- Pharmaceuticals

- Spinal Cord Trauma Treatment Market

Spinal Cord Trauma Treatment Market Size, Share, Growth, and Regional Forecast, 2025 to 2033

Spinal Cord Trauma Treatment Market by Treatment Type (Corticosteroid, Surgery, Spinal Traction), by Injury Type (Complete Spinal Cord Injuries, Partial Spinal Cord Injuries), by End User (Hospitals, Trauma Centers), by Regional Analysis, from 2026 to 2033

Spinal Cord Trauma Treatment Market Share and Trends Analysis

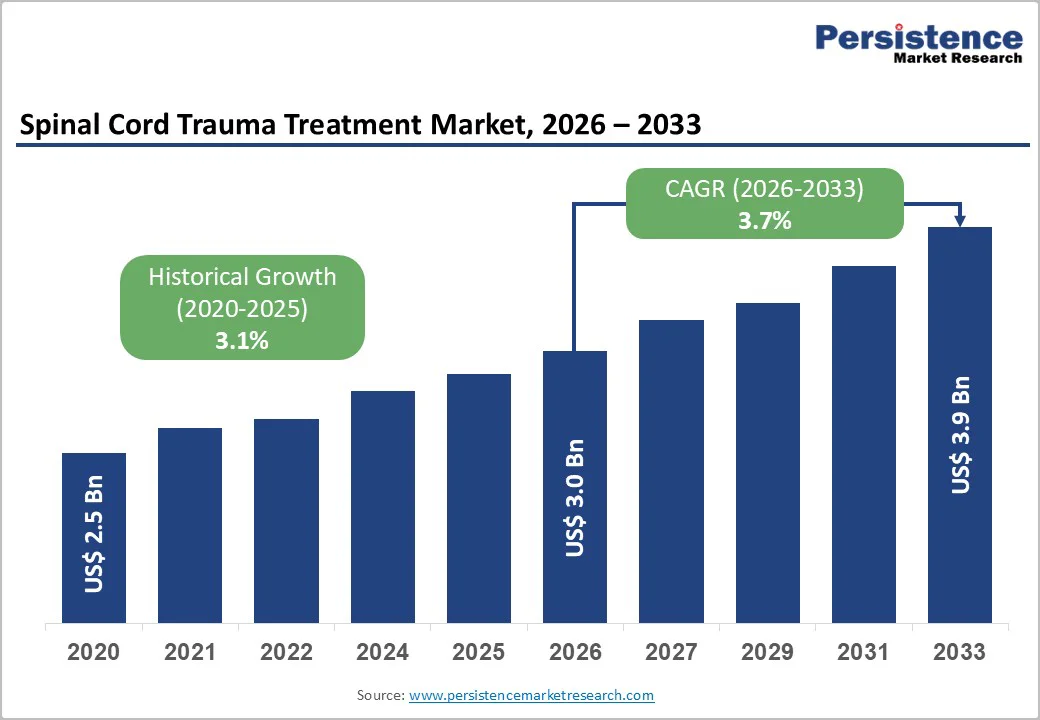

The global spinal cord trauma treatment market size is estimated to grow from US$ 3.0 billion in 2026 and reach US$ 3.9 billion by 2033, growing at a CAGR of 3.7% during the forecast period from 2026 to 2033.

The impact of spinal cord trauma results in severe pain, weakness, loss of mobility, breathing problems, and bladder or bowel dysfunction. Symptoms may improve after healing, but the treatment aims to stabilize and prevent further damage. Spinal cord trauma management includes medications, surgery to relieve pressure or repair structures, and rehabilitation involving physical and occupational therapy. Assistive technologies help improve movement, independence, and overall quality of life. Advanced research is exploring stem cell therapies, neural regeneration, and prosthetic systems to restore function. These innovations offer long-term potential for improving outcomes, enhancing neurological recovery, and reducing disability in patients affected by spinal cord injuries.

