- Animal Health

- Commercial Aquaculture Vaccines Market

Commercial Aquaculture Vaccines Market Size, Share, and Growth Forecast, 2026 - 2033

Commercial Aquaculture Vaccines Market by Vaccine (Inactivated, Attenuated, Subunit, DNA), Species (Salmon, Tilapia, Trout, Sea Bass, Carp), Pathogen (Bacteria, Virus), and Regional Analysis for 2026 - 2033

Commercial Aquaculture Vaccines Market Size and Trends Analysis

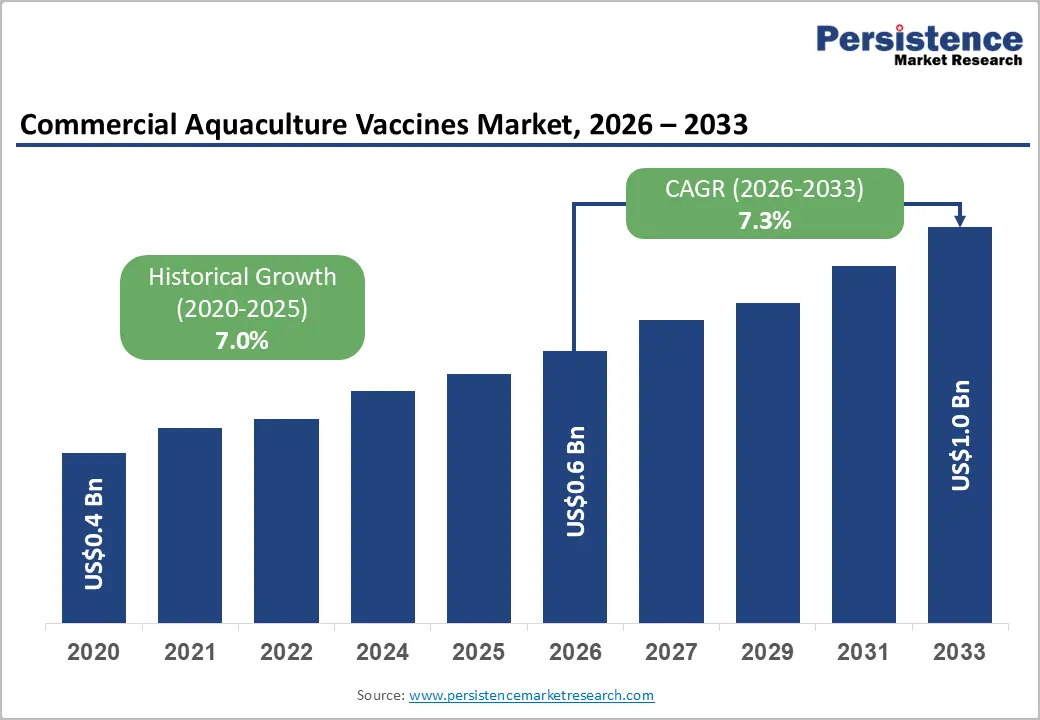

The global commercial aquaculture vaccines market size is likely to be valued at US$0.6 billion in 2026 and is expected to reach US$1.0 billion by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the rapid expansion of aquaculture production, rising incidence of infectious diseases in farmed fish, and increasing emphasis on sustainable seafood production.

According to the 2024 report by the Food and Agriculture Organization, global fisheries and aquaculture production reached a record 223.2 million tonnes in 2022. Aquaculture production alone accounted for 94.4 million tonnes of aquatic animals, representing 51% of total aquatic animal production for the first time. The organization also reported that over 3 billion people depend on aquatic foods as a major protein source, accelerating the need for effective fish disease prevention and vaccination programs in commercial aquaculture systems.

