- Plastics, Polymers & Resins

- Chlorinated Polyvinyl Chloride Market

Chlorinated Polyvinyl Chloride Market Size, Share, and Growth Forecast 2025 - 2032

Chlorinated Polyvinyl Chloride Market By Grade (Injection, Extrusion), Production Process (Aqueous Suspension, Others), Application (Plumbing systems, Others), End-use Industry, and Regional Analysis for 2025-2032

Chlorinated Polyvinyl Chloride Market Size and Trends Analysis

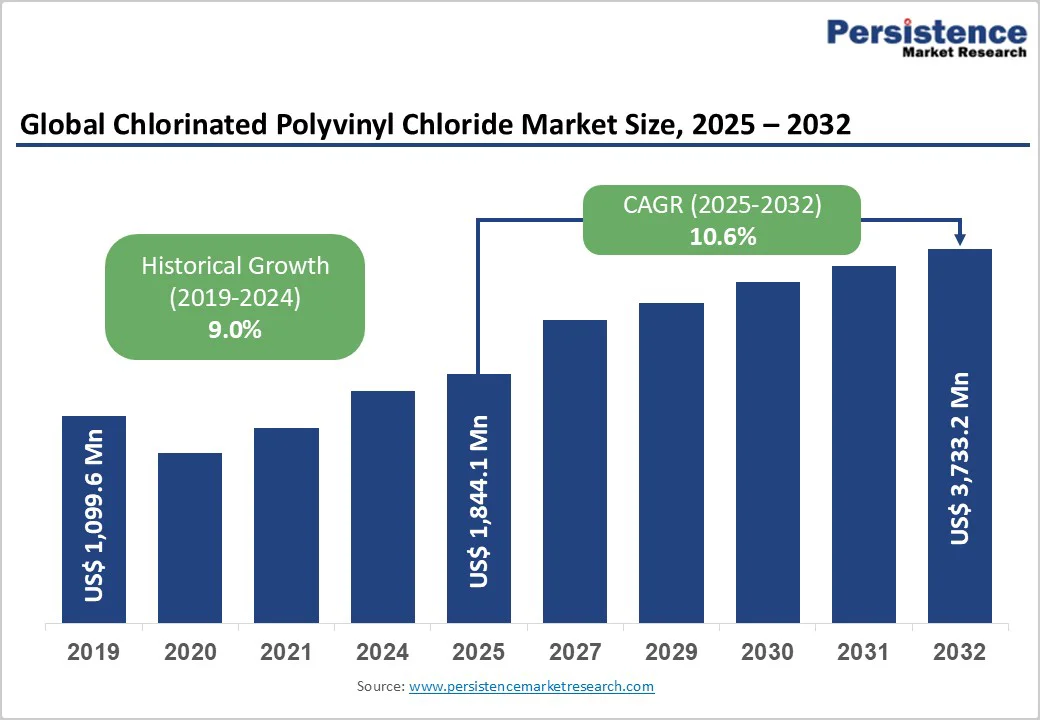

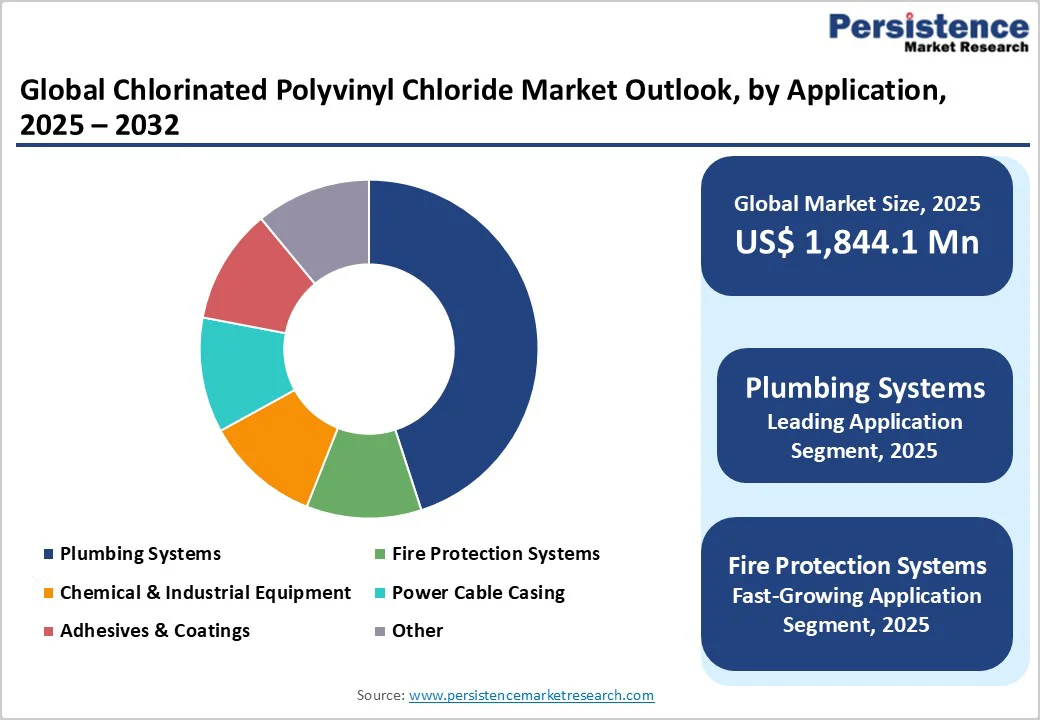

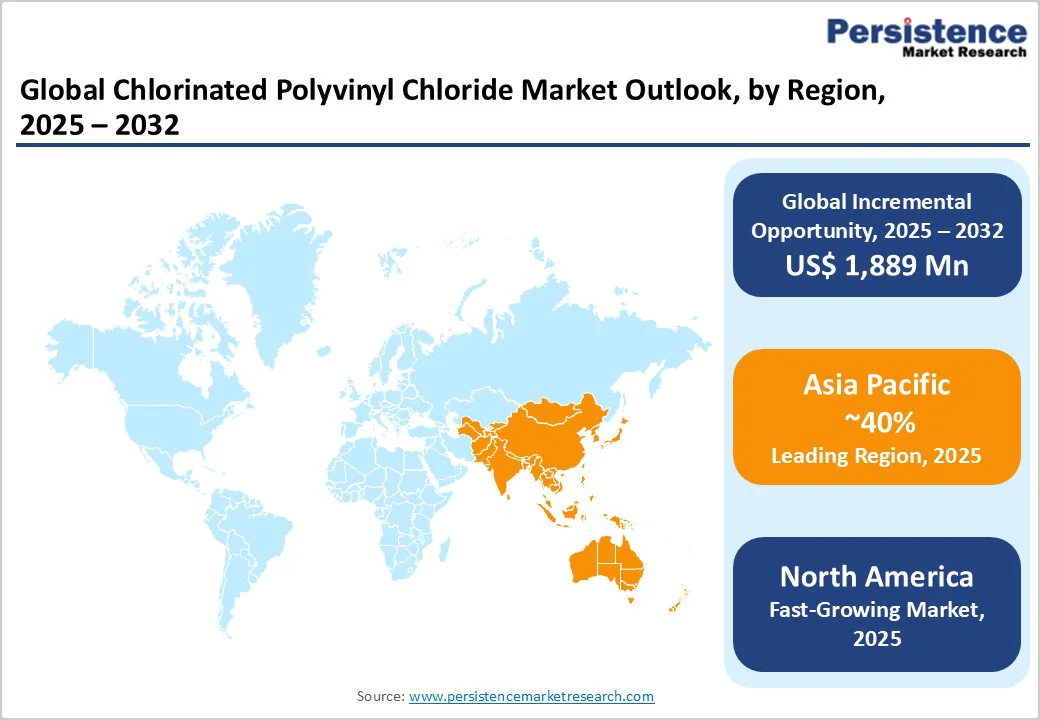

The global chlorinated polyvinyl chloride market size is likely to be valued at US$1,844.1 Million in 2025 and is projected to reach US$3,733.2 Million by 2032, growing at a CAGR of 10.6% during the forecast period from 2025 to 2032, driven by surging demand in construction and infrastructure projects worldwide, where CPVC's superior heat and corrosion resistance support durable plumbing and piping systems essential for urbanization. The superior thermal stability and corrosion resistance properties of CPVC make it an ideal choice for hot water distribution systems and fire sprinkler installations, particularly in emerging economies witnessing rapid urbanization and industrial growth.

Key Market Highlights

- Regional Leader: Asia Pacific leads the chlorinated polyvinyl chloride market due to rapid urbanization and manufacturing hubs in China and India, driving over 40% of the global demand through infrastructure investments.

- Fastest-Growing Region: North America emerges as the fastest-growing region, propelled by stringent fire safety regulations and retrofitting projects.

- Leading Segment: Extrusion Grade dominates across categories, capturing 65% share for its efficiency in pipe production, essential for plumbing and industrial uses worldwide.

- Fastest-Growing Segment: Industrial end-use grows the fastest, fueled by chemical processing demands and corrosion resistance needs.

