- Medical Devices

- Image Guided Systems Market

Image Guided Systems Market Size, Share, and Growth Forecast 2026 - 2033

Image Guided Systems Market by Product (Devices, Computed Tomography (CT) Scanners, Ultrasound Systems, Magnetic Resonance Imaging (MRI), Endoscopes, X-ray Fluoroscopy, Positron Emission Tomography (PET), Single Photon Emission Computed Tomography (SPECT), Softwares), by Application (Cardiac Surgery, Neurosurgery, Orthopedic Surgery, Gastroenterology, Urology, Oncology Surgery, Others), End User, and Regional Analysis, 2026 - 2033

Image Guided Systems Market Size and Trend Analysis

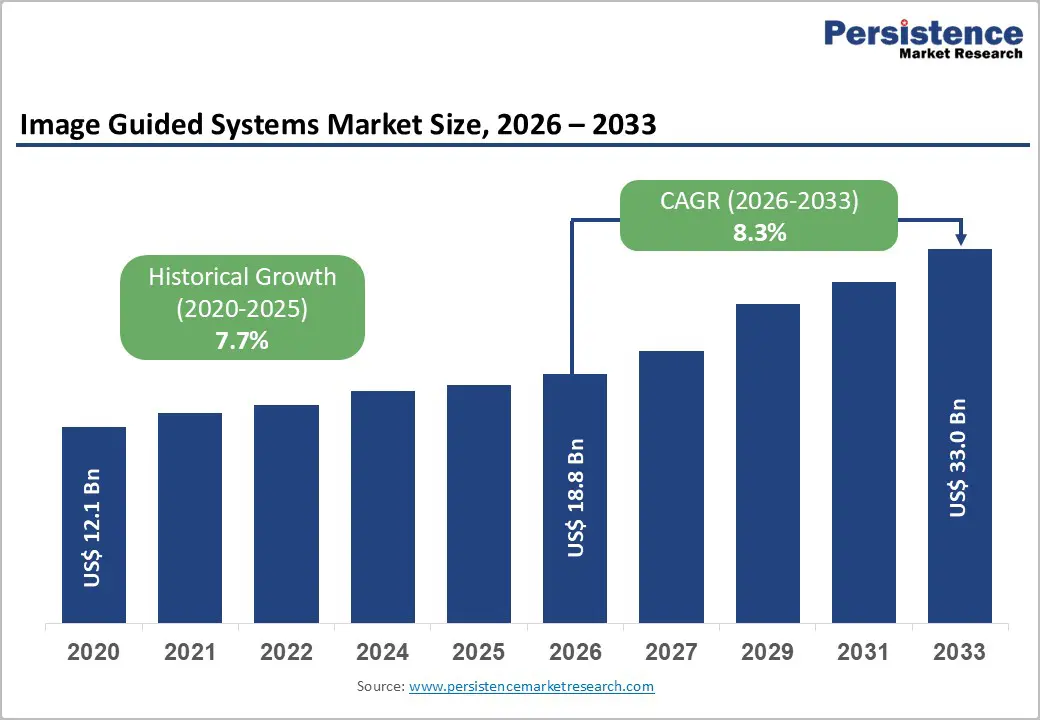

The global image guided systems market size is expected to be valued at US$ 18.8 billion in 2026 and projected to reach US$ 33.0 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033.

Strong growth is driven by rapid adoption of minimally invasive and precision-guided procedures, rising chronic disease burden, and continuous innovation in advanced imaging modalities and navigation software across surgical specialties. Increasing procedure volumes in cardiac surgery, oncology, and orthopedic surgery, coupled with hospital investments in hybrid operating rooms and integrated image-guided therapy systems, further underpin market expansion. Supportive regulatory approvals for oncology and diagnostic imaging devices in major markets such as the U.S. and Europe also accelerate clinical adoption and replacement demand.

