- Media & Entertainment

- Ad-Supported Video on Demand Market

Ad-Supported Video on Demand Market Size, Share, and Growth Forecast 2026 - 2033

Ad-Supported Video on Demand Market by Content (Media & Entertainment, Travel & Tourism, Sports, Others), by Streaming Device (Smart TVs, Laptops & Desktops, Smartphones & Tablets, Other OTT Devices), by Regional Analysis, 2026 - 2033

Ad-Supported Video on Demand Market Size and Trend Analysis

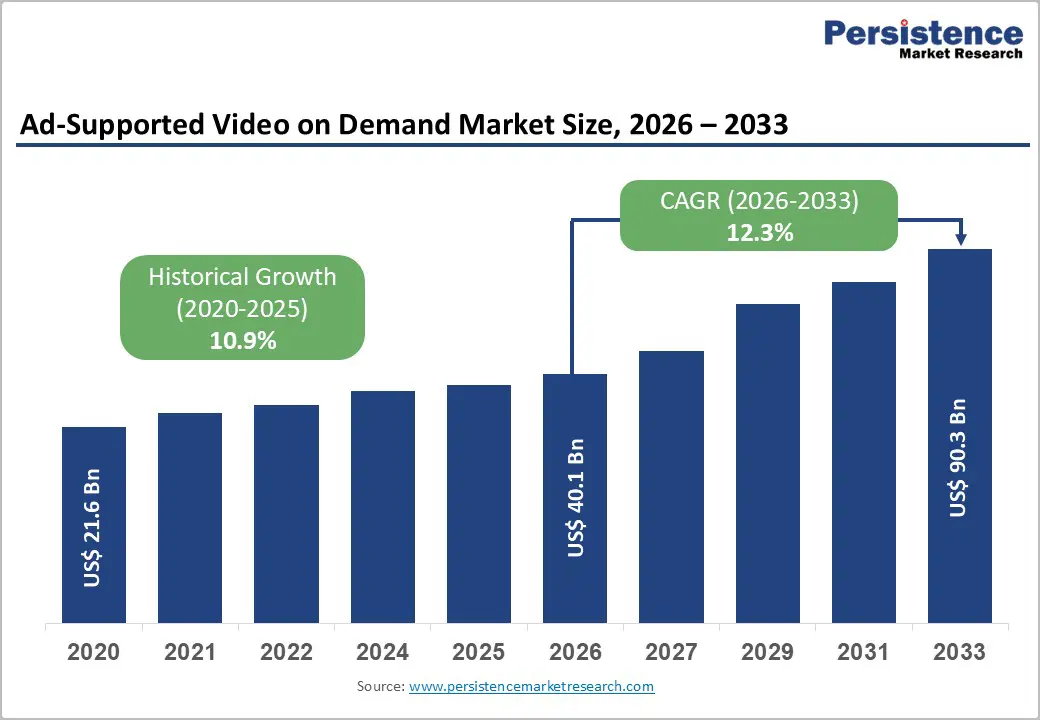

The global ad-supported video on demand market size is expected to reach US$ 40.1 billion in 2026 and is projected to reach US$ 90.3 billion by 2033, growing at a CAGR of 12.3% between 2026 and 2033.

This growth is primarily driven by rising consumer preference for free streaming platforms amid increasing subscription fatigue. Cord-cutting trends continue to strengthen AVOD adoption, with over 51 million U.S. households relying on OTT services for entertainment. At the same time, advertisers are increasingly shifting budgets toward digital video, as 78% prioritize AVOD for advanced audience targeting. Additionally, the dominance of ad-supported viewing, accounting for 72.4% of U.S. TV time, further supports sustained market expansion.

