- Retail

- Consumer Electronic Accessories Market

Consumer Electronic Accessories Market Size, Share, and Growth Forecast, 2025 - 2032

Consumer Electronic Accessories Market By Product Type (Mobile phone accessories, Audio accessories, Others), Technology (Wired accessories, Wireless accessories, Others), Application, and Regional Analysis for 2025 - 2032

Consumer Electronic Accessories Market Size and Trends Analysis

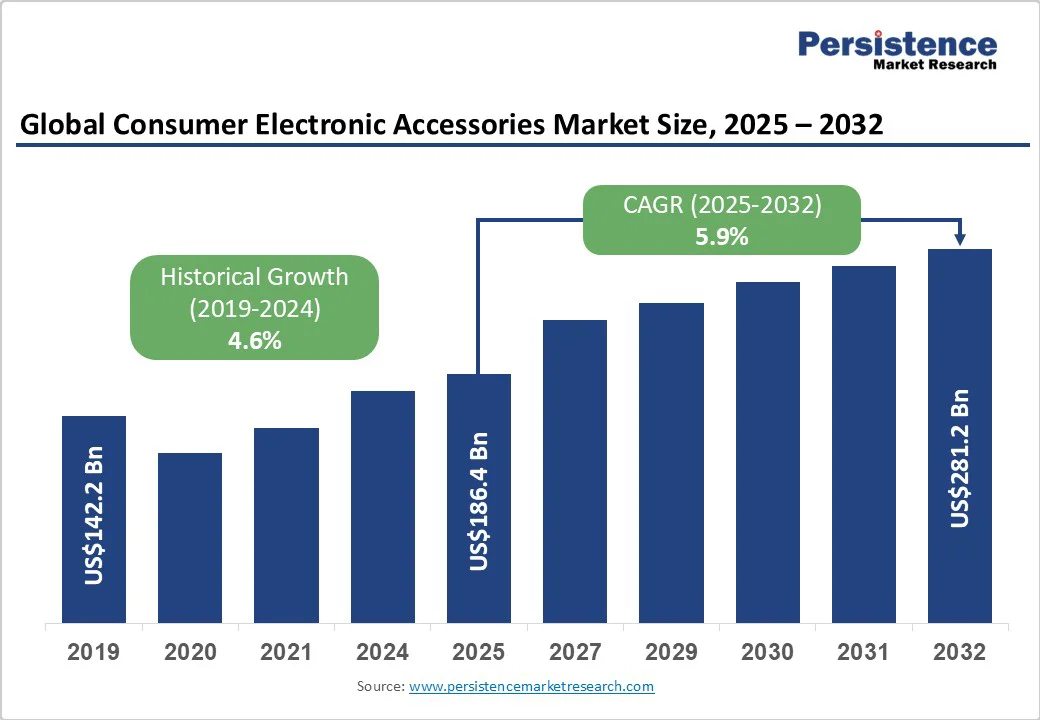

The global consumer electronic accessories market size is likely to be valued at US$186.4 Billion in 2025 and is projected to reach US$281.2 Billion by 2032, growing at a CAGR of 5.9% between 2025 and 2032, driven by rising smartphone and wearable device penetration, faster replacement cycles for personal audio and charging accessories, and expanding distribution through ecommerce and direct-to-consumer channels.

The market shows broad-based demand across Asia Pacific, North America, and Europe; Asia Pacific is currently the largest contributor due to manufacturing scale and consumer adoption. Technology convergence, wireless connectivity, miniaturized batteries, and embedded sensors are increasing average spend per device.

