- IT and Telecommunication

- Virtual Data Optimizer (VDO) Market

Virtual Data Optimizer (VDO) Market Size, Share, and Growth Forecast, 2026 - 2033

Virtual Data Optimizer (VDO) Market by Product Type (Software Platforms, Services), Deployment Mode (On-Premises, Cloud-Based), Optimization Type (Data Compression, Data Deduplication, Data Caching, Data Tiering, Bandwidth Optimization, Misc.), End Use Industry (BFSI, IT & Telecom, Healthcare, Retail & E-Commerce, Manufacturing, Government) and Regional Analysis for 2026 - 2033

Virtual Data Optimizer (VDO) Market Size and Trends Analysis

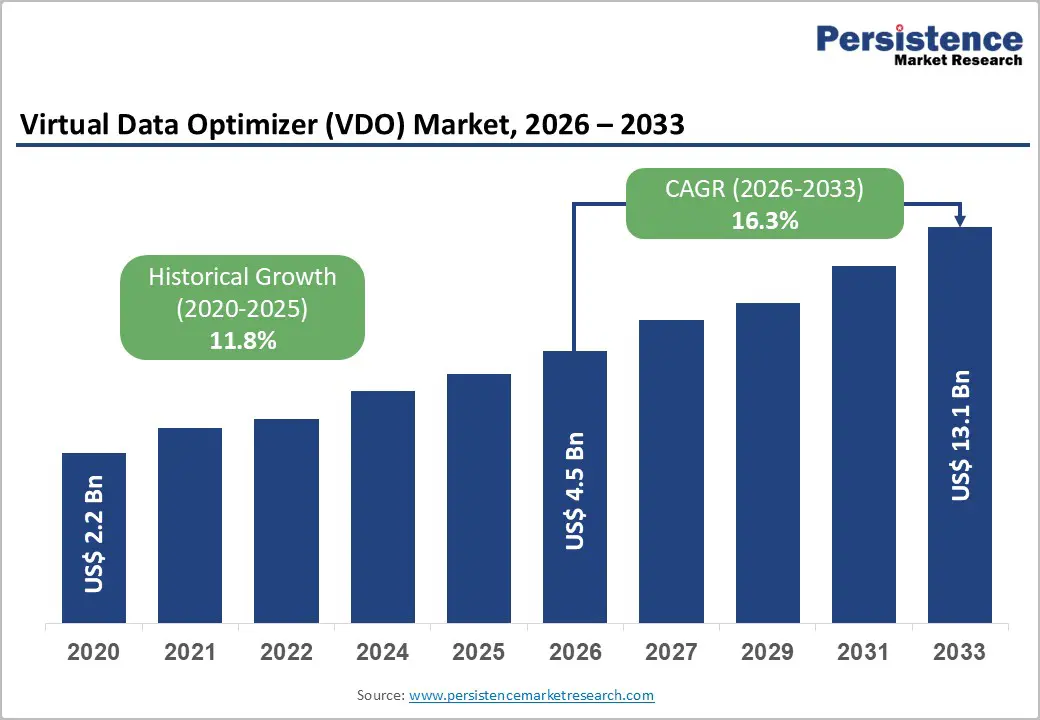

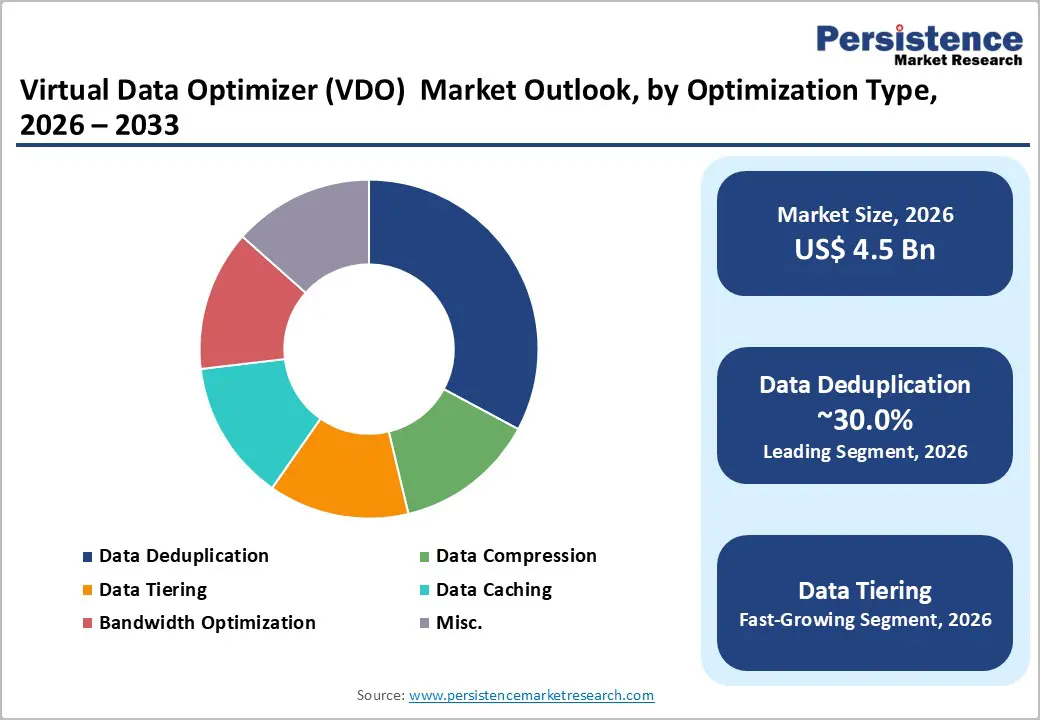

The Global Virtual Data Optimizer (VDO) Market size was valued at US$ 4.5 billion in 2026 and is projected to reach US$ 13.1 billion by 2033, growing at a CAGR of 16.3% between 2026 and 2033. This substantial market expansion reflects accelerating digital transformation initiatives, exponential data volume growth, and enterprise demand for cost-efficient storage solutions that reduce infrastructure expenditures while enabling seamless cloud and hybrid IT deployment.

The Market is experiencing momentum from regulatory compliance requirements in the banking sector, modernization pressures in legacy enterprise systems, and the transition from capital-intensive infrastructure models to operational expenditure-based cloud consumption patterns.

Key Industry Highlights:

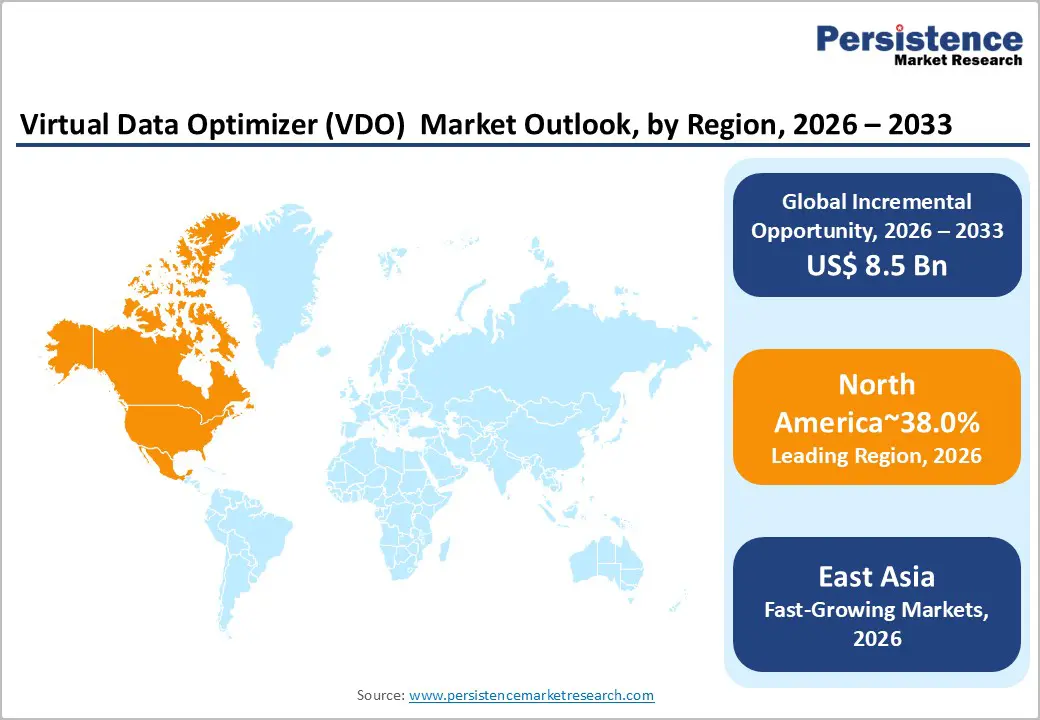

- Regional Leadership: North America leads the global Virtual Data Optimizer (VDO) market with ~38% share, driven by mature data center infrastructure, widespread hybrid and multi-cloud adoption, and strong demand from BFSI and hyperscale cloud operators.

- Fastest-Growing Region: East Asia accounts for 20% share and represents the fastest-growing region, supported by rapid digital transformation, IoT-driven data growth, and government-backed technology initiatives in China, Japan, and South Korea.

- Significant European Market: Europe holds 24% share, underpinned by stringent data protection regulations (GDPR), sustainability-focused data center investments, and rising adoption of open-source, vendor-neutral storage optimization solutions.

- Leading Component Segment: Software-based VDO solutions dominate with 62% market share, reflecting enterprise preference for vendor-neutral, scalable deduplication and compression platforms integrated at the OS and storage virtualization layer.

- Leading Optimization Type: Data deduplication remains the largest optimization segment with 30% share, driven by high data reduction efficiency across virtualized environments, backups, and containerized workloads.

| Key Insights | Details |

|---|---|

|

Virtual Data Optimizer (VDO) Market Size (2026E) |

US$ 4.5 Bn |

|

Market Value Forecast (2033F) |

US$ 13.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.8% |

Market Dynamics

Growth Drivers

Exponential Data Volume Expansion and Digital Infrastructure Modernization

Enterprise data generation has accelerated dramatically, driven by Internet of Things (IoT) proliferation, unstructured data accumulation from digital services, and advanced analytics deployment.

Organizations across manufacturing, retail, telecommunications, and financial services sectors confront storage capacity constraints that threaten system performance and escalate operational costs. The Virtual Data Optimizer (VDO) Market addresses this structural challenge through block-level data deduplication, compression, and thin provisioning technologies that dramatically reduce physical storage requirements while maintaining full data accessibility.

Market research indicates that organizations implementing advanced data reduction technologies achieve storage utilization efficiency improvements from conventional 50-60% to optimized 80-90% ranges, directly translating to deferred capital expenditures for storage array expansion and reduced data center footprints. Linux kernel integration of VDO functionality, particularly the March 2024 integration into the mainline kernel with support for deduplication rates of 254:1 and compression ratios of 14:1, demonstrates ecosystem maturation and broad adoption readiness across enterprise computing environments.

BFSI Sector Modernization and Data Governance Compliance

The Banking, Financial Services, and Insurance (BFSI) sector represents the fastest-growing end-user segment for Virtual Data Optimizer (VDO) Market solutions, driven by regulatory compliance requirements, legacy system modernization pressures, and explosive data volume growth from customer analytics and risk assessment systems. India's BFSI sector reached market capitalization of US$1 trillion in 2025, with contribution to national GDP increasing from 6% to 27%, generating corresponding demand for advanced data infrastructure solutions.

European BFSI generated €0.9 trillion in value added across approximately 867,000 enterprises employing 5 million professionals, with insurance and pension funding subsector generating €1.2 trillion in turnover.

China's banking and insurance sectors demonstrated robust growth with total banking assets reaching RMB 467.3 trillion and insurance assets growing 9.2% to RMB 39.2 trillion as of Q2 2025, reflecting accelerating data infrastructure requirements. BFSI organizations implementing VDO technologies achieve substantial reductions in storage-related capital expenditures while meeting stringent data protection, privacy, and business continuity requirements mandated by regulators including the Reserve Bank of India, European Central Bank, and China Banking and Insurance Regulatory Commission.