Key Market Highlights

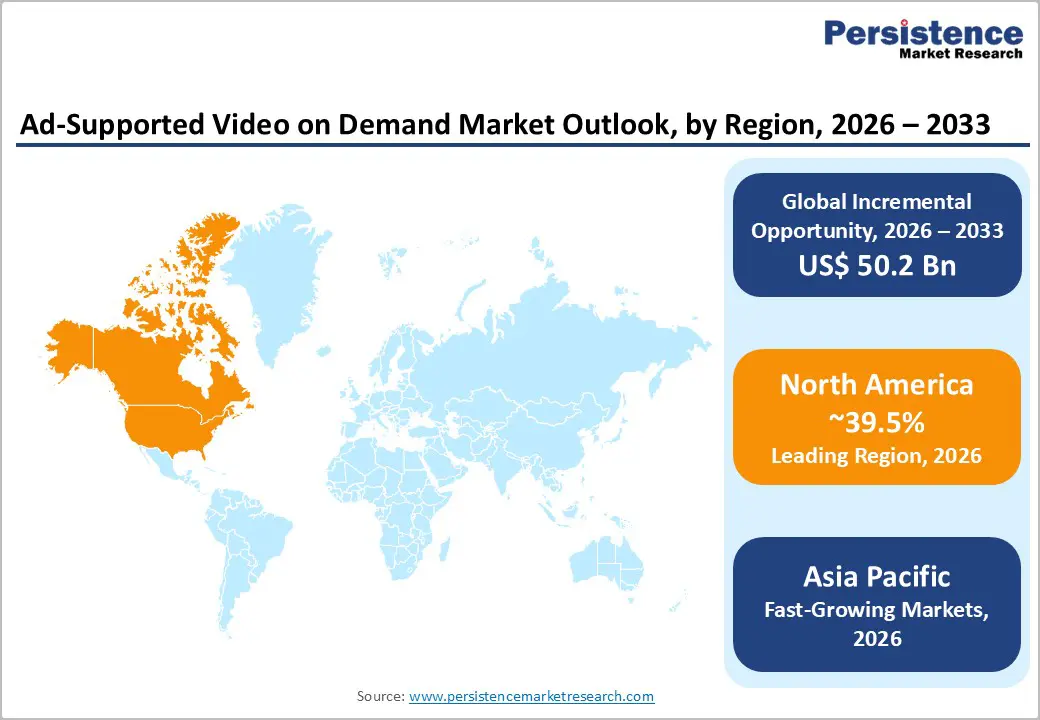

- Leading Region: North America leads the AVOD market with a 39.5% share in 2024, driven by U.S. cord-cutting trends and a mature advertising ecosystem.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at over 14% CAGR, fueled by mobile penetration in China, India, and ASEAN countries.

- Leading Content Category: Media & Entertainment dominates AVOD content with a 45% share, supported by extensive libraries on major platforms.

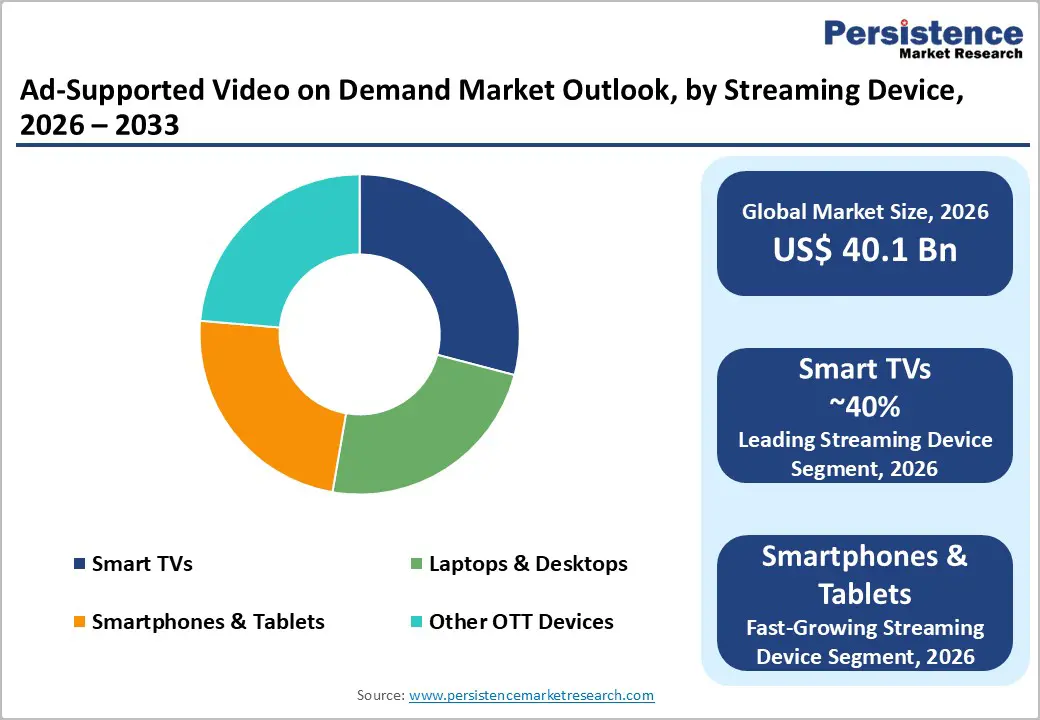

- Leading Device Category: Smart TVs lead device consumption with a 40% share, boosted by FAST channels and big-screen advertising placements.

