- Specialty & Fine Chemicals

- Textile Colors Market

Textile Colors Market Size, Share, and Growth Forecast, 2026 - 2033

Textile Colors Market by Colorant Type (Reactive Dyes, Direct Dyes, Acid Dyes, Basic (Cationic) Dyes, Disperse Dyes, Organic Pigments, Inorganic Pigments, Digital Textile Inks, Others), Process (Batch Dyeing, Continuous Dyeing, Fiber Dyeing, Digital Printing, Finishing/Special Effects), Technology (Digital Textile Printing, Water-Less/Low-Water Solutions, Closed-Loop/Wastewater Recovery & Chemical Recycling, Others), and Regional Analysis for 2026 - 2033

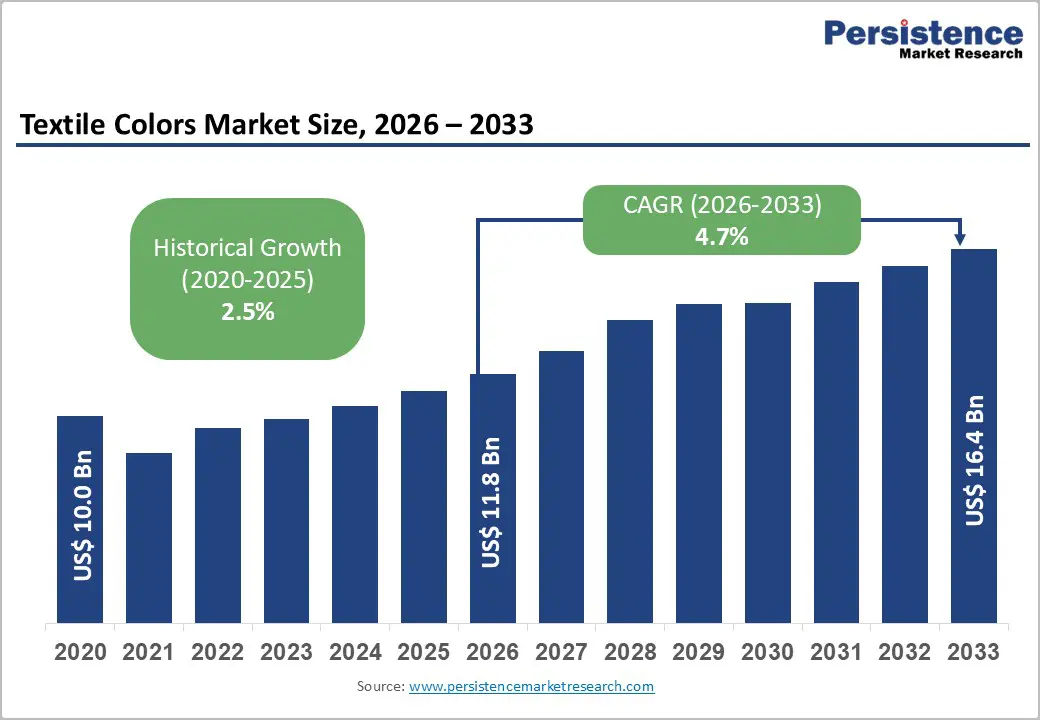

Textile Colors Market Share and Trends Analysis (2020: US$ 10.0 billion, CAGR H: 2.5%)

The global textile colors market size is likely to be valued at US$ 11.8 billion in 2026, and is projected to reach US$ 16.4 billion by 2033, growing at a CAGR of 4.8% during the forecast period 2026 - 2033.

Structural shifts in textile manufacturing, regulatory tightening on chemical use, and the accelerating adoption of digital and low-impact coloration technologies are the primary growth drivers for this market. Demand is increasingly linked to process efficiency, compliance readiness, and color performance requirements across fibers and end-use applications. Growth is primarily supported by rising textile production in the Asia Pacific, sustained substitution of conventional dyes with reactive and pigment-based systems, and the scaling of digital textile printing in fast fashion, home textiles, and customized apparel.

According to data from the International Textile Manufacturers Federation (ITMF) and UN Industrial Development Organization (UNIDO), global textile output is recovering steadily post-pandemic, while regulatory initiatives such as the Zero Discharge of Hazardous Chemicals (ZDHC) wastewater guidelines, and national chemical safety frameworks in China and India are actively reshaping supplier portfolios. The market is shifting toward higher-margin specialty colorants, including low-salt reactive dyes, binder-optimized pigment systems, and digital inks compatible with on-demand manufacturing. While cost pressures from energy, intermediates, and compliance investments remain elevated, suppliers with integrated R&D, application support, and regulatory alignment are achieving pricing resilience.

