- Non-food Packaging

- Water Soluble Pods Packaging Market

Water Soluble Pods Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Water Soluble Pods Packaging Market by Product Type (Multi-Chamber Water Pods, Dual-Layer Water Pods, Others), Application (Laundry Detergent Pods, Household Products, Others), Material, and Regional Analysis for 2026 - 2033

Water Soluble Pods Packaging Market Size and Trends Analysis

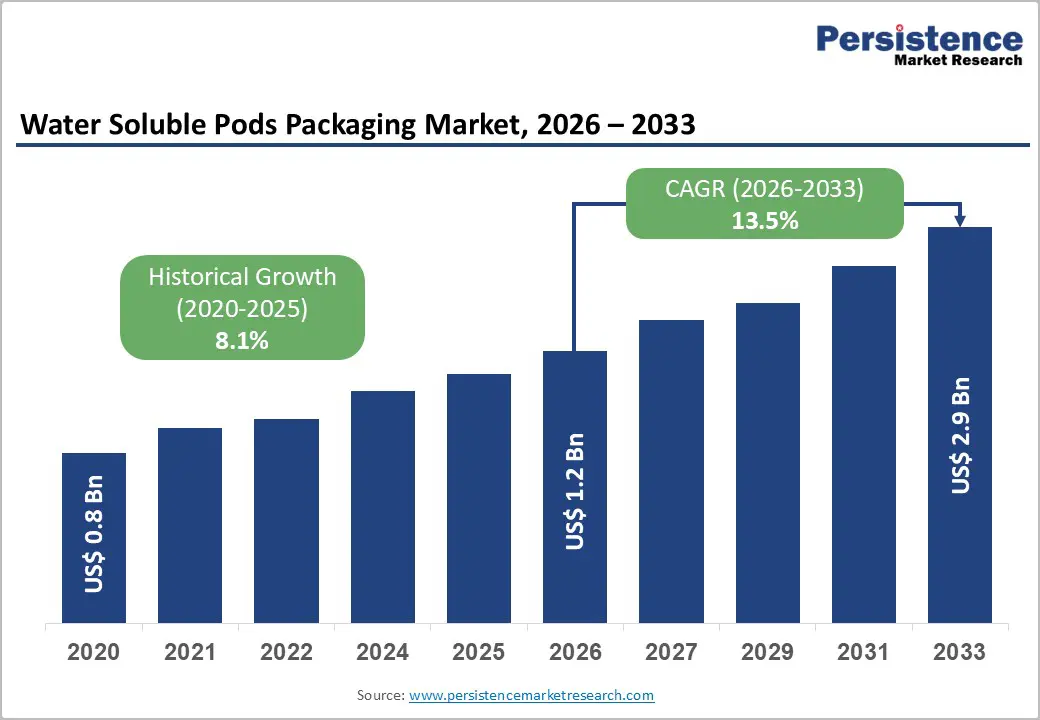

The global water soluble pods packaging market size is likely to be valued at US$1.2 billion in 2026 and is expected to reach US$2.9 billion by 2033, growing at a CAGR of 13.5% between 2026 and 2033, driven by structural adoption of unit-dose detergent formats, tightening packaging sustainability regulations across North America and Europe, and advancements in biodegradable polyvinyl alcohol (PVA) and bio-based polymer films.

Increasing demand for dosing precision, reduced packaging waste, and compatibility with cold-water washing cycles further strengthen commercial viability. The market outlook reflects convergence between regulatory compliance, material science innovation, and evolving consumer purchasing behavior.