Key Industry Highlights:

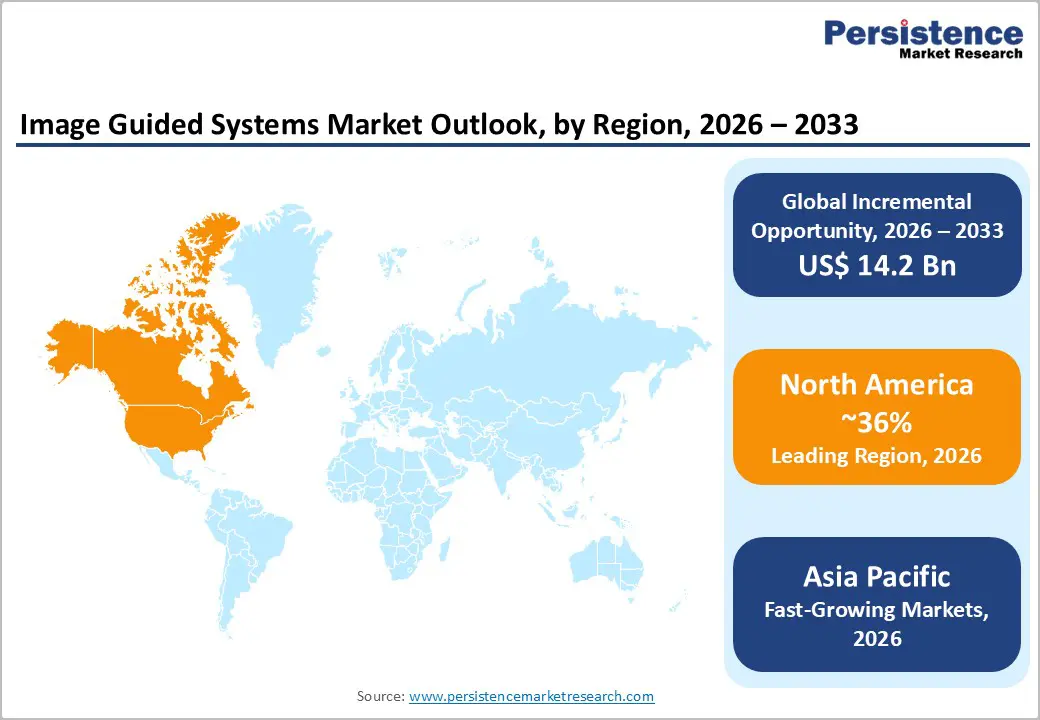

- North America leads the image-guided systems market due to advanced healthcare infrastructure, favorable reimbursement, and strong innovation in the U.S. and Canada, driving high adoption of complex procedures.

- Asia-Pacific is the fastest-growing region, supported by hospital modernization, government initiatives such as Healthy China 2030, and rising surgical volumes in China, Japan, India, and ASEAN.

