- Industrial Goods & Service

- Tool Box Market

Tool Box Market Size, Share, and Growth Forecast, 2026 - 2033

Tool Box Market by Product Types (Portable Tool Boxes, Rolling Tool Boxes, Others), Materials (Metal, Plastic, Others), End-user, Capacity Ranges, and Regional Analysis for 2026 - 2033

Tool Box Market Size and Trends Analysis

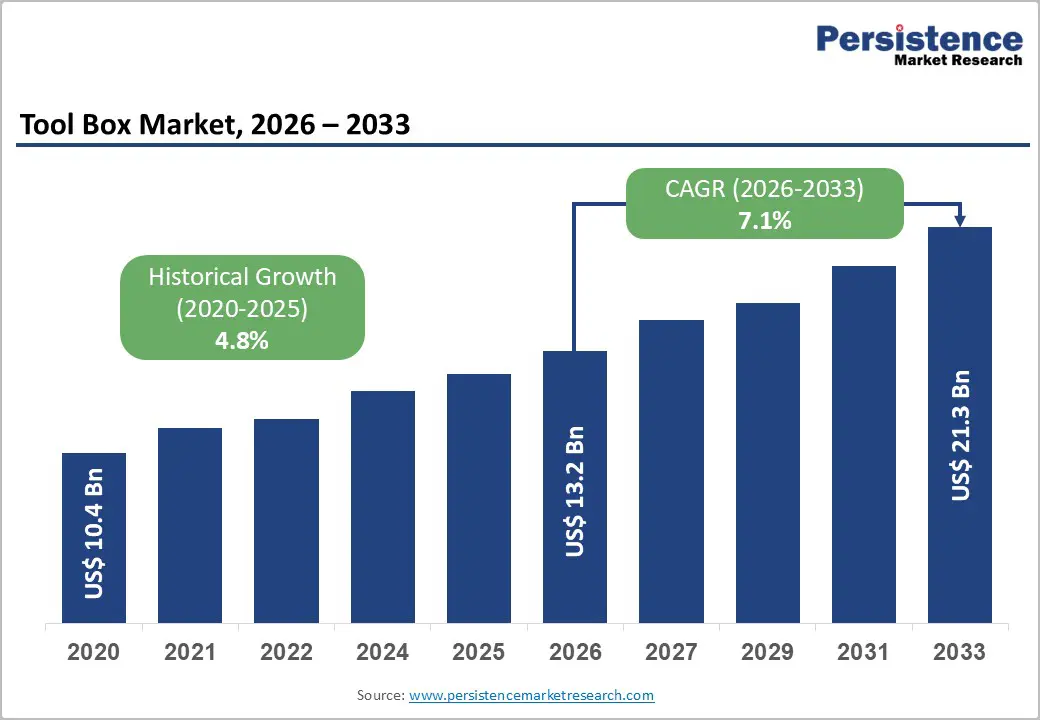

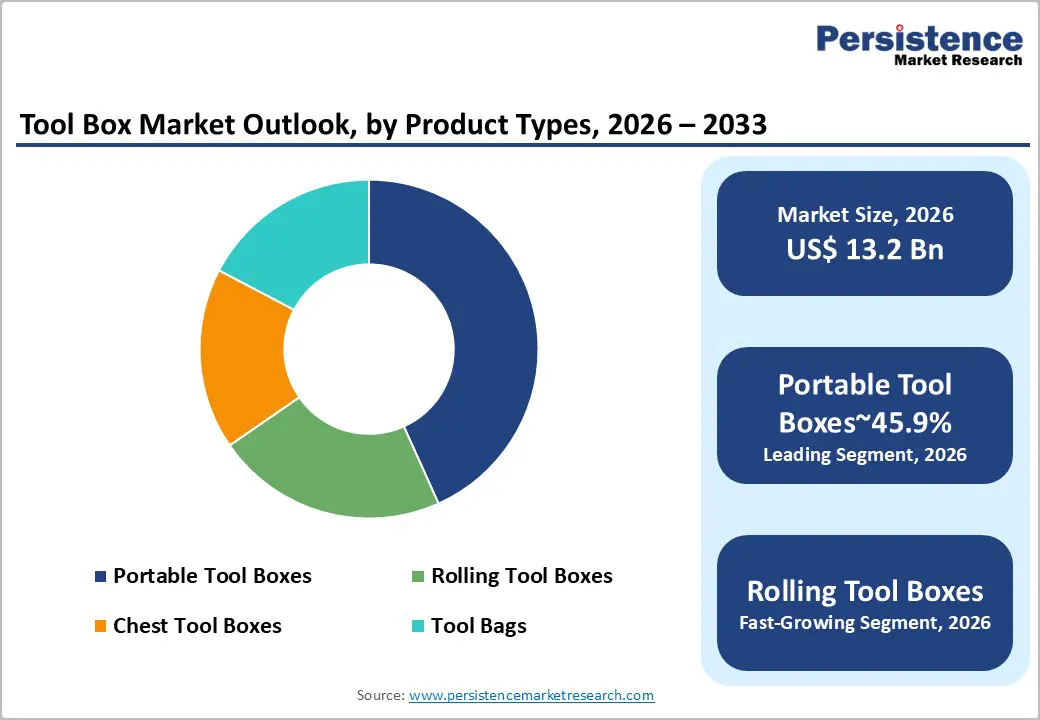

