- Clothing, Footwear, & Accessories

- GCC Textile Market

GCC Textile Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

GCC Textile Market by Material (Cotton, Jute, Silk, Wool, Synthetics), By Process (Woven, Non-woven), by Application (Clothing, Industrial/Technical, Household), and Country Analysis for 2025 - 2032

GCC Textile Market Size and Trends Analysis

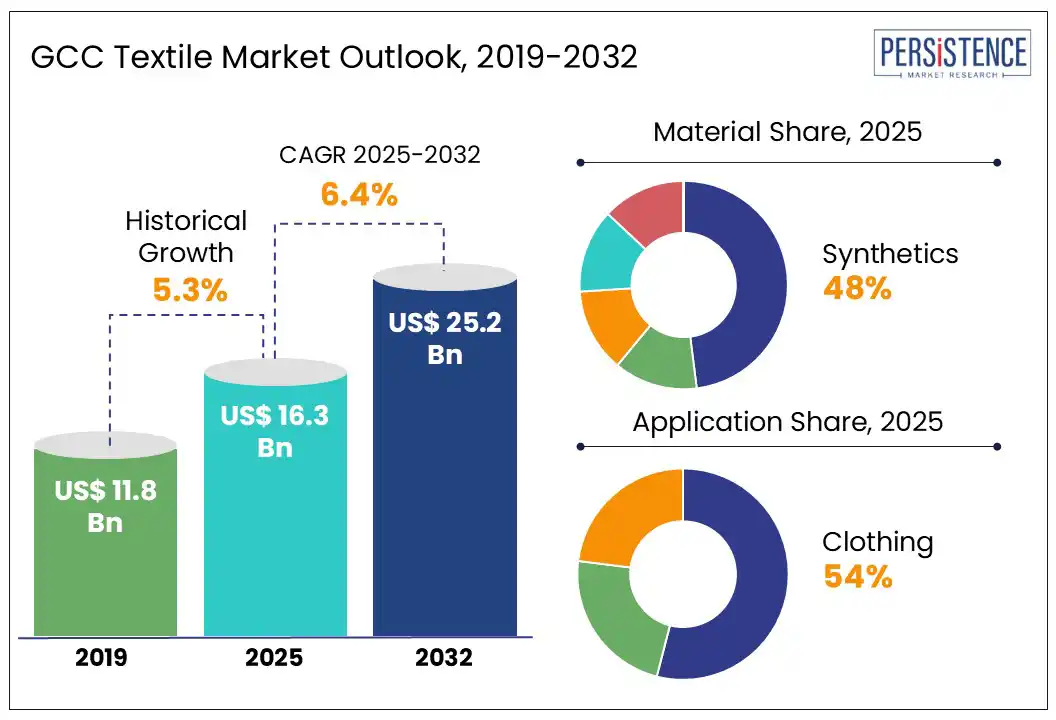

The GCC textile market size is likely to be valued at US$ 16.3 Bn in 2025 and is estimated to reach US$ 25.2 Bn in 2032, growing at a CAGR of 6.4% during the forecast period 2025-2032. The Gulf Cooperation Council (GCC) textile industry is transforming from an import-dependent sector into a driver of sustainable innovation and industrial diversification. Traditionally overshadowed by oil and petrochemicals, textiles in the GCC are now gaining renewed focus with national visions such as Saudi Arabia’s Vision 2030. With surging demand for luxury apparel, developments in recycled fabrics, and rising awareness of sustainability, the region is gradually moving toward economic resilience.

Key Industry Highlights

- Shift from oil-based economies is encouraging diversification into manufacturing, including textiles.

- Collaborations between local designers and global brands are expected to boost textile variety.

- Increasing demand for biodegradable alternatives is anticipated to open the door to next-gen bio-textiles.

- Emphasis on traceable sourcing and ESG reporting across retail and institutional buyers is a significant trend.

- Synthetics are likely to account for nearly 48.0% share in 2025 owing to strong compatibility with performance, uniform, and athleisure wear segments.

- Clothing is estimated to be the dominant application due to rising demand for ready-to-wear and customized apparel from e-commerce platforms.