- Key Opportunities: Wastewater treatment offers a key opportunity, leveraging CPVC's chemical durability to meet the 24% projected global wastewater increase by 2030 via sustainable piping solutions.

| Key Insights | Details |

|---|---|

|

Chlorinated Polyvinyl Chloride Market Size (2025E) |

US$1,844.1 Mn |

|

Market Value Forecast (2032F) |

US$3,733.2 Mn |

| Projected Growth CAGR (2025-2032) | 10.6% |

| Historical Market Growth (2019-2024) | 9.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand in Construction and Infrastructure

The escalating global construction sector, fueled by urbanization and infrastructure development, significantly propels the chlorinated polyvinyl chloride market. With over 2.5 billion people expected to live in urban areas by 2050, according to United Nations projections, the need for reliable piping systems has intensified. This need drives the demand for CPVC material due to its ability to handle hot and cold water up to 93°C without degradation

CPVC pipes are favored for their corrosion resistance, ability to withstand elevated temperatures up to 200°F (90°C), and economic viability compared to copper and steel alternatives. The plumbing components market is experiencing parallel growth as construction activities surge in smart city developments, residential housing projects, and commercial infrastructure across China, India, Japan, and Southeast Asian nations.

Stringent Fire Safety Regulations

Regulatory mandates for enhanced fire protection in buildings are a key catalyst for CPVC adoption, particularly in sprinkler systems. The National Fire Protection Association (NFPA) standards require materials with high flame retardancy, where CPVC demonstrates a limiting oxygen index of 60%, far surpassing traditional PVC. This compliance has led to a 25% increase in CPVC installations in new constructions across North America since 2020, as per the U.S. Fire Administration data, mitigating fire risks effectively. As global codes align with International Building Code (IBC) updates emphasizing non-combustible piping, CPVC's integration in high-rise and commercial structures fosters market reliability and growth.

Barrier Analysis - High Production and Raw Material Costs

Elevated costs associated with CPVC production pose a significant barrier. Processing CPVC requires specialized extrusion equipment with precise temperature control, typically within 190-210°C, necessitating capital investments approximately 15-20% higher than standard PVC extrusion lines. These technical requirements create barriers for smaller manufacturers lacking technical expertise and infrastructure, limiting market penetration.

Fluctuations in raw material prices, such as chlorine, impacted by supply chain disruptions, have raised costs by 15% in 2024, according to European Chemical Industry Council reports, deterring adoption in cost-sensitive developing markets. This pricing premium limits penetration in low-budget infrastructure projects, potentially slowing the overall market expansion.

Environmental and Health Concerns

Concerns over PVC derivatives' environmental impact, including potential dioxin emissions during production, hinder CPVC market progress. The Environmental Protection Agency (EPA) highlights that improper disposal contributes to microplastic pollution in waterways, prompting stricter regulations in Europe under the REACH framework, which has increased compliance costs by 10-15% for manufacturers. Specifically, the EPA data reveal that PVC production facilities released 238 tons of the total air toxics annually, including chlorinated dioxins, necessitating US$18 Million in capital investments for emission controls under the 2012 National Emission Standards.

Public awareness and bans in some regions on PVC-based materials further restrict usage, challenging sustainable positioning despite recyclability efforts. The REACH Annex XVII amendment restricting lead in PVC to 0.1% by weight, effective in November 2024, exemplifies heightened regulatory scrutiny.

Opportunity Analysis - Expansion in Wastewater Treatment Applications

The burgeoning wastewater treatment sector presents a prime opportunity for CPVC, given its resistance to corrosive chemicals such as acids and alkalis used in processes. With global wastewater generation projected to rise 24% by 2030, per the World Health Organization estimates, CPVC pipes can handle flows up to 95°C, reducing replacement frequency by 40% in treatment plants. Recent developments, such as the U.S. Infrastructure Investment and Jobs Act allocating US$55 Billion for water infrastructure, underscore demand potential, enabling companies to target municipal projects for revenue growth.

In India, the Namami Gange Programme has sanctioned 203 sewerage infrastructure projects, creating 6,255 million liters per day sewage treatment capacity, further demonstrating regional investment momentum. This aligns with the trends toward durable, low-leakage systems, where the EPA data highlights that enhanced wastewater treatment could address pollution affecting 2.2 billion people lacking safely managed services, fostering sustainable expansion for CPVC in resilient infrastructure.

