- Home Care & Utilities

- Gardening Tools Market

Gardening Tools Market Size, Share, and Growth Forecast 2026 - 2033

Gardening Tools Market Size, Share, and Growth Forecast by Product Type (Shears and Pruning Tools, Digging Tools, Lawn Mowers, Blowers, Others), Operating Type (Manual Gardening Tools, Electric Gardening Tools), Sales Channel (Online Sales of Gardening Tools, Offline Sales of Gardening Tools), End-user (Commercial Gardening Tools, Non‑Commercial Gardening Tools), and Regional Analysis, 2026 ‑ 2033

Gardening Tools Market Size and Trend Analysis

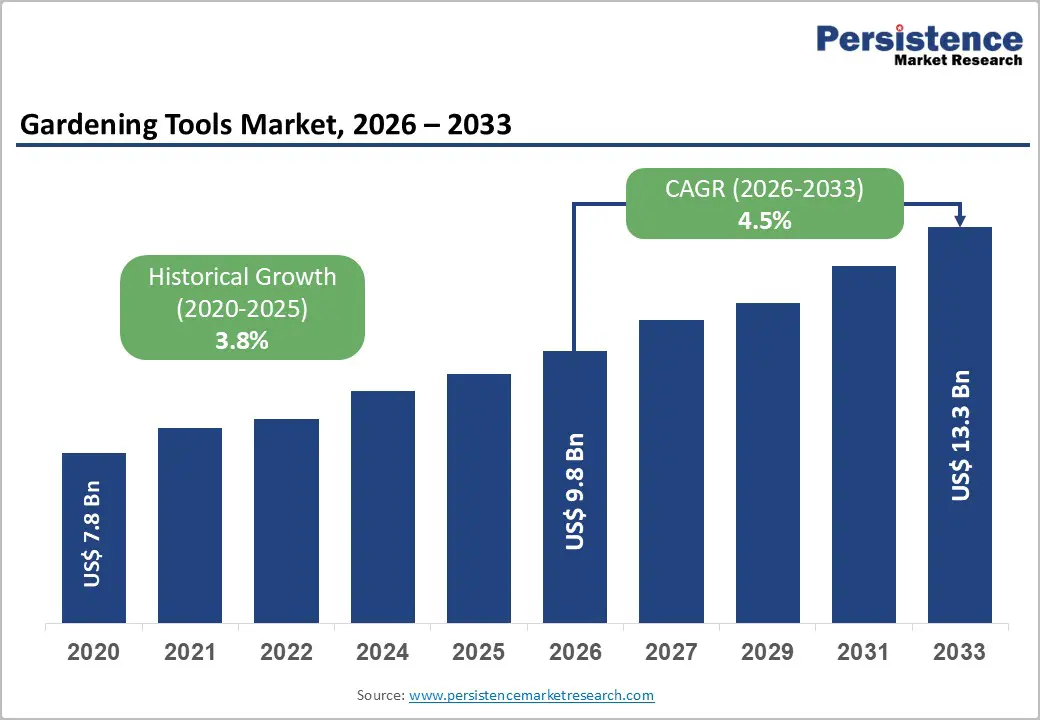

The global gardening tools market is projected to reach US$ 9.8 billion in 2026 and US$ 13.3 billion by 2033, growing at a CAGR of 4.5% over the forecast period. This expansion is underpinned by rising participation in home gardening, the expansion of urban green infrastructure projects, and a shift toward more ergonomic, multifunctional, and technologically advanced tools across residential and commercial landscapes.

Key Industry Highlights:

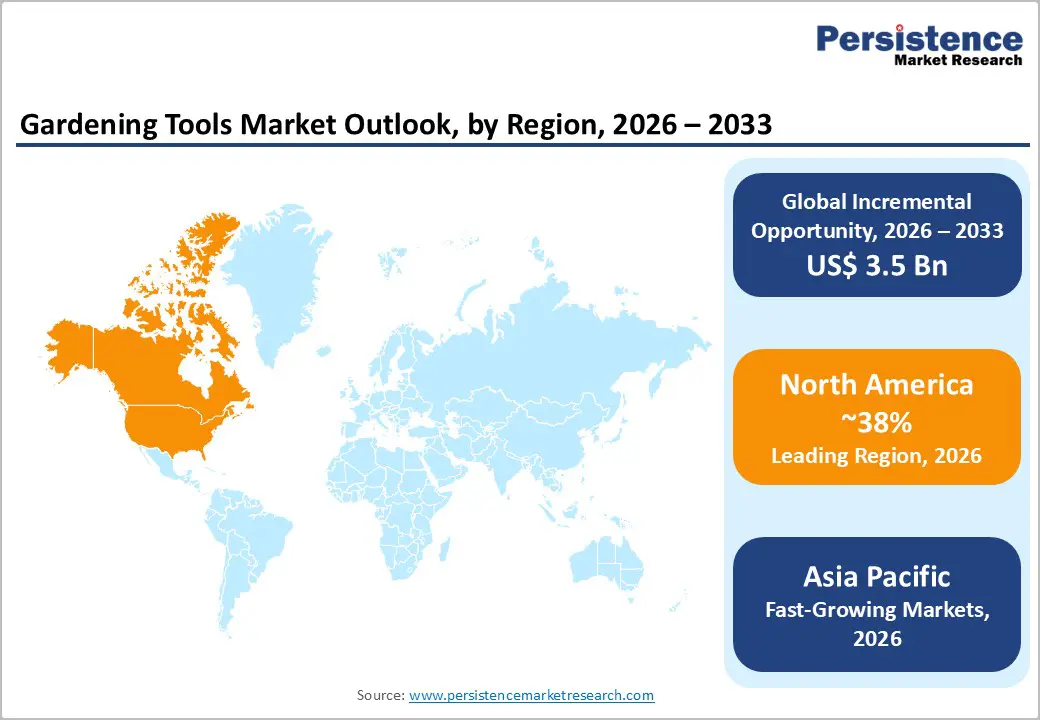

- Leading Region: North America dominates the Gardening Tools Market with a 38% share, driven by high homeownership, a strong DIY culture, and well-developed retail and e-commerce networks for manual gardening tools and electric lawn mowers.

- Fastest growing Region: Asia Pacific is the fastest-growing region with rising CAGR of 5.3%, driven by urbanization, rising middle-class incomes, and government-backed green-infrastructure projects that increase demand for commercial gardening tools and manual gardening tools.

- Dominant Operating Type: Manual Gardening Tools hold the largest share within the Operating Type category, accounting for roughly 60% of market value due to their affordability, simplicity, and broad applicability across residential and professional users.

- Fastest-growing Operating Type: Electric cordless lawn & garden tools are the fastest-growing segment, driven by environmental regulations, noise restrictions, and consumer preference for battery-powered lawn mowers, hedge trimmers, and blowers.

- Key Opportunity: The expansion of urban agriculture, vertical farming, and small-space gardening creates significant opportunities for manufacturers to introduce compact, lightweight, and multi-functional gardening tools tailored to apartment dwellers, schools, and community-garden initiatives.

