- Media & Entertainment

- Video PaaS Market

Video PaaS Market Size, Share, and Growth Forecast 2026 – 2033

Video PaaS Market by Deployment Type (Public Cloud and Private Cloud), by Application (Broadcasting Video Communication, Real-time Video communication, Video Content Management and Others), and End- user (Social, Media & Entertainment, Education, Healthcare, Banking & Finance and Others) and Regional Analysis for 2026 – 2033

Market Overview

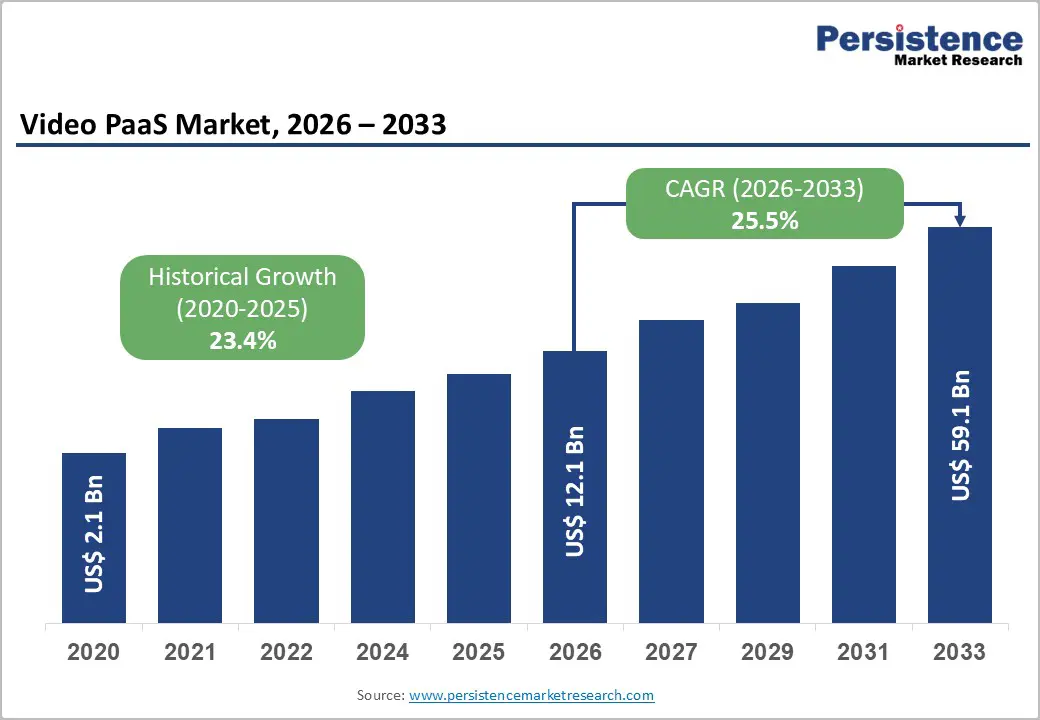

The global Video PaaS Market size was valued at US$ 12.1 Bn in 2026 and is projected to reach US$ 59.3 Bn by 2033, growing at a CAGR of 25.5% between 2026 and 2033. The market expansion is driven by three fundamental factors: accelerating digital transformation initiatives across traditional industries requiring scalable video delivery solutions, explosive adoption of artificial intelligence-driven communication capabilities enabling real-time transcription and automated meeting summaries, and proliferation of remote work and hybrid collaboration models necessitating sophisticated video communication infrastructure.