Emerging Markets Growth and Capacity Expansion Initiatives

Unprecedented capacity expansion announcements and manufacturing investments in high-growth markets signal transformative opportunities for industry stakeholders. Lubrizol Corporation and Grasim Industries Limited commenced construction of the world's largest single-site CPVC resin plant with 100,000 metric tons of capacity in Vilayat, Gujarat, India. In addition to the resin site, Lubrizol is doubling its existing CPVC compound manufacturing capacity at its Dahej, Gujarat, India site from 70,000MT to 140,000MT. DCW Limited announced US$16.8 Million investment to expand CPVC production capacity from 20,000 MT to 50,000 MT, with phased implementation targeting 20,000 MT operational by Q2 FY26 and an additional 10,000 MT by the end of FY26.

Sekisui Chemical Co., Ltd. is increasing its CPVC compound production capacity in Thailand by 1.6 times, aiming for completion by March 2026 to meet rising demand in India and the Middle East. Such expansions in India lead the market, driven by the construction boom and government initiatives supporting the Make in India program, as well as the need to replace aging water distribution networks in developing economies.

Category-wise Analysis

Grade Insights

The extrusion grade dominates the chlorinated polyvinyl chloride market with approximately 65% share, driven by its widespread use in continuous manufacturing of pipes and profiles essential for plumbing and industrial applications. This grade's superior flow properties enable efficient production of long-length pipes resistant to temperatures up to 110°C, aligning with infrastructure demands as evidenced by American Society for Testing and Materials (ASTM) standards F441, which certify its durability in high-pressure systems.

In regions such as the Asia Pacific, where infrastructure projects proliferate, extrusion grade CPVC aligns with the plastic pipes market, offering cost savings of 15-20% in fabrication while ensuring durability against corrosion. This leadership is further justified by its compliance with international standards such as ASTM F441, driving adoption in high-volume sectors.

Production Process Insights

The aqueous suspension method leads with about 55% of the market share in CPVC production, favored for its scalability and ability to achieve uniform chlorination levels of 64-67%, ensuring consistent thermal stability. This method's use of water as a dispersion medium minimizes environmental impact and enables precise chlorination control, as detailed in chemical engineering patents from China National Intellectual Property Administration. This process minimizes energy use by 25% compared to solvent methods, as reported by the Chemical Manufacturers Association, making it economical for high-volume output. Its dominance is justified by widespread adoption in facilities producing corrosion-resistant pipes, bolstering reliability in the plumbing components market.

Application Insights

Plumbing systems hold the top position with roughly 45% share, attributed to CPVC's exceptional resistance to hot water and scaling, outperforming copper in longevity by 2-3 times per ASTM testing. Urbanization trends, with 68% global population urban by 2050 per UN-Habitat, amplify demand for leak-proof systems in residential setups. The segment growth is reinforced by CPVC's cost-effectiveness, corrosion resistance, preventing tuberculation and scale buildup, and compatibility with potable water standards, including FDA CFR Title 21 in the U.S. and Regulation (EU) No. 10/2011 in Europe.

CPVC's resistance to scaling and microbial growth, compliant with NSF/ANSI 61 standards from NSF International, ensures safe potable water delivery, reducing leaks by 40% over traditional materials. In the plumbing components market, this segment benefits from infrastructure investments, such as India's Jal Jeevan Mission targeting 550 million connections by 2024.

End-use Industry Analysis

The industrial end-use industry dominates the chlorinated polyvinyl chloride market, commanding approximately 40% market share by leveraging CPVC's chemical inertness in harsh environments such as chemical processing plants and power generation facilities. Industrial output growth, projected at approximately 3.5% annually according to World Bank forecasts, amplifies demand for durable solutions across manufacturing and energy sectors.

CPVC tubing demonstrates superior performance with pressure ratings of 690 kPa at 82°C per PPI technical standards, effectively handling corrosive fluid transfer. The U.S. Department of Commerce study underscores its preference in corrosion-prone environments, achieving downtime reductions of approximately 25% compared to conventional materials. ISO 9001 certified CPVC systems ensure reliable performance in chemical-resistant applications, establishing clear technical superiority over residential alternatives and solidifying market leadership in industrial sectors.

Regional Insights

North America Chlorinated Polyvinyl Chloride Trends

North America leads in CPVC innovation, with the U.S. market spearheaded by robust regulatory frameworks from the EPA and NFPA, mandating fire-resistant materials in over 80% of new builds since 2023. This has spurred a 15% rise in CPVC adoption for fire sprinklers, supported by the Building Officials and Code Administrators International (BOCA) codes emphasizing safety.

The region's leadership stems from high construction activity, valued at over US$1.5 Trillion in 2024 per the U.S. Census Bureau, favoring CPVC for its lifecycle cost benefits. Its ecosystem fosters R&D, with investments exceeding US$2 Billion in advanced materials per the National Institute of Standards and Technology, driving CPVC enhancements for plumbing in retrofits. This positions North America as a hub for high-performance applications amid infrastructure upgrades.

