- Specialty & Fine Chemicals

- GCC Industrial Gases Market

GCC Industrial Gases Market Size, Share, Trends, Growth, Forecasts for 2025 - 2032

GCC Industrial Gases Market by Gas Type (Oxygen, Nitrogen, Helium, Acetylene), Application (Metal Manufacturing and Fabrication, Healthcare, Automotive & Aerospace, Others), Supply Mode (Pipeline, Bulk Gas Delivery, Cryogenic Tanks & Liquid Dewars), and Regional Analysis 2025 - 2032

GCC Industrial Gases Market Share and Trends Analysis

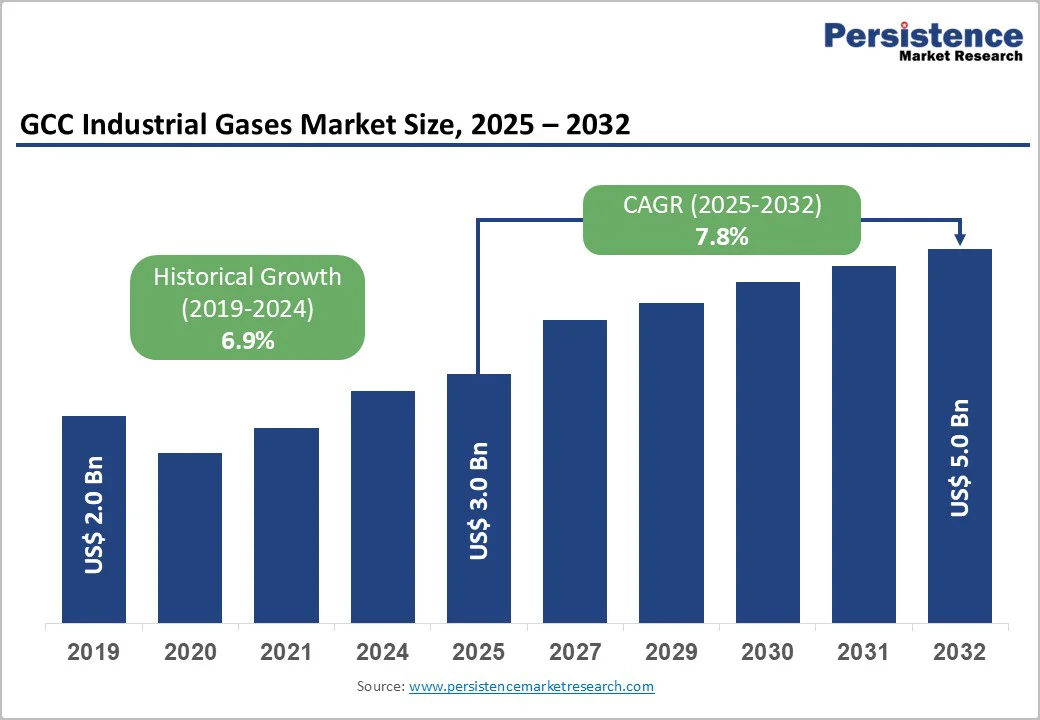

The GCC industrial gases market size is valued at US$ 2.95 billion in 2025 and projected to reach US$ 4.99 billion by 2032 at a 7.8% CAGR for the forecast period 2025 to 2032 is accelerating on the back of green hydrogen megaprojects, petrochemical expansion, and healthcare modernization.

Vision 2030 and UAE Energy Strategy 2050 fuel rising demand for hydrogen, nitrogen, and oxygen, while NEOM’s US$ 8.4 billion green hydrogen project and Aramco’s BHIG initiative anchor the region’s clean energy leadership. LNG expansion and growing medical oxygen needs further strengthen GCC’s rapid growth.

Key Industry Highlights:

- Hydrogen holds a dominant 42% share, supporting petrochemical refining and clean energy development. Meanwhile, helium is experiencing notable growth with a 5.3% CAGR, driven by the expansion of Qatar's North Field, which produces 20 tonnes of pure helium daily.

