- Technology

- Video Management Software Market

Video Management Software Market Size, Share, and Growth Forecast, 2025 - 2032

Video Management Software Market By Deployment (On-premise, Cloud (VSaaS), Others), Component (Core VMS, Video Analytics (AI), Others), Vertical, and Regional Analysis for 2025 - 2032

Video Management Software Market Size and Trends Analysis

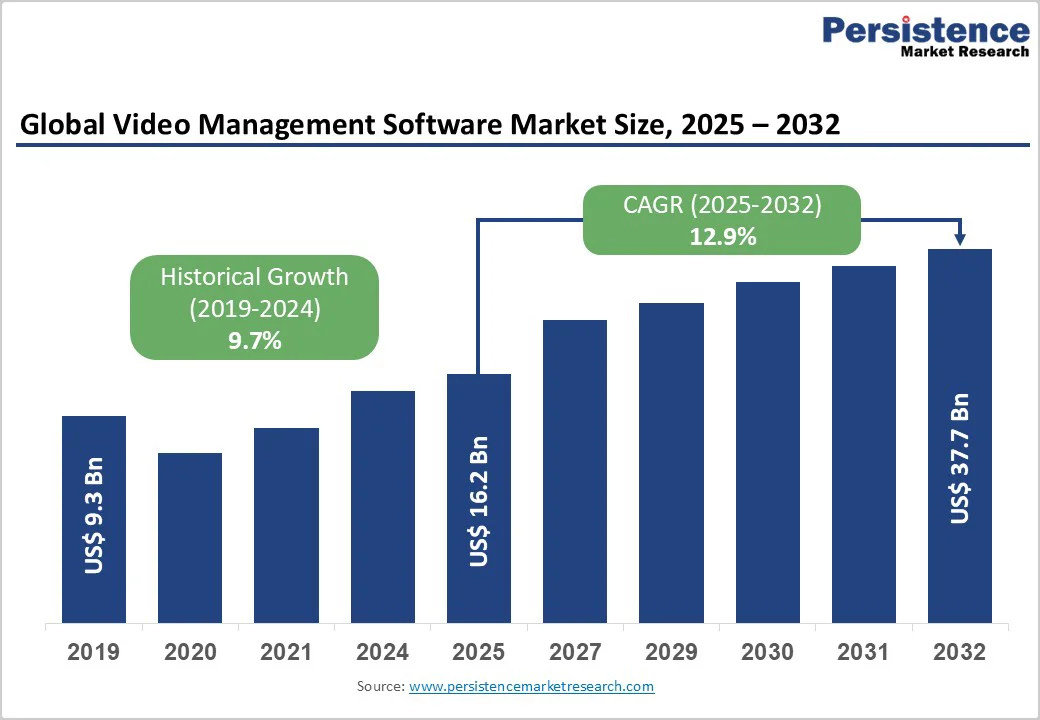

The global video management software market size is likely to be valued at US$16.2 Billion in 2025 and is expected to reach US$37.7 Billion by 2032, growing at a CAGR of approximately 12.9% during the forecast period from 2025 to 2032, driven by rapid cloud migration, accelerating adoption of AI-based analytics that turn video into operational intelligence, rising security investments across public and private sectors, and increased deployment of IP cameras in retail, transportation, and smart-city ecosystems.

Enterprises are shifting from on-premise VMS to hybrid and cloud platforms for scalability, lower costs, and integrated analytics, while prioritizing cybersecurity, privacy, and legacy-system compatibility.

