- Home Appliances

- Water Heater Market

Water Heater Market Size, Share, and Growth Forecast 2026 – 2033

Water Heater Market by Product type (Vibrating Sieves, Centrifugal Sieves, Rotary Sieves and Others), by Sieves Size (Coarse Sieves, Medium Sieves and Others), and End- user (Pharmaceutical, Food and Beverage, Chemical and Others) Regional Analysis for 2026 – 2033

Market Overview

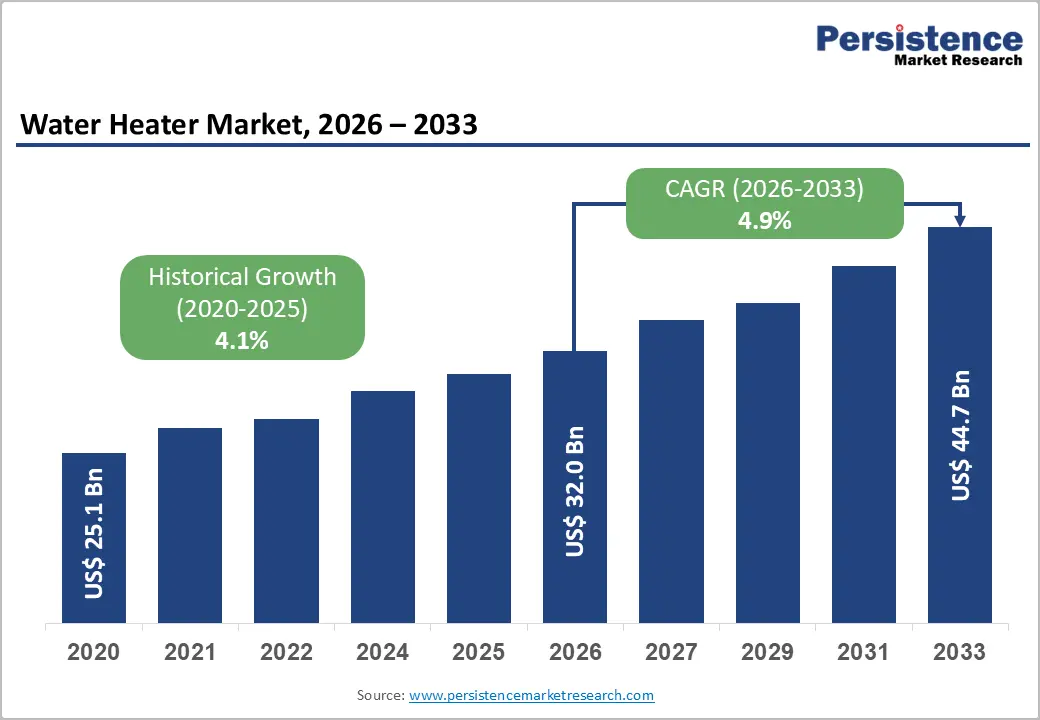

The global Water Heater Market size was valued at US$ 32.0 Bn in 2026 and is projected to reach US$ 44.7 Bn by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

Growth is anchored in rising residential electrification, stricter efficiency standards, and sustained construction activity across emerging and developed markets. Regulators such as the U.S. Department of Energy (DOE) estimate that water heating accounts for around 13% of residential energy use, making high efficiency and heat pump-based systems central to decarbonization and household cost reduction, which in turn accelerates replacement of legacy water heating systems.