Key Industry Highlights

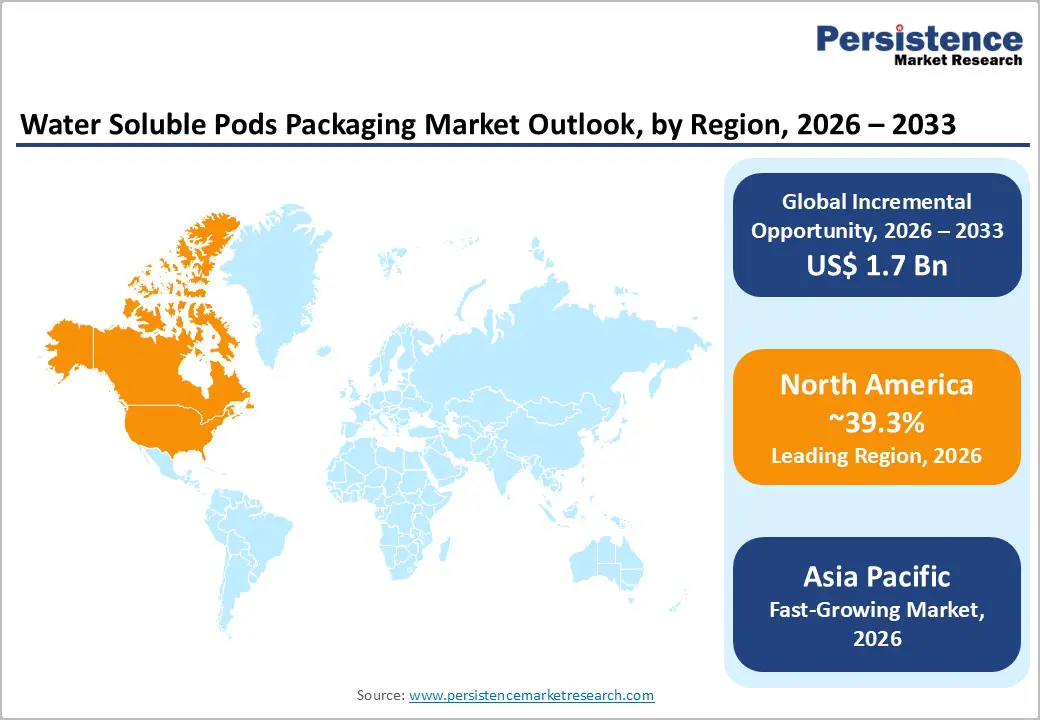

- Leading Region: North America is projected to hold approximately 39.3% of the market share, driven by high U.S. detergent pod penetration, premium multi-chamber adoption, and strong retail/e-commerce infrastructure.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region, supported by rapid urbanization, manufacturing scale advantages, and expanding household cleaning demand across China, India, and ASEAN markets.

- Investment Plans: Companies are investing in advanced PVA film capacity, biodegradable polymer R&D, and dual-layer/multi-chamber pod technologies, aligned with sustainability regulations and improvements in cold-water dissolution performance.