Key Market Highlights

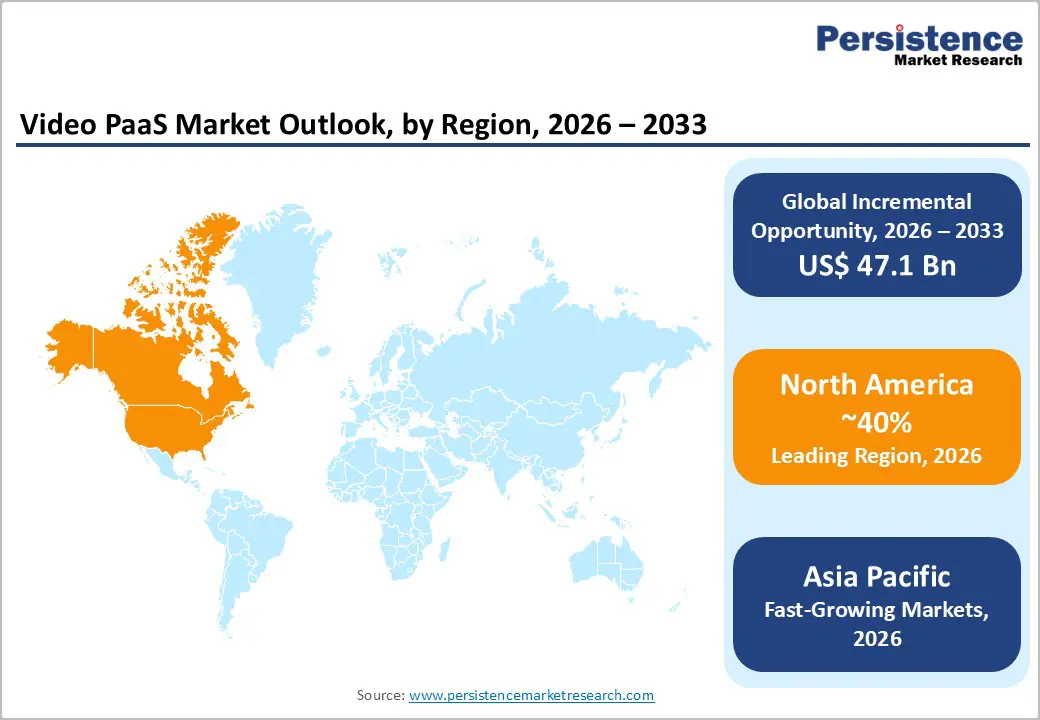

- Leading Region: North America maintains global market leadership with approximately 40% market share, supported by mature digital infrastructure, technology innovation ecosystems, and leading video PaaS platform providers, combined with strong enterprise IT budgets and normalized remote work adoption across corporate, financial services, and healthcare sectors driving sustained demand.

- Fastest Growing Region: Asia Pacific represents the fastest-growing region with projected CAGR of 25% through 2033, driven by rapid urbanization, industrial expansion, government digital transformation initiatives, mobile-first consumer preferences with 90%+ smartphone access, and explosive adoption of live streaming and e-commerce integration throughout Southeast Asia.

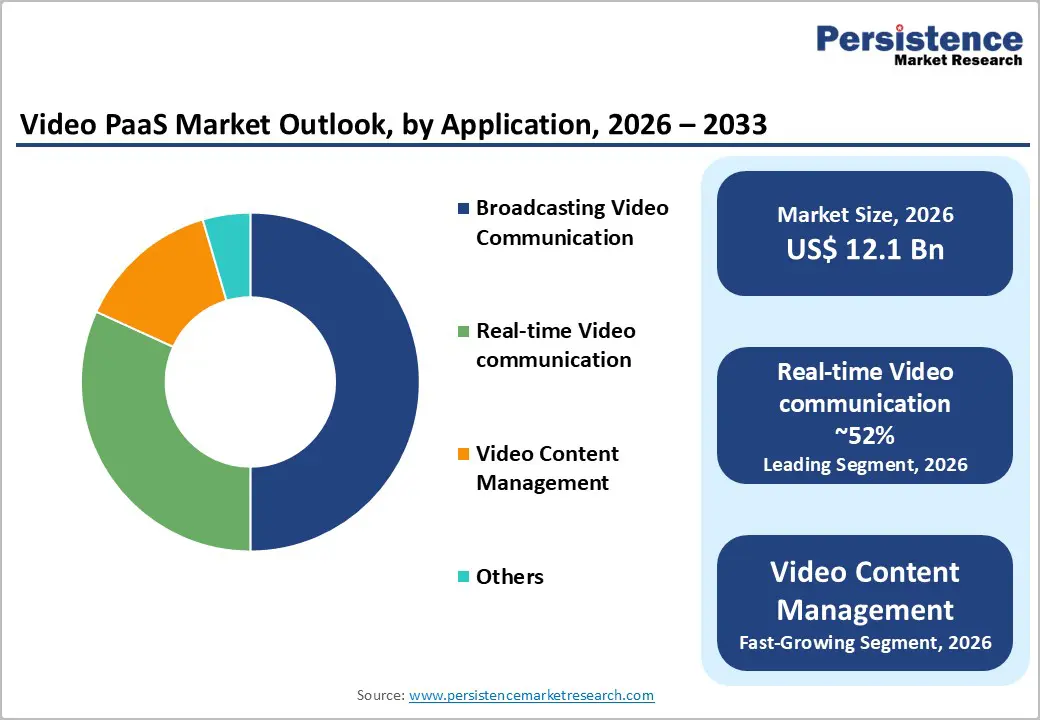

- Dominant Segment: Real-time Video Communication dominates with approximately 52% market share, reflecting universal adoption of synchronous visual interaction capabilities replacing traditional voice-only communication, established platform leadership through Zoom, Microsoft Teams, and Google Meet, and expanding integration within enterprise productivity ecosystems.