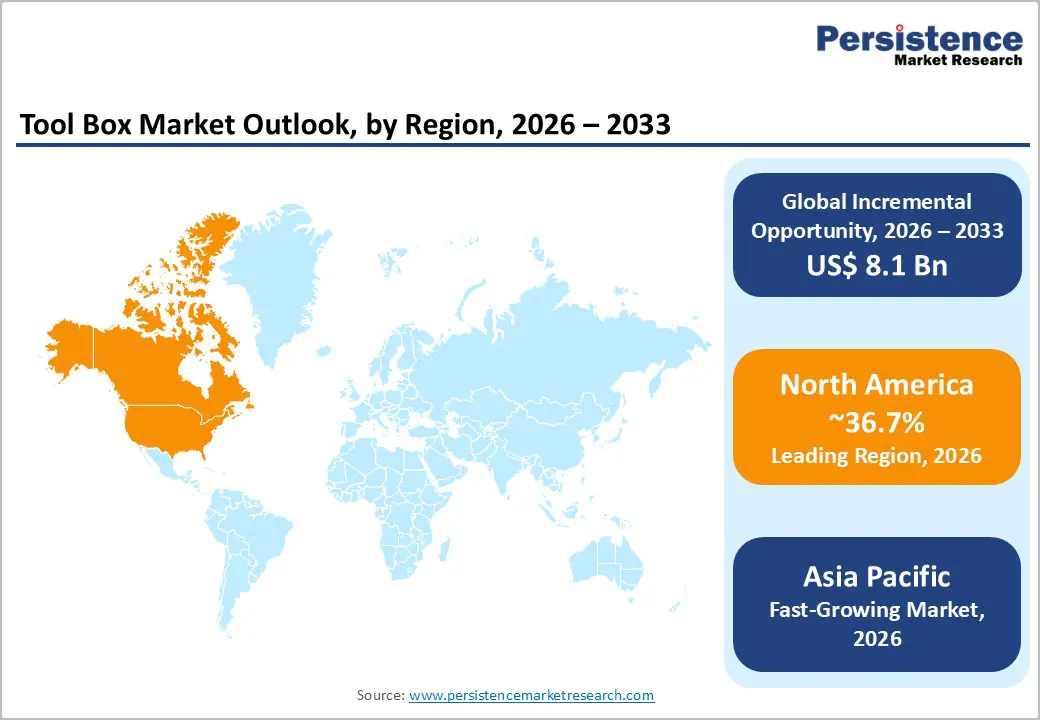

The global tool box market size is likely to be valued at US$13.2 billion in 2026 and is expected to reach US$21.3 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by rising professional tool ownership across construction, automotive service, and industrial maintenance sectors, alongside steady growth in the DIY and home improvement segment.