Europe Chlorinated Polyvinyl Chloride Trends

Europe's CPVC market thrives on regulatory harmonization under the EU Construction Products Regulation (CPR), ensuring uniform standards across Germany, the U.K., France, and Spain, where Germany accounts for 25% regional share due to stringent water quality directives. Recent EU Water Framework Directive updates have boosted CPVC in industrial equipment by 12% in 2024, as per European Environment Agency statistics.

Performance analysis reveals strong growth in the U.K. and France from post-Brexit infrastructure pushes, with Spain emphasizing sustainable piping in renovations, aligning with REACH compliance for chemical resistance. This fosters a cohesive market dynamic focused on durability and eco-standards.

Asia Pacific Chlorinated Polyvinyl Chloride Trends

Asia Pacific dominates with rapid growth in China, Japan, India, and ASEAN nations, where manufacturing advantages such as low labor costs drive 40% global production. China's infrastructure boom, with investments over CNY30 Trillion (US$4.11 Trillion) in 2025 per the National Development and Reform Commission, fuels demand for pipes in industrial hubs. China's Belt and Road Initiative has invested US$1 Trillion in infrastructure, increasing CPVC demand for pipes by 18% annually per the Asian Development Bank.

India benefits from anti-dumping duties extended in 2024, protecting local output, as reported by the Directorate General of Trade Remedies. Japan and ASEAN benefit from advanced production, with Japan's chemical sector innovating for high-purity applications.

Competitive Landscape

The global chlorinated polyvinyl chloride market exhibits a moderately consolidated structure, with top players controlling more than half of the market through strategic expansions and R&D investments exceeding US$500 Million annually. Companies focus on capacity enhancements, such as new plants in Asia, and partnerships for sustainable formulations to differentiate via superior heat resistance. Emerging models emphasize vertical integration, from resin production to end-products, fostering innovation in fire-safe applications while navigating regulatory shifts.

Key Industry Developments

- April 2025: Kaneka Corporation invested US$100 Million in a new extrusion facility in Japan, targeting a 20% output increase for plumbing exports.

- November 2024: Japanese petrochemical producer Sekisui Chemical plans to boost its chlorinated polyvinyl chloride (CPVC) compounds output capacity in Thailand during October 2025-March 2026 as demand in Asia, especially India, and the Middle East grows.

- November 2023: Lubrizol is doubling its existing CPVC compound manufacturing capacity at its Dahej, Gujarat, India site from 70,000MT to 140,000MT. DCW Limited announced a US$16.8 Million investment to expand CPVC production capacity from 20,000 MT to 50,000 MT.

Top Companies in the Chlorinated Polyvinyl Chloride Market

The Lubrizol Corporation (USA): A leader in specialty chemicals, Lubrizol drives the market through its Tempron brand CPVC, boasting a strong portfolio in industrial applications. Its maturity in North American manufacturing ensures reliable supply chains.

Sekisui Chemical Co., Ltd. (Japan): Renowned for advanced plastics, Sekisui drives the CPVC market via innovative extrusion grades, supported by R&D investments yielding heat-resistant variants for Asia-Pacific infrastructure. Portfolio strength includes sustainable formulations.

Kaneka Corporation (Japan): Kaneka excels in high-purity CPVC for fire protection, leveraging US$5 Billion polymer revenues and global maturity in chemical processing. Its expansion strategies enhance market positioning.

Companies Covered in Chlorinated Polyvinyl Chloride Market

- The Lubrizol Corporation

- Sekisui Chemical Co., Ltd.

- Meghmani Finechem Ltd.

- Shandong Novista Chemical Co., Ltd.

- Kaneka Corporation

- KEM One

- Shandong Yada New Materials Co., Ltd.

- DCW Ltd

- Shandong Xuye New Materials Co., Ltd.

- Sundow Polymers Co., Ltd.

- Mitsui & Co., Ltd.

Frequently Asked Questions

The chlorinated polyvinyl chloride market is valued at US$1,844.1 Million in 2025 and expected to reach US$3,733.2 Million by 2032.

Surging construction and infrastructure projects globally drive demand, with CPVC's heat resistance supporting urban plumbing needs.

Extrusion grade leads with 65% share, ideal for pipe manufacturing in infrastructure applications.

Asia Pacific leads, driven by manufacturing strengths and urbanization in China and India.

Wastewater treatment expansion offers potential, utilizing CPVC's chemical resistance for sustainable systems.

Leading players include The Lubrizol Corporation, Sekisui Chemical Co., Ltd., and Kaneka Corporation.