Key Industry Highlights

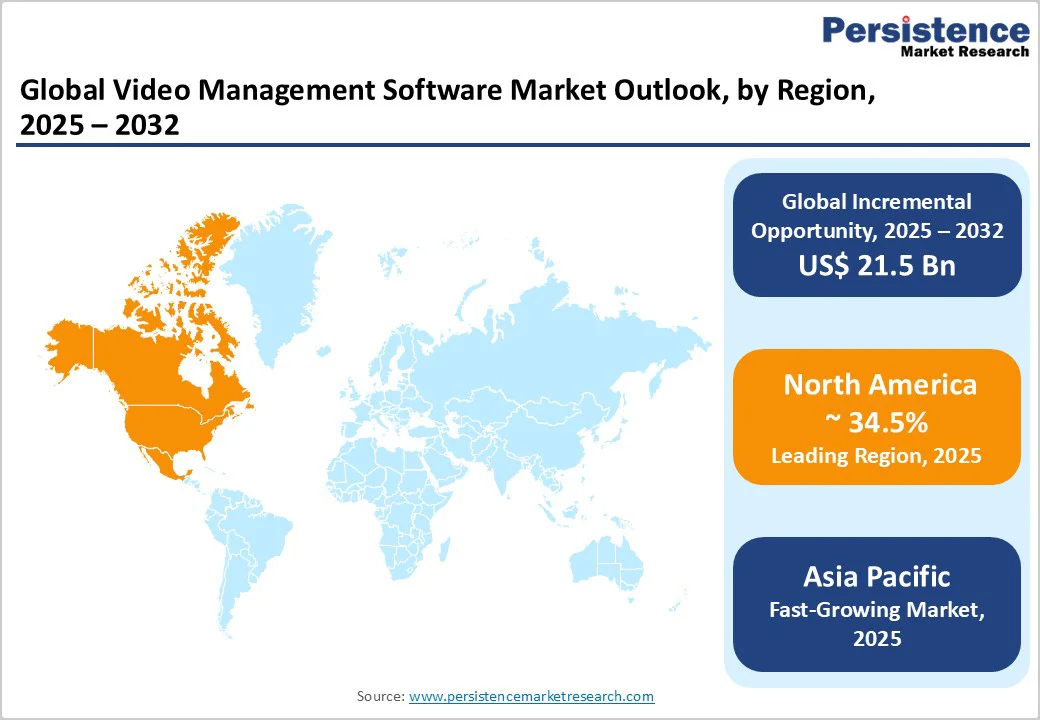

- Leading Region: North America retained the largest share of the VMS market in 2025, accounting for over 34.5% of global revenues, supported by mature surveillance ecosystems and high enterprise adoption.

- Fastest-growing Region: Asia Pacific recorded the fastest growth, driven by rapid smart-city deployments and rising investments in logistics and retail security.

- Investment Plans: Cloud-first migration and AI-driven analytics dominated capital allocation, with major vendors reporting double-digit annual growth in cloud subscriptions and edge-AI enhancements.

- Dominant Deployment Mode: On-premise systems continued to hold the largest share at around 54.8% of installations, supported by legacy investments and compliance-heavy sectors.

- Leading Component: Core VMS software remained the highest-revenue segment, contributing over 47.9% of the total market value due to its foundational role in multilevel surveillance architectures.

| Key Insights | Details |

|---|---|

| Video Management Software Market Size (2025E) | US$16.2 Bn |

| Market Value Forecast (2032F) | US$37.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 12.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 9.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Cloud Transformation and VSaaS Adoption

The shift from locally hosted VMS to cloud-based and hybrid Video Surveillance-as-a-Service (VSaaS) models is one of the strongest growth catalysts. Cloud VMS reduces upfront capital investments, centralizes management for multi-site operations, and enables rapid rollout of analytics capabilities such as object detection, license-plate recognition, and behavioral analysis.

Organizations planning digital transformation are prioritizing cloud architectures for scalability and ease of updates, while distributed enterprises and educational institutions increasingly adopt VSaaS to unify monitoring. This shift strengthens recurring-revenue models for providers and allows higher value capture through subscription analytics and integration add-ons.

AI and Edge Analytics Monetization

AI-driven analytics have transitioned from optional enhancements to core decision-making tools. Adoption is being fueled by edge-AI cameras that process data on-device, reducing bandwidth demands while enabling real-time insights such as anomaly identification, people counting, and crowd analysis.

VMS platforms integrating AI natively or through modular add-ons have seen expanding subscription uptake. As enterprises recognize quantifiable benefits such as reduced incident response times and improved operational efficiency, analytics attach-rates continue rising. This trend boosts average revenue per customer and strengthens long-term retention, positioning AI analytics as a major monetization engine for VMS providers.

