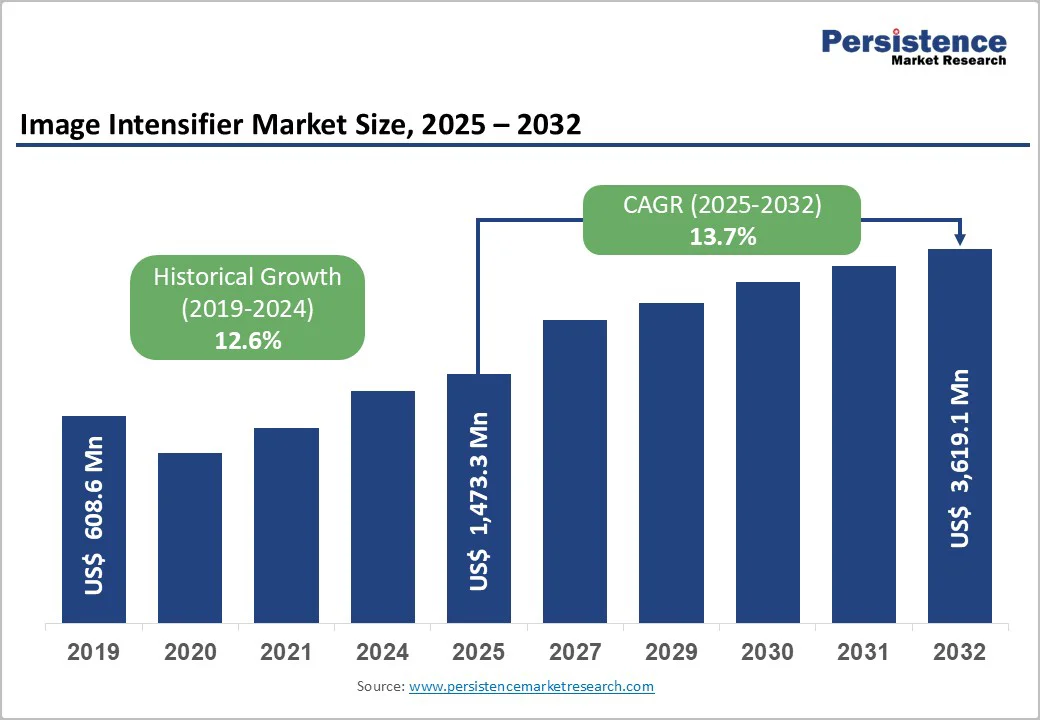

The global image intensifier market size is valued at US$ 1,473.3 million in 2025 and is projected to reach US$ 3,619.1 million by 2032, growing at a CAGR of 13.7% between 2025 and 2032.

This exceptional expansion reflects accelerating defense modernization with third generation (Gen III) image intensifier tubes achieving 10,000-hour lifespan and superior low-light sensitivity providing tactical advantage in military operations, healthcare diagnostics deployment expanding beyond radiology into emergency medicine with real-time surgical imaging.

Key Industry Highlights:

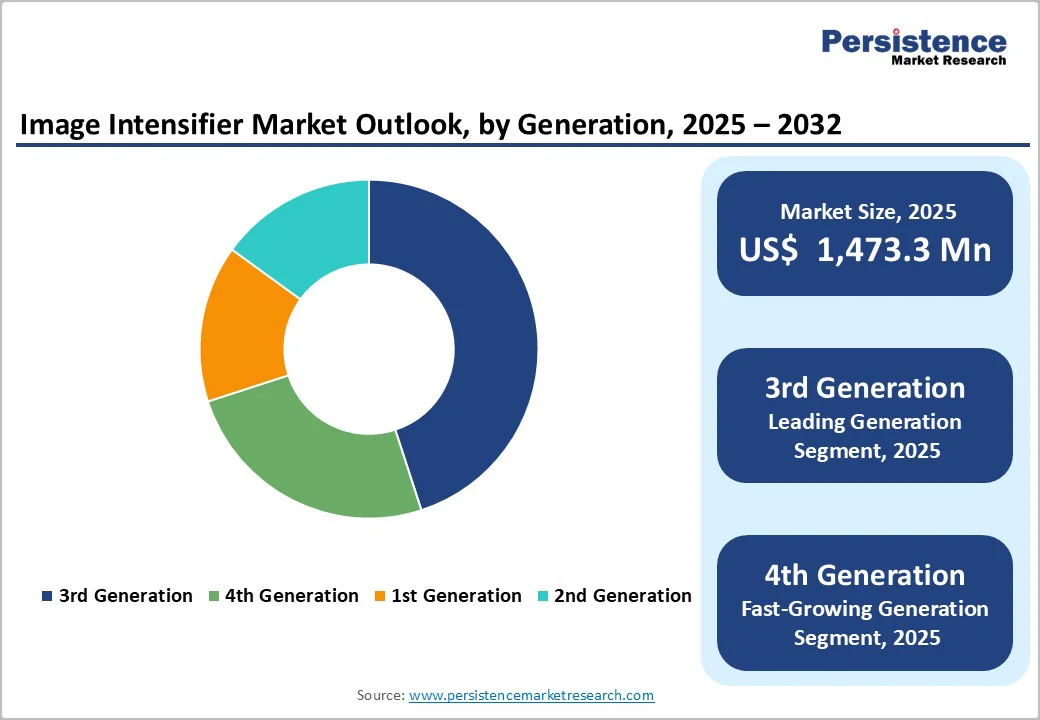

- Technology Generation Leadership: Third-generation systems dominate with 41.2% market share, driven by gallium-arsenide (GaAs) photocathodes, high sensitivity, and auto-gating capability that protects image intensifiers under bright-light exposure. Fourth-generation technology represents the fastest-growing segment at 15-18% CAGR, benefiting from filmless tube architecture, reduced noise, and operational lifespans exceeding 20,000 hours, supporting next-gen military and security deployments.

- End-User Dynamics: Healthcare and medical applications command 34.3% share, supported by surgical imaging, emergency diagnostics, and orthopedic visualization requirements. Government and law-enforcement agencies represent the fastest-growing end-user segment at 11% CAGR, driven by cross-border surveillance, crime-scene investigation, and enhanced nighttime operational capability.

- Application Trends: Binoculars and goggles dominate with 48.3% application share, reflecting widespread military usage, hands-free operation, and suitability for field missions. Night-vision cameras represent the fastest-growing segment at 10% CAGR, driven by surveillance system upgrades, autonomous platform integration, and demand for high-resolution night-time monitoring.

- Regional Growth Patterns: North America leads with 35% global market share, expanding at 12.8% CAGR through strong U.S. military procurement and advanced R&D activity. Asia Pacific is the fastest-growing region at 16.2% CAGR, with China accounting for nearly 38% of regional demand and India growing at 14% CAGR through ongoing defense modernization programs.

- Strategic Market Developments: L3Harris leads with 20-24% market share, backed by a comprehensive Gen III/IV product portfolio. Photonis, Elbit Systems, and GE Healthcare maintain strong competitive positions through diversified imaging technologies. Civilian applications represent a US$1.5-2.5 billion opportunities, while hybrid thermal-image-intensifier fusion systems are expected to reach US$800 million to 1.5 billion by 2032, driven by demand for enhanced situational awareness.

| Key Insights | Details |

|---|---|

| Image Intensifier Market Size (2025E) | US$ 1,473.3 Mn |

| Market Value Forecast (2032F) | US$ 3,619.1 Mn |

| Projected Growth (CAGR 2025 to 2032) | 13.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 12.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Market Dynamics

Drivers - Growing Demand for High Speed Imaging Intensifier Units

Image intensifier units are devices used in various imaging applications to increase the brightness of images captured by a camera or other imaging equipment. This makes it easier to capture high-quality images in low-light conditions, as well as to capture images of fast-moving objects that would otherwise be too blurry to see.

High-speed imaging requires image intensifier units because it involves capturing images at very fast frame rates. For example, in industrial and scientific applications, high-speed imaging is used to capture images of fast-moving processes such as explosions, fluid dynamics, and combustion. In medical applications, high-speed imaging is used to capture images of the heart and other organs in motion.

- In November 2022, L3Harris had completed the dispatch of its 10,00th Enhanced Night Vision Goggle-Binocular (ENVG-B). This was followed by another production order for the product from the U.S. army. The night vision binoculars provide the soldiers with better speed and accuracy.

- In July 2022, Subtle Medical, a provider of AI solutions for medical imaging partnered with Siemens Healthineers which is a medical technology company. The partnership will focus on the integration of subtle medical MR-image enhancement software. The focus will be on developing the technology and improving the patient experience.

Market Restraints

High Cost and Affordability Constraints Limiting Civilian Adoption

Advanced image intensifier tubes commanding $15,000-30,000 per unit for Gen III civilian-market products versus $8,000-15,000 for military variants create substantial financial barriers constraining widespread commercial deployment.

Complete night vision goggle systems incorporating Gen III image intensifiers reaching $40,000-60,000 per unit represent significant investment for civilian applications including law enforcement agencies, security firms, and commercial industries with limited budgets.