| Key Insights | Details |

|---|---|

|

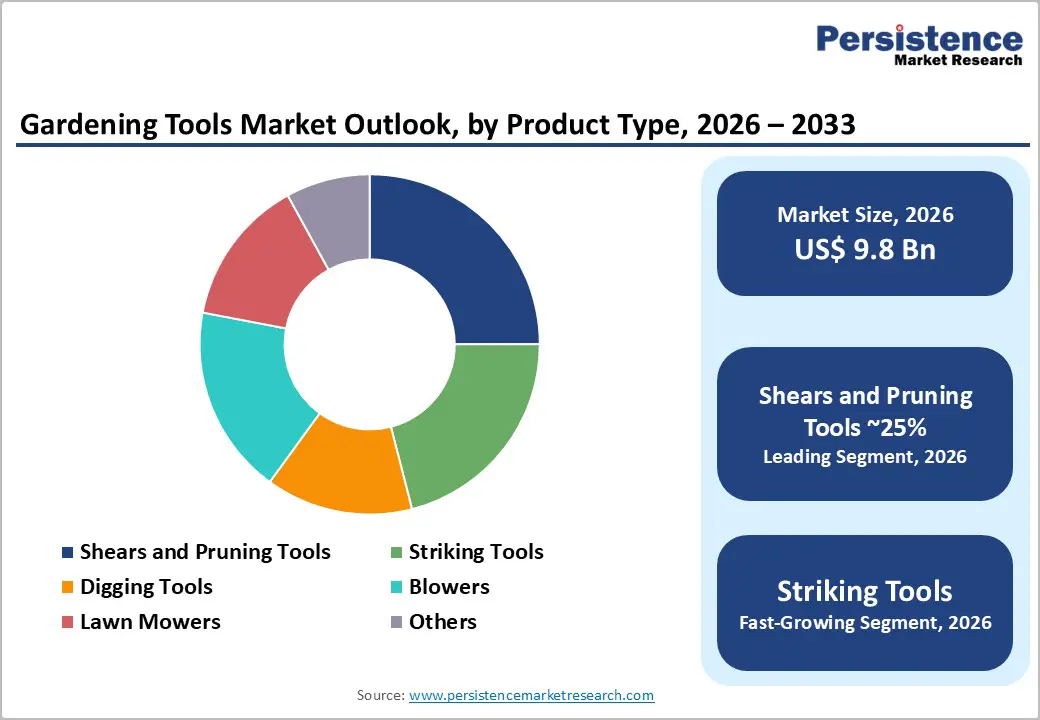

Gardening Tools Market Size (2026E) |

US$ 9.8 Bn |

|

Market Value Forecast (2033F) |

US$ 13.3 Bn |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

3.8% |

Market Dynamics

Drivers - Growing Popularity of Home Gardening and DIY Landscaping Boosts Consistent Residential Demand for Gardening Tools

Home gardening and DIY landscaping have become major growth drivers for the Gardening Tools Market, particularly in North America, Europe, and parts of Asia Pacific. In the United States, more than 65% of households own their homes, according to the U.S. Census Bureau, and many homeowners actively invest in lawn care, vegetable gardens, and decorative landscaping. This directly increases demand for tools such as lawn mowers, pruning shears, digging tools, and hedge trimmers.

Social media platforms and gardening influencers have further encouraged balcony gardening, small backyard setups, and vertical gardens, making gardening more accessible and popular. The Community Gardening Association reports that more than 18,000 active community gardens exist across the United States and Canada, all requiring regular use of durable hand and power tools. Similar trends are seen in Germany, the United Kingdom, and France, where gardening is a preferred leisure activity. This consistent participation drives frequent tool replacement, upgrades to better-quality products, and broader product adoption, supporting steady market growth.

Rising Urban Green Infrastructure Projects and Commercial Landscaping Services Accelerate Professional Tool Adoption Worldwide

Growing investment in urban green infrastructure is creating strong demand for professional gardening tools across residential, commercial, and municipal projects. Cities worldwide are expanding parks, roadside greenery, rooftop gardens, and public green spaces to improve air quality, reduce heat island effects, and enhance living standards. These projects require large volumes of tools such as lawn mowers, hedge trimmers, blowers, and electric pruning equipment. In India, government initiatives like the Smart Cities Mission have led to extensive landscaping contracts, boosting bulk purchases of gardening tools.

In North America and Europe, commercial landscaping companies are shifting toward electric and cordless equipment to reduce noise, emissions, and worker fatigue. Environmental regulations are limiting gasoline-powered tools, encouraging the adoption of battery-operated alternatives. This transition not only increases equipment upgrades but also supports higher-value tool segments. Combined with the rapid expansion of landscaping services, urban greening continues to strengthen long-term demand across the Gardening Tools Market.

Restraints - High Purchase Costs and Ongoing Maintenance Challenges Slow Widespread Adoption of Electric Gardening Equipment

The high upfront cost of electric gardening tools remains a major challenge for market growth, particularly in price-sensitive regions. Advanced cordless and battery-powered tools from leading brands such as Stanley Black & Decker, Fiskars Group, and Husqvarna Group are often significantly more expensive than traditional manual tools. While these products offer convenience and efficiency, many consumers hesitate to purchase them due to higher prices. Additionally, battery replacement, charging systems, and electronic repairs add long-term maintenance expenses.

