- Home Care & Utilities

- Water Filter Market

Water Filter Market Size, Share, and Growth Forecast, 2025 - 2032

Water Filter Market By Technology (Reverse Osmosis (RO), Ultrafiltration (UF), Others), Product Type (Point-of-Use, Point-of-Entry), End-Use, Distribution Channel and Regional Analysis for 2025 - 2032

Water Filter Market Size and Trends Analysis

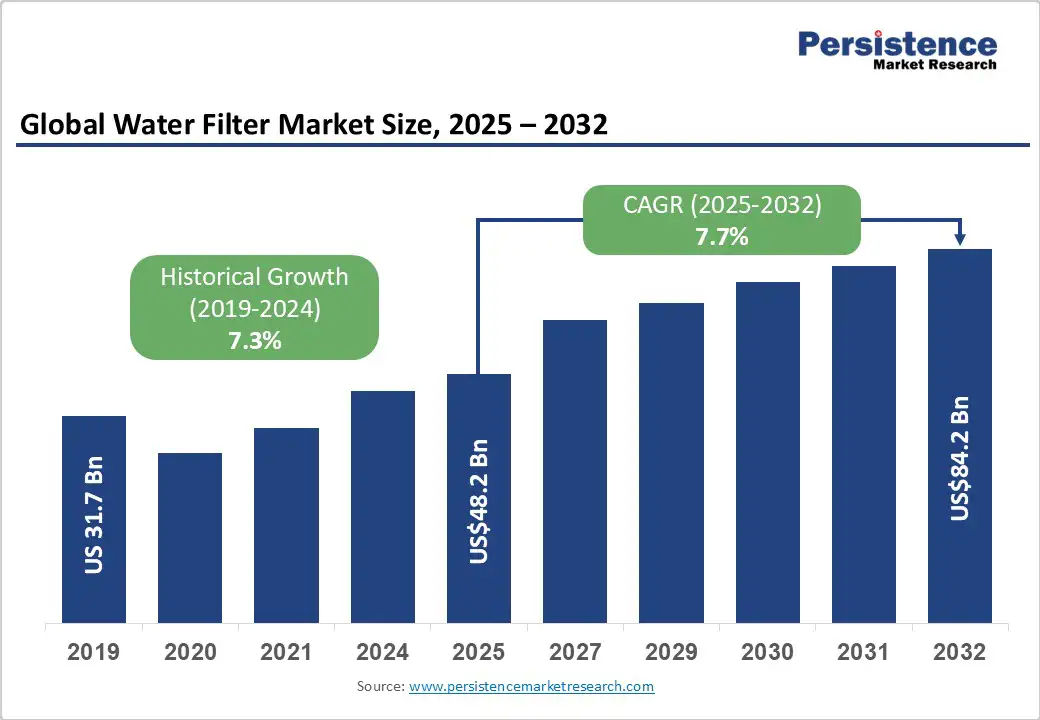

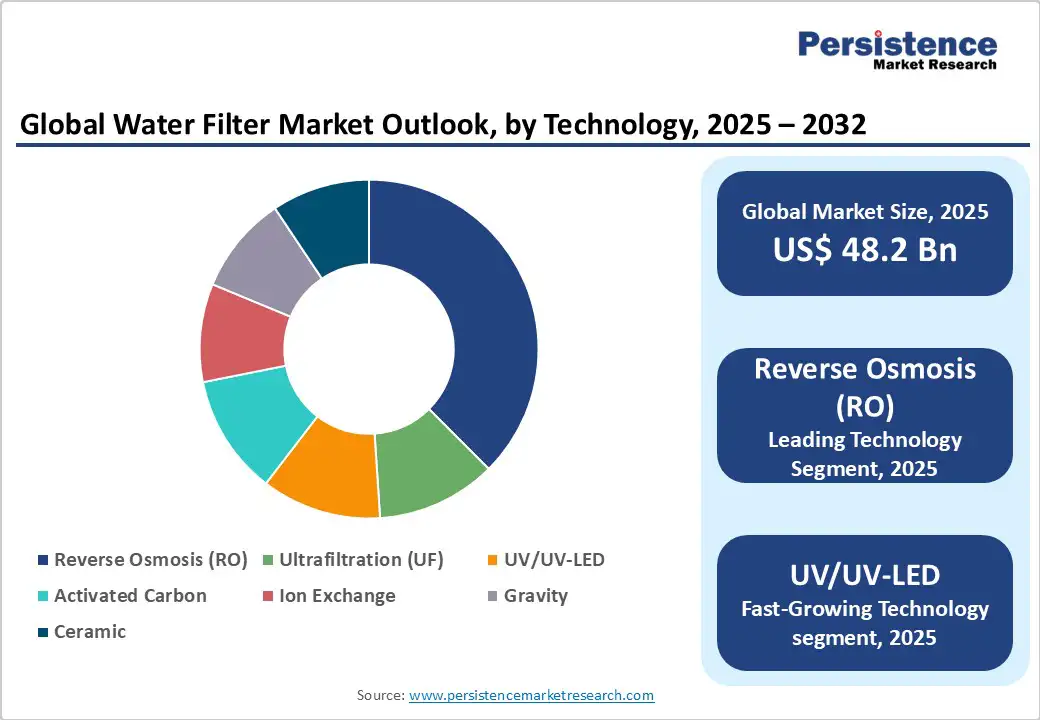

The global water filter market size is likely to be valued at US$48.2 Bn in 2025 and is expected to reach US$84.2 Bn by 2032, growing at a CAGR of 7.7% during the forecast period from 2025 to 2032.

Market expansion is primarily driven by rising demand for safe drinking water, urbanization, and technological innovation in