- Key Market Opportunity: Hybrid monetization models represent a significant growth opportunity, surging at 21.1% CAGR and enabling diversified revenue streams.

| Global Market Attributes | Key Insights |

|---|---|

| Ad-Supported Video on Demand Size (2026E) | US$ 40.1 billion |

| Market Value Forecast (2033F) | US$ 90.3 billion |

| Projected Growth CAGR (2026 - 2033) | 12.3% |

| Historical Market Growth (2020 - 2025) | 10.9% |

Market Dynamics

Market Drivers

Surging Cord-Cutting and Subscription Fatigue Driving AVOD Adoption

Consumers are increasingly shifting away from traditional cable and paid streaming subscriptions as content costs rise, accelerating cord-cutting trends worldwide. With 72.4% of U.S. TV time now ad-supported and more than 51 million households abandoning cable, audiences are actively seeking cost-free entertainment alternatives. This behavioral shift strongly favors AVOD platforms, which offer broad content access without monthly fees, aligning well with price-sensitive viewers.

The impact is further reinforced by consumer preferences, as nearly 88% of cord-cutters favor free streaming services over paid options. In response, major OTT providers such as Netflix and Disney+ have launched ad-supported tiers to retain users and unlock incremental revenue streams. Notably, over half of new streaming subscribers now select ad-supported plans, highlighting AVOD’s expanding role in the digital entertainment ecosystem.

Advancements in Targeted and Programmatic Advertising Technologies

Rapid innovation in advertising technologies is significantly strengthening AVOD monetization capabilities. AI-driven personalization and data analytics have improved ad relevance, boosting viewer engagement by 32% in 2024 and supporting higher conversion efficiency. These capabilities enable advertisers to reach well-defined audiences at scale, making AVOD platforms increasingly attractive compared to traditional linear television advertising.

Programmatic advertising is another critical growth lever, with real-time bidding and automation expected to account for nearly 75% of AVOD ad inventory by 2027. Additionally, interactive and shoppable ad formats are generating strong consumer response rates, while mobile-first ad strategies benefit from rising smartphone usage. Collectively, these advancements are accelerating advertising budget shifts toward AVOD platforms, sustaining long-term market growth.

Market Restraints

Consumer Resistance to Ad Interruptions and Its Impact on AVOD Growth

While ad-supported streaming offers free access, many viewers experience ad fatigue, particularly during short viewing sessions, which diminishes engagement and satisfaction. Frequent interruptions can frustrate lighter users, while account sharing complicates precise ad targeting, reducing overall monetization efficiency. Connectivity issues, such as buffering, further disrupt the viewing experience, creating additional barriers to AVOD adoption and user retention.

Privacy concerns also play a critical role, as users increasingly worry about how personal data is collected and utilized for ad targeting. Surveys indicate a strong preference for ad-free options despite higher costs, forcing platforms to carefully balance ad frequency. This delicate trade-off limits revenue potential, as overloading content with ads risks alienating audiences while under-monetizing valuable viewership.

Privacy Regulations and Data Restrictions Constraining Market Expansion

Increasingly stringent privacy regulations worldwide, including GDPR in Europe and emerging U.S. privacy laws, are restricting platforms’ ability to collect and use user data for targeted advertising. These rules reduce ad effectiveness and lower CPM values, making it harder for AVOD providers to deliver measurable results to advertisers. Compliance also adds operational complexity and cost, impacting platform scalability.

Shared or multiple-user accounts further complicate segmentation, limiting precise targeting. Rising consumer opt-outs and restrictions on cookie-based tracking erode audience insights, weakening personalization strategies. Consequently, AVOD revenue growth faces constraints, as advertisers demand highly measurable, ROI-driven campaigns amid tightening data regulations and rising consumer privacy expectations.