Key Industry Highlights:

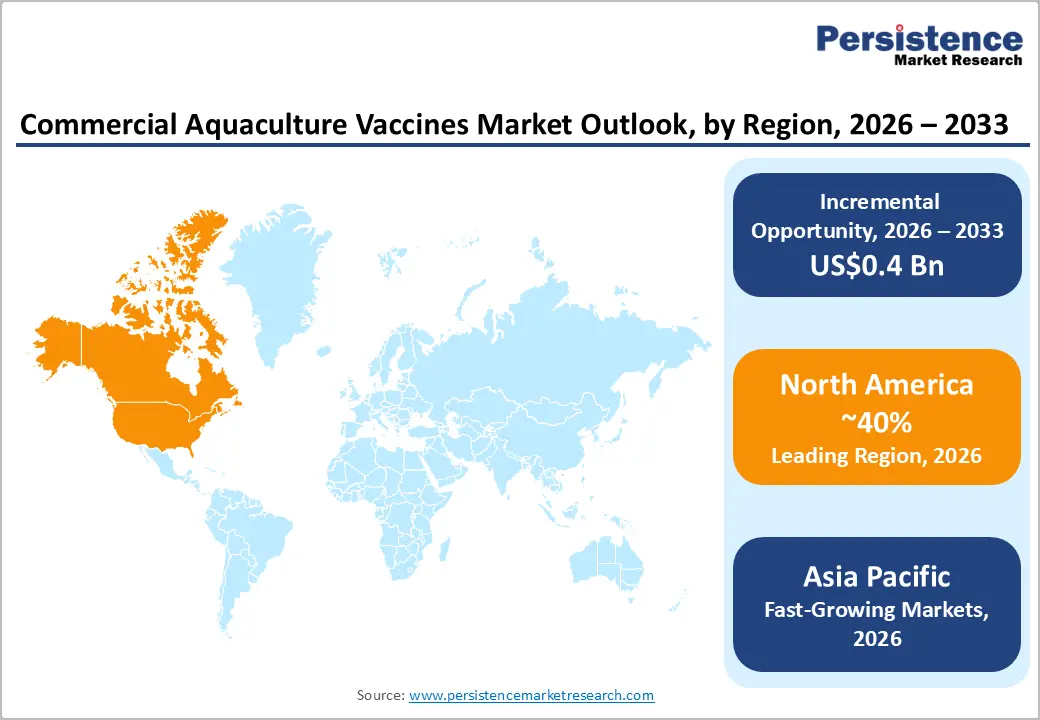

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong U.S. leadership in aquaculture innovation, regulatory support, and advanced fish health management practices.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by large-scale aquaculture production, expanding commercial fish farming, and increasing adoption of disease prevention solutions.