Market Restraining Factors

Technical Integration Complexity and Legacy System Compatibility Challenges

Organizations deploying Virtual Data Optimizer (VDO) solutions confront substantial technical implementation barriers when integrating advanced data reduction technologies with heterogeneous storage environments comprising equipment from multiple vendors spanning different generations and architectural paradigms. Legacy storage arrays lacking modernized firmware, network-attached storage systems with proprietary file systems, and mission-critical applications with strict latency requirements create implementation constraints that extend deployment timelines and increase integration costs.

Inline data deduplication and compression processing introduce computational overhead that consumes CPU resources and generates latency penalties for I/O-intensive workloads, necessitating careful performance characterization and tuning to avoid degrading application responsiveness. Organizations require specialized technical expertise in storage architecture, performance analysis, and data integrity validation that exceeds typical IT staff skill levels, creating sustained demand for consulting services and professional implementation support that adds material expense to deployment projects.

Key Market Opportunities

Edge Computing Infrastructure and Distributed Storage Optimization

Edge computing architectures, which place computing and storage resources closer to data generation points to reduce latency and bandwidth consumption, are emerging as a significant growth opportunity for Virtual Data Optimizer (VDO) Market solutions. The proliferation of remote branch offices, retail locations, manufacturing facilities, and autonomous systems generates distributed data that organizations seek to optimize locally before transmission to centralized data centers or cloud platforms. Organizations deploying edge storage infrastructure leverage VDO technologies to maximize capacity utilization across geographically dispersed storage devices, enabling efficient data retention and processing at distributed locations while minimizing bandwidth requirements for data replication and backup operations.

Organizations implementing edge computing and distributed storage architectures report capability enhancements including reduced latency for local applications (sub-100 millisecond response times), optimized bandwidth utilization through local data caching and deduplication, and improved business continuity through local data redundancy.

The data center infrastructure market includes substantial investment in edge data center deployment across emerging economies, manufacturing regions, and retail-dense areas, creating corresponding demand for cost-efficient storage solutions. Virtual Data Optimizer (VDO) Market technologies enable organizations to implement edge storage without proportional increases in facility square footage or cooling capacity requirements, supporting sustainable infrastructure expansion.

Artificial Intelligence and Machine Learning Integration with Storage Infrastructure

Emerging Virtual Data Optimizer (VDO) Market opportunities center on integration of artificial intelligence and machine learning algorithms that optimize storage performance, predict maintenance requirements, and adapt deduplication and compression policies dynamically based on workload characteristics. Next-generation data storage platforms are increasingly incorporating AI-native capabilities including predictive analytics for storage failure identification, machine learning-driven workload characterization for optimal data reduction configuration, and automated policy management that adjusts compression aggressiveness and deduplication intensity based on performance observations.

Organizations implementing AI-enhanced VDO solutions achieve superior data reduction ratios compared to static policy configurations, with reported improvements of 15-25% in compression efficiency through dynamic algorithm selection based on detected data characteristics.

The software-defined storage market reflects accelerating integration of AI and automation into storage infrastructure management. Virtual Data Optimizer (VDO) Market participants integrating machine learning capabilities for anomaly detection, performance prediction, and configuration optimization position themselves advantageously to capture emerging demand from data-intensive organizations requiring increasingly intelligent infrastructure. AI-driven storage optimization contributes to broader organizational digital transformation initiatives by reducing manual infrastructure management overhead, improving resource utilization, and enabling IT teams to redirect effort from reactive system management toward strategic infrastructure planning.

Category-wise Analysis

Component Type Insights

Software platforms commanded 62% of the Virtual Data Optimizer (VDO) Market in 2026, reflecting the fundamental role of deduplication and compression software in enabling block-layer data reduction across heterogeneous storage environments.[User provided data] Software-based VDO implementations offer substantial advantages over hardware-accelerated approaches, including vendor-neutral deployment across commodity storage hardware, simplified upgrade and patch management through software updates rather than firmware revisions, and reduced capital expenditure requirements by leveraging existing infrastructure.

Red Hat's integration of VDO into the Linux 6.9 kernel, completed in March 2024, exemplifies open-source software platform maturation where deduplication logic, compression algorithms (LZ4), and thin provisioning functionality operate at the operating system kernel level, enabling transparent data reduction for all block storage consumers without application-level modifications.Organizations deploying VDO software platforms achieve profound independence from specific storage hardware vendors, reducing proprietary lock-in and enabling migration flexibility as technology landscape evolves.