Key Industry Highlights

- Dominant Colorant: Reactive dyes are expected to command approximately 34% of market revenue in 2026, reflecting their continued dominance in cotton and cellulosic textile processing.

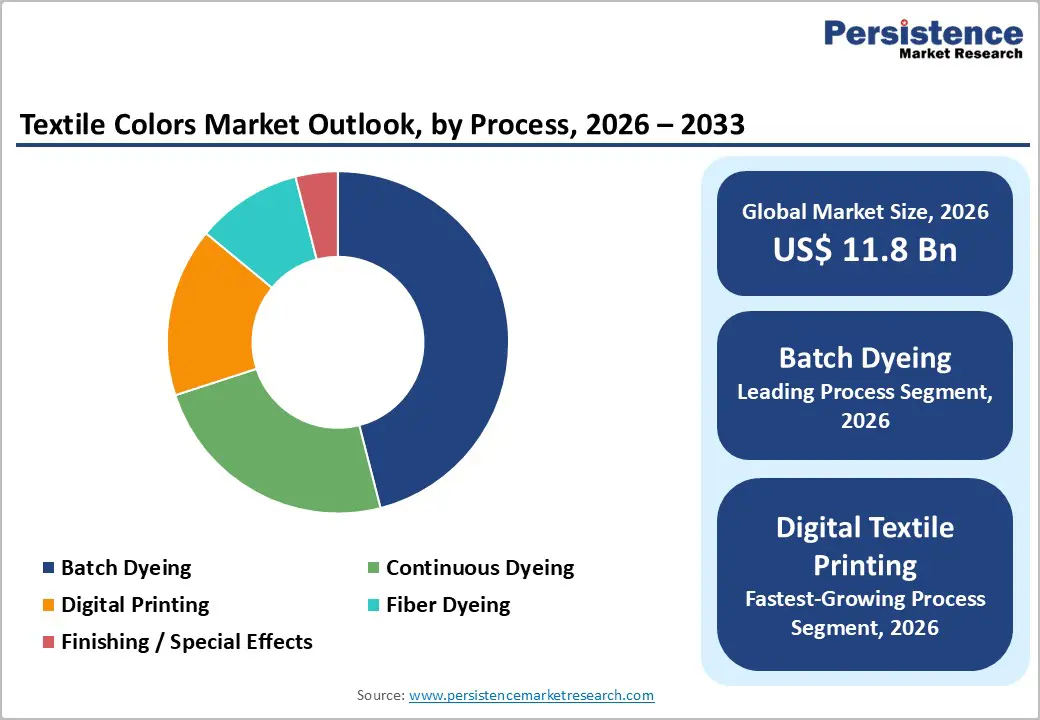

- Leading Process: Batch dyeing is anticipated to account for nearly 46% of market revenue in 2026, owing to its flexibility across fiber types and production scales.

- Fastest-growing Process: Digital textile printing is projected to grow at the fastest pace through 2033, driven by the increasing demand for shorter lead times and improved water efficiency.

- Technology Dynamics: Conventional wet dyeing technologies are expected to account for about 71% of the market in 2026, supported by their extensive installed base, while low-water and waterless dyeing are forecast to achieve the strongest 2026-2033 CAGR, as regulatory pressure on effluent discharge intensifies.