Key Industry Highlights

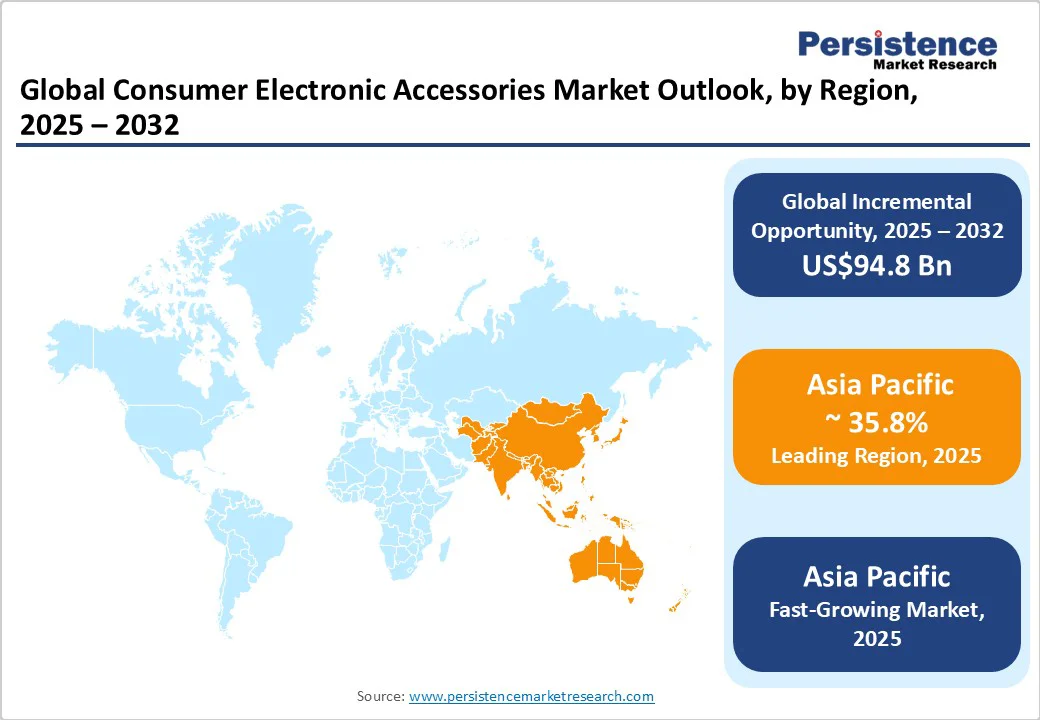

- Leading Region: Asia Pacific captured over 35.8% of global revenues in 2025, led by China’s manufacturing ecosystem and India’s smartphone-driven demand.

- Fastest-growing Region: Asia Pacific is also projected to grow the fastest, supported by localized production and low-cost innovation.

- Investment Plans: Key players such as Anker (US$150 Million in India, 2025) and Samsung (SmartThings partnership, 2024) are investing in regional manufacturing hubs and smart accessory integration.

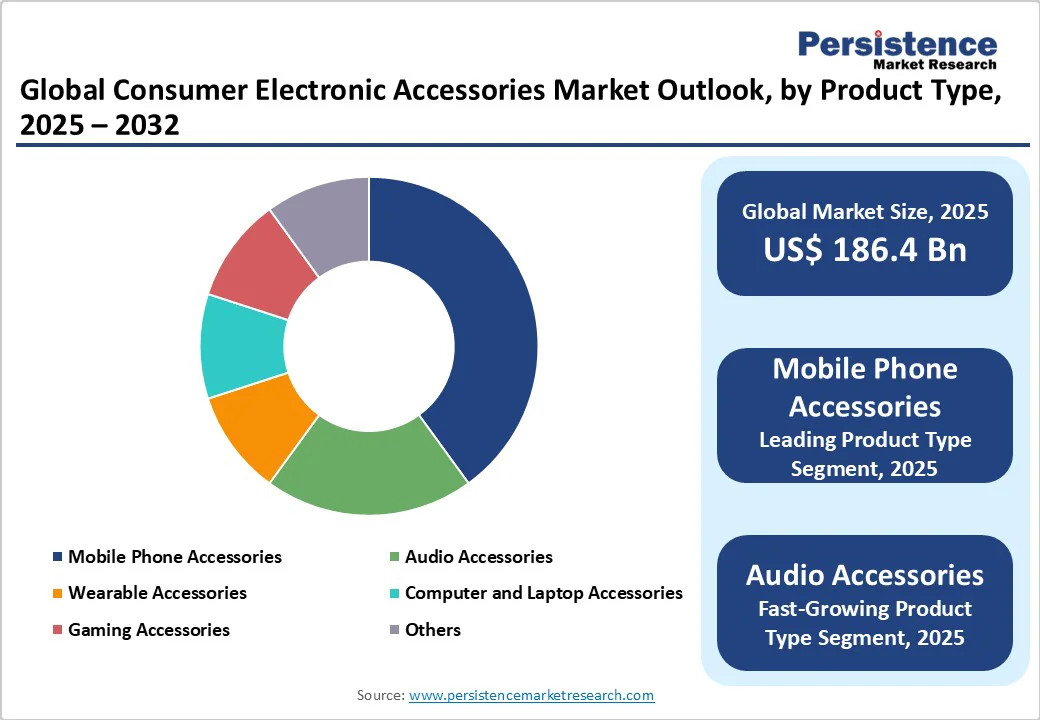

- Leading Product Type: Mobile phone-related accessories dominate, accounting for over 40.4% of global revenue in 2025, driven by high smartphone volumes and frequent replacement purchases.