Maintenance and replacement cost burden representing 20-30% of annual operational budget creates multi-year financial commitment constraining adoption among budget-constrained organizations including small municipal police departments and private security firms.

Thermal imaging alternative technologies achieving comparable performance at 25% cost reduction threaten image intensifier market share in civilian applications, with thermal technology deployment accelerating 8% annually as manufacturing costs decline.

Export Regulations and Technology Control Constraints

International Traffic in Arms Regulations (ITAR) and Munitions List classification restricting image intensifier tube export to approved nations limit manufacturing capacity utilization and geographic market access. U.S. State Department export controls preventing Gen III and Gen IV tube sales to non-allied nations including China, Russia, Iran, and North Korea constrain manufacturers to 35-40% global addressable market excluding restricted regions.

Technology transfer restrictions preventing foreign manufacturing partnerships and joint ventures in image intensifier production limit supply chain globalization and cost reduction opportunities available in conventional consumer electronics.

Military secrecy classification of advanced filmless Gen III and experimental Gen IV technologies restricts public technical disclosure and academic research constraining innovation acceleration versus openly developed alternative technologies.

Market Opportunities

Asia Pacific Defense Modernization and Border Security Investment

India, Southeast Asia, and Asia Pacific nations collectively investing $150 billion in defense modernization through 2030 create substantial image intensifier demand driven by border security requirements, counterinsurgency operations, and maritime domain awareness.

India military modernization targeting 2,500+ Gen III night vision goggles procurement supports defense equipment localization through technology transfer and joint production agreements creating manufacturing opportunity estimated at $2-4 billion.

ASEAN nations including Vietnam, Philippines, and Indonesia expanding maritime surveillance capabilities addressing contested territorial claims and piracy risks support image intensifier deployment in coastal surveillance systems. Japan and South Korea defense modernization addressing North Korean threats and technological parity maintenance drive continued Gen III upgrade cycles and emerging Gen IV technology adoption.

Civilian Commercial Applications and Non-Military Market Expansion

Emerging civilian applications including wildlife observation, cave exploration, search and rescue, outdoor recreation, and aviation support market diversification, reducing military-dependency exposure, and expanding addressable market. Night vision hunting applications representing 25-35% of civilian image intensifier market support sport hunting precision and hunter safety in low-light conditions, with civilian market penetration reaching 8-12% of total deployed units.

Aerial platform integration includes commercial drone night operations for infrastructure inspection, environmental monitoring, and precision agriculture applications, create $500 million to $1 billion emerging opportunity. Aviation night vision operations enabling helicopter rescue missions, air ambulance services, and emergency response supporting medical applications growth through specialized aviation night vision imaging system (ANVIS) integration.

Category-wise Analysis

Generation Insights

Gen III image intensifiers hold a 41.2% share, driven by gallium arsenide (GaAs) photocathodes that deliver over 10,000 hours of lifespan, high sensitivity in the 800-900 nm range, and reduced halo effects through ion-barrier technology. Auto-gating protects operators from bright-light exposure and maintains mission readiness. Unfilmed Gen III variants further boost clarity and extend lifespan to 20,000 hours, supporting special operation’s needs.

Gen IV intensifiers are the fastest-growing segment at 10% CAGR, enabled by filmless tube architecture offering superior low-light performance, 30% higher signal-to-noise ratio, and clearer imaging. Their 20,000+ hour durability and improved reliability justify a 20% price premium and accelerate military adoption.

End-User Insights

Healthcare and medical applications command 34.3% end-user share through diversified deployment across fluoroscopic surgical imaging, emergency diagnostics, dental radiography, and orthopedic procedures supporting minimally invasive surgery acceleration. Portable image intensifier integration enabling point-of-care diagnostics benefits emergency medicine and rural healthcare facilities lacking advanced imaging infrastructure.

Government and law enforcement applications represent fastest-growing end-user segment at 12% CAGR, driven by cross-border surveillance expansion, evidence collection requirements, and criminal investigation support. Border security modernization programs are investing in advanced surveillance infrastructure to support law enforcement in night vision technology adoption.

Application Insights

Binocular and goggle applications command 48.3% application share through military personnel use supporting surveillance, navigation, and target identification with portable wearable systems. Compact form factor enabling helmet integration and handheld operation supports rapid deployment in diverse tactical scenarios.

Night vision camera systems represent fastest-growing application segment at 10% CAGR, driven by surveillance camera deployment, autonomous platform integration, and commercial security applications. Compact sensor integration enabling miniaturized camera systems supports drone reconnaissance and surveillance vehicle deployment.