Key Market Highlights

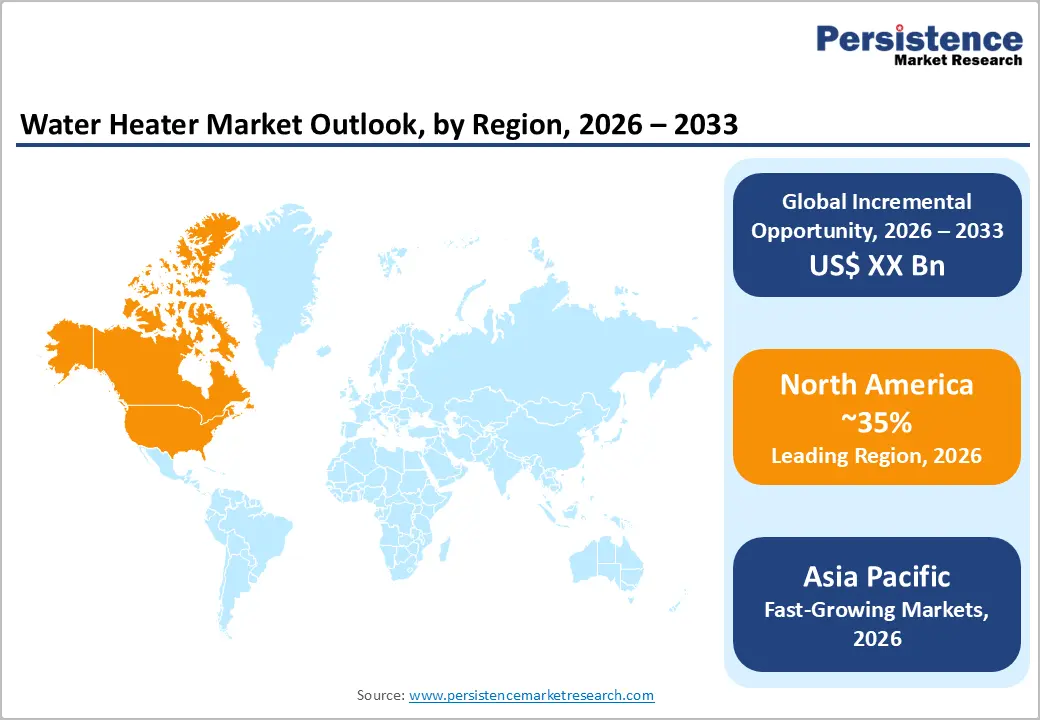

- Leading region: North America leads the Water Heater Market by value, supported by a large installed base, frequent replacement cycles, stringent DOE efficiency standards, and active innovation in smart and heat pump water heaters among established U.S. manufacturers.

- Fastest growing region: Asia Pacific is the fastest growing market, propelled by rapid urbanization, rising middle class incomes, high residential construction growth in China, India, and ASEAN, and increasing electrification and appliance penetration rates.

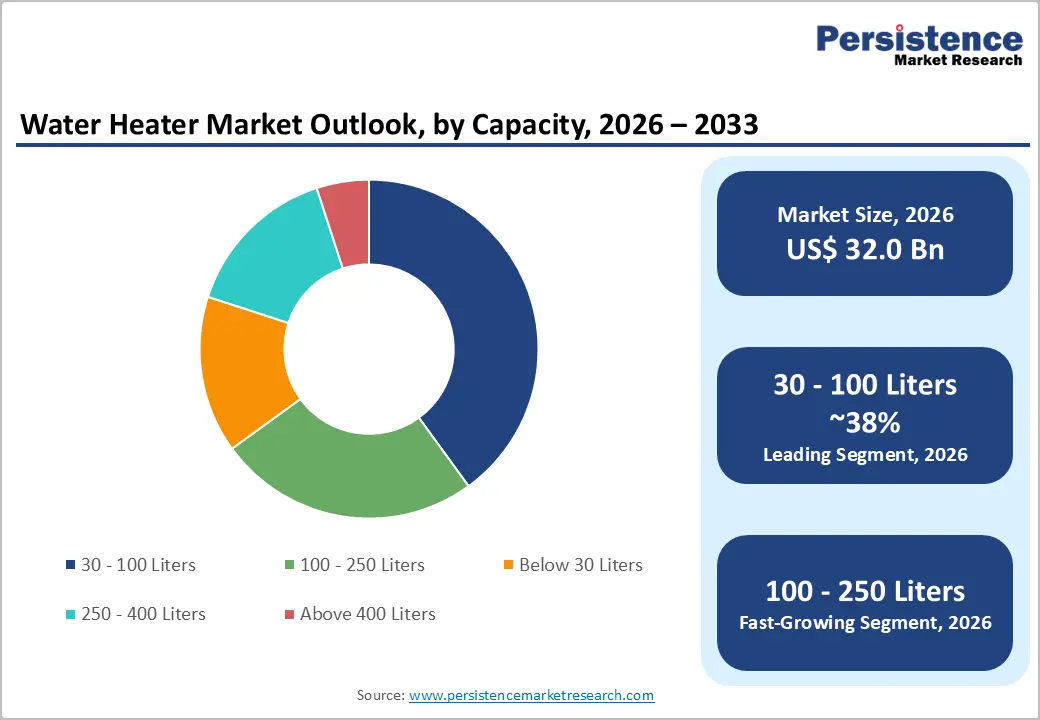

- Dominant segment: The 30 – 100 Liters capacity band dominates by volume, with around 38% share, as it best matches typical residential hot water demand profiles and is widely adopted in apartments and single family homes globally.