Key Industry Highlights

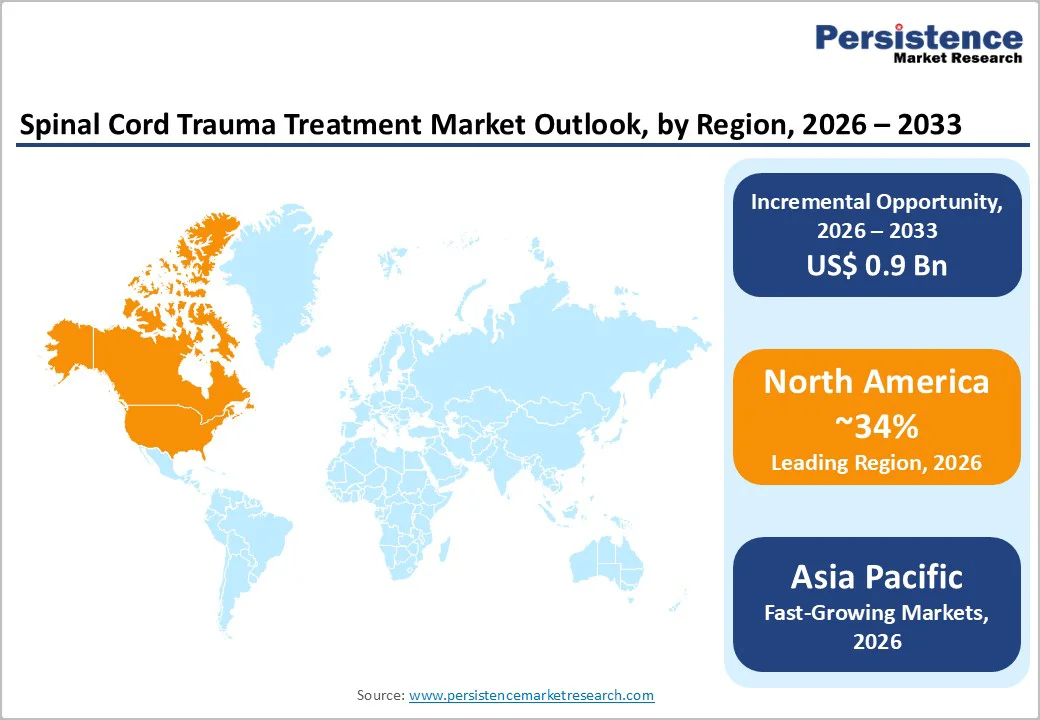

- Leading Region: North America leads the global market with approximately 34% share in 2025, supported by high SCI prevalence, advanced trauma networks, and favorable reimbursement.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising road traffic injuries, expanding tertiary care capacity, and leadership in regenerative medicine trials across China, Japan, India, and ASEAN.