- Red Sea Fashion Week and local designer acceleration programs are currently fostering fashion entrepreneurship across Saudi Arabia.

|

Market Attribute |

Key Insights |

|

GCC Textile Market Size (2025E) |

US$ 16.3 Bn |

|

Market Value Forecast (2032F) |

US$ 25.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Dynamics

Driver - Expansion of Designer Retail Spurs Premium Fabric Manufacturing

The booming luxury clothing industry is propelling the GCC textile market growth, bolstering high-end textile production, raising standards, and unlocking novel downstream opportunities. High disposable income and tourism have fueled a luxury apparel boom. This surge compels textile manufacturers to shift from basic fabrics to premium-quality materials. They are hence extensively using silk blends, cashmere, and high-thread-count cotton made for mono-brand flagship stores and luxury boutiques.

Retail infrastructure expansion such as Dubai Mall, Place Vendôme in Qatar, and upcoming Riyadh malls has also spurred demand for exclusive, bespoke fabrics. Examples include Chanel in Bahrain’s Marassi Galleria and Prada staging a villa-style runway in Dubai. These events and venues rely on domestically produced fabrics meeting global luxury standards. GCC governments are launching high-end textile hubs and investing in digital printing as well as finishing facilities to support on-demand luxury collections.

Restraint - Freshwater Deficit and Import Surge Expose Vulnerabilities

Water scarcity and increasing import competition are significantly hampering the GCC textile market to a certain extent by raising costs, limiting scale, and pushing local producers into vulnerability. The GCC relies on desalinated and non-renewable groundwater, which is an expensive and energy-intensive foundation for textile manufacturing. The region’s per capita renewable freshwater falls below 100 cubic meters per year, which is far below the 500 cubic meter threshold. It compels manufacturers to rely on desalination.

It consumes 10 to 25% of total electricity in the GCC and has jumped from 7.5 to 8.3 billion cubic meters every year in capacity since 2015. Cotton farming and fabric dyeing, key inputs to textiles, are water-based processes. Meeting such demand with desalinated water raises production costs significantly. Operating Effluent Treatment Plants (ETPs), membrane filtration systems, and zero-liquid-discharge setups also add capital and operational burden.

Opportunity - Recycled textile innovation creates new growth avenues

The production of ready-to-wear garments using recycled fabrics in the GCC is creating opportunities across manufacturing, branding, and sustainability. Consumer demand for sustainable fashion is accelerating. Recent online surveys, for example, found that 74% of consumers want to dress more sustainably, but about 41% avoid it due to high costs and confusing labels. GCC brands that offer transparent recycled-fabric lines are predicted to fill this gap, gaining consumer trust and high willingness to pay.

In Saudi Arabia, eco-streetwear brands such as Glamming Sisters are capitalizing on recycled-fabric lines to position themselves as ethical alternatives. In addition, Dubai’s supportive free-zone environment encourages fashion-tech start-ups to prototype zero-waste and recycled collections. Recycled ready-to-wear lines are also generating momentum in the hospitality and sportswear sectors. Luxury hotel chains in the UAE and Qatar have begun sourcing recycled-fiber uniforms and linens to meet sustainability certification criteria such as Green Globe.