- Fastest growing segment: Heat pump and hybrid water heating technologies, often configured as storage systems, are the fastest growing sub segment, driven by climate policies, incentives, and significantly higher efficiency compared with conventional resistance and gas units.

- Key opportunity: Integration of smart, grid interactive water heaters that support demand response and pair with rooftop solar offers a major opportunity, enabling utilities and consumers to optimize energy use while meeting tightening decarbonization and building performance targets.

| Global Market Attributes | Key Insights |

|---|---|

| Water Heater Market Size (2026E) | US$ 32.0 Bn |

| Market Value Forecast (2033F) | US$ 44.7Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.1% |

Market Dynamics

Market Growth Drivers

Rapid Urbanization, Housing Stock Expansion, and Replacement Demand

Accelerating urbanization and rising incomes are driving installation and replacement of water heaters in both new and existing housing, particularly in Asia Pacific and parts of Latin America. The U.S. DOE notes that water heating typically represents about 12% of household energy consumption, making efficiency upgrades a high impact lever for both utilities and consumers. As construction of multi family housing and residential towers rises, especially in large metros where hot water access is a core amenity, builders increasingly specify energy efficient electric and gas storage units as standard.

Parallel growth in non esidential buildings hotels, hospitals, and educational facilities further reinforces demand, closely linked to broader building materials and Construction Chemicals Market trends for thermally efficient envelopes and plumbing systems that support optimized hot water distribution.

Policy Led Shift to High Efficiency and Heat Pump Technologies

Governments are tightening minimum efficiency standards and promoting heat pump and high efficiency electric water heaters through incentives, standards, and climate policies. The U.S. DOE finalized new residential water heater efficiency standards expected to save households about US$ 7.6 billion per year on energy and water bills and cut 332 million metric tons of CO emissions over 30 years of shipments, with most common electric units required to use heat pump technology.

In Europe, the European Commission and IEA highlight heat pumps as a key tool to cut gas use in buildings by at least 21 billion cubic meters annually, directly favoring electric and hybrid water heating solutions. These policies structurally shift demand toward advanced tankless, storage, and hybrid systems, underpinning long term market expansion.

Market Restraints

High Upfront Cost of Advanced and Heat Pump Systems

Despite lifecycle savings, high initial capital costs of heat pump and high efficiency condensing units remain a significant barrier for many households and small businesses. Studies on heat pump adoption show that while such systems can significantly cut operating expenses, payback times are still sensitive to local electricity and gas tariffs and available subsidies, limiting penetration among cost constrained consumers. In developing markets, basic gas and resistive electric storage heaters often remain preferred due to lower upfront prices, slowing the transition to premium, more efficient water heater technologies.

Grid, Fuel, and Infrastructure Constraints

The shift from gas to electric and heat pump water heaters can increase electricity demand and require reinforcement of local distribution networks, especially in dense urban areas with aging infrastructure. In regions where gas pipelines are well established and electricity prices are volatile, many consumers continue to favor conventional gas storage heaters despite efficiency trade offs. Furthermore, installers and contractors may lack training for newer hybrid and smart connected systems, creating soft infrastructure bottlenecks that delay broader adoption and limit near term growth in advanced product segments.

Market Opportunities

Acceleration of Heat Pump and Hybrid Water Heaters

Heat pump water heaters are one of the fastest growing segments as they can deliver 2–3 times higher efficiency than conventional electric resistance units by transferring rather than generating heat. The IEA and multiple national programs position heat pumps as central to net zero roadmaps, with projections indicating hundreds of millions of heat pump systems in operation globally by 2050, a portion of which will be dedicated to water heating. The residential end user segment is particularly attractive, with some studies indicating residential heat pump water heater CAGRs exceeding 15% in select markets, supported by incentives, building codes, and green building certifications that prefer low carbon heating solutions.

For established brands like A.O. Smith, Rheem Manufacturing Company, and Rinnai America Corporation, this creates a sizeable opportunity to scale premium hybrid and variable speed heat pump portfolios.