Services comprising consulting, implementation, training, and ongoing support represent the fastest-growing Virtual Data Optimizer (VDO) Market component, driven by technical complexity inherent in deploying advanced data reduction technologies and organizational demand for expert guidance in configuration optimization and workload tuning

Optimization Type Insights

Data deduplication maintained approximately 30% of the Virtual Data Optimizer (VDO) Market share in 2026, establishing it as the predominant optimization technique across enterprise storage deployments.

Deduplication identifies and eliminates redundant data copies at block, file, or byte level, achieving particularly high reduction ratios in environments storing multiple instances of similar data including virtual machine images, containerized application deployments, and backup datasets where identical data patterns naturally proliferate. VDO-enabled systems report deduplication ratios ranging from 4:1 to 10:1 in primary storage deployments, with backup and archival scenarios achieving ratios exceeding 20:1 where identical data naturally accumulates across multiple backup cycles. Organizations deploying deduplication achieve direct cost savings through reduced storage hardware requirements, improved data transfer performance through bandwidth optimization, and extended data retention capabilities within existing storage infrastructure without proportional capacity expansion.

Data tiering represents the fastest-growing optimization methodology within the Virtual Data Optimizer (VDO) Market, reflecting organizational recognition that not all data requires equivalent storage performance and cost characteristics. Tiering technology automatically migrates data between storage tiers based on access patterns, age, and priority, positioning frequently accessed data on high-performance flash storage, moderate-activity data on mid-tier SSD or hybrid arrays, and infrequently accessed archive data on cost-optimized nearline storage or cloud object repositories.

Regional Insights and Trends

North America Market Trend

North America retained approximately 38% of the Global Virtual Data Optimizer (VDO) Market share, maintaining leadership through technological innovation concentration, mature infrastructure modernization initiatives, and supportive regulatory environments. The U.S. data storage market alone is growing, with North America's data storage market forecast at 8.5% CAGR through 2032, reflecting sustained enterprise investment in storage infrastructure modernization. The region benefits from presence of major technology companies including IBM, Dell Technologies, Microsoft, and cloud providers including Amazon Web Services, Microsoft Azure, and Google Cloud Platform that drive innovation in storage virtualization and data optimization technologies.

North American enterprises demonstrate particularly advanced adoption of hybrid cloud and multi-cloud strategies, with 85% of financial institutions implementing hybrid or multi-cloud architectures to balance regulatory compliance, cost optimization, and operational flexibility. This architectural approach creates demand for storage virtualization and optimization solutions that seamlessly manage data across on-premises data centers and multiple cloud providers. U.S. BFSI organizations investing in cloud modernization frameworks seek storage solutions that reduce bandwidth consumption for data replication and backup operations between cloud environments while maintaining data consistency and regulatory compliance. The region's data center infrastructure concentration, with substantial numbers of hyperscale data centers supporting cloud and artificial intelligence workloads, drives demand for efficient storage solutions that reduce facility space requirements and energy consumption.

East Asia Market Trend

East Asia represented approximately 20% of the Global Virtual Data Optimizer (VDO) Market share while demonstrating the fastest regional growth trajectory, driven by accelerating digital transformation across manufacturing, financial services, and telecommunications sectors. China's comprehensive Healthy China 2030 initiative and digital economy policies prioritize advanced technology infrastructure development including storage virtualization and data optimization capabilities.

Government-backed research institutions and commercial technology companies across East Asia are developing VDO and storage optimization solutions competing effectively with Western incumbents through cost leadership and innovation in emerging use cases including Internet of Things data management, smart city infrastructure, and artificial intelligence workload optimization.

Japan and South Korea demonstrate mature data center infrastructure supporting advanced analytics and semiconductor manufacturing, creating demand for sophisticated storage management solutions. Southeast Asian markets including Vietnam, Thailand, and Indonesia experience accelerating digital transformation driven by rising incomes, mobile internet penetration, and fintech ecosystem development that generates corresponding storage infrastructure requirements.