Market Opportunities

Expansion into Emerging Markets: Unlocking AVOD Growth Potential

The rapid digital adoption in Asia Pacific presents substantial opportunities for AVOD platforms, driven by rising internet penetration and smartphone usage. Countries such as India and Indonesia are leading mobile AVOD growth through affordable internet access and locally relevant content. Telecom partnerships and low-cost streaming models allow providers to reach large populations, including China’s 1.4 billion users, positioning AVOD as a viable alternative to piracy.

As middle-class populations expand, demand for free and accessible entertainment rises, alongside increasing digital advertising spend. Platforms can leverage these trends by offering culturally tailored content, regional language libraries, and mobile-first experiences. This combination enhances user acquisition and engagement, creating a strong foundation for long-term market expansion across emerging economies.

Adoption of Hybrid Monetization Models to Enhance Revenue Streams

Hybrid monetization strategies are providing AVOD providers with new avenues for growth, combining ad-supported tiers with traditional subscription services. Leading platforms, including Netflix and Disney+, implement ad tiers to attract price-sensitive consumers while maintaining core subscriber bases. This approach helps retain users who might otherwise churn due to subscription fatigue, while simultaneously generating incremental ad revenue.

Over half of new subscribers now opt for ad-supported plans in exchange for lower fees, expanding both user reach and profitability. Integrating AI-driven ad optimization, personalized content recommendations, and exclusive content deals further strengthens the value proposition. These hybrid models allow platforms to diversify revenue streams and maximize engagement without compromising viewer satisfaction.

Category-wise Insights

Content Analysis

The Media & Entertainment segment dominates the AVOD market, holding a 45% share in 2025, driven by extensive libraries of movies, TV series, and original content. Platforms such as YouTube, Tubi, and Peacock capitalize on this vast content availability, attracting large, diverse audiences. Advertisers favor this category for its scale and targeting capabilities, with 78% prioritizing media and entertainment content. High engagement from binge-watching behavior and year-round relevance of various genres sustains the leadership position of this category, making it the backbone of AVOD platforms’ user retention and monetization strategies.

Meanwhile, educational and niche content segments are emerging rapidly as growth areas within AVOD. Demand for localized, short-form, and interactive content is increasing, especially among mobile-first viewers in emerging markets. Platforms are expanding offerings to include documentaries, kids’ programming, and user-generated content, leveraging personalization to boost engagement. These categories attract younger audiences and advertisers seeking targeted campaigns, presenting substantial opportunities for platforms to diversify content portfolios and capture new viewers beyond traditional entertainment.

Streaming Device Analysis

Smart TVs lead the AVOD device landscape, commanding a 40% market share in 2025, driven by large-screen experiences and integrated FAST channels on platforms like Roku Channel and Samsung TV Plus. Adoption is fueled by widespread ownership, with 79% of U.S. households equipped with smart TVs, enabling advertisers to command premium CPMs for living-room placements. Voice assistant integration and app ecosystems enhance accessibility, further solidifying smart TVs as the preferred home-viewing platform for ad-supported content.

Mobile devices are the fastest-growing category in AVOD consumption, benefiting from rising smartphone penetration and affordable mobile data plans. On-the-go viewing, app-based streaming, and short-form video formats appeal to younger, time-sensitive audiences. Platforms are optimizing mobile interfaces, interactive ads, and push notifications to increase engagement, while telecom partnerships and localized content support rapid adoption in emerging markets. Mobile’s flexibility and accessibility make it a key growth driver for AVOD expansion worldwide.

Regional Insights

North America Ad-Supported Video on Demand Market Trends

North America dominates the global AVOD market, with the U.S. holding a 39.5% share in 2024, driven by mature infrastructure, high digital ad spend, and strong OTT adoption. Platforms such as Hulu, Tubi, and Peacock lead viewership, supported by cord-cutting trends where 72.4% of TV time is now ad-supported. Regulatory frameworks encourage competition, sustaining market stability and investment in content licensing.