Structural drivers include sustained infrastructure spending and stable automotive repair activity in developed economies. Technological advancements such as modular rolling systems, integrated charging features, and digital tool tracking enhance product value. Supply-side shifts, including reshoring strategies and material cost pressures, influence pricing dynamics and competitive positioning.

Key Industry Highlights:

- Leading Region: North America is projected to hold 36.7% share, supported by high contractor density, a mature automotive aftermarket, and strong brand-led distribution networks such as Snap-on and Stanley Black & Decker.

- Fastest-growing Region: Asia-Pacific is likely to be the fastest-growing region, driven by manufacturing expansion in China, infrastructure development in India, and rising urbanization across ASEAN economies.

- Investment Plans: Major manufacturers are expanding domestic production capacity in the U.S. and increasing localized assembly operations in the Asia Pacific to strengthen supply chain resilience and reduce tariff exposure.

- Dominant Product Types: Portable toolboxes are expected to dominate, accounting for 45.9% of the market, owing to affordability, retail accessibility, and recurring replacement demand among DIY and light-trade users.

- Leading Materials: Metal toolboxes are estimated to hold a 42.3% share and maintain material leadership, reflecting professional preference for durability, load-bearing capacity, and long service life in automotive and industrial applications.

| Key Insights | Details |

|---|---|

| Tool Box Market Size (2026E) | US$13.2 Bn |

| Market Value Forecast (2033F) | US$21.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Professional Construction and Workshop Demand

Construction and professional maintenance activities remain the primary growth engines of the toolbox market. U.S. construction spending has exceeded in recent years, creating strong demand for durable and high-capacity storage systems. Growth in specialty trades, small contractors, and infrastructure modernization increases purchases of rolling chests, multi-drawer cabinets, and large mobile workstations. These products typically command higher average selling prices than portable boxes, thereby supporting revenue growth. Professional workshops and industrial facilities prioritize durability, load capacity, and security, reinforcing demand for premium metal tool storage systems and driving the projected 7.1% CAGR between 2026 and 2033.

Automotive Aftermarket and Service Expansion

The automotive aftermarket represents a significant end-use sector for tool storage solutions. As vehicle ownership remains high and fleet sizes expand, repair and maintenance activities continue to require organized, high-capacity storage systems. Professional garages increasingly adopt modular rolling tool boxes and integrated workshop cabinets to manage growing tool inventories. Fleet service centers favor standardized storage solutions to improve operational efficiency and technician productivity. This alignment between workshop modernization and storage investment contributes to rising average selling prices and recurring demand cycles. Growth in electric-vehicle servicing and advanced diagnostics further increases the number of tools per technician, thereby indirectly expanding storage requirements.

Product Innovation and Material Substitution

Product innovation significantly influences purchasing decisions across both professional and consumer segments. Metal toolboxes retain approximately a 42.3% share due to their durability and structural strength. Plastic and composite materials are expanding rapidly because of weight reduction, lower manufacturing costs, and improved impact resistance. Manufacturers are introducing hybrid designs combining reinforced polymers with metal frames to optimize performance and affordability. Innovations such as integrated charging ports, modular stacking systems, corrosion-resistant coatings, and digital inventory tagging increase product differentiation and enhance value per unit sold. These advancements elevate wallet share per customer and stimulate replacement demand.

Barrier Analysis -Raw Material and Manufacturing Cost Pressure

Steel and specialty alloy price volatility directly affects production costs for metal toolboxes, which account for 42.3% of the material segment. A sustained 10% increase in steel input costs can reduce gross margins by several percentage points for manufacturers relying on traditional metal construction. Producers must balance price increases against competitive pressures, particularly in price-sensitive consumer channels. While professional buyers tolerate higher prices for durability, excessive cost inflation can delay purchases or shift demand toward composite alternatives. This volatility constrains profitability and complicates long-term pricing strategies.