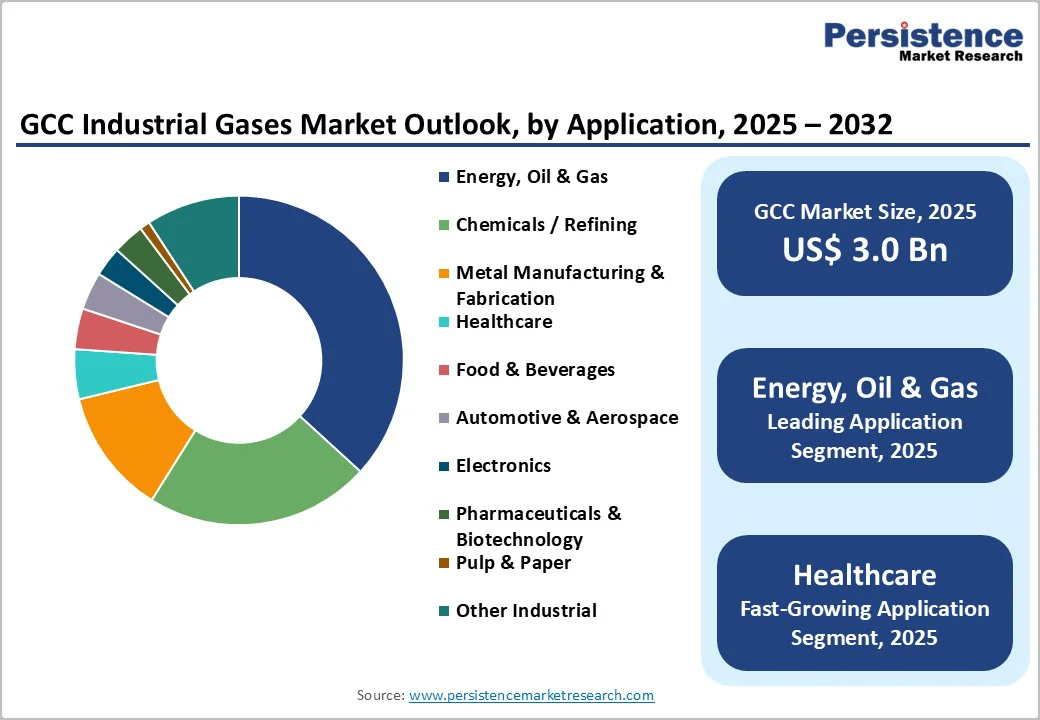

- Energy, oil, and gas applications hold a 37% market share as the leading segment, while healthcare experiences the fastest growth at a 9.3% CAGR. This growth is fueled by the increasing demand for new hospital beds during the forecast period, with Saudi Arabia accounting for 69% of the regional additions.

- Pipeline on-site tonnage supply commands 62% market share, providing cost-effective delivery to large industrial customers, while cryogenic tanks demonstrate considerable 7.5% CAGR growth supporting distributed customer segments and healthcare facilities.