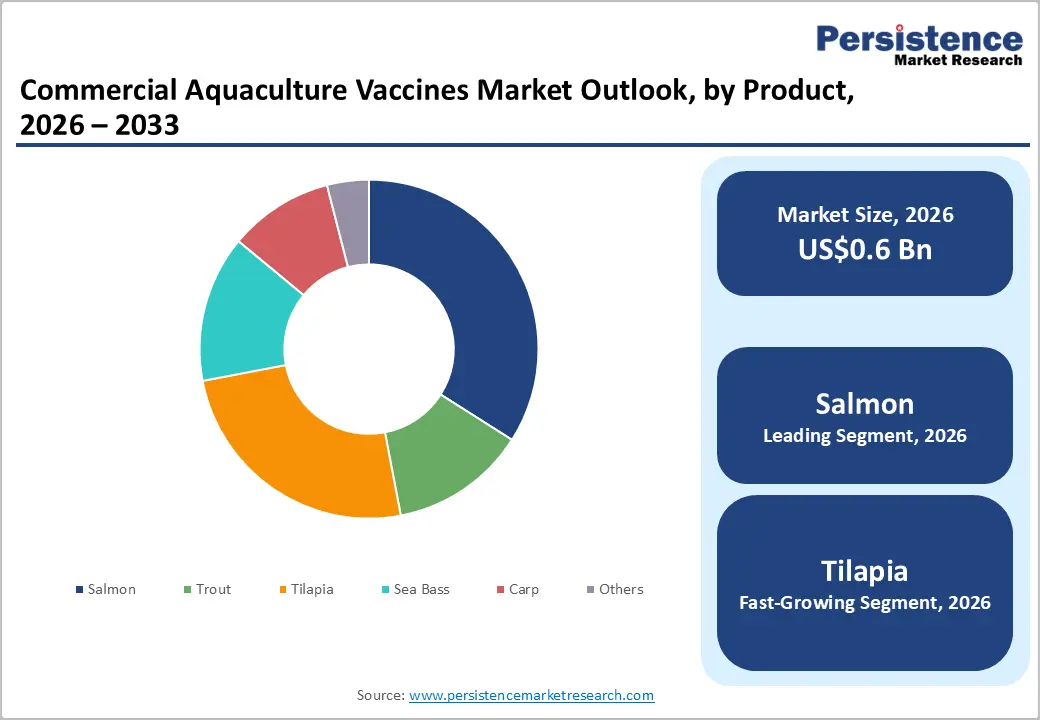

- Leading Vaccine: Inactivated vaccines are projected to represent the leading vaccine in 2026, accounting for 70% of the revenue share, due to their strong safety and widespread use in finfish farming.

- Leading Species: Salmon is anticipated to be the leading species, accounting for over 60% of the revenue share in 2026, supported by intensive farming and established vaccination practices.

- Key Opportunity: The key market opportunity in the commercial aquaculture vaccines market lies in the growing adoption of advanced oral, immersion, and DNA vaccines to support sustainable large-scale aquaculture production while reducing antibiotic dependency.

DRO Analysis

Driver - Rising Prevalence of Infectious Diseases in Aquaculture and Shift Away from Antibiotics

Diseases such as vibriosis, furunculosis, infectious salmon anemia, and streptococcosis continue to cause significant economic losses for aquaculture producers by reducing fish survival rates and productivity. Rising seafood demand has encouraged high-density farming practices, which accelerate disease transmission among aquatic species, including salmon, trout, carp, and tilapia.

Governments and regulatory agencies are also strengthening restrictions on antibiotic usage in aquaculture because of antimicrobial resistance concerns, encouraging producers to adopt preventive vaccination strategies that improve fish health management and sustainability. The transition away from antibiotics has significantly increased the adoption of commercial aquaculture vaccines across developed and emerging aquaculture economies.

Vaccination programs are now widely integrated into salmon farming operations in Norway, Chile, Canada, and Scotland, where disease prevention remains critical for maintaining export quality standards. Technological improvements in injectable, immersion, and oral vaccines are helping farmers achieve broader disease protection with reduced environmental impact. Consumer demand for antibiotic-free seafood products is also encouraging aquaculture companies to strengthen biosecurity and preventive healthcare measures.

Restraint - Limited Awareness and Adoption Among Small-Scale Farmers

Many small farmers continue relying on traditional fish farming practices with limited access to veterinary guidance, disease diagnostics, and modern healthcare technologies. The lack of technical knowledge regarding vaccine administration, storage requirements, and long-term economic benefits reduces confidence in adopting vaccination programs. In several rural aquaculture regions, inadequate cold-chain infrastructure and poor distribution networks further restrict vaccine accessibility.

Cost sensitivity among small and medium aquaculture operators also limits widespread vaccine adoption despite increasing disease outbreaks in farmed fish populations. Many farmers prioritize immediate production expenses over preventive healthcare investments, particularly in low-margin aquaculture sectors such as carp and tilapia farming. Inconsistent disease surveillance systems and limited government support programs slow awareness regarding vaccination benefits.

Opportunity - Technological Convergence in Oral and Immersion Vaccines

Traditional injectable vaccines remain effective but are labor-intensive and stressful for fish during large-scale vaccination procedures. Oral and immersion vaccines offer easier mass administration, reduced handling stress, and improved operational efficiency for commercial aquaculture farms. These technologies are gaining importance in high-volume species such as tilapia, carp, and shrimp, where manual injection is often impractical.

Continuous progress in biotechnology, nanotechnology, and antigen delivery systems is improving vaccine stability, immune response, and disease protection, encouraging wider adoption across intensive aquaculture production environments. The growing integration of advanced vaccine platforms with precision aquaculture technologies is accelerating market expansion significantly.

Companies are investing in recombinant vaccines, encapsulation technologies, and bioengineered oral formulations that improve vaccine absorption and long-lasting immunity in aquatic species. Immersion vaccination methods are also becoming increasingly attractive for hatcheries and juvenile fish production because they simplify large-scale immunization processes.