Channel Fragmentation and Pricing Pressure

The toolbox market operates through diverse distribution channels, including big-box retailers, professional distributors, tool truck networks, and e-commerce platforms. Rapid growth in online retail and private-label brands intensifies price competition, especially in portable and plastic categories. Smaller and mid-tier manufacturers face margin compression as marketing and logistics expenses rise. Channel fragmentation also increases customer acquisition costs and the complexity of inventory management. Without strong brand differentiation or pro-channel relationships, suppliers may struggle to maintain pricing power.

Opportunity Analysis - Premium Professional Storage Systems and Service Bundling

Premium workshop systems represent a significant strategic growth avenue as professional users increasingly prioritize efficiency, durability, and integrated workspace solutions. Manufacturers are moving beyond standalone storage units toward comprehensive workshop ecosystems that integrate high-capacity rolling chests, modular drawer systems, precision tool organizers, and integrated power management. These bundled configurations enhance workflow optimization by reducing tool-search time, improving safety compliance, and supporting structured inventory management in automotive service bays and industrial maintenance facilities. Professional buyers value long-term reliability, ergonomic design, reinforced drawer slides, anti-tilt safety mechanisms, and corrosion-resistant finishes, which elevate purchasing decisions from transactional to investment-driven. Suppliers are also introducing value-added services, including extended warranties, preventive maintenance support, customization options, and branded, fleet-standardized storage programs. Subscription-based consumable replenishment, accessory upgrades, and tool-tracking integration further strengthen customer retention while generating ongoing revenue streams. This shift toward solution-oriented offerings positions premium workshop systems as a cornerstone of competitive differentiation in the professional segment.

Consumer DIY Growth and E-Commerce Expansion

Plastic and composite portable toolboxes and tool bags are experiencing strong demand in DIY channels. Growth in home renovation, urban housing upgrades, and social media-driven DIY culture increases consumer ownership of tools. Direct-to-consumer models and online marketplaces enable manufacturers to expand reach with logistics-optimized SKUs. Lightweight materials reduce shipping costs and support modular product ecosystems. As DIY participation expands in North America, Europe, and the Asia Pacific, this segment provides steady mid-single-digit growth potential, contributing incremental volume gains to overall market expansion.

Category-wise Analysis

Product Types Insights

Portable tool boxes are anticipated to account for approximately 45.9% of market share in 2026, reflecting their broad accessibility across consumer and light-commercial markets. Their compact design, lower price points, and strong distribution through home improvement retailers such as Home Depot and Lowe’s, as well as e-commerce platforms, sustain consistent demand. Products range from single-tray polypropylene models for household maintenance to reinforced steel portables with lockable latches designed for trade technicians. Brands such as Stanley Black & Decker and Apex Tool Group offer diversified portable lines targeting both entry-level DIY buyers and semi-professional users. Shorter replacement cycles, especially in plastic variants exposed to outdoor conditions, contribute to recurring sales. Private-label expansion in mass retail further strengthens volume leadership within this segment.

Rolling tool boxes and mobile storage chests represent the fastest-growing product category, supported by increasing professional tool inventories and workshop modernization initiatives. Automotive repair centers, construction contractors, and industrial maintenance teams require high-capacity storage that enhances on-site mobility and ergonomic efficiency. Manufacturers such as Snap-on, Husky, and Milwaukee Tool have expanded modular rolling systems featuring ball-bearing drawer slides, anti-tip safety mechanisms, and integrated power strips for charging cordless tools. These units command higher average selling prices and often form part of bundled workshop packages. Standardization initiatives within franchise repair networks and fleet service operators are accelerating procurement of mobile systems, positioning this category to outpace overall market growth.

Materials Insights

Metal tool boxes are anticipated to hold approximately 42.3% of the market share in 2026, underscoring strong professional preference for structural durability and load-bearing capacity. Powder-coated steel cabinets and heavy-gauge chests remain standard fixtures in automotive workshops, aerospace maintenance facilities, and manufacturing plants. Their resistance to impact, corrosion, and forced entry enhances long-term value, particularly in high-usage environments. Companies such as Snap-on Incorporated and Lista (Stanley Black & Decker) specialize in heavy-duty steel storage engineered for high-weight thresholds and security compliance. Although raw material price fluctuations influence manufacturing costs, professional users prioritize longevity and safety certifications, sustaining metal’s leadership position within the materials segment.