For commercial users managing large tool fleets, the need for charging infrastructure, spare batteries, and specialized servicing increases operational costs. In regions with unstable electricity supply or limited service networks, electric tools become even less practical. As a result, many homeowners and small landscapers continue using manual tools, which are cheaper and easier to maintain. This slows the adoption of premium electrical products and limits growth in high-margin segments across developing markets.

Seasonal Weather Patterns Create Demand Fluctuations and Revenue Volatility across Global Gardening Tools Markets

The gardening tools market is strongly influenced by seasonal weather patterns, creating fluctuations in sales and operational planning. In regions such as North America and Europe, demand peaks during spring and early summer when homeowners and landscapers prepare gardens after winter. During the colder months, sales of lawn mowers, trimmers, and blowers decline sharply, often resulting in excess inventory and heavy discounting. In tropical regions, extreme heat and monsoon seasons also reduce outdoor gardening activity for extended periods.

Heavy rainfall in parts of India and Southeast Asia limits lawn maintenance and pruning, delaying tool purchases and replacements. These seasonal shifts make revenue forecasting difficult for manufacturers and retailers. Production scheduling, inventory storage, and cash flow management become more complex. For landscaping contractors, weather-related project delays further reduce tool usage. Overall, weather dependence remains a structural constraint that affects consistent market performance year-round.

Opportunities - Rapid Growth of Electric Cordless and Smart Gardening Tools Drives Premium Product Segment Expansion

Electric cordless and smart gardening tools represent the fastest-growing opportunity in the Gardening Tools Market. Consumers increasingly prefer battery-powered lawn mowers, hedge trimmers, blowers, and pruning tools because of their lower noise, reduced emissions, and easier operation. The global electric lawn and garden tools segment is projected to grow strongly through 2032, supported by improvements in battery life and charging speed.

Brands such as EGO Power+ and Greenworks have successfully introduced multi-tool battery platforms that enable a single battery to power multiple products. Major players such as Stanley Black & Decker, Husqvarna Group, and FELCO S.A. are also adding smart features, including performance tracking, maintenance alerts, and app connectivity. Urban regulations favoring low-emission equipment are further accelerating adoption among municipalities and commercial landscapers. As technology costs decline and performance improves, electric tools are expected to steadily replace gasoline-powered and manual tools, particularly in developed urban markets.

Urban Agriculture and Small-Space Gardening Trends Fuel Demand for Compact, Lightweight, Multi-Purpose Tools

The rapid rise of urban living is creating strong demand for compact and lightweight gardening tools designed for limited spaces. With more than half of the global population now living in cities, many households are turning to balconies, rooftops, and indoor gardens for food production and relaxation. This shift is boosting sales of small pruning shears, compact digging tools, mini lawn mowers, and ergonomic hand tools. Community gardens, school programs, and urban farming projects are also expanding across cities, necessitating standardized toolkits for volunteers and students.

In countries such as India, China, and Southeast Asia, government-supported green initiatives are promoting small-scale food cultivation in urban areas. Manufacturers are responding by launching rust-resistant, space-efficient, and multipurpose tools suited to modern urban lifestyles. Online retail channels further support this trend by making specialized products easily accessible. Urban agriculture continues to open new customer segments and long-term market growth opportunities.

Category-wise Analysis

Product Type Insights

Shears and pruning tools remain among the most widely used product categories in the gardening tools market, accounting for approximately 25% of total market volume. This segment includes pruning shears, loppers, handsaws, and hedge trimmers, all essential for plant maintenance, shaping, and harvesting. Unlike seasonal equipment, pruning is required year-round in most climates, ensuring steady replacement demand. Both home gardeners and professional landscapers rely heavily on these tools for daily tasks.

Leading brands such as Fiskars Group, FELCO S.A., and ANDREAS STIHL AG & Co. KG focus on ergonomic grips, sharp precision blades, and vibration-reduction features to improve comfort and performance. Professional users often prefer premium-quality tools that deliver cleaner cuts and greater durability, which supports higher price points. The combination of frequent usage, durability requirements, and premium upgrades continues to make this segment one of the strongest contributors to overall market revenue.

Operating Type Insights

Manual gardening tools continue to dominate the market, accounting for an estimated 60% of global revenue. This category includes hand tools such as pruners, shovels, spades, hoes, rakes, and handsaws that operate without electricity or fuel. Their popularity is driven by affordability, simplicity, and long service life, making them accessible to both casual gardeners and professional users. In emerging markets, limited access to power infrastructure further supports reliance on manual tools.