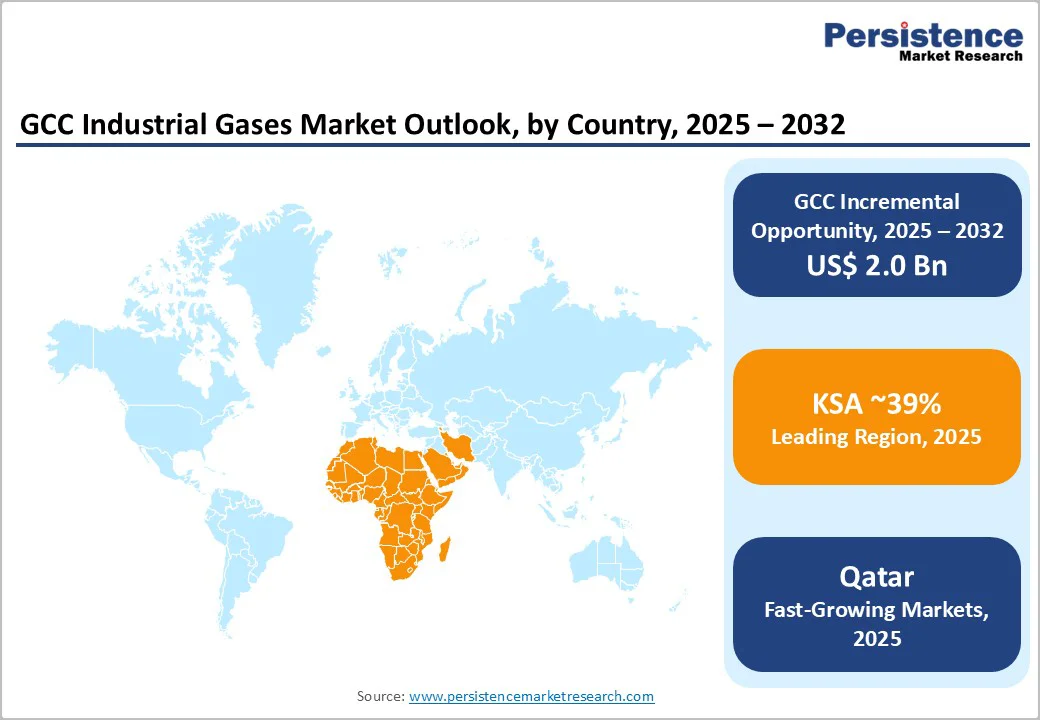

- Saudi Arabia dominates with 39% market share through Vision 2030 initiatives, the UAE holds 25% share growing at 8% CAGR via technology diversification, and Qatar achieves the fastest 8.7% CAGR growth from North Field LNG expansion targeting 126 million tonnes annually by 2027.

- Aramco's March 2025 BHIG acquisition completion, NEOM green hydrogen reaching 80% construction completion for 2027 commissioning, and ADNOC's 1.5 million tonnes annually carbon capture deployment represents transformational developments positioning GCC as a global clean energy hub.

| Key Insights | Details |

|---|---|

|

GCC Industrial Gases Market Size (2025E) |

US$ 3.0 billion |

|

Market Value Forecast (2032F) |

US$ 5.0 billion |

|

Projected Growth CAGR (2025-2032) |

7.8% |

|

Historical Market Growth (2019-2024) |

6.9% |

Market Dynamics Analysis

Drivers - Unprecedented Green and Blue Hydrogen Infrastructure Development

The GCC region is emerging as a global hydrogen production leader driven by more than ~20 billion dollars of clean hydrogen investments across Saudi Arabia, the UAE, and Qatar. Saudi Arabia’s NEOM Green Hydrogen Project, the world’s largest green hydrogen development, involves an 8.4 billion dollar investment by NEOM, ACWA Power, and Air Products and targets 600 tonnes of daily hydrogen production by 2027. By Q1 2025, construction had reached 80 percent completion across hydrogen facilities, 2.2 GW solar capacity, 1.6 GW wind capacity, and transmission networks, supporting production of 1.2 million tonnes annually of green ammonia while avoiding 5 million metric tonnes of CO2 emissions.

Saudi Aramco’s 2025 acquisition of 50 percent of Blue Hydrogen Industrial Gases Company delivers large-scale low-carbon hydrogen with carbon capture and pipeline systems in Jubail. ADNOC produces 300000 tonnes annually of hydrogen, with expansion to 500000 tonnes, and is developing a 1 million tonnes per year blue ammonia facility in Ruwais. Qatar Energy is advancing blue ammonia capacity of 1.2 million tonnes by 2026. Major projects at SABIC Agri Nutrients and Taziz reinforce integrated hydrogen corridors, driving sustained demand for hydrogen, nitrogen, oxygen, and specialty gases across regional industries.