Plastic and composite materials are expanding at the fastest pace due to advancements in high-impact polymers and fiber-reinforced designs. Lightweight construction reduces transportation costs and enhances portability, which is especially attractive for DIY consumers and mobile technicians. Manufacturers such as Tactix and Stanley have introduced modular stacking systems constructed from reinforced polypropylene, offering weather resistance and ergonomic handling. Hybrid configurations combining polymer shells with aluminum reinforcements deliver durability without significant weight increases. The rise of cordless tool ecosystems and compact job-site storage requirements further supports demand for lightweight solutions. Growth in e-commerce distribution channels, where shipping efficiency directly affects pricing competitiveness, reinforces the adoption of polymer-based tool storage systems.

Regional Insights

North America Tool Box Market Trends - Professional Contractor-Led Demand with Strong Brand and Retail Consolidation

North America is projected to account for approximately 36.7% of the market share in 2026, supported by a large installed base of professional users and a mature distribution ecosystem. The U.S. represents the dominant contributor, driven by sustained construction expenditure and a sizeable automotive aftermarket. According to the U.S. Census Bureau, construction spending has remained above US$1.9 trillion annually in recent years, sustaining demand for professional-grade storage systems across residential, commercial, and infrastructure projects. High contractor density and structured service networks create consistent procurement cycles for rolling chests, modular cabinets, and fleet-standardized storage systems.

Premium brands maintain a strong regional influence. Snap-on Incorporated, headquartered in Wisconsin, continues to expand its franchise-based mobile distribution model, enabling direct engagement with automotive technicians and reinforcing brand loyalty in the professional segment. Stanley Black & Decker, through brands such as DeWalt, Craftsman, and Stanley, has strengthened North American manufacturing investments, including facility expansions in the U.S. aimed at increasing domestic production capacity. These initiatives align with reshoring trends and supply chain risk mitigation strategies following pandemic-related disruptions. Retail consolidation also shapes the competitive environment.

Major home improvement chains such as Home Depot and Lowe’s allocate significant shelf space to private-label and branded portable storage solutions, supporting volume-driven categories while introducing modular systems targeting serious DIY users. Regulatory compliance requirements from organizations such as OSHA influence product design standards, particularly for load-bearing capacity and safety mechanisms in professional environments. Investment in warehouse automation and inventory digitization by large distributors improves fulfillment efficiency, raising entry barriers for smaller competitors lacking scale.

Europe Tool Box Market Trends - Quality- and Compliance-Focused Market Anchored by Industrial and Automotive Trades

Europe represents a mature yet structurally stable market anchored by advanced manufacturing, automotive engineering, and established trade professions. Germany leads regional demand, supported by its automotive supply chain and industrial machinery sectors. According to Germany Trade & Invest, the country remains Europe’s largest automotive production base, which sustains demand for heavy-duty metal storage cabinets used in assembly lines and service workshops. German manufacturers emphasize engineering precision and ergonomic design, reinforcing demand for high-load steel chests and modular workshop systems.

The U.K. and France demonstrate steady participation in DIY home improvement, supported by retail networks such as B&Q (Kingfisher Group) and Leroy Merlin. These retailers promote private-label and branded portable tool storage, sustaining mid-range consumer demand. Southern European markets, including Spain and Italy, show gradual growth among small and medium-sized contractors benefiting from EU-supported infrastructure modernization funds.

Regulatory harmonization under the European Union framework influences product specifications, particularly regarding chemical compliance under REACH regulations and environmental directives affecting coatings and materials. Sustainability initiatives increasingly shape procurement decisions, with manufacturers incorporating recyclable steel, powder-coated finishes with reduced volatile organic compounds, and modular designs that extend product life cycles. Companies such as Bott GmbH & Co. KG (Germany) and Facom (a Stanley Black & Decker brand) emphasize durable, long-service workshop systems tailored to industrial clients. These regulatory and environmental standards reinforce Europe’s focus on quality and compliance-driven differentiation rather than volume-led growth.