Smart, Connected, and Grid Interactive Water Heating

Digitalization and smart home adoption open new value pools in connected water heaters with Wi Fi, app based control, and grid interactive capabilities. Utilities in North America and Europe are increasingly piloting demand response programs that use water heaters as flexible thermal storage, shifting heating loads to off peak hours to balance grids with higher shares of renewables. Smart water heaters equipped with sensors and connectivity can optimize setpoints, detect leaks, and provide predictive maintenance alerts, improving user experience and lowering lifecycle costs.

For manufacturers such as Bosch Terotechnology Corp., Ariston Holding N.V., and Haier Inc., integrating connectivity, interoperability with home energy management systems, and over the air software updates represents a key differentiator and recurring revenue opportunity through service and extended warranties.

Category wise Insights

Capacity Outlook Analysis

The 30 - 100 Liters capacity segment holds the leading share of the global Water Heater Market, accounting for an estimated 38% of total unit demand due to its suitability for typical residential households and small commercial applications such as small offices and retail outlets. In many markets, this range matches the hot water needs of 2-4 person households, aligning with average dwelling sizes and daily per capita hot water usage, which IEA linked analyses in Europe estimate at around 24 liters per person per day. These units balance footprint, storage volume, and energy consumption and are widely available in electric, gas, and emerging heat pump configurations.

As urban housing projects and mid size apartments proliferate, especially in Asia Pacific, the 30–100-liter class is expected to remain the anchor capacity band for replacement and new installations.

Product Outlook Analysis

Electric water heaters constitute the dominant product segment, capturing roughly 55% of global market share, reflecting the widespread accessibility of electricity, flexibility of installation, and rapidly tightening efficiency policies favoring electric and heat pump technologies. Electrification of building heat is a key pillar in national decarbonization plans, and multiple jurisdictions are phasing out or restricting new fossil fuel-based heating in residential construction, structurally favoring electric storage, tankless, and hybrid water heaters.

Gas units retain strong positions in markets with abundant pipeline gas and legacy infrastructure, yet incremental growth is increasingly concentrated in electric and solar assisted systems, especially where rooftop photovoltaic adoption allows households to pair water heaters with onsite renewable generation.

Technology Analysis

Storage technology remains the leading segment, representing an estimated 60% of market share, driven by its entrenched installed base, relative simplicity, and ability to provide buffered hot water capacity for peak demand. Traditional tank type systems are familiar to installers and consumers, support both electric and gas energy sources, and are widely used from single family homes to hotels and institutional facilities. However, tankless and hybrid systems are gaining share, especially in new construction and premium retrofits, due to their compact footprint, On Demand capability, and higher efficiency.

Hybrid heat pump storage units combine storage benefits with high efficiency, positioning this sub segment for above average growth as regulatory standards tighten and whole home decarbonization strategies proliferate.

Application Analysis

The Residential segment is the largest application category, accounting for roughly 65% of global water heater demand, underpinned by the sheer scale of household installations and replacement cycles. The U.S. DOE estimates water heating contributes about 13% of annual residential energy use, rising even higher in colder climates, placing residential water heating at the center of household energy efficiency and climate strategies. Commercial applications including hospitality, healthcare, education, and foodservice represent around 25% of demand and tend to favor larger capacity storage and high recovery systems.

Industrial use, while smaller in unit volume, requires specialized high temperature and high capacity solutions, often integrated into process heating systems, creating opportunities for premium, application specific products from established manufacturers.

Regional Insights

North America Water Heater Market Trends

In North America, the United States leads regional demand, supported by a large installed base of legacy storage water heaters and active replacement cycles driven by new DOE efficiency standards and evolving state level building codes. Water heating accounts for around 8% of U.S. residential energy consumption, and the updated federal standards, effective for residential units by 2029, are expected to save households about US$ 7.6 billion per year and reduce 332 million metric tons of CO over 30 years. These regulations strongly encourage adoption of heat pump and high efficiency electric units in sizes commonly used in single family homes and multi family buildings.

The region also features a robust innovation ecosystem, with manufacturers like A.O. Smith, Rheem Manufacturing Company, Bradford White Corporation, and Rinnai America Corporation investing in smart, connected water heaters that integrate with home energy management systems and utility demand response programs. Pilot projects and electrification roadmaps, such as New England’s heating electrification forecasts, highlight water heating as a controllable load that can support renewable integration and peak load shaving.

Combined with ongoing residential construction and remodeling activity, this positions North America as a technology leader and early adopter of next generation electric and hybrid water heating solutions.