- Fastest Growing Segment: Real-time transcription and AI-powered communication features represent the fastest-growing application segment, driven by AI meeting transcription market growth from USD 3.86 billion in 2026 to USD 29.45 billion by 2034, exceptional accuracy improvements exceeding 95% accuracy in optimal conditions, and widespread demand for multilingual support, speaker identification, and automated meeting summaries.

- Key Market Opportunity: Healthcare telemedicine and medical education expansion represents the most significant growth opportunity, with 80% of individuals having used telemedicine services by 2023, 78% of physicians requiring 24/7 access to personalized video content, 88% of physicians preferring video-based learning over text alternatives, and sustained demand for HIPAA-compliant platforms supporting clinical education.

| Global Market Attributes | Key Insights |

|---|---|

| Video PaaS Market Size (2026E) | US$ 12.1 Bn |

| Market Value Forecast (2033F) | US$ 59.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 25.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 23.4% |

Market Dynamics

Market Growth Drivers

Digital Transformation Across Enterprise and Healthcare Sectors

Organizations across traditional industries including manufacturing, healthcare, education, and retail are accelerating digital transformation initiatives that fundamentally depend on robust video delivery infrastructure. Web Real-Time Communication (WebRTC) solutions are becoming central components of enterprise communication strategies, with the global WebRTC market projected to grow from USD 19.39 billion in 2026 to USD 755.48 billion by 2035 at a CAGR of 44.2%, demonstrating exceptional growth momentum in real-time communication technologies. Healthcare providers demonstrate particularly strong demand, as 78% of physicians require 24/7 access to personalized video content for educational purposes, while 93% acknowledge that video content influences how they conduct their medical practice. This healthcare acceleration reflects broader institutional recognition that video platforms deliver superior engagement compared to alternative communication modalities.

AI-Powered Transcription and Automated Communication Features

Artificial intelligence integration within video platforms is transforming communication capabilities through real-time transcription, automated meeting summaries, and AI-driven speech recognition. AI meeting transcription tools achieve accuracy rates exceeding 95% in optimal conditions, with advanced natural language processing enabling speaker diarization, emotion detection, and context-aware content analysis. Global AI meeting transcription market is projected to grow from USD 3.86 billion in 2026 to USD 29.45 billion by 2034, representing exceptional growth driven by workplace collaboration demands and accessibility requirements. Real-time transcription capabilities with multi-language support for over 100 languages enable seamless participation for globally distributed teams, while speaker identification and sentiment analysis provide valuable insights into meeting dynamics and participant engagement patterns. Organizations report productivity improvements of 3-5 hours weekly through automated meeting documentation, action item extraction, and asynchronous content summary generation.

Market Restraints

High Bandwidth Requirements and Network Infrastructure Constraints

Video PaaS solutions demand substantial network bandwidth, particularly for high-definition streaming exceeding 1080p resolution or multiple concurrent participants in collaborative sessions. Organizations operating in regions with underdeveloped internet infrastructure encounter deployment challenges and elevated operational costs. Low-latency video delivery requires sophisticated edge computing infrastructure and content delivery optimization, increasing technical complexity and infrastructure investment requirements. Developing nations with limited 5G adoption and fragmented telecommunications infrastructure struggle to deliver consistent user experiences across diverse network conditions.

Data Privacy Concerns and Regulatory Compliance Complexity

Granular video communication data including participant identity, interaction frequency, content viewing patterns, and behavioral information creates substantial privacy concerns requiring robust data protection mechanisms. European Union Data Act and similar regulatory frameworks impose stringent data residency requirements, forcing platform providers to establish localized infrastructure across multiple jurisdictions. Compliance with GDPR, HIPAA, and sector-specific regulations requires comprehensive encryption, access controls, and comprehensive audit trails, increasing development and operational complexity. Consumer enrollment rates in residential demand response programs remain below 5% in many jurisdictions despite attractive incentives, demonstrating persistent consumer hesitation regarding data privacy with connected service providers.