purification systems. Increasing regulatory pressure for water quality compliance and heightened consumer awareness of waterborne diseases are pushing both residential and commercial adoption. The replacement and service revenue from filter cartridges and maintenance contracts is expected to contribute significantly to recurring income streams during the forecast period.

Key Industry Highlights

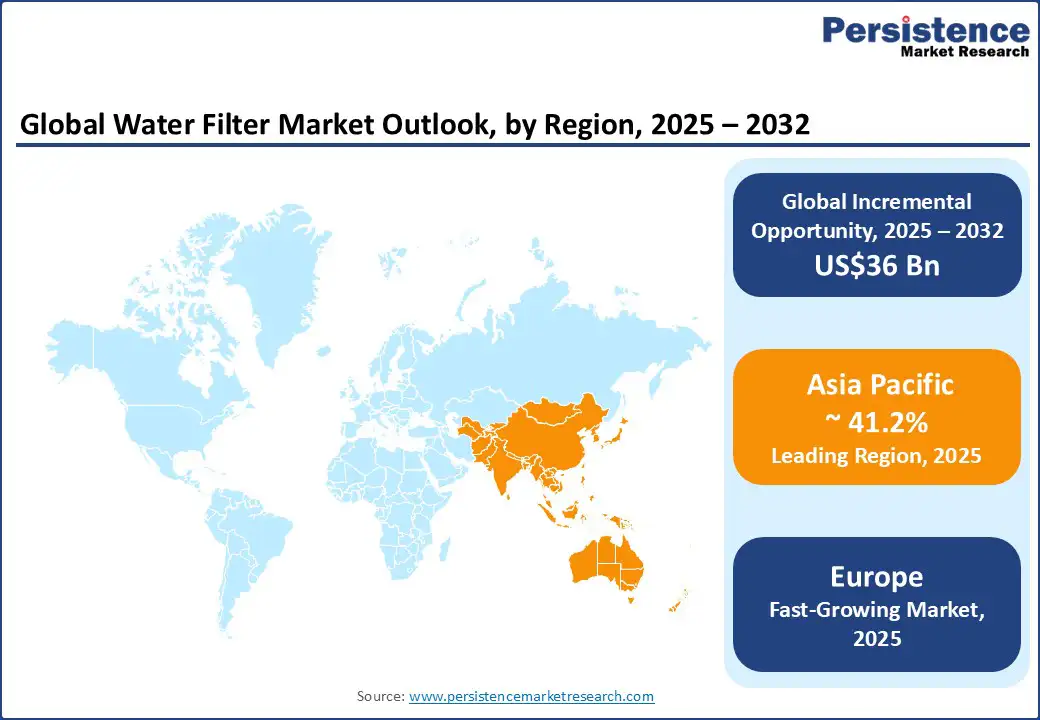

- Leading Region: Asia Pacific 41.2% of global market share in 2025, driven by high residential adoption and rapid urbanization.

- Fastest-Growing Region: Asia Pacific projected CAGR of 8.9% (2025–2032) due to rising disposable incomes, inconsistent municipal water quality, and government initiatives like India’s Jal Jeevan Mission.