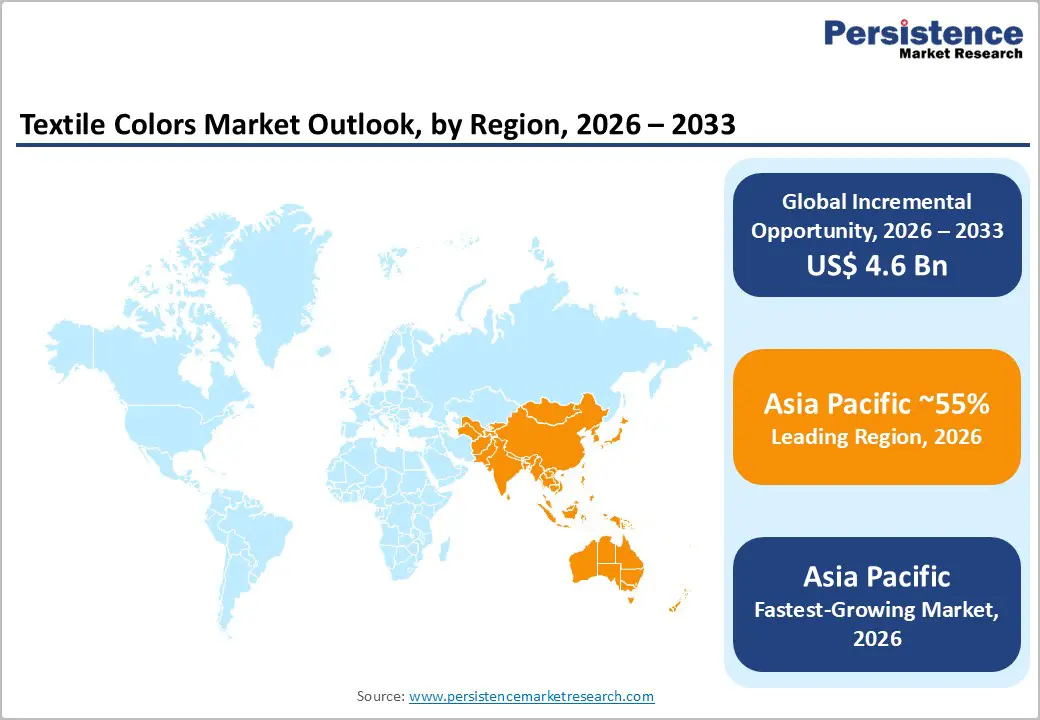

- Regional Leadership: Asia-Pacific is projected to lead the global market, with an estimated 55% revenue share in 2026 and a 5.4% CAGR through 2033, underpinned by large-scale textile manufacturing capacity and export-driven demand.

- Competitive Environment: Market competition is increasingly shaped by regulatory compliance and technology-driven differentiation, with leading firms prioritizing low-impact dye chemistries, digital ink systems, and integrated application support.

- July 2025: Sparxell, a Cambridge-based color platform technology company, partnered with Positive Materials to launch its first textile ink derived from dye-free pigments, exploring surface printing as an alternative to conventional dyeing.

| Key Insights | Details |

|---|---|

| Textile Colors Market Size (2026E) | US$ 11.8 Bn |

| Market Value Forecast (2033F) | US$ 16.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Concerted Shift toward Compliant and Low-Impact Coloration Systems

Regulatory enforcement across major textile manufacturing hubs is increasingly shaping demand for advanced textile color systems that reduce water consumption, limit chemical discharge, and minimize hazardous residues. Authorities and regulators are tightening effluent and chemical-use standards, particularly for azo compounds, heavy metals, salt load, and chemical oxygen demand (COD). These regulatory actions are progressively influencing purchasing decisions at the mill level, as compliance is becoming essential for continued operations and export access.

Textile producers are therefore prioritizing color solutions that comply with wastewater discharge thresholds and chemical management standards, as non-compliance increasingly results in operational restrictions, higher remediation costs, and reduced buyer confidence. Enforcement intensity continues to rise across Asia-Pacific, Europe, and parts of Latin America, thereby structurally embedding regulatory considerations into sourcing and production planning rather than treating them as episodic compliance exercises.

Textile manufacturers are responding by accelerating the adoption of low-salt reactive dyes, high-fixation disperse dyes, and pigment-based coloration systems that are reducing rinsing requirements and overall water intensity. Guidance from the ZDHC Foundation indicates that compliant dyehouses are achieving water savings of approximately 15-25% per kilogram of fabric, which directly lowers operational risk and strengthens eligibility for export-oriented supply chains.

As a result, mills are increasingly favoring suppliers that are offering reformulated products, on-site application support, and verifiable certification under frameworks such as OEKO-TEX®, bluesign®, and ZDHC. Regulatory alignment is functioning as a long-term value reallocation mechanism, as suppliers that are embedding compliance into product design and service models will have strengthened pricing power and deeper customer retention by the end of the decade.

Structural Cost Escalation and Margin Compression in Conventional Dye Manufacturing

The growth of the textile colors market is constrained by a sustained structural restraint, as input-cost volatility and margin compression increasingly affect commodity dye categories. Key inputs such as aromatic intermediates, dispersing agents, and specialty solvents remain exposed to fluctuations in crude oil prices, rising energy tariffs, and region-specific supply disruptions. Industry data indicate that energy expenses account for approximately 20% of total dye manufacturing costs across major producing regions.