Petrochemical Industry Expansion and North Field LNG Development

The GCC petrochemical sector expansion across Saudi Arabia’s Jubail and Yanbu complexes, UAE’s Ruwais Industrial City, and Qatar’s Ras Laffan drives sustained demand for hydrogen, nitrogen, and specialty gases supporting refining, chemical synthesis, and LNG production. Maaden’s third phosphate production line raises Saudi output to 9 million tonnes by 2027, strengthening its position among the top three global phosphate suppliers and increasing ammonia production needs, which consume hydrogen and nitrogen. Saudi Arabia’s Jafurah unconventional gas field with 200 trillion cubic feet of reserves will reach 15 billion cubic meters of production by 2026 and requires industrial gases for separation, purification, and transportation processes aligned with Vision 2032 energy diversification. Qatar’s North Field expansion increases LNG capacity from 77 million tonnes annually to 110 million tonnes by 2026 and 126 million tonnes by 2027 with future targets of 142 million tonnes by 2030. The NFE development creates nitrogen demand for inerting and hydrogen requirements through the production of 32 million tonnes annually of LNG, 4000 tonnes daily ethane, 260000 barrels daily condensate, 11000 tonnes daily LPG, and 20 tonnes daily pure helium. SABIC’s ongoing expansions and the GCC’s strategic resource position ensure multi-decade industrial gas demand.

Restraints - High Capital Intensity and Energy Consumption Requirements

Industrial gas production infrastructure requires very high capital investment, creating strong entry barriers and limiting geographic expansion across GCC markets. Air separation units, cryogenic storage systems, pipelines, and distribution assets demand multimillion-dollar commitments with payback periods of 7 to 12 years, depending on scale. Large ADNOC Industrial Gas facilities in Al Ruwais and Mirfa, with a combined capacity of 700230 cubic meters per hour, reflect investments reaching several hundred million dollars. Gulf Cryo’s network across 10 MENA countries, with more than 20 operating sites, including 8 ASU and CO2 plants, illustrates continuous capital needs to maintain regional competitiveness.

Energy-intensive separation and liquefaction processes drive high operating costs, with electricity representing 40 to 50 percent of total production expenses. Despite relatively low GCC energy prices, production economics remain pressured by depreciation, maintenance, workforce training, and safety compliance. Smaller suppliers struggle to finance advanced technologies such as pressure swing adsorption, membrane systems, and cryogenic distillation, limiting competition. Expansion into Oman and Bahrain requires new infrastructure, extending investment timelines, and reinforcing market concentration among global leaders controlling up to 75 percent market share.

Environmental Compliance Costs and Regulatory Framework Complexity

Industrial gas manufacturers in GCC markets face increasingly complex regulatory frameworks governing production, storage, transportation, and environmental compliance, creating notable cost pressures and operational constraints. Environmental Health and Safety regulations reduce growth outlook by an estimated 0.7% through requirements for continuous monitoring systems, leak detection technologies, safety training, and emergency response capabilities. Medical gas suppliers must meet strict purity standards enforced by regional health authorities aligned with global FDA and EMA expectations, requiring advanced production systems, quality laboratories, batch testing, and extensive documentation that elevate manufacturing costs.

Hazardous materials rules, including maritime dangerous goods codes and national transport regulations, mandate specialized vehicles, trained operators, and safety equipment, reducing logistics flexibility. Carbon emission rules increase near-term costs for monitoring, reporting, and carbon pricing preparedness, particularly for plants without carbon capture. Regulatory variations across GCC member states add operational complexity and require country-specific compliance systems. Additional requirements for water consumption in hydrogen production, along with strict occupational safety standards for cryogenic and high-pressure gases, further elevate operational costs and disproportionately impact smaller suppliers.