- Investment Plans: Expansion of smart filtration systems, hybrid RO-UV solutions, and subscription-based service models across North America, Europe, and Asia Pacific; regional manufacturing and distribution hubs are prioritized to mitigate supply chain risks.

- Dominant Technology: Reverse Osmosis (RO) captures 36% of market value in 2025, supported by high efficacy in removing dissolved salts, heavy metals, and chemical contaminants.

- Leading Product Type: Point-of-Use (POU) Systems accounts for 44.8% of market revenue, driven by affordability, easy installation, and widespread residential adoption, particularly in Asia Pacific and Latin America.

| Key Insights | Details |

|---|---|

|

Water Filter Market Size (2025E) |

US$48.2 Bn |

|

Market Value Forecast (2032F) |

US$84.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Concern for Water Safety and Quality

Over two billion people worldwide still lack access to safely managed drinking water, according to international public health organizations. This deficit has made water filtration and purification solutions a fundamental necessity. The growing incidence of waterborne illnesses and the contamination of municipal water supplies with heavy metals, fluoride, and microplastics have heightened the need for household and point-of-use (POU) filtration systems. This growing health awareness has accelerated sales across emerging markets, where urbanization and middle-class expansion continue to expand the customer base.

Regulatory Standards and Compliance Enforcement

Governments across the globe are tightening water safety regulations, pushing utilities and businesses to upgrade existing filtration systems. In North America, stricter limits on lead and copper levels in public water systems have increased the installation of certified filtration devices. Similarly, the European Union’s Drinking Water Directive mandates enhanced monitoring of contaminants such as microplastics and endocrine-disrupting compounds. This regulatory momentum is encouraging both residential and institutional investments in certified filtration solutions, supporting steady demand for replacement cartridges and consumables.

Technological Advancements and Product Innovation

Continuous technological improvements, including low-waste reverse osmosis (RO), ultrafiltration (UF), and UV-LED disinfection systems, are transforming the market landscape. Integration of Internet of Things (IoT) sensors allows real-time monitoring of water quality and filter life, improving user experience and operational efficiency. Hybrid systems combining RO with UV sterilization and activated carbon filtration are gaining prominence for their ability to deliver comprehensive purification with lower energy and water consumption. These innovations are reducing maintenance costs, driving premium adoption, and broadening the market’s consumer base.

High Initial and Maintenance Costs

The adoption of advanced RO and whole-home filtration systems often involves substantial upfront investment and recurring costs for filter replacement. In lower-income and rural markets, cost sensitivity reduces penetration, particularly where municipal water is perceived as acceptable. The total cost of ownership remains a key challenge, with replacement filter costs accounting for nearly 20–30% of product lifecycle spending.

Raw Material and Supply Chain Volatility

Water filtration components such as membranes, activated carbon, and plastic housings rely on raw materials prone to price fluctuations. Supply chain disruptions and import dependencies, especially from Asian manufacturing hubs, can cause production delays and margin pressures. Companies dependent on single-source suppliers face higher operational risks, making diversification and local sourcing critical to maintaining competitiveness.

Expansion of Point-of-Use Systems in Emerging Markets

Rapid urbanization and inadequate municipal water treatment in Asia-Pacific and Africa are creating substantial opportunities for point-of-use systems. If 10–15% of urban households in these regions adopt mid-tier purifiers by 2032, incremental market revenue could exceed US$ 6–8 Bn. The expansion of retail and e-commerce distribution channels is enabling better accessibility for these systems at affordable price points.

Growth in Commercial and Institutional Applications

Schools, hospitals, and office buildings are increasing their reliance on advanced filtration systems to ensure compliance with safety standards. The institutional segment, especially in healthcare, offers higher-value, longer-term contracts. The rise of sustainability certifications in commercial buildings is also encouraging the integration of centralized filtration units to reduce bottled-water dependence.

Subscription and Service-Based Business Models

The shift from one-time product sales to service subscriptions is a key growth frontier. Manufacturers that convert even 20% of their installed customer base to maintenance and cartridge subscription programs can enhance annual recurring revenue by 30–40%. This model also increases brand loyalty, ensures consistent cash flow, and enhances aftermarket profitability.