- Leading Application: Smartphone-related applications hold the largest share, representing nearly 49% of global accessory spending in 2025, supported by growing uses of chargers, protective cases, and earphones.

| Key Insights | Details |

|---|---|

| Consumer Electronic Accessories Market Size (2025E) | US$186.4 Bn |

| Market Value Forecast (2032F) | US$281.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Replacement Cycles and Wireless Smart-Accessory Convergence

Global smartphone users exceeded several billion in the mid-2020s, while wearable shipments surpassed 500 million units in 2024. These installed bases raise recurring demand for accessories, particularly in chargers, cases, earbuds, and protective films.

Higher installed device counts translate into a larger addressable accessory market even when smartphone unit growth slows. Replacement cycles for earbuds, cables, and chargers create recurring revenue, while premiumization (noise-canceling earbuds, fast chargers) boosts average selling prices. Companies that align stock keeping units (SKUs) with consumer replacement behavior see stronger repeat sales.

The shift from wired to wireless accessories (TWS earbuds, Bluetooth speakers, wireless chargers) and the introduction of sensor-rich accessories (hearables with biometric sensing) are raising product value. TWS and hearables segments are recording double-digit growth rates in many sub-markets.

Feature convergence lifts product differentiation and margins for OEMs that control hardware-software integration. Vendors with strong ecosystem partnerships capture a disproportionate share of premium spend, while commodity players rely on scale and cost efficiency.

Accessory brands increasingly combine direct-to-consumer models with offline retail. Offline still dominates volume sales, especially in developing regions, but ecommerce channels are growing rapidly. Brands with strong logistics and data-driven direct-to-consumer (DTC) strategies can launch products faster and retain higher margins. Hybrid models capture both impulse buyers in retail and research-driven buyers online, improving lifetime customer value.

Component Cost, Supply Chain Volatility, and Counterfeit Markets

Rising raw material and semiconductor costs are squeezing margins, especially in lower-priced segments. Lead-time volatility for Bluetooth chips and batteries forces SKU rationalization and stockouts. Accessory manufacturers experience margin compression of 100-300 basis points when commodity prices spike. Companies without diversified suppliers or vertical integration face greater exposure.

The sector remains highly fragmented, with numerous low-cost regional manufacturers. Online marketplaces increase visibility but also facilitate counterfeit and gray-market products, eroding branded players’ revenues. In emerging economies, low-cost brands win share on price rather than features, leading to annual market share erosion of several percentage points for premium brands.

Growth Opportunities in Premium Audio and Lifecycle Extensions

The earbuds and headphones submarket is valued in the tens of billions and continues to grow strongly. Hearables with integrated health sensors, such as heart rate and blood oxygen monitoring, can command higher average selling prices (ASPs) and service-linked revenues. Vendors combining sensor hardware with software services gain recurring monetization opportunities and deeper customer lock-in.

Chargers, power banks, and cables remain high-volume categories. With global adoption of USB-C and increasing demand for fast-charging, bundled ecosystems (charger + cable + power bank) represent significant growth potential. Proprietary charging solutions and certified safety standards help brands build customer loyalty and increase average order value.

Category-wise Analysis

Product Type Insights

Mobile phone-related accessories continue to dominate the market, accounting for over 40.4% of total revenue in 2025. This dominance is fueled by the ubiquity of smartphones, high user replacement cycles for chargers, cables, and protective cases, and the constant demand for personalization.

Rising penetration of mid- and high-end smartphones globally further supports strong unit demand, particularly in Asia Pacific and North America, where consumers are more inclined toward premium protective and audio accessories.