Regulatory and Public Safety Programs

Government-led programs in urban surveillance, transportation safety, school protection, and emergency-response modernization are creating a consistent pipeline of VMS procurement. Regulations mandating longer video-retention periods, audit-compliant logging, and secure chain-of-custody processes are pushing organizations to upgrade outdated VMS infrastructure.

Public-sector deployments often involve centralized command centers, integrated communications, and evidence-management capabilities, increasing overall solution value. These long-cycle contracts provide predictable revenues and enable suppliers to cross-sell analytics, cloud hosting, and maintenance services.

VMS companies with strong compliance and cybersecurity credentials are especially well-positioned in regions with evolving governance and data-handling requirements.

Barrier Analysis - Integration Complexity and Legacy Migration

Organizations with large fleets of legacy DVRs, NVRs, and proprietary camera systems face technical hurdles when migrating to modern VMS. Multi-vendor interoperability, complex network structures, and integration with access control or alarm systems prolong deployment timelines and raise professional services expenses.

Migration-related services often account for a significant portion of total project cost, challenging budget-constrained users. This slows adoption in some medium and small enterprises, while increasing demand for open-platform VMS solutions that support standardized protocols and flexible APIs.

Data Privacy and Cybersecurity Risks

Heightened focus on data protection and cybersecurity is increasing compliance requirements for VMS deployments. Organizations must implement strong encryption, secure role-based access controls, and hardened cloud environments to avoid breaches or regulatory penalties. Privacy obligations such as video redaction, consent management, and defined retention schedules add operational complexity.

Failure to meet compliance obligations can delay procurement, particularly in financial institutions, public agencies, and education sectors. Cybersecurity-readiness clauses added to contracts increase implementation costs and can deter risk-averse buyers from undertaking large-scale modernization.

Opportunity Analysis - Hybrid Cloud for Multi-site Enterprises

Hybrid cloud architectures combining local edge recording with centralized cloud management present one of the largest growth opportunities. These models deliver local resilience and bandwidth optimization while enabling cloud analytics and unified oversight across geographically dispersed facilities.

Demand is expanding within retail, logistics, corporate campuses, and hospitality chains. Hybrid deployments typically produce higher subscription revenues than traditional perpetual licenses, allowing vendors to capture incremental value from analytics, multisite orchestration, and ongoing maintenance. Providers offering seamless cloud migration, flexible subscription tiers, and certified multi-vendor integrations will gain share in this fast-expanding segment.

AI-driven Operational Intelligence Beyond Security

VMS is increasingly used for operational intelligence, not just security. Retailers use video analytics for queue management and merchandise optimization, logistics operations track workflows and space utilization, and industrial sites monitor compliance and productivity.

These cross-functional applications extend VMS relevance into operational, planning, and customer-experience departments. Early adopters report measurable ROI, such as reduced shrinkage, optimized staffing, and improved process throughput. As organizations integrate VMS with ERP, workflow tools, and enterprise SaaS platforms, operational analytics could account for a meaningful share of incremental VMS spending over the next five years.

Category-wise Analysis

Deployment Mode Insights

On-premise VMS continues to hold the largest market share at 54.8%, driven by long-standing enterprise deployments, legacy maintenance agreements, and sectors requiring strict data-residency compliance. Industries such as large retail chains, transport authorities, and critical-infrastructure operators often maintain on-premise systems due to significant hardware investments, predictable maintenance cycles, and reliance on low-latency, on-site processing.

Airports, for example, operate high-throughput on-premise architectures integrated with access control, perimeter security, and regulated storage servers. Similarly, power utilities and government agencies favor on-premise deployments to comply with regulatory audits and manage classified data workflows. The extended lifecycle of NVRs, servers, and storage arrays reinforces on-premise dominance, even as cloud-first adoption grows among newer organizations.

Cloud-based VMS (VSaaS) platforms are expanding at the fastest rate, offering elastic scalability, lower total cost of ownership, and simplified software maintenance. Cloud-native solutions provide automated updates, integrated analytics, rapid provisioning, and centralized multi-site monitoring. Growth is particularly strong among distributed retailers, logistics hubs, and mid-sized enterprises prioritizing remote management.