Opportunity - Carbon Capture, Utilization, and Storage (CCUS) Technology Deployment

The GCC pursuit of carbon neutrality creates major opportunities for industrial gas suppliers as CCUS infrastructure accelerates across Saudi Arabia, UAE, and Qatar. ADNOC advances large-scale deployment through the Hail and Ghasha project using Linde HISORP CC adsorption technology, targeting 1.5 million tonnes of annual CO2 capture within the world's largest offshore sour gas development operating with net zero emission objectives. Aramco develops a CCS hub in Jubail where BHIG low-carbon hydrogen production integrates CO2 capture and interconnected pipeline systems supporting refinery and petrochemical decarbonization. ADNOC expands leadership through the Al Reyadah project, capturing 800000 tonnes CO2 annually from steel operations with a planned increase to 5 million tonnes by 2030.

Gulf Cryo strengthens regional capacity through expansion of its Kuwait-based EQUATE facility and new clean CO2 projects across the UAE, Saudi Arabia, and Qatar. NEOM green hydrogen avoids 5 million tonnes CO2 each year while Qatar implements a 2.1 million tonnes CCS system at Ras Laffan. Integration of blue hydrogen ammonia production and carbon capture creates new value chains where industrial gas suppliers provide CO2 purification, compression, transportation, and injection services supported by government incentives and long-term supply opportunities.

On-Site Generation Systems Integration with Digital Technologies

On site gas generation systems create major growth prospects across GCC industrial markets by reducing operating costs, strengthening supply security, and supporting regional sustainability objectives. Pipeline based on site tonnage supply accounts for nearly sixty two percent of total demand, reflecting strong preference among large industrial consumers for reliable and cost efficient continuous gas delivery. ADNOC Industrial Gas demonstrates this model through advanced facilities in Al Ruwais and Mirfa producing seven hundred thousand cubic meters per hour through dedicated pipelines serving petrochemical and refining customers.

Linde expansion in 2024 with 59 long term agreements covering 64 small on site nitrogen and oxygen plants highlights rising adoption among metals producers and energy intensive industries. Economic benefits include up to thirty percent cost reduction, elimination of trucking emissions, reduced product losses, improved operational control, and increased supply assurance. Digital transformation further enhances performance as artificial intelligence predictive maintenance and real time monitoring lift uptime above 98% while lowering service costs. Internet of Things sensor networks enable remote diagnostics and production optimization. Strategic collaborations with leading automation firms such as Siemens and Schneider Electric support integrated technology enabled on site solutions. Cold energy recovery using LNG infrastructure reduces energy consumption by up to forty percent creating compelling opportunities across Qatar and Saudi Arabia.

Category-wise Analysis

Gas Type Insights

Hydrogen dominates the GCC industrial gases market with approximately 42% share, driven primarily by petrochemical refining applications, ammonia production for fertilizers, enhanced oil recovery operations, and emerging clean energy initiatives. The region's concentrated refining capacity across Saudi Arabia, UAE, and Qatar creates sustained hydrogen demand for hydro-treating processes, removing sulfur and nitrogen contaminants, hydrocracking converting heavy oil fractions to valuable products, and fuel production meeting international environmental standards.

SABIC Agri-Nutrients' 1.2 million tonnes annually blue ammonia project in Jubail requires substantial hydrogen volumes for ammonia synthesis, while ADNOC's 1 million tonnes annually blue ammonia facility in Ruwais establishes the UAE as a major hydrogen consumer. The GCC's strategic positioning as a global hydrogen production hub, leveraging abundant natural gas for blue hydrogen and exceptional renewable resources for green hydrogen, establishes structural competitive advantages supporting both domestic consumption and export opportunities.

Helium emerges as a prominent high-growth segment with 5.3% CAGR through 2032, following hydrogen's market-leading position. Qatar's North Field expansion produces 20 tonnes daily pure helium as LNG production byproduct, establishing Qatar as the world's second-largest helium supplier after United States. Helium applications span MRI medical imaging requiring liquid helium for superconducting magnets, semiconductor manufacturing for controlled atmosphere processes, aerospace applications, scientific research, and specialty welding operations. The global helium shortage and supply concentration create premium pricing opportunities, with helium commanding prices 50-100x higher than commodity nitrogen per unit volume.