Category-wise Analysis

Technology Insights

Reverse osmosis (RO) continues to dominate the technology segment, accounting for around 36% of market value in 2025, according to estimates from the World Health Organization (WHO) and industry bodies such as the Water Quality Association (WQA). The strong demand stems from RO’s capability to remove up to 99% of dissolved salts, heavy metals, fluoride, and nitrates, which are particularly prevalent in regions with poor groundwater quality such as India, China, and parts of the Middle East. RO systems are widely used in residential, commercial, and industrial sectors, including bottled water production, food processing, and pharmaceuticals. The introduction of smart RO systems with IoT-enabled monitoring and TDS (Total Dissolved Solids) sensors has further strengthened consumer trust in advanced purification.

Ultraviolet (UV), particularly UV-LED-based technologies, are registering the fastest growth. Their compact design, low energy consumption, and absence of chemical residues make them ideal for urban apartments, small offices, and portable devices. For instance, LG Electronics and Panasonic have introduced UV-LED purifiers capable of sterilizing water within seconds while consuming up to 30% less power than traditional mercury-based UV lamps. Markets in Japan, Singapore, and Western Europe are rapidly adopting these advanced systems due to growing concerns over microbial contamination and pharmaceutical residues in tap water. Government initiatives promoting eco-friendly, zero-waste technologies are further accelerating adoption. As LED prices decline and product lifespans increase, UV-LED systems are expected to become a mainstream technology within the next five years.

Product Type Insights

Point-of-Use (POU) systems comprising countertop, under-sink, faucet-mounted, and portable units, represent the largest product category, contributing nearly 44.8% of total market revenue in 2025. Their affordability, ease of installation, and minimal maintenance requirements make them the preferred choice for residential applications, particularly in densely populated regions across Asia-Pacific and Latin America. According to data from UNESCO’s Water Development Report, over 1.4 billion people in these regions rely on POU systems as their primary source of clean water. Brands such as Brita GmbH (Germany), Pureit (Unilever, India), and Aquasana (U.S.) continue to innovate with compact filtration cartridges, app-based filter replacement alerts, and eco-friendly refill options. The rising trend of rental-based water filter services in urban India and Brazil, offered by companies like Eureka Forbes, is also making high-end systems more accessible to middle-income households.

Point-of-Entry (POE) or whole-home systems are experiencing rapid growth, particularly in North America, Western Europe, and urban China. These systems filter all water entering a household, covering both potable and non-potable applications such as bathing, laundry, and kitchen use. As awareness grows regarding the impact of chlorine, hardness, and microbial content on skin, appliances, and plumbing, consumers are increasingly opting for whole-house protection. Leading brands like Culligan International, 3M Purification Inc., and Pentair PLC are investing heavily in smart POE systems integrated with AI-based monitoring and real-time water quality analytics. For example, Pentair’s Connected Water platform allows homeowners to track filtration performance and water consumption via smartphone applications.

Regional Insights

Asia Pacific Water Filter Market Trends-Urban Growth and Smart Tech Propel Water Filter Demand

Asia Pacific represents the largest and fastest-growing regional market, accounting for nearly 41.2% of global water filter revenue in 2025, driven by rapid urbanization, industrial expansion, and government-led initiatives to improve water access and quality. According to the Asian Development Bank (ADB), more than 1.2 billion people in Asia still lack reliable access to potable water, which continues to propel household and community-level filtration adoption.

China remains the manufacturing hub, hosting major players such as Midea Group, Haier Smart Home, and Qinyuan Group, all of which are investing in smart RO and IoT-enabled filtration systems. In India, programs such as the Jal Jeevan Mission and Smart Cities Mission have accelerated residential adoption, while companies like Eureka Forbes, Kent RO Systems, and Livpure dominate domestic sales. Japan and South Korea lead in technological sophistication, with UV-LED and nano-filtration products by Panasonic and Coway setting benchmarks for low-energy, high-performance purification. ASEAN markets, particularly Vietnam, Thailand, and Indonesia, are attracting foreign investment from European and U.S. firms expanding their regional presence. Increasing consumer income, a booming e-commerce sector, and public awareness campaigns are reinforcing Asia Pacific’s leadership position through 2032.