Quick-service restaurant chains, for instance, increasingly manage hundreds of outlets via centralized cloud platforms, while logistics firms adopt hybrid deployments combining on-site recording with cloud analytics for vehicle tracking and safety compliance. Cloud VMS adoption thrives in regions with robust broadband infrastructure and supportive data-governance frameworks, driving sustained double-digit recurring revenue growth for providers.

Component Insights

Core VMS software, encompassing recording management, live monitoring, playback, event correlation, device administration, and system health diagnostics, remains the largest market segment with a 47.9% share. It serves as the foundational layer for nearly all surveillance installations, managing cameras, storage, and alarms. Mature enterprise platforms retain customers through multi-year support agreements and standardized upgrade paths.

Federated VMS deployments are common in universities, corporate campuses, and transportation hubs, where multiple sites are managed from a centralized operations center. These systems often integrate with access control, intrusion alarms, fire panels, and emergency-response solutions to streamline incident management.

Despite growing adoption of advanced analytics, the core VMS layer continues to anchor procurement cycles and generate steady recurring revenues.

Analytics and AI capabilities are the fastest-growing segment, fueled by demand for automated detection, real-time intelligence, and post-event investigation tools. Organizations increasingly adopt modular analytics such as facial recognition, license-plate reading, behaviour detection, occupancy counting, and forensic search. Subscription models align with enterprise budgeting cycles and enhance per-camera value.

Edge-based analytics are widely used in retail for queue monitoring and theft prevention, while cloud-based AI supports logistics operations by analyzing dwell times, forklift safety, and throughput efficiency. Hybrid solutions combining edge AI with cloud dashboards are gaining traction, reducing bandwidth demands while delivering richer, actionable insights.

Regional Insights

North America Video Management Software Market Trends - Cloud-First Adoption, Analytics Expansion & Compliance-Driven Modernization

North America remains the largest regional market, holding over 34.5% of global share, supported by early adoption of cloud and hybrid VMS architectures.

The U.S. drives most demand through federal, state, and enterprise investments in surveillance modernization, transportation security, and digital transformation initiatives across airports, logistics hubs, higher-education campuses, and large retail chains. These sectors continue expanding VMS deployments as part of broader safety, compliance, and operational-efficiency programs.

The region’s multi-location enterprises, such as national retailers, QSR chains, and corporate campuses, adopted cloud VMS earlier than many global peers, benefiting from centralized dashboards, automated patching, remote administration, and mature broadband infrastructure.

This shift is reinforced by growing interest in managed video services, subscription-based billing, and advanced analytics used for loss prevention, operational insights, and incident response across retail, logistics, and corporate security environments.

North American procurement priorities increasingly emphasize multi-site visibility, reduced IT overhead, and integrated intelligence across access control, alarms, and analytics platforms. Deployment decisions are strongly influenced by a complex patchwork of state-level privacy regulations.

Requirements for encryption, audit logging, secure cloud environments, data residency, and retention controls play a central role in vendor evaluation. Government and enterprise buyers frequently prioritize VMS providers demonstrating compliance readiness, including FedRAMP, SOC 2, or CJIS-aligned frameworks, ensuring secure, scalable, and regulation-aware deployments.

Europe Video Management Software Market Trends - GDPR-Shaped Hybrid Architectures & Infrastructure-Integrated Surveillance

Europe represents a significant share of global VMS spending, though adoption varies widely across the region due to differing privacy regulations, industry structures, and procurement practices. The Nordics and the U.K. lead in cloud and hybrid VMS adoption, supported by strong digital infrastructure, progressive cloud policies, and high enterprise readiness for SaaS-based security systems.

Central and Eastern Europe, by contrast, maintains a more conservative stance. Many organizations continue to rely on on-premise systems due to strict compliance requirements, public-sector procurement limitations, and long-standing comfort with established infrastructure.

Activity is strong in high-value manufacturing, rail transport, retail chains, and public infrastructure, where organizations are gradually modernizing legacy surveillance environments. European airports, metro systems, and national rail operators increasingly integrate VMS with access control, perimeter intrusion detection, and passenger-flow analytics to enhance safety and operations.

GDPR remains a defining factor in design and deployment choices, shaping requirements for data minimization, masking and redaction, consent-aligned usage, and purpose-specific retention. This has accelerated the development of privacy-centric capabilities, including automated video-redaction tools, EU-based cloud storage nodes, and analytics tailored to rail safety and industrial quality control.