Application Insights

Energy, oil, and gas applications dominate the GCC industrial gases market with 37% share, reflecting the region's hydrocarbon resource endowment and petrochemical industry concentration. Saudi Aramco's extensive refining operations processing 6.5 million barrels daily, ADNOC's gas processing facilities producing 9.6 million tonnes annually LNG, and Qatar Energy's North Field development targeting 126 million tonnes annually consume massive quantities of hydrogen for refining processes, nitrogen for inerting and pressure maintenance, oxygen for enhanced oil recovery and combustion enhancement, and specialty gases for analytical and process control applications. Upstream operations utilize nitrogen for reservoir pressure maintenance, pipeline purging, and well completion; hydrogen for hydrocarbon upgrading; and CO2 for enhanced oil recovery, particularly in mature fields. The sector's ongoing expansion through Jafurah field development, North Field LNG trains, and blue hydrogen facilities ensures sustained multi-decade baseline industrial gas demand.

Healthcare applications are expected to grow at a CAGR of 9.3% through 2032, driven by the GCC's healthcare modernization demand for new hospital beds by 2032, with Saudi Arabia contributing dominantly to this growth. Medical oxygen is a key market player in the region due to its importance in surgeries, respiratory therapies, and emergency care. Saudi Arabia’s increasing healthcare budget, the UAE's advanced hospital network, and Kuwait’s healthcare equipment growth all contribute to rising medical gas consumption. Post-pandemic demand for oxygen remains high due to improved emergency preparedness, maintaining strategic reserves, and supporting chronic disease management and home healthcare, fostering continuous market growth regardless of economic fluctuations.

Supply Mode Insights

Pipeline supply and on-site tonnage generation command 62% GCC market share, providing cost-effective, reliable delivery to large industrial customers requiring consistent high-volume supplies, eliminating transportation logistics and product losses. This supply mode dominates for major petrochemical facilities, refineries, steel manufacturers, and fertilizer producers concentrated in Saudi Arabia's Jubail and Yanbu industrial cities, the UAE's Ruwais Industrial Complex, and Qatar's Ras Laffan Industrial City.

Saudi Arabia's concentrated petrochemical clusters enable extensive pipeline networks, reducing per-unit distribution costs while supporting large-scale cryogenic air separation unit investments, achieving economies of scale. ADNOC Industrial Gas's 700,230 cubic meters hourly processing capacity delivered through dedicated pipeline infrastructure demonstrates an integrated on-site supply model serving Linde, Borouge, and major industrial customers with guaranteed reliability and pricing stability through long-term contracts.

Cryogenic tank and liquid dewar distribution is projected to grow at a 7.5% CAGR through 2032, catering to various sectors such as healthcare, food processing, and remote locations. This flexible supply mode enables penetration into diverse markets, including hospitals needing medical-grade oxygen, restaurants using food-grade CO2, and manufacturers requiring high-purity gases. The healthcare sector's expansion in GCC markets, particularly in secondary cities and remote areas, fuels this growth. Gulf Cryo's extensive network across 10 countries supports cryogenic delivery where pipeline infrastructure is not viable.

Regional Market Insights

Kingdom of Saudi Arabia (KSA) Industrial Gases Market Trends

Saudi Arabia dominates the GCC industrial gases market with around 39% share, driven by the concentrated petrochemical industry, Vision 2030 economic diversification initiatives, and healthcare infrastructure expansion. The Kingdom commands the largest regional industrial base with petrochemical production concentrated in Jubail Industrial City (the world's largest civil engineering project by land mass) and Yanbu Industrial City, housing SABIC, Aramco refineries, and numerous joint ventures.