Category-wise Analysis

Vaccine Insights

Inactivated vaccines are expected to account for 70% of revenue in 2026, driven by its proven safety profile, strong regulatory acceptance, and broad effectiveness against bacterial infections in farmed fish species. These vaccines are widely used across salmon, trout, and sea bass farming because they provide stable immunity without the risk of pathogen replication. A notable example includes PHARMAQ, a subsidiary of Zoetis, which supplies inactivated vaccines for salmon aquaculture and supports disease management programs.

DNA vaccines are likely to represent the fastest-growing segment, supported by increasing demand for advanced protection against viral diseases in intensive fish farming systems. These vaccines provide targeted immune responses, improved biosafety, and reduced risk of pathogen reversion compared with conventional vaccine technologies. For example, the DNA vaccine developed against infectious hematopoietic necrosis virus in salmon farming, which demonstrated effective viral disease protection.

Species Insights

Salmon is projected to lead the market, capturing around 60% of the revenue share in 2026, supported by the species’ high commercial value, intensive farming practices, and well-established vaccination programs across Europe and North America. Commercial salmon producers increasingly rely on advanced vaccination schedules to reduce antibiotic dependence and comply with strict seafood safety regulations in export markets. For instance, the use of multivalent salmon vaccines by PHARMAQ in Norwegian aquaculture operations, where integrated vaccination programs are widely implemented to control diseases.

Tilapia is likely to be the fastest-growing species, due to sustainability concerns, cost efficiency, expanding freshwater aquaculture production, and increasing disease pressures. Oral and immersion vaccines are gaining importance in tilapia farming because they support easier mass administration in high-volume production systems. For example, the increasing use of Streptococcus agalactiae vaccines in tilapia farms, where commercial vaccination programs are helping producers improve fish survival rates.

Pathogen Insights

Bacterial pathogens are expected to lead the commercial aquaculture vaccines market, accounting for 45% share in 2026, supported by the widespread occurrence of bacterial diseases in intensive aquaculture environments and the strong effectiveness of existing vaccine technologies against these infections. A notable example includes the widespread use of Vibrio vaccines in salmon farming operations across Norway and Chile, where bacterial disease prevention remains essential for maintaining fish health.

Viral pathogens are likely to represent the fastest-growing segment, supported by rising concerns regarding severe viral outbreaks in high-density fish farming systems worldwide. Biotechnology innovations, including DNA vaccines, recombinant vaccines, and gene-based immunization platforms, are driving rapid progress in viral disease management within the aquaculture industry. For example, the adoption of DNA vaccines against Infectious Salmon Anemia and Infectious Hematopoietic Necrosis Virus in salmon aquaculture, where advanced viral vaccines are supporting disease control strategies and helping producers strengthen sustainable fish farming operations.

Regional Insights

North America Commercial Aquaculture Vaccines Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, supported by increasing emphasis on sustainable seafood production, disease prevention, and reduced antibiotic usage across commercial fish farming operations. For example, Zoetis-owned PHARMAQ, which continues to expand fish vaccine technologies and health management solutions for salmon farming operations.

U.S. Commercial Aquaculture Vaccines Market Trends

The U.S. dominates the regional market, driven by rising demand for sustainable seafood and increasing focus on advanced fish health management systems. Salmonid farming and freshwater aquaculture operations are increasingly adopting vaccination programs to minimize disease-related losses. Biotechnology companies in the country are investing in innovative DNA vaccines and precision aquaculture solutions for disease prevention.

Canada Commercial Aquaculture Vaccines Market Trends

Canada is a significant market for commercial aquaculture vaccines, supported by its strong Atlantic salmon farming industry and focus on fish disease prevention. The country is actively strengthening vaccination strategies to address bacterial and viral infections affecting marine aquaculture operations. Canadian aquaculture producers are increasingly adopting preventive healthcare technologies to improve export-quality seafood production.

Europe Commercial Aquaculture Vaccines Market Trends

Europe is likely to be a significant market for commercial aquaculture vaccines in 2026, due to strong regulatory frameworks, established salmon farming industries, and extensive adoption of preventive fish healthcare solutions. A notable example includes HIPRA, which continues expanding aquatic vaccine research and fish health technologies.