Asia Pacific Tool Box Market Trends - Infrastructure-Driven, Manufacturing-backed High-growth Trends

Asia Pacific represents the fastest-growing regional market, supported by infrastructure expansion, industrialization, and rising urbanization. China plays a dual role as both a major production hub and a significant consumption market. The country’s large-scale manufacturing ecosystem supports exports of metal and plastic tool storage products to North America and Europe. Companies such as GreatStar Industrial Co., Ltd. (owner of Workpro tools) leverage vertically integrated production facilities to supply global retailers, strengthening China’s export competitiveness. Domestic infrastructure investments and growth in automotive servicing also support internal demand for professional storage systems.

India demonstrates rising demand linked to infrastructure development and growth in organized automotive service networks. Government initiatives promoting manufacturing expansion, such as “Make in India,” encourage local assembly and distribution investments. International brands, including Bosch and Stanley Black & Decker have expanded distribution partnerships across India to serve both professional contractors and DIY consumers through modern retail and e-commerce platforms. Japan maintains a strong emphasis on precision engineering and industrial quality standards.

Companies such as TONE Co., Ltd. and other established Japanese tool manufacturers focus on high-grade metal storage systems tailored for automotive and industrial workshops. Across ASEAN countries, urbanization and small-contractor growth drive demand for portable and mid-capacity rolling systems. Expanding e-commerce platforms such as Alibaba and regional online marketplaces accelerate market penetration for consumer-grade storage products. Trade policy adjustments and localization strategies continue to influence manufacturing footprints, with companies investing in regional assembly facilities to mitigate tariff exposure and reduce logistics costs, positioning Asia Pacific as a strategic growth engine within the market.

Competitive Landscape

The global tool box market is moderately fragmented. Mass-market and portable tool box categories remain highly fragmented, characterized by numerous regional manufacturers, private-label brands, and contract OEM suppliers competing primarily on price and distribution reach. In contrast, the professional-grade rolling chest and heavy-duty metal cabinet segments demonstrate partial consolidation, where established brands with strong dealer networks, warranty programs, and premium positioning command a significant share of revenue.

Key strategic priorities include premiumization in professional segments, cost-efficient production for consumer plastics, omnichannel distribution expansion, and service-based differentiation through warranties and integrated tool management solutions.

Key Industry Developments

- In March 2025, Snap-on Incorporated launched an RFID-enabled modular tool storage system designed for automotive workshops, allowing real-time tracking and inventory management via a mobile app that automates asset audits and integrates with existing workshop IT infrastructure.

- In August 2025, Homak unveiled a corrosion-resistant aluminum bottom roll-away tool chest tailored for marine and humid work environments, complete with lockable drawers and soft-close mechanisms to appeal to specialized maintenance sectors.

Companies Covered in Tool Box Market

- Stanley Black & Decker

- Snap-on Incorporated

- Techtronic Industries (Milwaukee Tool)

- Apex Tool Group

- Matco Tools

- Husky

- Craftsman

- Beta Utensili

- Cornwell Quality Tools

- Facom

- TONE Co., Ltd.

- Kobalt Tools

- DeWalt (brand of Stanley Black & Decker)

- Makita

- Bosch Power Tools

- Proto Industrial (Stanley Black & Decker)

- Wright Tool

- US General

Frequently Asked Questions

The global tool box market size is valued at US$13.2 billion in 2026.

The tool box market is projected to reach US$21.3 billion by 2033.

Key trends include rising adoption of premium rolling workshop systems, growth in modular and stackable plastic storage solutions, integration of charging and tool management features, expansion of omnichannel distribution, and increasing localization of manufacturing to improve supply chain resilience.

Portable tool boxes lead the product category with an anticipated 45.9% share, while metal tool boxes dominate the materials segment with an anticipated 42.3% share due to strong professional demand.

The tool box market is expected to grow at a CAGR of 7.1% between 2026 and 2033.

Major companies include Stanley Black & Decker, Snap-on Incorporated, Techtronic Industries (Milwaukee Tool), Apex Tool Group, and Matco Tools.