Saudi Arabia's crude oil production saw a 14% yearly rise in 2022, with liquid fuels production reflecting a 12% annual increase, while the Kingdom maintains its position as the leading oil and gas producer, ensuring sustained demand for industrial gases in exploration, processing, and refining activities. Large pipeline networks across Jubail and Yanbu reduce distribution costs, supporting ongoing cryogenic ASU investments, with several international and regional suppliers maintaining production facilities. Saudi Arabia's healthcare budget allocation of $8 billion, with a prominent year-over-year increase, drives medical oxygen demand, while the Kingdom requires 8,500 new hospital beds, representing 69% of GCC's total additions through 2029.

Saudi Arabia’s Vision 2030 framework accelerates industrial gas demand through NIDLP and IKTVA initiatives supporting local production and reduced import reliance. Carbon neutrality targets drive CCUS, blue hydrogen, and green hydrogen investments, creating premium opportunities. Strategic partnerships with Aramco, SABIC, and major global suppliers, combined with expanding petrochemical and mining projects, ensure long term market growth.

UAE Industrial Gases Market Trends

UAE holds a considerable 25% of GCC market share with a robust 8% CAGR through 2032, driven by technology diversification, manufacturing expansion, advanced healthcare infrastructure, and strategic positioning as a regional trade and logistics hub. ADNOC Industrial Gas operates state-of-the-art facilities at Al Ruwais Industrial City and Mirfa, producing gaseous and liquid nitrogen, liquid oxygen, and specialty products. ADNOC currently produces 300,000 tonnes of hydrogen annually, with expansion plans to 500,000 tonnes supporting blue ammonia facility targeting 1 million tonnes annual capacity. The UAE shipped first low-carbon ammonia demonstration cargo to Germany in 2022, establishing credentials as reliable exporter while securing European market offtake agreements supporting hydrogen economy development. Technology park development across Dubai Silicon Oasis, Abu Dhabi's Masdar City, and specialized free zones including JAFZA attracts electronics manufacturing, data centers, and advanced technology investments requiring high-purity specialty gases.

The UAE’s regulatory environment supports strong industrial gas investment through free-zone incentives, full foreign ownership, and advanced port infrastructure enabling efficient trade. Energy Strategy 2050 drives green hydrogen and CCUS adoption, while Operation 300bn expands manufacturing demand. Strategic partnerships with global energy majors and leading suppliers, alongside semiconductor, healthcare, and data center investment growth, ensure sustained long-term market opportunities.

Qatar Industrial Gases Market Trends

Qatar demonstrates the fastest GCC growth rate at 8.7% CAGR despite a comparatively smaller absolute market size, driven primarily by North Field LNG expansion, representing the world's largest natural gas field development and petrochemical investments. Qatar's North Field expansion increases LNG production from the current 77 million tonnes annually to 110 million tonnes by 2026 (North Field East phase) and 126 million tonnes by 2027 (North Field South phase), with further expansion targeting 142 million tonnes by 2030.

The $82.5 billion total investment includes eight new LNG production trains producing 32 million tonnes annually of LNG, 4,000 tonnes daily ethane, 260,000 barrels’ daily condensate, 11,000 tonnes daily LPG, and 20 tonnes daily pure helium, establishing Qatar as the world's second-largest helium supplier. Nitrogen demand grows substantially for inerting applications across LNG trains, storage tanks, and transportation systems, while hydrogen requirements increase for gas processing, purification, and treating operations. Blue ammonia development targeting 1.2 million tonnes annual capacity by 2026 integrates with North Field gas processing and carbon capture infrastructure at Ras Laffan.

Qatar leverages abundant low-cost natural gas reserves, advanced LNG and GTL infrastructure at Ras Laffan, and strategic export positioning. Pro-investment regulations and economic zones align with diversification goals. Expanding healthcare, food processing, and tourism sectors elevate industrial gas demand. Supplier expansions and Qatar Energy partnerships with global majors reinforce technology capabilities and long-term market stability across regional and international operations.