Market Opportunities

Healthcare Telemedicine and Medical Education Expansion

Healthcare represents an exceptionally promising market for video PaaS expansion, driven by persistent demand for remote patient consultations, virtual care delivery, and medical education acceleration. Telemedicine services experienced 44% growth from 2015 to 2019, with adoption further accelerating post-pandemic as healthcare systems recognized operational efficiencies from virtual care delivery. Medical schools, continuing medical education providers, and healthcare systems require sophisticated video platforms supporting interactive educational content, live clinical demonstrations, and surgical procedure recording. Physician adoption of telemedicine increased from 5% in 2015 to 22% by 2019, with expectations for further acceleration as reimbursement models mature and digital literacy expand. Patient demand for remote consultations continues intensifying, with 55% of patients experiencing "much more satisfaction" with teleconsultations compared to in-person care, while 63% express interest in wider digital health solutions.

Real-Time Video Broadcasting for Media and Entertainment Integration

Media and entertainment companies recognize exceptional opportunities for live streaming integration with interactive engagement capabilities, creating immersive viewer experiences combining traditional broadcasting with real-time audience participation. Broadcast distribution segment is projected to grow at significant CAGR during the forecast period, driven by media companies' adoption of cloud-based video solutions for efficient content delivery and audience engagement. Live shopping and commerce integration with video platforms enable interactive purchasing experiences combining entertainment with e-commerce, particularly gaining traction in Southeast Asia where over 90% of users access content via smartphones. Streaming services are increasingly venturing into live sports and event-based programming, capitalizing on enduring demand for real-time content that requires low-latency delivery and high-quality video capture. Media & entertainment segment anticipated to grow at the fastest CAGR over the forecast period, reflecting rising consumer demand for on-demand video content and live-streaming services.

Category-wise Insights

Deployment Analysis

Public Cloud deployment dominates the Video PaaS market with approximately 68% market share in 2026, reflecting organizations' strong preference for cloud-native infrastructure offering exceptional scalability, maintenance simplicity, and cost efficiency. Public cloud deployment eliminates capital infrastructure investments, enabling rapid scaling to accommodate demand fluctuations without infrastructure procurement complexity. Managed services provided by public cloud vendors including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform deliver enterprise-grade infrastructure with built-in redundancy, disaster recovery capabilities, and global content delivery optimization.

Organizations require only software licensing costs and consumption-based infrastructure fees, substantially reducing total cost of ownership compared to on-premises alternatives. Public cloud's inherent elasticity accommodates variable demand patterns characteristic of video conferencing applications, automatically allocating resources to match demand without manual intervention. Hybrid deployment models are emerging as organizations seek to balance public cloud scalability with private infrastructure control for sensitive applications.

Application Analysis

Real-time Video Communication represents the largest application segment with approximately 52% market share in 2026, driven by universal demand for synchronous visual interaction replacing traditional voice calls. Zoom, Microsoft Teams, and Google Meet have established dominant positions through superior video quality, reliability, and seamless integration with enterprise productivity suites. WebRTC-based platforms increasingly commoditize real-time communication by offering developers accessible APIs and comprehensive SDKs that enable rapid deployment of video-calling capabilities within custom applications.

Broadcasting Video Communication demonstrates particularly strong growth momentum as media companies and content creators leverage video PaaS platforms for live event distribution, virtual conferences, and interactive webinars. Video Content Management systems integrated within video PaaS platforms enable organizations to organize, catalog, and distribute recorded video assets efficiently.

End User Analysis

Media & Entertainment constitutes the largest end-user segment with approximately 38% market share in 2026, reflecting sustained demand for streaming services, live event broadcasting, and interactive content creation. Entertainment platforms, including Netflix, Disney+, TikTok, and YouTube, drive substantial infrastructure investment in video PaaS capabilities supporting multi-bitrate streaming, geolocation-based content delivery, and audience analytics.

Education is the fastest-growing segment, driven by the persistent adoption of hybrid learning models that combine in-person instruction with recorded video content and live virtual sessions. Educational institutions including universities, K-12 schools, and corporate training organizations deploy video PaaS platforms for asynchronous learning content, live classroom instruction, and recorded lecture libraries. Healthcare demonstrates accelerating adoption through telemedicine expansion, medical education integration, and patient engagement video content.

Regional Insights

North America

North America maintains global market leadership with approximately 40% market share, supported by mature digital infrastructure, sophisticated enterprise technology adoption, and leading video PaaS platform providers headquartered in the region. United States demonstrates particularly strong demand driven by technological innovation ecosystems in Silicon Valley, Austin, and Seattle generating continuous platform improvements and feature enhancements. The region's mature telecommunications infrastructure enables consistent high-bandwidth delivery supporting demanding video applications including ultra-high-definition streaming and real-time interactive experiences.