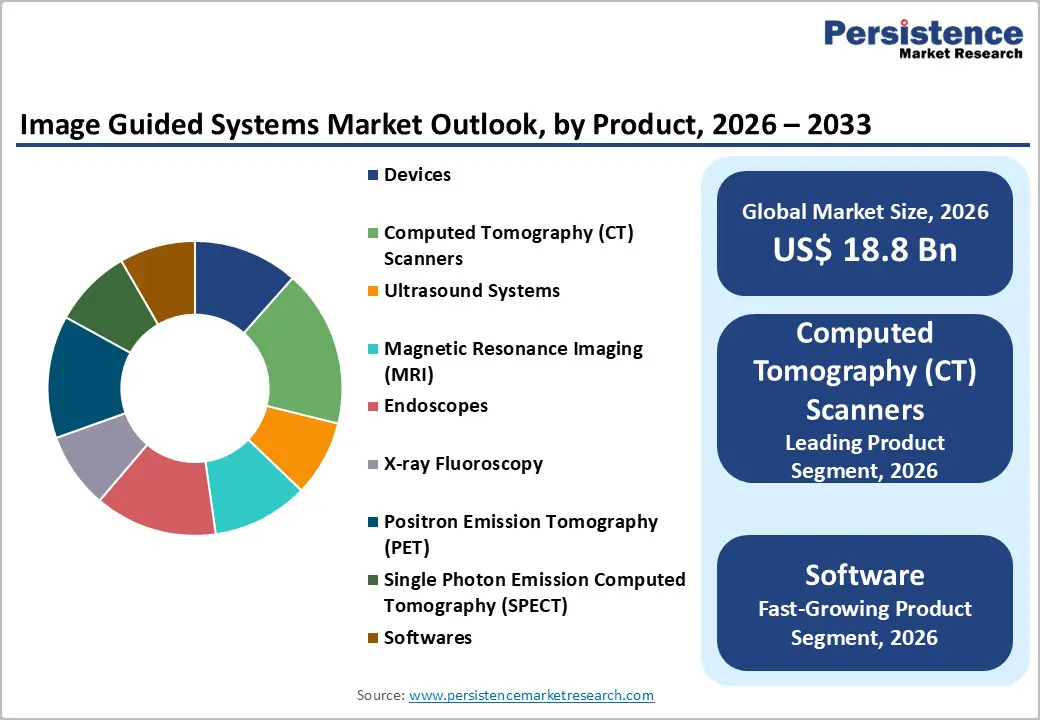

- CT scanners are the leading product category, with ~18% market share, and play a central role in preprocedural planning and intraoperative guidance in oncology, cardiovascular, and trauma surgery.

- Software for image registration, 3D navigation, and AI guidance is the fastest-growing segment, as hospitals focus on workflow efficiency and decision support in hybrid ORs.

- Key opportunities exist to expand image-guided systems in emerging Asian markets through localized manufacturing and cost-effective solutions.

| Key Insights | Details |

|---|---|

| Image Guided Systems Market Size (2026E) | US$ 18.8 billion |

| Market Value Forecast (2033F) | US$ 33.0 billion |

| Projected Growth CAGR (2026 - 2033) | 8.3% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Drivers - Rising burden of chronic and complex diseases

The growing incidence of cancer, cardiovascular disease, and degenerative musculoskeletal disorders is a primary driver for image-guided systems. According to the World Health Organization (WHO), cardiovascular diseases remain the leading cause of mortality worldwide, while global cancer cases continue to rise, requiring ever more precise diagnostic and interventional approaches. Image-guided platforms integrating CT, MRI, PET, ultrasound, and navigation software enable real-time targeting, margin assessment, and reduced complication rates in oncology surgery, cardiac interventions, and neurosurgery. In Europe, radiation-based treatments are used in more than 120,000 patients annually in the U.K. alone, highlighting the scale of demand for advanced image-guided treatment systems that improve safety and accuracy in therapy delivery.

Shift toward minimally invasive and hybrid operating room procedures

Health systems and patients increasingly favor minimally invasive surgery (MIS) due to shorter hospital stays, reduced post-operative pain, and faster return to normal activities. MIS procedures depend heavily on intraoperative imaging, endoscopic visualization, and 3D navigation, boosting demand for integrated image-guided therapy systems in hybrid operating rooms. Hospitals are deploying advanced angiography, CT, and MRI suites to support complex cardiovascular and neurovascular interventions, often combining robotic-assisted platforms with real-time image guidance. Regulatory bodies in North America and Europe are also encouraging safer, radiation-optimized systems, driving upgrades from legacy fluoroscopy and X-ray to more sophisticated, dose-efficient solutions with embedded guidance software.

Market Restraints

High capital and lifecycle costs of advanced systems

Acquisition, installation, and maintenance of image-guided systems, especially high-end CT, MRI, hybrid OR suites, and navigation platforms, require substantial capital budgets that can strain hospitals and ambulatory centers, particularly in emerging markets. Advanced intraoperative imaging and navigation devices often require infrastructure upgrades, shielding, and specialized IT integration, which add to the total cost of ownership. Smaller clinics and public facilities with constrained reimbursement may delay adoption or rely on refurbished systems, limiting penetration rates in price-sensitive regions.

Complex regulatory and interoperability challenges

Image-guided systems must comply with stringent regulatory frameworks, including FDA device approvals and CE marking requirements for safety, electromagnetic compatibility, and radiation dose. Achieving interoperability among imaging modalities, surgical navigation platforms, and hospital information systems remains technically complex, thereby extending integration timelines and increasing costs. Vendors face extensive validation and post-market surveillance obligations, which may slow rollout of innovative features such as AI-driven guidance and advanced automation across multiple jurisdictions.