Europe Market Trend

Europe accounted for approximately 24% of the Global Virtual Data Optimizer (VDO) Market share, characterized by stringent regulatory frameworks governing data protection and privacy, sustainability emphasis, and accelerating digital transformation investments. The European Union committed €17 billion in funding for healthcare digitalization through Recovery and Resilience Facility and Cohesion Policy programs through 2027, with comparable investments in broader digital infrastructure modernization initiatives. Germany, as the EU's largest economy, driven by automotive manufacturing sector requirements, financial services digital transformation, and Industry 4.0 manufacturing modernization initiatives.

European regulatory requirements including the General Data Protection Regulation and EU Digital Act mandate comprehensive data protection and privacy infrastructure that drive enterprise investment in storage solutions incorporating encryption, access controls, and audit logging.

The EU's emphasis on digital sovereignty and open-source technology adoption creates favorable conditions for VDO technologies, particularly Red Hat's Linux kernel integration of VDO functionality, which enables European organizations to implement data reduction technologies without dependency on proprietary vendors. Cloud adoption across Europe, particularly adoption of European cloud providers and sovereign cloud offerings to meet regulatory requirements, generates demand for storage virtualization and optimization solutions that reduce data transfer costs and improve cross-border data replication efficiency.

Competitive Landscape

The global Virtual Data Optimizer (VDO) market is moderately consolidated, with a small group of large enterprise technology providers holding a dominant position alongside a limited number of specialized vendors. IBM Corporation, Microsoft Corporation, Oracle Corporation, Red Hat, Inc., Hewlett Packard Enterprise (HPE), and Fujitsu Limited are the leading players, leveraging integrated storage, virtualization, and cloud data management portfolios.

These companies benefit from strong enterprise relationships, global distribution networks, and continuous R&D investment, creating high entry barriers for new entrants. Competition is driven by platform integration, performance optimization, and compatibility across hybrid and multi-cloud environments. Strategic partnerships and acquisitions are commonly used to enhance data optimization capabilities within broader infrastructure stacks.

Key Industry Developments

- May 15, 2024 – Red Hat / Linux Community: The Linux 6.9 kernel integrates the Virtual Data Optimizer (VDO), enhancing FUSE file system performance and increasing disk space savings. VDO, acting as a device mapper, provides duplication, compression with LZ4, and zero-block elimination, reducing storage requirements and enabling more efficient data management in enterprise Linux environments.

- March 5, 2024 – Red Hat / Linux Community: The Virtual Data Optimizer (DM-VDO), originally developed by Permabit Technology Corp., is being integrated into the Linux DeviceMapper "for-next" branch, bringing inline deduplication, compression, zero-block elimination, and thin provisioning to the mainline kernel. The VDO target can handle up to 256TB of physical storage while presenting a logical size of up to 4PB, enabling deduplication rates of up to 254:1 and compression rates of 14:1. This integration marks a significant milestone for open-source storage optimization tools.

Companies Covered in Virtual Data Optimizer (VDO) Market

- Thomas Krenn AG

- Phoronix

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- NetApp, Inc.

- Commvault Systems, Inc.

- Veritas Technologies

- Cohesity, Inc.

- Rubrik, Inc.

Frequently Asked Questions

The global Virtual Data Optimizer (VDO) Market is projected to be valued at US$ 4.5 Bn in 2026.

IT & Telecom Segment is expected to account for approximately 34% of the global Virtual Data Optimizer (VDO) Market by End Use Industry in 2026.

The market is expected to witness a CAGR of 9.1% from 2026 to 2033.

Virtual Data Optimizer (VDO) Market growth is driven by exponential enterprise data volume expansion, digital infrastructure modernization, and rising BFSI demand for cost-efficient, compliant storage optimization through advanced duplication and compression technologies.

Key opportunities in the Virtual Data Optimizer (VDO) Market arise from expanding edge computing and distributed storage deployments requiring efficient local optimization, and from AI/ML-integrated storage platforms that enable intelligent, adaptive data reduction, performance optimization, and automated infrastructure management.

The key players in the Virtual Data Optimizer (VDO) Market include IBM Corporation, Microsoft Corporation, Oracle Corporation, Red Hat, Inc., Hewlett Packard Enterprise (HPE), and Fujitsu Limited.