TWS earbuds and premium audio solutions represent the fastest-growing segment, recording high single- to double-digit CAGR between 2025 and 2032. Consumer preference is shifting toward wireless, compact, and multifunctional devices with features such as active noise cancellation, in-ear biometric tracking, and integration with virtual assistants.

The popularity of music streaming, remote working, and fitness applications has significantly boosted adoption. Vendors that offer ecosystem compatibility and AI-driven features are capturing higher average selling prices, while entry-level brands grow volume through cost-competitive wireless options.

Technology Insights

Wireless accessories represent the largest share of the market in 2025, surpassing wired products in both audio and power categories. With the removal of headphone jacks from smartphones, wireless earbuds and headphones have become mainstream.

Wireless charging pads and Bluetooth-enabled speakers also drive adoption, supported by convenience and portability. Improved battery life, affordability of Bluetooth chips, and global compatibility standards have further accelerated penetration, positioning wireless as the central growth enabler for the overall market.

Smart and connected accessories are forecast to expand at the fastest pace, as consumers seek devices that go beyond basic utility. Hearables embedded with biometric sensors, fitness bands with AI coaching, and app-synced charging solutions provide data-driven personalization.

This segment benefits from the convergence of IoT and consumer electronics, with health and lifestyle features playing a pivotal role. Market growth is reinforced by rising consumer willingness to pay premiums for connected ecosystems that seamlessly link smartphones, wearables, and smart home devices.

Application Insights

Smartphone-related applications dominate accessory spending, holding a market share of 49% with chargers, protective cases, earphones, and screen guards driving the bulk of global demand. As smartphones are nearly universal across demographics, the accessory ecosystem has evolved into a high-volume, fast-replacement market.

Consumers frequently purchase multiple accessories per device, driving a stable and recurring revenue stream. Smartphone-related accessories also benefit from strong distribution across both offline and online channels, ensuring sustained sales momentum.

Wearable-related accessories are emerging as the fastest-growing application segment, propelled by rising smartwatch and fitness band adoption. Charging docks, replacement straps, and protective covers for wearables are increasingly popular among consumers who value customization and extended usability.

Health-focused applications, particularly in North America and Asia, have boosted wearable penetration, creating sustained demand for complementary accessories. By 2032, wearable-related accessories are expected to outpace growth in traditional mobile categories, reflecting the diversification of personal technology ecosystems.

Regional Insights

Asia Pacific Consumer Electronic Accessories Market Trends - High-Volume Growth Backed by Local Manufacturing and Value Innovation

Asia Pacific is the largest and fastest-growing regional market, holding over 35.8% of global revenues in 2025, underpinned by China’s expansive manufacturing ecosystem, India’s booming smartphone user base, and Japan’s premium consumer segment.

In 2025, the region will contribute over one-third of global accessory sales, led by demand for mobile-related products such as chargers, cables, and earphones. Rising disposable incomes, urbanization, and affordable device availability continue to expand the consumer base, while e-commerce platforms accelerate regional distribution.

Government regulations play a pivotal role in shaping supply chains, particularly in India, where local manufacturing requirements and import duties favor domestic assembly. China remains central as a production hub, while Southeast Asia is emerging as an alternative manufacturing base due to cost advantages.

The competitive landscape is fragmented, with both multinational leaders and low-cost regional brands competing aggressively. Investment strategies focus on localizing production, offering feature-rich products at competitive prices, and expanding omnichannel retail presence. Asia Pacific’s combination of scale, affordability, and innovation ensures its sustained dominance through 2032.

North America Consumer Electronic Accessories Market Trends - Premium Market Led by Innovation, Loyalty, and Fast Upgrades

North America represents one of the most lucrative regions for consumer electronic accessories, accounting for a significant share of global premium revenues. The U.S. dominates the region, supported by high consumer spending power, fast technology adoption cycles, and brand loyalty to premium products.

In 2025, the regional market is characterized by strong demand for TWS earbuds, gaming accessories, and wireless charging devices. Growth is further reinforced by replacement demand, with consumers upgrading frequently to higher-spec models.

Regulatory frameworks, including safety standards and interoperability requirements such as the mandated shift toward USB-C, shape design and production strategies. The competitive environment is consolidated, with Apple, Bose, Logitech, and Anker leading premium categories.

Investment flows are directed toward integrating hardware with AI-driven software features and scaling direct-to-consumer distribution. North American players are also prioritizing domestic logistics hubs and localized assembly to reduce supply chain risks. These factors ensure continued leadership in premium segments while offering opportunities for new entrants targeting affordable wireless and health-linked accessories.