Regulatory frameworks in North America generally facilitate technology adoption while establishing clear data protection standards, reducing adoption friction compared to regions with ambiguous regulatory environments. GDPR-equivalent state-level privacy regulations in California, Virginia, and other states drive investment in privacy-enhancing video platforms featuring granular consent controls and transparent data handling policies. Healthcare providers increasingly integrate video PaaS with electronic health records systems, requiring platform providers to maintain FDA compliance and HIPAA certification.

Europe

Europe represents the second-largest regional market with approximately 22% global market share, driven by stringent data protection regulations and emphasis on digital sovereignty requiring localized infrastructure deployment. European Union Data Act and GDPR enforcement have established strict data residency requirements, compelling video PaaS providers to establish European data centers and comply with comprehensive privacy documentation. Germany, the United Kingdom, and France lead regional adoption, driven by strong technology sectors and regulatory clarity providing a competitive advantage for compliant platform providers.

Manufacturing and industrial sectors in Northern Europe drive demand for technical collaboration platforms supporting remote equipment inspection and maintenance guidance across distributed facilities. The financial services sector's adoption accelerates as regulatory frameworks establish clear requirements for digital customer verification and secure communications, driving demand for certified, compliant video platforms.

Asia Pacific

Asia Pacific represents the fastest-growing regional market with a projected CAGR of 25% through 2033, driven by rapid urbanization, industrial expansion, and government digital transformation initiatives. China dominates regional adoption, with Alibaba Group, Tencent, and Huawei Technologies controlling substantial market shares through comprehensive ecosystem integration combining social media, e-commerce, and enterprise collaboration. India's burgeoning IT services and software development sectors drive substantial demand for cost-effective, feature-rich video communication platforms supporting remote collaboration across distributed development teams. Live streaming and e-commerce integration particularly dominates Southeast Asia, where over 90% of users access content via mobile devices, creating demand for mobile-optimized video platforms with low-bandwidth operation capabilities.

Healthcare telemedicine expansion across Asia-Pacific reflects constrained physician availability in rural areas and government initiatives promoting virtual care delivery to underserved populations. Manufacturing sectors in Southeast Asia drive demand for technical collaboration platforms supporting remote quality inspection and equipment maintenance guidance across distributed production facilities.

Competitive Landscape

Market Structure Analysis

The global Video PaaS market exhibits moderate consolidation, with dominant positions held by Twilio Inc., Agora.io, and Vonage (through its TokBox subsidiary), which together command approximately 45-50% of the market share through comprehensive platform portfolios and extensive developer ecosystems. Twilio maintains market leadership through superior developer-centric documentation, comprehensive API coverage spanning voice, SMS, email, and video, and strategic partnerships with OpenAI, enabling AI-driven communication features. Mid-tier technology companies, including Sinch, Vidyo, and Sightcall, specialize in vertical-specific solutions addressing healthcare, enterprise communications, and specialized use-cases. Company strategies emphasize API standardization, cross-platform interoperability, and the integration of AI capabilities to differentiate offerings in an increasingly commoditized market.

Key Market Developments

- In May 2025, GardaWorld Security Corporation unveiled ECAM, a leading AI-powered surveillance technology in North America. ECAM integrates cutting-edge live video surveillance with human expertise to provide precise and vigilant real-time protection.

- In April 2025, Hikvision India introduced the Power X DVR, a state-of-the-art upgrade in the digital video recorder (DVR) market. Crafted to boost both intelligence and performance, this next-gen DVR incorporates advanced technologies, delivering enhanced features and efficiency to improve video security systems.

Frequently Asked Questions

The global Video PaaS Market is projected to reach US$ 59.3 Bn by 2033 from US$ 12.1 Bn in 2026, representing a CAGR of 25.5% during the forecast period.

Primary demand drivers include digital transformation acceleration across traditional industries requiring cloud-based video infrastructure, AI-powered transcription capabilities achieving over 95% accuracy with multilingual support across 100+ languages, overwhelming healthcare demand with 88% of physicians preferring video-based learning and 78% requiring 24/7 personalized video content access.

Real-time Video Communication dominates with approximately 52% market share, reflecting universal adoption of synchronous visual interaction capabilities replacing traditional voice-only communication, established market leadership through Zoom, Microsoft Teams, and Google Meet integrations, and expanding integration within enterprise productivity ecosystems including Microsoft 365, Google Workspace, and Slack.

North America leads with approximately 40% of the global market share.

Market leaders include Twilio Inc., Agora.io, Vonage (through TokBox), Sinch, and Huawei Technologies.