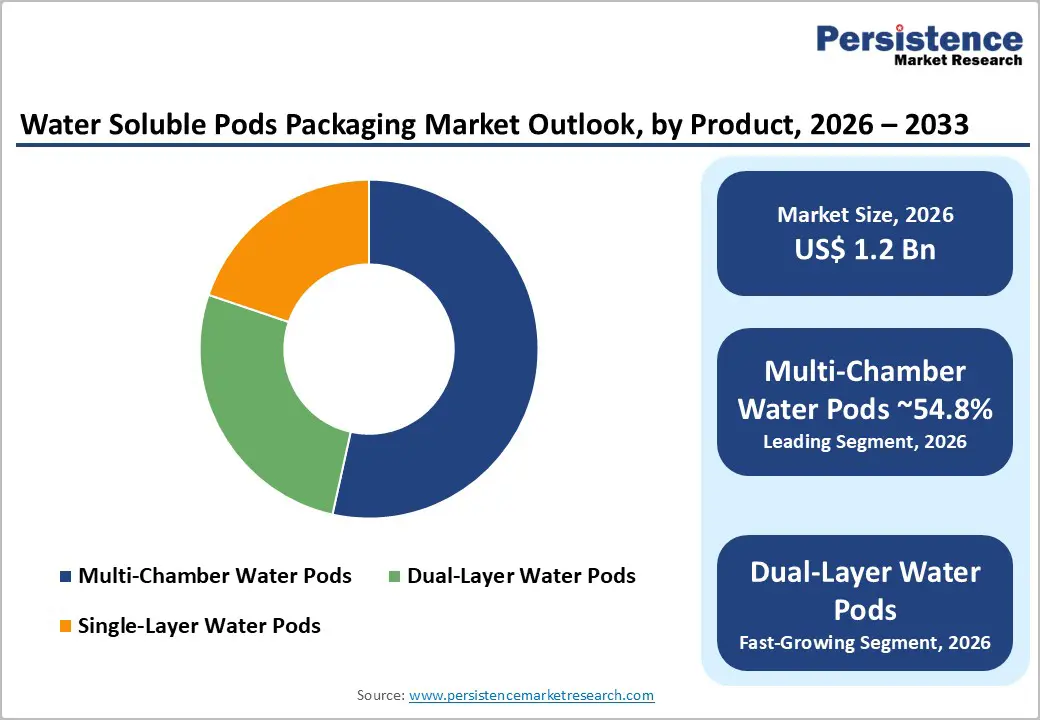

- Dominant Product Type: Multi-chamber water pods are anticipated to lead with an anticipated 54.8% market share, driven by superior formulation stability and premium detergent applications.

- Leading Application: Detergents are estimated to account for approximately 55.3% of the total market, with laundry detergent pods as the primary driver of demand.

| Key Insights | Details |

|---|---|

| Water Soluble Pods Packaging Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 2.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Acceleration toward Sustainable Packaging

Government authorities across developed economies continue tightening restrictions on conventional single-use plastics. The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective in a phased rollout through 2030, establishes binding requirements for recyclability, waste reduction, and material transparency. Similar regulatory initiatives in U.S. states emphasize extended producer responsibility (EPR) and restrictions on PFAS in packaging materials. These policy developments directly incentivize the adoption of dissolvable packaging formats. Water-soluble pods reduce secondary packaging needs and align with corporate sustainability goals tied to Scope 3 emissions reduction. Procurement policies in institutional cleaning sectors increasingly favor low-residue, reduced-waste formats. Regulatory certainty provides long-term visibility for investment, encouraging film manufacturers and converters to expand capacity.

Advancements in Polyvinyl Alcohol (PVA) and Film Engineering

Polyvinyl alcohol (PVA) remains the dominant material for water-soluble films due to its controlled solubility, tensile strength, and compatibility with automated filling systems. Ongoing improvements in polymerization processes have enhanced cold-water dissolution performance, critical for energy-efficient washing trends in North America and Europe. Certain grades of PVA are recognized in regulatory inventories for food-contact and pharmaceutical applications, reducing compliance friction for consumer product manufacturers. Newer film grades demonstrate improved seal integrity and barrier properties, supporting multi-chamber and dual-layer pod designs. These technical improvements reduce the risk of rupture, improve transport durability, and expand applicability beyond laundry to household, personal care, and agricultural formulations.

Consumer Preference for Precision and Convenience

Unit-dose packaging addresses three persistent consumer concerns: dosing accuracy, product waste, and convenience. Single-dose pods eliminate overuse of liquid detergents, improving wash consistency and reducing product waste. Retailers benefit from compact packaging, simplified shelf merchandising, and reduced leakage claims. E-commerce growth reinforces pod adoption. Compact, spill-resistant formats reduce returns and improve transport reliability. Subscription-based purchasing models favor consistent-dose formats, thereby strengthening repeat-purchase behavior. Institutional and commercial cleaning sectors increasingly specify pods to standardize cleaning protocols and minimize misuse. This structural shift in demand supports long-term revenue stability for pod packaging suppliers.

Barrier Analysis - Raw Material and Production Cost Volatility

PVA production depends on vinyl acetate monomer and energy-intensive polymerization processes. Feedstock price fluctuations and energy cost volatility can compress converter margins. During periods of raw material inflation, film manufacturers are likely to face margin pressure of approximately 2-6 percentage points. Capital expenditure requirements for advanced multi-layer or multi-chamber pod production lines are significant, with typical payback periods extending between three and six years. These financial considerations may slow adoption among smaller brands or private-label manufacturers operating on cost-sensitive models.