Even in developed regions, homeowners prefer manual tools for light gardening tasks because of their ease of use, portability, and low maintenance. Manufacturers continue improving these tools with ergonomic handles, corrosion-resistant coatings, and lightweight materials to enhance comfort and durability. This segment offers consistent demand and stable revenue streams while allowing brands to differentiate through design and material innovation. Despite rising adoption of electric tools, manual gardening tools remain essential across all regions and user groups.

Sales Channel Insights

Offline retail remains the leading sales channel for gardening tools, contributing around 65% of total market value. Home improvement stores, hardware outlets, garden specialty shops, and local dealers allow customers to inspect tools in person before purchase. Shoppers can assess weight, grip comfort, blade quality, and overall durability, which builds confidence in their purchase. In North America, large retail chains such as The Home Depot and Lowe’s play a major role in distributing products from major brands, including Stanley Black & Decker, Husqvarna Group, and Fiskars Group.

Seasonal promotions, in-store demonstrations, and bundled offers further drive high-volume sales during peak gardening months. For commercial buyers, specialized dealers provide technical support, spare parts, and repair services, making offline channels essential for professional tool purchases. While online sales are growing rapidly, especially for smaller tools, the hands-on experience and service advantages keep offline retail dominant across the market.

End-user Insights

Non-commercial users represent the largest end-use segment, accounting for approximately 60% of total market revenue. This group includes homeowners, apartment residents, hobby gardeners, and community garden participants who purchase tools for personal use. Rising homeownership rates, growing interest in DIY landscaping, and increased awareness of the health benefits of gardening continue to support strong residential demand. In the United States, over 65% of households own their homes, creating continuous demand for lawn mowers, pruning tools, shovels, and hedge trimmers.

In Europe, especially in countries like Germany and the United Kingdom, gardening is a popular leisure activity among older populations, driving demand for ergonomic and lightweight tools. Manufacturers are increasingly offering starter kits, colorful designs, and beginner-friendly tool sets to attract new users. The non-commercial segment provides stable recurring revenue and opportunities for long-term customer engagement and brand loyalty.

Regional Insights

North America Gardening Tools Market Trends

North America remains the largest regional market for gardening tools, supported by high homeownership, strong retail networks, and a deep-rooted gardening culture. In the United States, more than 65% of households own homes, with many maintaining lawns, flower beds, and landscaped yards. This drives continuous demand for lawn mowers, trimmers, blowers, and pruning tools. Residential users frequently replace or upgrade equipment, especially toward more ergonomic and cordless electric products. Regulatory policies that encourage lower noise and emissions are accelerating the shift away from gasoline-powered tools.

Environmental agencies promote electric alternatives, boosting adoption among both homeowners and landscaping professionals. Large home improvement retailers and growing e-commerce platforms further improve product accessibility across the region. Seasonal promotions and new product launches also support strong sales volumes. With rising environmental awareness and continued suburban development, North America is expected to maintain its leadership position while driving innovation in electric and smart gardening tools.

Europe Gardening Tools Market Trends

Europe represents a mature yet steadily evolving market driven by strong gardening traditions and sustainability-focused regulations. Countries such as Germany, the United Kingdom, France, and Spain show consistent demand for high-quality manual and electric gardening tools. Allotment gardens and backyard horticulture remain popular in Germany, supporting regular purchases of pruning shears, digging tools, and ergonomic equipment. In the United Kingdom, an aging population favors lightweight and easy-to-use tools that reduce physical strain.

European Union safety and environmental regulations on noise, vibration, and emissions have encouraged manufacturers to invest in quieter, energy-efficient electric systems. Companies such as Fiskars Group, Husqvarna Group, and STIHL continue to launch advanced ergonomic designs to meet regulatory standards. Meanwhile, urban greening projects across major cities are expanding public parks and rooftop gardens, creating additional commercial demand. Europe’s combination of cultural gardening habits and sustainability initiatives positions it as a key innovation center in the global market.