Regional Market Insights

North America Image Intensifier Market Trends

North America generates approximately US$515 million market value in 2025 representing 35% global market share growing at 12.8% CAGR through 2032, driven by U.S. military leadership, defense modernization, and security infrastructure investment.

The United States dominates regional market with 82-86% North American share through defense procurement leadership including military special operations, law enforcement agencies, and government surveillance deployment.

Diagnostic Imaging Systems, including those that utilize image intensifiers, have been increasingly used in the healthcare sector to improve visibility and provide more accurate diagnoses. These systems are used to capture high-resolution images of internal organs and tissues, which can help doctors to detect and diagnose medical conditions.

Also, improving the accuracy of diagnoses, the use of diagnostic systems in healthcare can also improve patient outcomes by enabling doctors to detect medical conditions at an early stage. This early detection can lead to more effective treatments and better patient outcomes, encouraging the adoption of image intensifier devices. Due to these reasons, in 2022, the United States Image Intensifier Market held the leading share of 12.5% in the global marketplace.

Europe Image Intensifier Market Trends

Europe represents US$372 million market in 2025 capturing 25% global market share growing at 13.2% CAGR through 2032, characterized by NATO alliance coordination, advanced technology development, and stringent regulatory compliance. United Kingdom (UK) has one of the most well equipped and developed healthcare sectors in the world.

This allows the use of image intensifier to be large in the healthcare sector. This country is also leading in the fields of scientific research and development, the UK space agency is increasing its investments in the purchase of devices and technological development, allowing the market for image intensifiers, to grow in the space exploration sector as well.

The space industry has been at the forefront of adopting advanced technologies. Image intensifiers are highly sensitive devices that amplify available light, enabling better visibility in low light conditions. In the space industry, where visibility is often limited due to the lack of natural light, image intensifiers play a crucial role in enhancing the quality of images captured.

They are widely used in various applications such as space exploration, satellite imaging, and remote sensing.

Asia Pacific Image Intensifier Market Trends

Asia Pacific represents fastest-growing region at approximately 16.2% CAGR through 2032, with an estimated market value reaching US$1.2 billion by 2032 comprising 30% global market share by 2032, driven by defense modernization, border security emphasis, and emerging technology adoption.

China is a country that is rapidly progressing in the development of artificial intelligence patents and publications, and is leading among several powerful countries according to Harvard Business Review this country also has one of the largest militaries and has turbulent relations with its neighbours, causing it to invest in the resources and technologies of the military.

Image Intensifier Market Competitive Landscape

Companies invest in research and development to create new and improved image intensifier technologies. Companies may offer a wide range of image intensifier products to cater to different applications and industries.

Companies may focus on building strong brand recognition and promoting their products through various marketing channels. Companies may collaborate with other firms or organizations to expand their reach and increase their market share. Companies may strive to reduce costs and increase efficiency to offer competitively priced products.

Key Industry Developments

- In February 2025, Microsoft Corporation and Anduril announced a partnership toadvance the Integrated Visual Augmentation System (IVAS) program for the U.S. Army. Via this partnership agreement, Anduril will assume the oversight of production and future development related to IVAS.

- In February 2025, Exosens announced the strengthening of its partnership as a keysupplier to Senop for night vision image intensifier tubes. The contract is the third for Senop and reflects the rising demand for night vision goggles.

- In November 2022, the U.S. Army received its 10,000th Enhanced Night Vision Goggle-Binocular from L3Harris Technologies, along with a fresh production order for more ENVG-Bs. The combat-tested ENVG-B gives soldiers the advantage in night vision since it allows them to detect, assess, and engage targets faster and more accurately than any other device.

Companies Covered in Image Intensifier Market

- L3 Technologies, Inc.

- Thales Group

- FLIR Systems, Inc.

- Siemens

- Canon Medical Systems Corporation

- ASELSAN A.S.

- PHOTONIS

- Ziehm Imaging GmbH

- Dantec Dynamics A/S

- Lambert Instruments BV

- Harder.digital

- Photek

- Optexim JSC

- Others Key Players

Frequently Asked Questions

The Image Intensifier market is estimated to be valued at US$ 1,473.3 Mn in 2025.

The key demand driver for the Image Intensifier market is the growing focus on driver and passenger safety through real-time health assessment.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Image Intensifier market.

Among the Generation Type, 3rd Generation holds the highest preference, capturing beyond 41.2% of the market revenue share in 2025, surpassing other Generation type.

The key players in Image Intensifier are L3 Technologies, Inc., Thales Group, FLIR Systems, Inc., Siemens and Canon Medical Systems Corporation.