Opportunity - Software-driven navigation, AI, and workflow optimization

The fastest-growing opportunity lies in software for image registration, 3D reconstruction, navigation, and decision support, as providers prioritize upgrades that enhance existing hardware. Software already accounts for a sizable share of revenue in image-guided surgery devices and is expected to grow at a double-digit rate as hospitals seek real-time guidance, dose optimization, and analytics capabilities. Regulatory acceptance of AI-enabled imaging and planning tools is advancing, with multiple oncology and diagnostic imaging devices cleared in 2023 by CDRH and the FDA Oncology Center of Excellence, including systems enhancing visualization and treatment planning. These trends create attractive recurring revenue models through licenses, service contracts, and cloud-based imaging applications for vendors in the image-guided systems market.

Expansion in emerging Asian healthcare systems and smart hospitals

The Asia-Pacific region presents a significant opportunity as healthcare infrastructure scales up and governments prioritize advanced surgical care. In China, initiatives such as “Healthy China 2030” promote investments in smart hospitals, digital imaging, and minimally invasive surgery, driving demand for image-guided surgical devices and therapy systems. Domestic players and international manufacturers are expanding manufacturing and R&D footprints, making high-performance CT, MRI, and endoscopic platforms more accessible to secondary and tertiary facilities. Rapid growth in surgical equipment markets across China, Japan, India, and ASEAN, driven by aging populations and rising prevalence of chronic diseases, underpins strong medium-term expansion prospects for image-guided systems vendors.

Category-wise Analysis

Product Insights

Computed Tomography (CT) scanners are estimated to hold approximately 18% of the market in 2025, making them the leading product segment within image-guided systems due to their pivotal role in planning and guiding complex interventions. CT provides high-resolution cross-sectional images that support oncology, cardiovascular, trauma, and orthopedic procedures, often serving as the backbone modality for intraoperative navigation and hybrid OR workflows. The increasing use of CT-based 3D reconstructions for preoperative planning and intraoperative verification, together with improvements in iterative reconstruction and dose management, sustains strong clinical preference. In many hospitals, CT-guided biopsies, ablations, and structural heart interventions are now standard of care, reinforcing CT’s leadership within the broader image-guided systems product mix.

Application Insights

Cardiac surgery accounts for the largest share of applications, accounting for more than 34% of revenues in related image-guided treatment and surgery markets in 2023, reflecting the heavy reliance on imaging in structural heart and coronary procedures. Globally, cardiovascular diseases remain the foremost cause of death, and the growing use of transcatheter aortic valve replacement (TAVR), complex percutaneous coronary interventions, and electrophysiology ablations all require advanced fluoroscopy, CT, and 3D mapping systems. Hospitals in North America and Europe have invested significantly in cath labs and hybrid ORs equipped with angiography and CT systems specifically tailored for cardiovascular interventions, driving high utilization of image-guided platforms in this specialty.

End-user Insights

Hospitals constitute the dominant end-user group, accounting for more than 37% of revenue in comparable image-guided therapy and surgery markets in 2023. This dominance stems from hospitals’ role as primary sites for complex neurosurgical, cardiovascular, and oncologic procedures that demand advanced imaging, navigation, and hybrid OR capabilities. Large tertiary and academic medical centers also act as innovation hubs, adopting next-generation intraoperative MRI, CT, and robotic-assisted systems earlier than ambulatory settings. Rising surgical volumes, the need to optimize clinical workflows, and increasing reimbursement for minimally invasive, image-guided procedures support sustained hospital investment in upgrading imaging suites and integrating therapy systems with enterprise IT platforms.

Regional Insights

North America Image Guided Systems Market Trends and Insights

North America is the leading regional market, capturing an estimated 36-39% share in recent years across closely related image-guided therapy and surgery systems, with the U.S. being the primary revenue contributor. The region benefits from a well-established healthcare infrastructure, high per-capita health expenditure, and early adoption of technologically advanced imaging modalities and navigation solutions in both hospitals and specialty centers. Strong reimbursement frameworks for minimally invasive and image-guided procedures further enable providers to invest in high-value CT, MRI, PET, and hybrid OR platforms.

The U.S. Food and Drug Administration (FDA) plays a critical role in shaping market dynamics through clear regulatory pathways for oncology, cardiovascular, and neurosurgical imaging devices. In 2023, the CDRH, in collaboration with the Oncology Center of Excellence, authorized 118 oncology devices, including 41 radiation oncology and diagnostic imaging devices, underscoring a robust pipeline of innovations entering clinical practice. North America’s rich innovation ecosystem, encompassing major manufacturers such as GE Healthcare and Siemens Healthineers, as well as leading academic centers, continues to stimulate the development of AI-enabled guidance, robotic integration, and advanced intraoperative visualization tools for image-guided systems.