Innovation hubs like Silicon Valley drive advancements in AI targeting and programmatic advertising, enabling experimentation with interactive ad formats and optimized CPMs. Sports streaming deals, including NBA and NFL partnerships, concentrate ad budgets, protecting revenue even in a saturated market. Strong infrastructure, high household connectivity, and premium advertising placements reinforce North America’s leadership position in AVOD globally

Europe Ad-Supported Video on Demand Market Trends

Europe’s AVOD market is expanding steadily, led by the U.K. and Germany through broadcaster-backed platforms like ITVX and Joyn. Regulatory frameworks such as GDPR shape privacy-conscious ad targeting, while EU content quotas ensure investments in local productions. Hybrid models combining ad-supported and subscription tiers support adoption across diverse demographics. Programmatic advertising is gaining momentum, with a projected 11.5% CAGR, enabling better monetization and advertiser engagement.

France and Spain are seeing increasing uptake via mobile bundles, driven by rising smartphone penetration. Investments in local content and technology infrastructure balance the presence of global AVOD giants. Combined with cross-border digital strategies, these trends are positioning Europe as a key growth region for AVOD, emphasizing privacy-compliant yet effective advertising.

Asia Pacific Ad-Supported Video on Demand Market Trends

Asia Pacific is rapidly emerging as a key AVOD region, capturing 35.8% of the global market in 2025, driven by mobile-first consumption and expanding internet penetration. China leads the region with platforms like iQIYI and Youku, supported by mobile dominance and localized content that appeals to diverse demographics. Affordable smart devices and strong connectivity enable widespread adoption.

India and ASEAN countries are experiencing the fastest regional growth, led by platforms such as MX Player offering vernacular libraries and mobile-optimized experiences. Rising smartphone penetration and an expanding middle-class digital audience accelerate AVOD adoption. Targeted advertising, interactive formats, and telecom partnerships further enhance engagement and monetization, positioning Asia Pacific as the primary growth engine for the global AVOD market.

Competitive Landscape

The AVOD market remains highly consolidated, with leading players controlling over 60% of the global share through extensive content libraries, advanced technology, and robust user bases. Market leaders focus on expanding their offerings via mergers and acquisitions, investing heavily in AI-driven personalization, and launching hybrid ad-supported tiers to attract price-sensitive consumers while retaining existing subscribers.

Differentiation strategies increasingly revolve around innovative ad formats, including interactive and shoppable ads, as well as exclusive content to drive engagement. Meanwhile, the rise of FAST (Free Ad-Supported Streaming TV) models is fragmenting long-tail competition but simultaneously consolidating premium inventory, reinforcing revenue potential for dominant platforms.

Key Market Developments

- In April 2025, Amazon Prime Video introduced ad-supported streaming in India, capitalizing on growing demand for free and lower-cost content amid subscription fatigue. The move allowed the platform to attract new users, diversify revenue streams, and compete in the expanding AVOD segment.

- In March 2025, Disney+ expanded its ad-supported offerings to additional international markets, strengthening its hybrid monetization strategy. This expansion enhanced subscriber retention, generated incremental advertising revenue, and positioned the platform competitively against other AVOD services while catering to cost-conscious viewers.

- In June 2024, Netflix launched its global ad-supported tier, attracting millions of users seeking discounted subscription options. The initiative boosted platform engagement, opened new advertising revenue channels, and demonstrated Netflix’s adaptation to evolving consumer preferences and AVOD market trends.

Companies Covered in Ad-Supported Video on Demand Market

- Alphabet Inc.

- Fox Corporation

- Paramount Global

- Roku, Inc.

- The Walt Disney Company

- Comcast Corporation

- Amazon.com, Inc.

- Samsung Electronics

- Charter Communications

- Fandango Media

- Chicken Soup for the Soul Entertainment

- Tencent Holdings

- iQIYI, Inc.

- Alibaba Group

- Baidu, Inc.

Frequently Asked Questions

The market is expected to reach US$ 40.1 billion in 2026, driven by growing adoption of free streaming.

Cord-cutting and subscription fatigue, with 72.4% U.S. TV time ad-supported and 88% cord-cutters favoring free tiers.

North America leads with a 39.5% share in 2024, supported by mature OTT infrastructure and high ad spending.

Hybrid monetization models offer growth potential, surging at 21.1% CAGR, combining subscriptions with ads for broader reach.

Leaders include YouTube, Hulu, Tubi, Roku Channel, and Pluto TV.