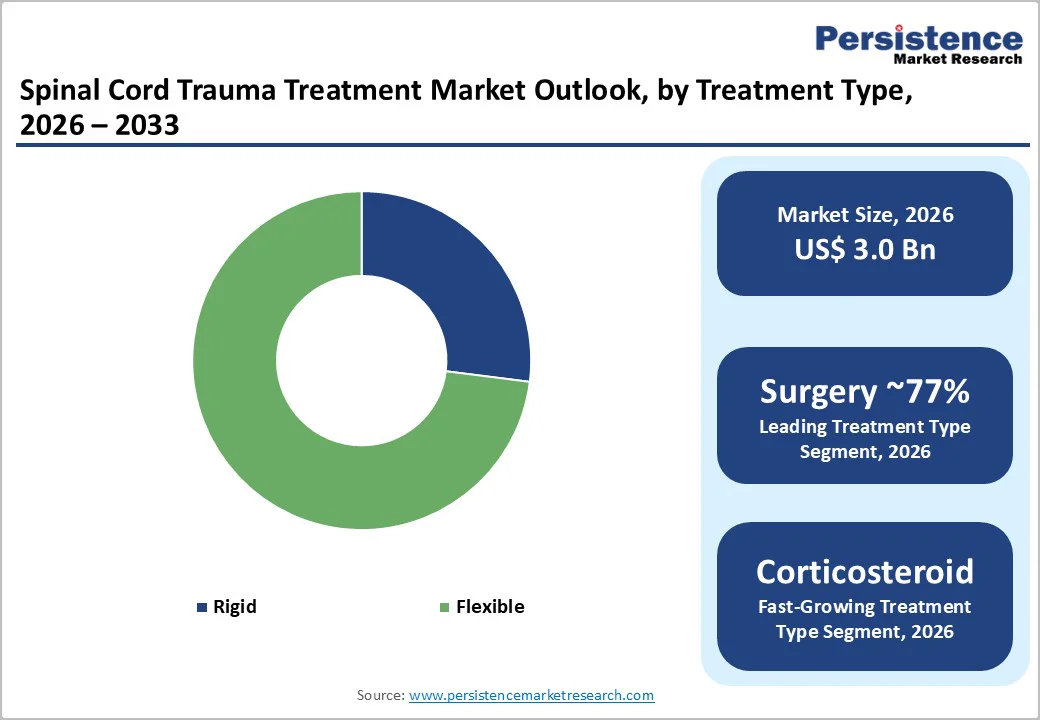

- Dominant Segment: Surgery remains the dominant segment due to high procedure volumes, effectiveness in stabilizing the spine, and widespread availability of advanced trauma systems.

- Fastest Growing Segment: Corticosteroids are the fastest-growing segment, driven by increasing adoption for neuroprotection, inflammation control, and early intervention in spinal injuries.

| Key Insights | Details |

|---|---|

| Spinal Cord Trauma Treatment Market Size (2026E) | US$ 3.0 Bn |

| Market Value Forecast (2033F) | US$ 3.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Dynamics

Driver - Rising Global Burden of Spinal Cord Injury

The continuous rising global burden of traumatic and non-traumatic spinal cord injuries (SCI) significantly drives the market growth. Epidemiological reviews show that incidence rates remain high worldwide, especially due to road accidents, falls, violence, and occupational hazards. Between 1990 and 2019, the number of people living with SCI increased by more than 50%, and multiple studies estimate standardized incidence rates of 11-12 cases per 100,000 population. The WHO indicates that more than 15 million patients were living with SCI in 2021, representing a large medically dependent population requiring emergency surgical stabilization, intensive neurological care, corticosteroid-based pharmacological intervention, complication management, and structured rehabilitation planning. A gradual rise in traffic-related trauma, increasing workplace injuries, and obesity-associated fall risk accelerates hospital admissions for acute spinal trauma.

Additionally, demographic trends are expanding the patient base. Aging populations increase susceptibility to vertebral fractures, degenerative spinal instability, and osteoporosis-associated trauma, especially in North America, Europe, Japan, China, and South Korea. Low - and middle-income countries are experiencing higher accident exposure due to limited enforcement of safety regulations, infrastructural gaps, and inadequate workplace protections. Increasing awareness of early surgical decompression, better diagnostic capabilities, and improved trauma network infrastructure also push treatment rates upward. Over the forecast period, growing incidence directly sustains demand for spinal fusion hardware, decompression devices, corticosteroids used in selected protocols, neuromonitoring solutions, ICU drugs, and structured rehabilitation services. This expanding caseload, coupled with higher survival rates due to better emergency systems, ensures persistent procedure volumes and repeat interventions.

Restraints - High Treatment Costs and Limited Access in Low-Resource Settings

A major restraint in the spinal cord trauma treatment market is the disproportionately high cost of surgery, long-term rehabilitation, and assistive solutions, especially in lower-income settings. Emergency decompression, intensive care admission, orthopedic implants, neuro-rehabilitation sessions, speech therapy, mobility aids, and home modifications significantly increase financial burden. In low- and middle-income countries, access is further limited due to minimal insurance coverage, shortage of trauma centers, and inadequate reimbursement schemes. WHO indicates that in-hospital mortality among SCI patients is nearly three times higher in low-resource settings, reflecting treatment delays, inadequate emergency stabilization, and lack of modern imaging and ICU infrastructure. Lifetime care requirements covering pressure sore management, urinary support, wheelchair upgrades, physiotherapy, and caregiver dependency restrict affordability and slow adoption of advanced technologies such as robotics-based rehabilitation and neurostimulation devices.