End-of-Life Perception and Wastewater Treatment Variability

Although PVA dissolves in water, biodegradation outcomes depend on wastewater treatment infrastructure and concentration levels. Differences in municipal treatment standards across regions create compliance and communication challenges. Consumer confusion between “soluble” and “biodegradable” terminology presents reputational risk. Regulatory agencies increasingly scrutinize environmental claims, requiring third-party testing and documentation. Brands must invest in lifecycle assessments and transparent labeling to mitigate potential liability exposure.

Opportunity Analysis - Asia Pacific Industrial and Consumer Expansion

Asia Pacific represents the fastest-growing regional market, driven by urbanization, expanding middle-class populations, and retail modernization. Converting even 10-15% of conventional flexible detergent packaging to pod formats across major APAC economies could generate a multi-hundred-million-dollar incremental opportunity over the forecast period. Growth in commercial cleaning across healthcare, hospitality, and industrial sectors further strengthens demand. Localized production partnerships can improve cost competitiveness while supporting regional regulatory alignment.

Premiumization through Multi-Chamber and Dual-Layer Pods

Multi-chamber and dual-layer pods enable separation of incompatible actives and timed-release mechanisms. These advanced formats support concentrated formulations and specialty applications, including personal care and certain agricultural inputs. Premium pod formats can command a 8-12% premium over single-layer alternatives. Investment in encapsulation technologies and proprietary sealing systems enhances differentiation and intellectual property defensibility.

Bio-Based Polymer Development

Emerging bio-based polymer blends and modified PVA variants offer reduced dependence on fossil feedstocks and improved environmental performance. Adoption of biomass-content films supports corporate carbon reduction strategies and compliance with sustainability procurement frameworks. As regulatory definitions of biodegradable packaging evolve, early movers investing in certified bio-based materials can secure first-mover advantages in environmentally regulated markets.

Category-wise Analysis

Product Type Insight

Multi-chamber water pods are anticipated to account for approximately 54.8% of market share in 2026, supported by their functional superiority in detergent and specialty cleaning applications. These pods separate incompatible chemical components, such as surfactants, enzymes, bleaching agents, and fragrance boosters, until the point of use, preserving formulation stability and maximizing cleaning performance. This separation capability is particularly valuable for high-performance laundry detergents and industrial cleaning solutions where chemical compatibility is critical. The design supports premium detergent SKUs and improves consistency in cleaning efficacy across wash cycles. Major global detergent brands have widely adopted three-chamber configurations to combine stain removers, brighteners, and softening agents within a single unit-dose format. Manufacturers benefit from higher unit margins and strong product differentiation in competitive retail environments. Advanced lamination, precision dosing, and heat-sealing technologies enable scalable production with minimal risk of leakage. Multi-chamber pods are especially dominant in North America and Europe, where consumers demonstrate a higher willingness to pay for performance-enhanced and convenience-oriented products.

Dual-layer pods are likely to be the fastest-growing product category, driven by enhanced mechanical durability and controlled dissolution characteristics. An outer protective layer improves resistance to humidity and transport-related stress, while the inner layer ensures accurate timed release of active ingredients. This structure makes dual-layer formats well-suited for cold-water detergent formulations and concentrated cleaning chemistries. Compared with complex multi-chamber systems, dual-layer pods require less intricate tooling and lower capital investment, reducing entry barriers for mid-sized converters. Recent product introductions in cold-wash laundry detergents and bathroom cleaning concentrates demonstrate strong commercial traction. Growth is particularly notable in the Asia Pacific, where cost-sensitive markets favor technically enhanced yet production-efficient pod formats.

Application Insights

Detergents are expected to account for approximately 55.3% of the market in 2026, with laundry detergent pods as the primary revenue driver. Unit-dose packaging addresses dosing inconsistencies, minimizes product waste, and reduces secondary packaging relative to bulk liquid and powder formats. Consumers value the convenience of pre-measured doses, particularly in urban households and subscription-based purchasing models. Major household brands have positioned detergent pods as premium offerings, often incorporating multi-chamber technology to combine stain removal, fabric care, and fragrance enhancement. Retailers prioritize pod SKUs for premium shelf placement and compact packaging displays that improve inventory efficiency. Institutional cleaning contracts, including hospitality and healthcare facilities, increasingly specify standardized dosing formats to reduce operational variability and improve compliance with cleaning protocols. These structural advantages reinforce detergents as the anchor application within the market.