Category-wise Analysis

Material Insights

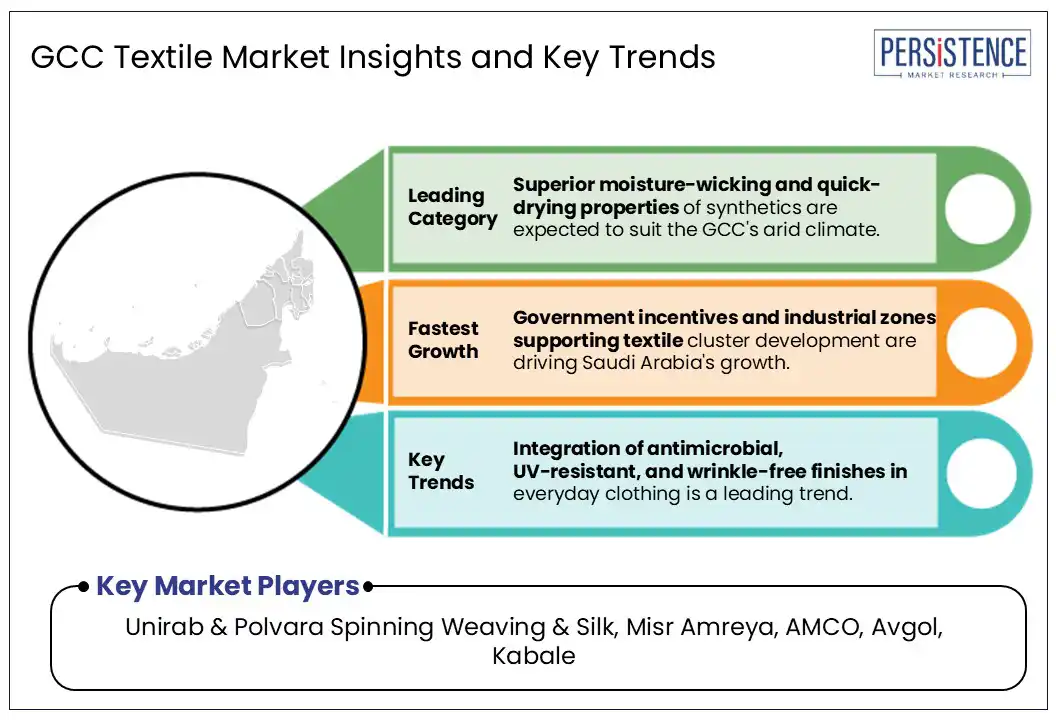

Based on material, the GCC textile market is divided into cotton, jute, silk, wool, and synthetics. Among these, synthetics are estimated to account for approximately 48.0% of share in 2025 due to their superior response to the region’s climatic, economic, and logistical elements. The extreme desert climate necessitates fabrics that are lightweight, moisture-wicking, quick-drying, and UV-resistant. Synthetic fibers such as polyester and nylon meet these demands far more efficiently than natural fibers such as cotton, which retain moisture and degrade faster under intense sunlight. Economically, these fibers are more cost-effective for mass production and import.

Cotton remains a key material owing to its unmatched breathability, softness, and skin-friendly properties, especially for everyday and premium clothing segments. In the GCC, cotton is not cultivated locally due to extreme water scarcity. It, however, holds strategic value in high-demand applications such as hospitality textiles, school uniforms, and high-end fashion basics. Hotel groups often source high-thread-count cotton linens and bathrobes to meet luxury standards expected by global travelers as synthetic alternatives often fall short in comfort.

Application Insights

In terms of application, the market is trifurcated into clothing, industrial/technical, and household. Out of these, the clothing segment is expected to hold around 54.0% of the GCC textile market share in 2025 as it directly feeds into the region’s booming retail, tourism, and hospitality economies. Demand for apparel, especially fast fashion, modest wear, and athleisure, continues to boost textile consumption more than any other segment. One of the most significant contributors is the region’s youth-heavy demographic and fashion-conscious consumers. These consumers fuel the demand for ready-to-wear garments, streetwear, and luxury fashion, pushing textile manufacturers to focus on apparel fabrics over home textiles.

The industrial/technical segment is poised to witness steady growth through 2032 due to the GCC’s ongoing infrastructure expansion, energy sector modernization, and surging emphasis on self-sufficiency in critical materials. Saudi Arabia and the UAE are prioritizing non-oil industrialization under long-term economic plans. It has opened the door for widespread use of geotextiles, filtration fabrics, and flame-retardant materials across construction, oil and gas, transportation, and defense sectors. The GCC’s large-scale energy, desalination, and waste management plants have also created significant demand for filtration textiles.

Country Insights

United Arab Emirates Textile Market Trends

The UAE is currently undergoing a strategic evolution, shifting from conventional garment trade to innovative, sustainable manufacturing as well as digital innovation. A significant growth driver is recycling and circular economy initiatives. Dubai South’s new recycling plant, which is run by Landmark Group and Dubai Customs, for example, transforms counterfeit clothing and surplus into reusable materials. It even incentivizes residents with vouchers to donate old textiles.