Opportunity - Expansion of Specialized Trauma and Rehabilitation Centers

An important market opportunity is emerging from the ongoing strengthening and expansion of specialized trauma and rehabilitation centers dedicated to spinal injury management. Across North America, Europe, and parts of the Asia Pacific, governments and private healthcare operators are prioritizing the modernization of trauma systems and building structured referral pathways for faster diagnosis and early stabilization. Recent epidemiological findings in Europe indicate traumatic spinal cord injury rates of nearly 25-30 cases per million population particularly with a higher occurrence of cervical injuries among elderly patients. This trend has created a strong need for organized trauma networks, early surgical access, and concentrated centers of excellence capable of managing complex cases.

In response, investments are being directed toward advanced imaging suites, neuromonitoring systems, rehabilitation technologies, and specialized acute care units. Clinical guidelines now emphasize rapid transfer to high-capability hospitals, coordinated rehabilitation programs, and multidisciplinary clinical teams. For manufacturers of surgical implants, fusion hardware, intensive care consumables, and rehabilitation devices, expanding hospital infrastructure translates into recurring procurement cycles and wider adoption of standardized treatment protocols. Pharmaceutical companies also benefit as hospitals increasingly implement structured pathways involving pain management drugs, corticosteroid use in selected cases, and complication-related therapies. As new facilities scale up, suppliers gain stronger institutional partnerships and long-term product demand.

Category-wise Analysis

By Treatment Type Insights

The Surgery segment dominates the By Treatment Type category, accounting for around 77% share in 2025, reflecting its central role in stabilizing the spine, decompressing neural elements, and preventing secondary neurological deterioration in traumatic spinal cord injury. Population-based data from European trauma networks show that more than half of traumatic SCIs involve cervical lesions, often requiring urgent surgical intervention in highly specialized centers. International guidelines and large multicenter surveys across the Nordic countries support early decompression and stabilization as standard of care in most clinically significant cases, which structurally anchors surgery as the primary revenue-generating modality across hospitals and trauma centers. In contrast, corticosteroid therapy has become more selectively used due to concerns over side effects and conflicting evidence on neurological benefits, while spinal traction is utilized mainly as an adjunct for fracture reduction or pre-surgical stabilization, thus contributing a smaller share to total market revenues.

By Injury Type

By Injury Type category, Partial Spinal Cord Injuries lead with an estimated 60% share in 2026, supported by epidemiological evidence that incomplete lesions are more common than complete injuries in many regions. Studies on SCI epidemiology indicate that improvements in pre-hospital care, rapid transport, and early surgical intervention have increased survival and contributed to a rising proportion of incomplete injuries, especially in high-income countries. Individuals with partial injuries often have better prospects for neurological and functional recovery and therefore become key candidates for advanced surgical techniques, rehabilitation programs, and emerging regenerative therapies, which concentrates treatment demand in this subgroup. This trend also encourages industry and academic sponsors to prioritize incomplete SCI populations in clinical trials for novel drugs, stem cell products, and neuroprosthetic devices, further reinforcing the commercial and clinical importance of the partial injury segment.

Region-wise Insights

North America Spinal Cord Trauma Treatment Market Trends

North America, led by the U.S., remains the largest market for spinal cord trauma treatment, accounting for approximately 34% of the global share in 2025. This dominance is driven by the high prevalence of spinal cord injuries, robust trauma care systems, and comprehensive reimbursement frameworks. In the U.S., certain studies estimate SCI prevalence at nearly 900 cases per million population, creating a substantial patient population requiring surgical stabilization, pharmacological intervention, and long-term rehabilitation. The region benefits from advanced trauma networks, rapid transfer protocols to Level I trauma centers, and widespread access to diagnostic imaging such as MRI and CT, as well as state-of-the-art operating rooms, all of which contribute to high procedure volumes for decompression and fusion surgeries.

North America also leads in innovation, supported by a strong ecosystem of medical device, biotechnology, and pharmaceutical companies developing regenerative and neuromodulation therapies. Numerous clinical trials are underway evaluating stem cell transplantation, biomaterial scaffolds, and electrical stimulation devices. Companies including InVivo Therapeutics, Acorda Therapeutics, Vertex Pharmaceuticals, and Pfizer are advancing neuroprotective and regeneration programs. FDA regulatory pathways, including Breakthrough Therapy and RMAT designations, facilitate expedited development and clinical adoption, reinforcing the region’s position at the forefront of spinal cord trauma treatment and technological innovation.