Vendors across Europe are releasing strengthened hybrid-VMS platforms with enhanced multi-site management and cyber-hardening, including GDPR-oriented masking workflows and cloud providers launching EU-specific infrastructure zones for video workloads.

Asia Pacific Video Management Software Market Trends-Smart-City Megaprojects, IP Migration & Large-Scale VMS Expansion

Asia Pacific is the fastest-growing regional market for video management systems, driven by rapid urbanization, expanding public-safety programs, and accelerated migration from analog to IP-camera networks.

Major economies, including China, India, Japan, Australia, and leading ASEAN nations, are deploying VMS at scale across smart-city projects, airports, metro systems, retail chains, and industrial facilities. The region hosts a broad mix of global enterprise vendors and strong domestic players offering tightly integrated hardware-software solutions.

Smart-city initiatives remain a primary catalyst, with municipalities implementing wide-area camera networks for traffic optimization, public-safety monitoring, and urban analytics. Transportation infrastructure growth, new metro lines, airport expansions, and upgraded seaports further boosts VMS demand.

While regulatory maturity varies across APAC, many countries are strengthening cybersecurity and video-surveillance governance. Requirements around local data hosting, cloud-deployment approvals, and compliance with regional security certifications increasingly shape procurement decisions.

Vendors with local data centers, government partnerships, and in-region integration teams are gaining market advantage. Recent developments include integrated traffic analytics platforms for metro authorities, AI-powered crowd-density monitoring for high-traffic public spaces, and hybrid VMS deployments built with regional cloud providers.

New large-scale management capabilities also support tens of thousands of cameras across multi-city or nationwide installations, reinforcing the region’s momentum.

Competitive Landscape

The global video management system market features established enterprise vendors with deep integration ecosystems alongside cloud-native challengers offering simplicity and scalability. Traditional vendors dominate government, critical-infrastructure, and large-enterprise deployments, while cloud providers lead in SMB and multi-site retail with rapid rollout and predictable subscriptions.

Market concentration is moderate, with competition focused on analytics, cloud performance, and cybersecurity. Leading players emphasize recurring revenue, advanced AI, open APIs, and strong security credentials, while challengers differentiate through ease of deployment, intuitive design, and competitive cloud pricing.

Key Industry Developments

- In February 2025, Genetec announced the addition of intrusion management to its Security Center SaaS platform, enabling unified threat detection by combining video surveillance, access control, and intrusion systems.

- In March 2025, Milestone Systems launched XProtect 2025 R1, bringing expanded cloud integration via the Arcules VSaaS plugin (now supporting more editions) and upgraded vehicle analytics for license-plate recognition (including classification, color, make/model, and angle detection).

Companies Covered in Video Management Software Market

- Genetec Inc.

- Milestone Systems

- Motorola Solutions (Avigilon)

- Eagle Eye Networks

- Verkada Inc.

- Axis Communications

- Hanwha Vision

- Bosch Security Systems

- Honeywell International

- Hikvision Digital Technology

- Dahua Technology

- Huawei Technologies

- Siemens Smart Infrastructure

- Panasonic i-PRO

- Johnson Controls (Tyco Security)

- ZKTeco

- Qognify (Hexagon)

- Salient Systems

- VideoInsight (Panasonic)

- Synology Inc.

Frequently Asked Questions

The global video management software market size in 2025 is estimated at US$16.2 Billion.

By 2032, the video management software market is expected to reach US$37.7 Billion.

Major trends include the rapid adoption of cloud and hybrid VMS, growing demand for AI-driven analytics, rising investments in edge-based video processing, expansion of multi-site unified monitoring, and stronger integration between VMS, access control, and operational analytics.

The on-premise deployment mode continues to lead the market, contributing roughly 54.8% of the installed base due to legacy hardware, regulatory compliance, and low-latency processing needs.

The video management software market is projected to grow at a CAGR of 12.9% from 2025 to 2032, driven by digital transformation across retail, logistics, transportation, and critical infrastructure.

Major companies include Genetec Inc., Motorola Solutions (Avigilon), Milestone Systems, Eagle Eye Networks, and Verkada Inc.