Competitive Landscape

The GCC industrial gases market remains highly consolidated as global leaders strengthen regional dominance through advanced technologies, long-standing customer partnerships, and extensive production footprints. Linde, Air Liquide, and Air Products anchor the competitive landscape with large-scale air separation, hydrogen, and carbon management capabilities supporting petrochemical, metals, and energy sectors. Regional players such as Gulf Cryo and ADNOC Industrial Gas enhance competitiveness through localized production networks, pipeline-based supply, and sector-specific technical expertise across refining, healthcare, and manufacturing applications.

Strategic Developments

Saudi Aramco's Blue Hydrogen Industrial Gases Company Acquisition Completion (March 2025)

- In March 2025, Saudi Aramco finalized its acquisition of a fifty percent stake in Blue Hydrogen Industrial Gases Company, advancing large-scale low-carbon hydrogen production and carbon capture capacity in Jubail. The project strengthens Aramco’s CCS hub operations and supports refinery decarbonization while expanding regional hydrogen supply capabilities. ADNOC's Hail and Ghasha Carbon Capture Technology Agreement (October 2024)

- In October 2024, Linde Engineering agreed to supply advanced adsorption-based carbon capture technology for ADNOC’s Hail and Ghasha sour gas project, targeting one point five million tonnes annual CO2 capture. The agreement supports ADNOC’s emission reduction strategy and reinforces GCC leadership in large-scale carbon management infrastructure. Nikkiso Clean Energy Middle East Service Center Expansion (2025)

- In 2025, Nikkiso Clean Energy and Industrial Gases Group expanded its regional presence by opening a new service center in Qatar, providing cryogenic equipment support for LNG and industrial gas customers. The facility strengthens technical service capabilities as Qatar scales LNG production and blue ammonia developments requiring advanced processing equipment.

Market leaders strengthen competitive positioning through proprietary technologies, long term partnerships, and integrated solution models supporting industrial and energy transition priorities. Linde advances on site generation and carbon capture solutions, while Air Liquide expands specialty and medical gas capabilities. Air Products accelerates hydrogen leadership through major regional partnerships. Regional players like Gulf Cryo focus on geographic expansion and service excellence. Digital optimization enhances efficiency and lowers operational costs for customers.

Companies Covered in GCC Industrial Gases Market

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- ADNOC Industrial Gas

- Gulf Cryo Holding CSC

- Messer SE and Co. KGaA

- Praxair Technology Inc.

- Taiyo Nippon Sanso Corporation

- Air Water Inc.

- Iwatani Corporation

- Abdullah Hashim Industrial Gases (AHG)

- Buzwair Industrial Gases

- National Industrial Gas Plants (NIGP)

- Oman Gas Company

- Bahrain National Gas Company

Frequently Asked Questions

The GCC industrial gases market was valued at US$ 2.95 Billion in 2025 and is projected to reach US$ 4.99 Billion by 2032.

The GCC industrial gases market is experiencing significant growth due to the rapid expansion of green and blue hydrogen infrastructure, the development of the petrochemical industry driven by Qatar's North Field, increasing LNG capacity, and the rising demand for healthcare infrastructure, which is leading to a greater need for medical oxygen.

The GCC industrial gases market is projected to grow at 7.78% CAGR in the forecast period.

Key market opportunities include the deployment of carbon capture and storage technology, the integration of on-site generation systems, and the establishment of green hydrogen export infrastructure. These initiatives position the Gulf Cooperation Council (GCC) to capture a significant share of the global clean energy market, creating production-to-export value chains that meet the decarbonization needs of Europe and Asia.

The key GCC market players are Linde plc., Air Liquide, Air Products, ADNOC Industrial Gas, Gulf Cryo, Messer SE, Taiyo Nippon Sanso, Air Water Inc., Iwatani Corporation, AHG, Buzwair Industrial Gases, NIGP, and Oman Gas Company, with the leading 4-5 multinational companies collectively holding a dominating market share.