Europe Consumer Electronic Accessories Market Trends - Sustainability and Compliance Driving Accessory Preferences

Europe is a mature yet evolving market, with accessory adoption supported by high per-capita spending in countries such as Germany, the U.K., and France. The region is notable for early adoption of wearables, noise-cancelling earbuds, and sustainable charging solutions.

In 2025, smartphone and wearable-related accessories dominate, while gaming and smart-home-linked accessories are gradually expanding their footprint. Perceived product durability and compliance with stringent EU safety and environmental regulations influence consumer purchase decisions significantly.

The market is shaped by regulatory standards, including electronic waste directives, packaging regulations, and charging connector mandates, particularly the EU-wide requirement for USB-C. Global brands such as Samsung, Apple, and Sony remain dominant, but regional players carve out share through sustainability-driven propositions.

Investment trends highlight growing interest in environmentally friendly materials, modular accessories, and recycling programs. Traditional brick-and-mortar retail continues to be a key channel alongside strong ecommerce penetration. The focus on sustainability and compliance provides long-term growth opportunities for brands able to align with green supply chain practices.

Competitive Landscape

The global consumer electronic accessories market is moderately consolidated, with the top 10 players accounting for an estimated 45% of global revenues in 2025. Leading multinational companies such as Apple, Samsung, Sony, and Bose dominate the premium segment, while brands such as Anker, Belkin, and Logitech hold strong positions in mid-range categories.

The market also includes numerous regional manufacturers, particularly in Asia Pacific, catering to cost-sensitive segments. Competitive positioning is influenced by ecosystem compatibility, product differentiation, and distribution networks, with premium players prioritizing design and brand loyalty, and regional players focusing on affordability and volume growth.

Leading companies are emphasizing ecosystem integration, wireless innovation, and premium positioning as core strategies. Cost leadership and localized production remain critical for regional brands competing in emerging markets. Market leaders increasingly invest in sustainability initiatives, such as recyclable materials and modular designs, while omnichannel distribution and e-commerce partnerships strengthen customer reach.

Key Industry Developments

- In March 2025, Anker Innovations announced a US$150 Million investment in India to establish a local manufacturing hub for charging accessories and wireless audio. The expansion aimed at reducing dependency on Chinese supply chains and meeting India’s growing demand, driven by rapid smartphone penetration.

- In May 2024, Samsung Electronics partnered with IKEA to co-develop smart wireless charging furniture integrated with Samsung’s SmartThings ecosystem. The partnership reflected the convergence of consumer electronics with smart home infrastructure, offering a competitive edge in connected living environments.

- In January 2024, Apple Inc. introduced a USB-C-based MagSafe charging accessory line, aligning with EU regulatory mandates. This move reinforced Apple’s premium ecosystem strategy while expanding opportunities for third-party accessory makers. The development significantly influenced global adoption of USB-C in charging solutions.

Companies Covered in Consumer Electronic Accessories Market

- Apple Inc.

- Samsung Electronics

- Sony Corporation

- Bose Corporation

- Logitech International

- Anker Innovations

- Belkin International

- Xiaomi Corporation

- Huawei Technologies

- JBL (Harman International)

- Sennheiser Electronic

- Panasonic Corporation

- Philips Electronics

- Skullcandy Inc.

- Plantronics (Poly)

- ZAGG Inc.

- Ugreen Group

- Aukey Technology

- Lenovo Group

- HP Inc.

Frequently Asked Questions

The market size in 2025 is estimated at US$186.4 Billion.

The consumer electronic accessories market is projected to reach US$281.2 Billion by 2032.

Key trends include rising adoption of TWS earbuds and wireless audio devices, integration of smart and connected features in accessories, increased replacement cycles for mobile and wearable accessories, and expansion of e-commerce and omnichannel distribution.

Mobile phone-related accessories are the leading segment, accounting for over 40.4% of global revenue in 2025.

The consumer electronic accessories market is expected to grow at a CAGR of 5.9% from 2025 to 2032, driven by smartphone and wearable adoption and wireless accessory penetration.

Major players include Apple Inc., Samsung Electronics, Sony Corporation, Bose Corporation, and Logitech International.