Europe Water Heater Market Trends

Europe exhibits strong momentum toward high efficiency and renewable compatible water heating as part of broader building decarbonization efforts and reduced dependency on imported gas. Countries such as Germany, the U.K., France, and Spain are tightening building performance standards and supporting adoption of heat pump technologies through subsidies and regulatory frameworks under the European Green Deal and related national programs.

The European Commission and IEA underscore that heat pumps, including heat pump water heaters, can cut gas demand for building heating by at least 21 billion cubic meters annually, reinforcing the strategic role of electric and hybrid solutions in water heating portfolios.

Manufacturers in Europe focus on condensing gas units, high performance storage systems, and integrated space and water heating solutions, often combined with solar thermal or photovoltaic systems. Harmonization of appliance labeling and eco design directives across the EU helps standardize performance metrics and creates a level playing field for cross border product offerings. As renovation of Europe’s aging building stock accelerates, particularly in multi family and social housing, replacement of outdated boilers and cylinders with efficient storage, tankless, and hybrid systems is expected to drive steady market growth across key economies.

Asia Pacific Water Heater Market Trends

Asia Pacific is the fastest growing regional market, driven by rapid urbanization, sustained economic growth, and rising living standards across China, India, and ASEAN countries. Expanding middle class populations are increasing adoption of modern bathroom and kitchen amenities, including electric storage and instant water heaters in urban apartments and single family homes. In China, urban housing construction and government emphasis on energy efficiency underpin robust demand for high efficiency electric and gas units, while domestic brands and multinationals compete aggressively on performance and price.

In India, rising electrification rates, government schemes for housing and sanitation, and strong presence of brands such as Bajaj Electricals India and Havells India Ltd. support sustained volume growth in small to mid capacity electric storage and instant heaters.

Competitive Landscape

The global Water Heater Market is moderately consolidated, with leading manufacturers such as A.O. Smith, Rheem Manufacturing Company, Bosch Thermotechnology Corp., Ariston Holding N.V., and Rinnai America Corporation holding significant combined share in key regions while competing with strong regional brands like Bajaj Electricals India, Haier Inc., and Havells India Ltd.

Market leaders differentiate through broad portfolios spanning electric, gas, solar, and emerging heat pump technologies, along with smart connectivity, high efficiency ratings, and strong after sales service networks. Emerging business models emphasize integrated solutions bundling water heaters with home energy systems, service contracts, and digital monitoring platforms while R&D priorities focus on hybridization, higher Energy Factor ratings, compact designs, and compatibility with evolving regulatory standards.

Key Market Developments

- In June 2025, LG Electronics acquired Norway-based OSO Group, a specialist in premium stainless-steel water heaters. The move enhances LG’s HVAC portfolio, especially in Europe. OSO’s technology will support LG’s integrated heat pump and water heating solutions. OSO will continue to operate independently under LG’s ownership.

- In May 2025, Ariston Group and Lennox formed a joint venture to introduce Lennox-branded residential water heaters in North America by 2026. Ariston holds a 50.1% stake, while Lennox owns 49.9%. Product will be sold through Lennox’s dealer network and distributors. Ariston will continue offering its own brands separately.

Companies Covered in Water Heater Market

- A.O. Smith

- Bosch Thermotechnology Corp.

- Ariston Holding N.V.

- Rheem Manufacturing Company.

- Rinnai America Corporation.

- Bradford White Corporation, USA.

- Noritz America Corp

- Whirlpool.

- Westinghouse Electric Corporation.

- Bajaj Electricals India.

- Others Key Players

Frequently Asked Questions

Key demand drivers include rapid urbanization and housing expansion, tightening efficiency and climate regulations, electrification of building heat, and growing adoption of high‑efficiency, heat pump, and smart connected water heaters.

The 30 – 100 Liters capacity segment leads by volume, while electric water heaters hold the largest product share, supported by widespread grid access, electrification policies, and regulatory pressure favoring efficient electric and heat pump technologies over conventional fossil‑fuel-based systems.

North America, led by the United States, currently dominates by value owing to its large installed base, frequent replacement cycles, stringent DOE efficiency standards, and rapid adoption of high‑efficiency, smart and heat pump water heater solutions.

Leading players include A.O. Smith, Rheem Manufacturing Company, Bosch Thermotechnology Corp., Ariston Holding N.V., Rinnai America Corporation, Bradford White Corporation, USA, Noritz America Corp, Whirlpool, Haier Inc., Bajaj Electricals India, and Havells India Ltd., supported by strong regional brands and global appliance majors.