Asia Pacific Image Guided Systems Market Trends and Insights

Asia-Pacific is the fastest-growing market for image-guided systems, driven by the rapid expansion of healthcare infrastructure, rising procedure volumes, and government initiatives to modernize hospitals. Markets such as China, Japan, and India are experiencing a significant increase in chronic diseases, including cancer and cardiovascular disorders, which in turn fuel demand for minimally invasive, image-guided interventions. In China, the “Healthy China 2030” agenda promotes large-scale investment in medical technologies and smart hospitals, while local manufacturers such as United Imaging Healthcare are becoming important suppliers of advanced imaging platforms.

Japan and other developed economies in Asia-Pacific combine aging populations with stringent quality expectations, leading to strong uptake of advanced imaging and guidance systems, particularly in oncology and cardiovascular care. Emerging ASEAN markets, including Vietnam, Thailand, and Indonesia, are expanding surgical capacity and increasingly adopting modern surgical equipment, thereby supporting future demand for image-guided therapy systems as purchasing power and insurance coverage improve. These structural shifts, together with localized manufacturing and cost-optimized product offerings, underpin Asia Pacific’s position as the fastest-growing region in the image-guided systems market.

Competitive Landscape

The global image-guided systems market is moderately consolidated at the high end, with major multinational manufacturers dominating advanced CT, MRI, angiography, and integrated navigation platforms, while a broader field of regional and niche players competes in endoscopes, ultrasound, and specialized software. Leading companies focus on R&D, AI-enabled imaging, software ecosystems, and strategic partnerships with hospitals for hybrid OR installations and clinical workflow integration. Emerging business models emphasize service contracts, cloud-based image analytics, and upgradable software architectures, allowing vendors to generate recurring revenues and differentiate on usability, interoperability, and clinical decision support.

Key Developments

- In October 2025, Royal Philips, a global leader in health technology, announced the 5,000th installation of its Philips Zenition mobile surgery imaging system at Kolín Regional Hospital in the Czech Republic. Since its launch in 2019, Zenition has become a trusted solution in hospitals across more than 170 countries, enabling surgeons and interventional teams to perform image-guided procedures more efficiently and supporting improved treatment outcomes.

- In August 2025, Sony Healthcare Solutions Europe and Siemens Healthineers announced a strategic global collaboration to combine ARTIS, Siemens Healthineers' high-end angiography system, with Sony’s advanced NUCLeUS audio-visual management platform.

Companies Covered in Image Guided Systems Market

- Siemens Healthineers

- Analogic Corporation

- GE Healthcare

- Koninklijke Philips N.V.

- Stryker Corporation

- Carestream Health

- Hitachi Medical Corporation

- Hologic

- United Imaging Technologies Inc.

- BrainLab AG

- Karl Storz Gmbh & Co. Kg

- Smith & Nephew Plc

- Esaote SpA

- Zimmer Biomet

- Medtronic Plc.

Frequently Asked Questions

The global image-guided systems market size is expected to reach about US$ 18.8 billion in 2026.

The main demand driver is the rising burden of chronic and complex diseases, particularly cancer and cardiovascular disorders, which require precise, minimally invasive, image-guided interventions to improve outcomes and reduce complications.

North America is the leading region, supported by advanced healthcare infrastructure, strong reimbursement frameworks, and a robust innovation ecosystem anchored by major device manufacturers and academic medical centers in the U.S. and Canada.

A key opportunity lies in software-driven navigation, AI-enabled imaging, and workflow optimization tools that enhance existing hardware, create recurring revenue streams, and support smarter hybrid operating rooms and interventional suites worldwide.

Key players include Siemens Healthineers, GE Healthcare, Koninklijke Philips N.V., Stryker Corporation, Medtronic Plc, Zimmer Biomet, Hologic, United Imaging Technologies Inc., BrainLab AG, Karl Storz GmbH & Co. KG, Smith & Nephew Plc, Canon Medical Systems Corporation, and FUJIFILM Holdings Corporation, among others.