Household cleaning products are likely to be the fastest-growing application segment. Growth is driven by product innovation across surface cleaners, bathroom disinfectants, glass cleaners, and concentrated refill systems. Water-soluble pods allow brands to offer highly concentrated formulations that consumers dilute at home, reducing plastic bottle usage and transportation emissions. Several brands have introduced pod-based multi-surface cleaning kits and refill tablets packaged in dissolvable films to support sustainability positioning. The format aligns well with direct-to-consumer and e-commerce distribution, where compact, spill-resistant packaging lowers logistics costs. Household applications also enable greater SKU diversification than the mature laundry category, supporting premium pricing strategies and improved margin realization for both brand owners and packaging converters.

Regional Insights

North America Water Soluble Pods Packaging Market Trends - Innovation-Led Detergent Pod Adoption and Advanced PVA Film Demand

North America is expected to lead, accounting for a market share of 39.3% in 2026, supported by strong detergent pod penetration in the U.S. and a well-developed retail and e-commerce ecosystem. The U.S. market has achieved high household adoption of unit-dose laundry detergents, led by brands such as Tide PODS (Procter & Gamble), Gain Flings, and Persil Discs (Henkel). These products rely heavily on multi-chamber PVA film technology, reinforcing demand for advanced soluble film packaging. The region benefits from mature distribution infrastructure, including subscription-based delivery models through major retailers and online platforms, which favor compact, spill-resistant packaging formats.

Key growth drivers include high disposable income levels, sustainability-focused procurement policies, and a robust innovation ecosystem that links chemical suppliers, film producers, and consumer goods companies. Corporate sustainability commitments from companies such as Procter & Gamble and Unilever have accelerated the shift toward concentrated formulations and reduced secondary plastic packaging. At the material level, suppliers such as Kuraray America and Sekisui Specialty Chemicals maintain production and technical support operations that serve detergent and industrial customers across the region. State-level environmental regulations, such as restrictions on PFAS and evolving labeling transparency standards in California and New York, directly influence material selection and sustainability claims.

Investment activity has centered on expanding advanced film production capacity and launching dual-layer and cold-water-optimized pod formats. Recent product upgrades in cold-water detergent lines have increased demand for improved dissolution films that perform in energy-efficient wash cycles. These developments reinforce North America’s position as a premium, innovation-led market where performance differentiation and regulatory alignment drive steady value growth.

Europe Water Soluble Pods Packaging Market Trends - Regulation-Driven Sustainable Packaging and Cold-Water Performance Focus

Europe’s market growth is anchored in regulatory harmonization and strong sustainability mandates. The EU Packaging and Packaging Waste Regulation (PPWR) has accelerated packaging redesign efforts across consumer goods categories, encouraging the adoption of recyclable, reusable, and dissolvable formats. Major European detergent brands such as Ariel (P&G) and Persil (Henkel) have continued to expand their concentrated pod offerings, which align with circular-economy principles and reduce plastic usage. These product transitions increase demand for high-performance PVA films engineered for consistent dissolution and minimal residue.

Germany remains a leader in industrial and institutional cleaning demand, supported by strict environmental compliance standards and large-scale commercial procurement. The U.K. drives retail innovation, with supermarket chains actively promoting refill solutions and concentrated cleaning formats. France and Spain are experiencing rapid growth in household pod adoption, driven by sustainability awareness campaigns and urban consumers' preference for convenience. Cold-water washing trends across Western Europe further increase demand for advanced film grades that dissolve at lower temperatures, consistent with regional energy-saving practices.

European material suppliers, including Kuraray’s European operations and specialty film producers in Italy and Japan serving the EU market, have invested in research and certification of biodegradable polymers to meet evolving regulatory thresholds. Companies are also allocating capital to third-party compliance-testing infrastructure to validate biodegradability and wastewater-compatibility claims. These developments reinforce Europe’s role as a regulation-driven innovation hub where environmental performance and compliance credibility are central to competitive positioning.