Dubai stands as a strategic hub in the UAE. Dubai Textile City hosts more than 170 garment manufacturers, re-exports across 52 countries, and leverages Jebel Ali’s free zone advantages. These include zero corporate income tax, modern logistics, and full foreign ownership. However, the UAE still imports over 70 % of its textiles from China, India, and Europe. Domestic manufacturers are also looking for upskilling workforces to operate novel machinery.

Saudi Arabia Textile Market Trends

In Saudi Arabia, domestic manufacturing is leaping forward, pushed by the Made in Saudi initiative and industrial clusters in regions, including Jazan, Jubail, and King Abdullah Economic City. Local textile output is being bolstered by government incentives and upskilling efforts, reducing reliance on imports. Digital textile printing is also expanding rapidly. The most prominent growth is in direct-to-garment technology, encouraging on-demand and customization adoption across SMEs.

Sustainability and traditional crafts are further converging in Saudi Arabia. The Sustainable Ihram Initiative, for instance, recycles pilgrimage garments, while local designers such as Hindamme and Moh Khoja are embedding upcycled textiles into contemporary fashion. The Royal Institute of Traditional Arts nurtures heritage textile knowledge essential for cultural branding. Local textile chemical manufacturers are also shifting toward performance and eco-friendly formulations used in medical, automotive, and fashion sectors.

Qatar Textile Market Trends

Qatar’s textile industry remains modest but is gaining momentum in niche manufacturing, digital printing, and sustainability. The country has introduced tax incentives and subsidies to attract foreign investment in modern textile machinery. The government's push aims to replace imports by increasing domestic output, especially in eco-conscious wool, cotton, and synthetic blends. On the cultural front, Design Doha 2024 exhibited over 100 regional designers, integrating textile craft into national creative narratives and strengthening market identity.

Key players such as EcoThreads Textiles are ramping up recycled-fiber products geared toward both retail and industrial markets. It is a part of a projected recycling market ramp through 2031. Early steps toward AI-driven textile sorting through hyperspectral imaging also comply with GCC-wide efforts to close looping textile waste. However, skilled labor shortages hamper scaling high-tech operations, a common GCC-wide obstacle.

Competitive Landscape

The GCC textile market is evolving rapidly, shaped by strategic localization efforts, government incentives, and an increasing shift toward sustainability. While traditionally reliant on imports from South Asia and China, GCC countries are now investing in domestic textile manufacturing. They aim to reduce dependency and enhance economic diversification under their respective Vision 2030 plans. Saudi Arabia is emerging as a significant hub in technical textiles with state-backed initiatives promoting high-value textile production. Competition is also intensifying due to new entrants, mainly SMEs and sustainable fashion start-ups.

Key Industry Developments

- In February 2025, Saudi Arabia’s Fashion Commission announced that it is working on strengthening partnerships with Japan in fashion and textile. The commission hosted ‘A Journey into Japanese Textile Mastery’ in partnership with the Japan External Trade Organization. It focused on bringing together leading textile manufacturers, industry experts, and designers from both countries.

- In January 2025, niLuu, a U.S.-based luxury vegan silk brand, extended its presence in the Middle East by launching in Qatar and Saudi Arabia for the first time. The brand offers high-quality, well-made clothing and stylish pieces suited to warm climates.

Companies Covered in GCC Textile Market

- Unirab & Polvara Spinning Weaving & Silk

- Misr Amreya

- AMCO

- Avgol

- Kabale

- Embee Group

- Millennium Fashions Industries

- FPC Coated Technical Textiles

- Aratex Group

- Alyaf Industrial Company Ltd.

- Lomar Selection

- Valleystar Uniforms

- Others

Frequently Asked Questions

The GCC textile market is projected to reach US$ 16.3 Bn in 2025.

Expanding e-commerce platforms and favorable trade policies are the key market drivers.

The GCC textile market is poised to witness a CAGR of 6.4% from 2025 to 2032.

Rise of gender-neutral apparel and youth-driven fashion culture are the key market opportunities.

Unirab & Polvara Spinning Weaving & Silk, Misr Amreya, and AMCO are a few key market players.