North America Water Filter Market Trends - Aging Infrastructure and Smart Systems Drive Adoption

North America represents one of the most mature and technologically advanced regions in the global water filter market, with the United States accounting for most of regional demand. Market growth is strongly driven by aging municipal water infrastructure, increased incidence of lead contamination, and regulatory enforcement under the U.S. Safe Drinking Water Act (SDWA) and the EPA’s Water Quality Standards Program. Rising consumer awareness following contamination events in Flint, Michigan, and Newark, New Jersey, has led to accelerated adoption of certified home filtration systems from companies like 3M, Culligan, and A.O. Smith. Technological innovation is also advancing rapidly, several startups, including Hydroviv and ZeroWater, are integrating AI-based quality monitoring sensors and low-waste RO membranes. The U.S. and Canada are leading in the rollout of smart filtration ecosystems, combining IoT, predictive maintenance, and digital customer interfaces. Government incentives promoting energy-efficient and lead-free systems under the EPA WaterSense program are further encouraging investment, while the commercial and industrial segments, particularly foodservice and healthcare are witnessing strong retrofit activity.

Europe Water Filter Market Trends - Regulatory Pressure and Eco Innovation Shape Market Growth

The Europe water filter market is led by Germany, the U.K., France, and Spain leading regional demand. Growth in Europe is characterized by regulatory harmonization under the EU Drinking Water Directive (2020/2184), which mandates stricter limits on emerging contaminants such as PFAS (per- and polyfluoroalkyl substances) and microplastics. Germany remains the region’s largest market, supported by advanced domestic manufacturing from players like Brita GmbH, Bosch Thermotechnology, and BWT AG. The U.K. and France are witnessing surging adoption of under-sink and whole-home filtration systems, particularly in areas with hard water conditions. Moreover, the European Commission’s Green Deal initiatives have accelerated the shift toward eco-designed, recyclable, and low-carbon water filter materials, prompting innovation in activated carbon and membrane technology. Investment is expanding in Eastern Europe, especially in Poland and the Czech Republic, where rising urbanization is driving adoption of compact filtration devices. Strategic partnerships, such as Veolia’s collaboration with BWT on industrial filtration systems, underline the region’s growing emphasis on sustainability and resource efficiency as competitive differentiators.

Competitive Landscape

The global water filter market displays a balanced structure, with major multinational corporations holding strong global positions and numerous regional brands leading in local markets. The sector is moderately fragmented in consumer categories but consolidated in industrial and institutional applications. Global players such as A. O. Smith, Pentair, Culligan, 3M, and Brita command notable shares through technology and distribution scale. Regional companies like KENT, Eureka Forbes, and BWT maintain dominance in domestic markets with localized service and brand trust.

Leading players emphasize technological innovation, regional market expansion, cost optimization, and subscription-based service offerings. Certification compliance and brand reputation remain key differentiators. Companies are increasingly adopting IoT-enabled monitoring and predictive maintenance systems to improve customer retention and profitability.

Key Industry Developments

- In April 2025, Samsung unveiled its Bespoke AI Water Purifier in South Korea, a high-tech countertop appliance priced at $1,000. This purifier features AI integration, Bixby voice control, and SmartThings app compatibility, utilizing a four-stage filtration system to remove up to 82 harmful substances.

- In June 2025, Kent RO Systems unveiled an advanced RO-UV hybrid purifier in India, featuring smart TDS control and app-based filter replacement notifications to cater to the growing urban middle-class segment.

Companies Covered in Water Filter Market

- O. Smith Corporation

- Pentair PLC

- Culligan International

- 3M Company

- Brita GmbH

- KENT RO Systems Ltd.

- Eureka Forbes Ltd.

- BWT AG

- Livpure Pvt. Ltd.

- Panasonic Corporation

- LG Electronics Inc.

- Midea Group

- Whirlpool Corporation

- Watts Water Technologies

- Aquaphor Corporation

- Coway Co., Ltd.

- Veolia Water Technologies

- Evoqua Water Technologies

- Pall Corporation

- Pureit (Unilever)

Frequently Asked Questions

The global market size in 2025 is US$ 48.2 Bn.

By 2032, the market is projected to reach US$ 84.2 Bn, reflecting robust growth across residential, commercial, and industrial segments.

Key Trends are the rising adoption of hybrid RO-UV and UV-LED systems and increasing demand for point-of-use (POU) systems in emerging markets.

Product Type Segment: Point-of-Use (POU) systems lead with 44.8% market revenue.

The market is expected to grow at a CAGR of 7.7% from 2025 to 2032.

Major players include A. O. Smith Corporation, Pentair PLC, Brita GmbH, Culligan International, and Kent RO Systems Ltd.