Asia Pacific Gardening Tools Market Trends

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, rising incomes, and large-scale green infrastructure programs. In China, as residential and commercial complexes expand, landscaped areas are increasingly common, driving demand for lawn mowers, blowers, and trimming tools used by property management firms. In India, government programs such as the Smart Cities Mission have significantly boosted public landscaping projects, increasing purchases of both manual and electric gardening equipment.

The region also benefits from strong manufacturing capabilities, making China, India, and Southeast Asia major production hubs for global markets. Local manufacturers focus on affordable yet durable designs using stainless steel and composite materials. The rapid expansion of e-commerce platforms has improved access to gardening tools for urban households, especially compact and hand-operated products. As interest in home gardening and urban green spaces continues to grow, the Asia Pacific is expected to contribute significantly to future market expansion.

Competitive Landscape

The gardening tools market is moderately fragmented, featuring a mix of global brands, regional manufacturers, and numerous small local producers. Major players such as Stanley Black & Decker, Inc., Husqvarna Group, Fiskars Group, FELCO S.A., and ANDREAS STIHL AG & Co. KG dominate developed markets in North America and Europe. Meanwhile, regional companies hold strong positions in the Asia Pacific, Latin America, and Africa by offering cost-effective products tailored to local needs. This fragmented structure encourages continuous innovation and brand differentiation.

Leading firms are investing heavily in electric cordless platforms, ergonomic designs, and smart tool technologies to strengthen customer loyalty. Sustainability initiatives, such as recyclable materials and energy-efficient equipment, are also becoming key competitive factors. New business models, including direct-to-consumer sales, rental services, and maintenance subscriptions, are emerging to increase customer engagement. Overall, competition remains strong, with innovation and distribution reach defining long-term market leadership.

Key Market Developments

- In April 2025: Stanley Black & Decker’s DEWALT brand expanded its outdoor power lineup with new battery-powered and cordless lawn mowers featuring advanced lithium-ion systems and higher performance for residential and light commercial use, reinforcing its focus on electrification and smart garden equipment growth.

- In March 2024, Husqvarna Group has been advancing connected lawn care and smart gardening experiences, including enhancing robotic mower connectivity and integrating garden products with home automation platforms to offer voice-enabled and app-based smart lawn care features.

Companies Covered in Gardening Tools Market

- Stanley Black & Decker, Inc.

- The Ames Companies, Inc.

- CobraHead LLC

- Estwing Manufacturing Company

- Seymour Midwest LLC

- Bully Tools, Inc.

- Zenport Industries

- Ray Padula Holdings, LLC

- Root Assassin Shovel LLC

- Lee Valley Tools Ltd.

- Garden Tool Company

- Fiskars Group

- Husqvarna Group

- FELCO S.A.

- ANDREAS STIHL AG & Co. KG

Frequently Asked Questions

The Gardening Tools Market is projected to grow from US$ 9.8 Billion in 2026 to US$ 13.3 Billion by 2033, registering a CAGR of 4.5%, supported by rising home gardening, urban green‑infrastructure projects, and the adoption of electric cordless tools.

Key demand drivers include rising home gardening and DIY landscaping, urban green‑infrastructure investments, and regulatory shifts toward electric and low‑emission tools, which are increasing purchases of lawn mowers, hedgers, pruning shears, and manual gardening tools.

Manual Gardening Tools is the leading segment within the Operating Type category, accounting for roughly 60% of market value due to their affordability, simplicity, and broad use by homeowners, small‑scale farmers, and budget‑conscious landscapers.

North America leads the Gardening Tools Market, supported by high homeownership, a strong culture of lawn and garden maintenance, and well‑developed retail and e‑commerce channels for manual gardening tools and electric lawn mowers.

A key opportunity lies in urban agriculture, vertical farming, and small‑space gardening, which are driving demand for compact, lightweight, and multi‑functional gardening tools tailored to apartment dwellers, schools, and community‑garden initiatives.

Major players include Stanley Black & Decker, Inc., Husqvarna Group, Fiskars Group, FELCO S.A., ANDREAS STIHL AG & Co. KG, The Ames Companies, Inc., CobraHead LLC, Estwing Manufacturing Company, Seymour Midwest LLC, Bully Tools, Inc., Zenport Industries, Ray Padula Holdings, LLC, Root Assassin Shovel LLC, Lee Valley Tools Ltd., and Garden Tool Company.