U.K. Commercial Aquaculture Vaccines Market Trends

The U.K. is a significant market for commercial aquaculture vaccines, supported by its established salmon farming industry and continuous investments in fish health management technologies. Scotland remains a major hub for Atlantic salmon production, where disease prevention is critical for maintaining seafood quality and export performance.

Germany Commercial Aquaculture Vaccines Market Trends

Germany dominates the regional market due to rising interest in sustainable seafood production and freshwater fish farming expansion. The country is focusing on strengthening biosecurity and fish health management practices in trout and carp farming systems. German biotechnology firms and research institutes are actively working on innovative aquatic disease management technologies.

Asia Pacific Commercial Aquaculture Vaccines Market Trends

The Asia Pacific region is likely to be the fastest-growing region in commercial aquaculture vaccines in 2026. Its large-scale aquaculture production, increasing seafood consumption, and rising disease outbreaks in intensive fish farming systems. For instance, Virbac continues strengthening aquatic animal health solutions and fish vaccine research in Asia Pacific through expanding aquaculture partnerships and disease prevention technologies.

China Commercial Aquaculture Vaccines Market Trends

China dominates the regional market, supported by its massive aquaculture production capacity and increasing focus on fish disease management. The country is expanding vaccination programs across carp, tilapia, and marine fish farming operations to improve productivity and reduce economic losses from disease outbreaks.

India Commercial Aquaculture Vaccines Market Trends

India is a significant market for commercial aquaculture vaccines, due to rapid expansion in freshwater aquaculture and rising demand for disease management solutions. Carp, tilapia, and shrimp farming activities are increasing significantly across several aquaculture-producing states. Disease outbreaks affecting freshwater fish production are encouraging farmers to adopt preventive healthcare practices and improved vaccination strategies.

Competitive Landscape

The global commercial aquaculture vaccines market exhibits a moderately fragmented structure, driven by increasing demand for sustainable aquaculture practices, rising disease outbreaks in farmed fish populations, and growing regulatory pressure to reduce antibiotic usage in seafood production.

With key leaders including Zoetis, HIPRA, Merck & Co., Inc., Virbac, and Vaxxinova, the competitive environment continues evolving through strategic acquisitions, biotechnology investments, and expansion into emerging aquaculture regions. Recent developments include HIPRA’s launch of ICTHIOVAC VR/PD vaccine for sea bass and MSD Animal Health’s expansion of its aquaculture vaccine portfolio through acquisition activities, strengthening fish health capabilities.

Key Industry Developments:

- In April 2025, BioVaxys Technology Corp. and SpayVac for Wildlife expanded their licensing agreement into commercial aquaculture, advancing the development of single-dose immunocontraceptive vaccines for farm-raised salmon and trout as an alternative to traditional fish sterilization methods.

- In June 2025, HIPRA launched ICTHIOVAC® VR/PD, an injectable vaccine targeting vibriosis and pasteurellosis in sea bass, strengthening its commercial aquaculture vaccine portfolio with advanced AQUAMUN adjuvant technology for improved fish disease protection.

Companies Covered in Commercial Aquaculture Vaccines Market

- Ceva Biovac

- Zoetis (PHARMAQ)

- Vaxxinova

- Barramundi Asia Pte Ltd. (UVAXX Asia)

- HIPRA

- AniCon Labor GmbH

- sanphar (ipeve)

- Kennebec River Biosciences

- Merck & Co. Inc.

- Tecnovax

- HIPRA

- Virbac

Frequently Asked Questions

The global commercial aquaculture vaccines market is projected to reach US$0.6 billion in 2026.

Rising infectious disease outbreaks in farmed fish and increasing demand for sustainable antibiotic-free aquaculture practices are driving the commercial aquaculture vaccines market.

The commercial aquaculture vaccines market is expected to grow at a CAGR of 7.3% from 2026 to 2033.

Key market opportunities lie in the development of oral and DNA vaccines, the expansion of aquaculture production in Asia Pacific region, and the growing adoption of advanced fish health management technologies.

Ceva Biovac, Zoetis (PHARMAQAS), Vaxxinova, Barramundi Asia Pte Ltd, and AniCon Labor GmbH are the leading players.