Asia Pacific Water Soluble Pods Packaging Market Trends - Rapid Urbanization, Manufacturing Scale, and Film Technology Expansion

Asia Pacific is the fastest-growing regional market, driven by rapid urbanization, rising middle-class purchasing power, and the region’s strong manufacturing base for chemicals and specialty films. China is the largest contributor to volume growth, supported by the expansion of domestic detergent brands and by multinational players increasing localized production. Companies such as Nice Group (China) and multinational firms, including Procter & Gamble, have expanded pod offerings in urban retail and e-commerce channels, responding to growing consumer demand for convenience and compact packaging.

Japan plays a critical role in technological innovation, with companies such as Aicello Corporation, Mitsubishi Chemical Group, and Sekisui Chemical leading advancements in high-performance PVA films and biomass-content grades. These technological capabilities influence pod production not only domestically but across export markets. Japanese film innovation, particularly improvements in cold-water solubility and film strength, supports broader regional adoption in varied climate conditions.

India and the ASEAN countries are experiencing rapid growth in the household and institutional cleaning segments, driven by retail modernization and the penetration of digital commerce. Indian manufacturers such as Arrow Greentech are scaling up production of water-soluble films to serve both domestic detergent brands and export markets. Cost-effective manufacturing and contract packaging capabilities in China and Southeast Asia reduce production expenses, accelerating regional competitiveness. Strategic local partnerships help international brands navigate diverse regulatory frameworks and wastewater standards, improving speed to market.

Competitive Landscape

The global water soluble pods packaging market demonstrates moderate concentration at the material supply level and higher fragmentation among converters. Major PVA producers control meaningful revenue shares, while regional converters compete on cost-efficiency and customer proximity. Vertical integration strategies, combining resin production, film extrusion, and pod conversion, are increasingly common among leading players. Market leaders focus on material innovation, capacity expansion in Asia Pacific, and premium pod engineering. Differentiation centers on proprietary film grades, regulatory validation support, and advanced multi-layer encapsulation capabilities.

Key Industry Developments

- In August 2025, Cortec Corporation introduced Eco Works 100, a 100% USDA-certified biobased and industrially compostable water-soluble packaging film, reinforcing sustainable material offerings for detergents, cleaners, and agricultural pods and advancing eco-friendly packaging adoption.

- In July 2025, TerraSafe completed a merger with DisSolves, a dissolvable film packaging startup, and subsequently launched two plastic-free products, including water-soluble laundry detergent sheets and edible pod packaging to expand sustainable alternatives to traditional plastics.

Companies Covered in Water Soluble Pods Packaging Market

- Mitsubishi Chemical Group Corporation

- Sekisui Chemical Co., Ltd.

- Kuraray Co., Ltd.

- Aicello Corporation

- MonoSol LLC

- Arrow Greentech Ltd.

- Ecopol S.p.A.

- Changzhou Water Soluble Co., Ltd.

- Jiangmen Proudly Water-Soluble Plastic Co., Ltd.

- Cortec Corporation

- Aquapak Polymers Ltd.

- AMC (UK) Ltd.

- Soltec Development Corp.

- Guangzhou Liby Enterprise Group Co., Ltd.

- Nice Group Co., Ltd.

- Procter & Gamble (P&G)

- Henkel AG & Co. KGaA

- Unilever PLC

Frequently Asked Questions

The global water soluble pods packaging market is valued at US$1.2 billion in 2026.

The water soluble pods packaging market is expected to reach US$2.9 billion by 2033.

Key trends include a shift toward multi-chamber and dual-layer pod designs for enhanced performance and premium positioning and adoption of biodegradable and bio-based PVA film grades to meet sustainability regulations.

By product type, multi-chamber water pods hold the leading share, primarily due to their superior formulation stability and performance in premium detergent applications. By application, detergents account for approximately 55.3% of market share, with laundry pods representing the core demand driver.

The water soluble pods packaging market is projected to grow at a CAGR of 13.5% between 2026 and 2033.

Major companies include Mitsubishi Chemical Group Corporation, Sekisui Chemical Co., Ltd., Kuraray Co., Ltd., Aicello Corporation, and Procter & Gamble (P&G).