Asia Pacific Spinal Cord Trauma Treatment Market Trends

Asia Pacific spinal cord trauma treatment market is shaped by rising injury incidence, improving trauma systems, and expanding tertiary care capabilities. Increasing motor vehicle accidents, elderly fall-related injuries, and workplace-associated trauma continue to drive patient volume, particularly in India, China, Indonesia, and Thailand. Several countries are establishing trauma referral networks and designated spinal injury units, which are increasing surgical intervention rates and post-trauma rehabilitation demand. Governments in Japan, South Korea, and Australia are upgrading neurosurgical capacity, investing in rehabilitation robotics, and widening access to assistive technologies.

At the same time, market expansion is influenced by economic disparities across the region. Although advanced implants and early decompression surgeries show better outcomes, the high out-of-pocket burden restricts procedure uptake in emerging economies. Families often postpone treatment due to uncertainty regarding long-term functional recovery, especially when rehabilitation is prolonged and costly. Growing private hospitals, tele-rehabilitation solutions, and hospital-linked rehabilitation centers are gradually addressing these gaps. International collaborations, academic research partnerships, and localized manufacturing of surgical systems are also supporting market penetration. As healthcare insurance adoption improves and government reimbursement schemes expand, the region is expected to shift toward systematic trauma management and higher utilization of structured surgical and rehabilitation services.

Competitive Landscape

The global Spinal Cord Trauma Treatment Market has a moderately fragmented competitive landscape, comprising established pharmaceutical companies and emerging regenerative medicine developers. Major players such as Novartis AG, Pfizer Inc., Vertex Pharmaceuticals Inc., and Acorda Therapeutics focus on neuroprotection, inflammation control, pain management, and disease-modifying programs. Specialized firms, including InVivo Therapeutics, ReNetX Bio, BioArctic AB, Kringle Pharma, BioAxone Biosciences, and Pharmicell emphasize cell-based repair, regeneration-supportive biologics, and scaffold technologies. Companies actively pursue academic collaborations, licensing deals, and multicenter trial participation to expand portfolios. Increasing differentiation is driven by clinically validated recovery outcomes, improved safety, minimally invasive surgical support, and integration with rehabilitation, assistive technologies, and remote monitoring platforms for long-term functional improvement.

Key Industry Developments:

- In 2024, a Phase-1 study at Mayo Clinic demonstrated that stem cell therapy is safe and shows potential benefits for subacute and chronic spinal cord injury patients, advancing regenerative treatment.

- In May 2023, an article on TechTarget Network reported that the Reeve Foundation partnered with the University of Alberta to promote open data sharing in spinal cord injury research, enhancing knowledge exchange, transparency, and overall research value.

Companies Covered in Spinal Cord Trauma Treatment Market

- Acorda Therapeutics, Inc.

- Asterias Biotherapeutics

- ReNetX Bio.

- BioArctic AB

- BioTime, Inc.

- InVivo Therapeutics

- Kringle Pharma, Inc.

- Novartis AG

- Pfizer Inc.

- Pharmicell Co. Ltd.

- Vertex Pharmaceuticals Inc.

- Bioaxone Biosciences, Inc.

- Others

Frequently Asked Questions

The global spinal cord trauma treatment market is projected to be valued at US$ 3.0 Bn in 2026.

The spinal cord trauma treatment market is driven by rising spinal injury cases, better trauma management, and advances in regenerative, neuromodulation, and stem-cell therapies.

The global spinal cord trauma treatment market is poised to witness a CAGR of 3.7% between 2026 and 2033.

Major opportunities lie in commercializing personalized regenerative therapies, biomaterial scaffolds, and neuromodulation solutions within specialized rehabilitation networks.

Major players include Acorda Therapeutics, Inc., Asterias Biotherapeutics, ReNetX Bio., BioArctic AB, InVivo Therapeutics, Kringle Pharma, Inc., Novartis AG, Pfizer Inc., and Pharmicell Co. Ltd.