As a result, manufacturers operating under legacy cost structures experience limited pricing flexibility, while buyers exert downward pressure on contract pricing. This cost environment continues to erode the economic viability of low-margin dye portfolios, particularly where scaling or backward integration is absent. Compliance-driven capital expenditure is further increasing fixed-cost intensity across the supply base.

Investments in effluent treatment plant upgrades, wastewater recycling infrastructure, and recurring compliance audits are raising operating thresholds for small and mid-scale dye manufacturers, especially in India, Pakistan, and Bangladesh. Industry bodies such as the China Dyestuff Industry Association report that sub-scale producers have experienced erosion of Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margins of roughly 200 to 350 basis points since 2021, attributable to combined regulatory and cost pressures.

This environment is accelerating consolidation, while also creating short-term supply instability through supplier exits and inconsistent delivery performance. For investors and strategists, the core risk lies in structural inefficiencies in traditional production models, which limit scalability unless manufacturers adopt process automation, advanced formulations, or vertical integration strategies over the forecast period.

Scaled Adoption of Digital Textile Printing and Pigment-based Coloration in Asia

A high-value opportunity is emerging at the convergence of digital textile printing, pigment-based ink systems, and Asia-centric apparel manufacturing. Digital printing is increasingly addressing structural inefficiencies associated with conventional dyeing, such as extended lead times, rigid minimum order quantities, and elevated inventory exposure. Trade and production data indicate that more than 65% of global apparel exports originate from the Asia-Pacific region, creating a large and scalable demand base for digitally enabled color solutions.

As apparel brands are continuing to prioritize speed to market, design flexibility, and lower working capital intensity, digital coloration is becoming a strategic production enabler rather than a niche printing alternative. This shift is particularly relevant for export-oriented manufacturers serving the fast-fashion, home textiles, and customized apparel sectors. Pigment-based digital inks are gaining adoption because they are fiber-agnostic, eliminating washing and steaming stages, and substantially reducing water consumption. Assessments from the European Commission Joint Research Centre (JRC) show water savings of up to 80-90% per meter of fabric when compared with conventional wet dyeing processes.

This opportunity is strengthening in India, Vietnam, and Indonesia, where governments are supporting textile modernization through production-linked incentive (PLI) programs, export incentives, and technology upgradation funds. Suppliers offering integrated solutions that cover ink formulation, printer compatibility, and color management software are likely to capture disproportionate value, while investors benefit from technology-driven growth, premium pricing potential, and structurally defensible differentiation relative to conventional dye categories.

Category-wise Analysis

Colorant Type Insights

Reactive dyes are expected to account for approximately 34% of the textile colors market revenue share in 2026. Their dominance stems from their strong chemical affinity for cotton and other cellulosic fibers, which account for the largest share of global textile fiber consumption. Reactive dye systems deliver high wash fastness, improved fixation efficiency, and consistent shade reproducibility, which aligns well with large-scale dyeing operations. Textile mills across the Asia Pacific, particularly in India and China, are increasingly adopting low-salt and bifunctional reactive dye formulations to comply with tightening wastewater discharge requirements.

This transition is strengthening long-term demand stability, as mills are prioritizing dye chemistries that reduce salt load and improve overall process efficiency while maintaining color performance standards required by export-oriented buyers. Digital textile inks are emerging as the fastest-growing colorant segment and are projected to register an estimated CAGR of around 8.1% between 2026 and 2033. Growth is being supported by the accelerating shift toward on-demand manufacturing and shorter fashion cycles across the apparel and home textile segments.

Pigment-based and reactive digital inks are benefiting from rising investments in digital printing equipment and steadily declining per-meter printing costs, which are improving commercial viability at scale. Adoption remains strongest in fast fashion, home textiles, and customized apparel applications, where brands prioritize inventory risk reduction, design flexibility, and shorter replenishment cycles. As digital infrastructure continues to expand, digital inks are increasingly positioning themselves as a strategic growth engine rather than a complementary coloration solution.

Process Insights

Batch dyeing is projected to account for approximately 46% of the textile color market share in terms of revenue in 2026. Its dominance is supported by high operational flexibility across multiple fiber types and strong suitability for varied production lot sizes, which are common in fragmented textile manufacturing ecosystems. Batch dyeing systems remain widely deployed across small and mid-scale mills, particularly in the Asia Pacific, where production diversity and frequent shade changes are prevalent. Despite ongoing environmental scrutiny, manufacturers are increasingly adopting process optimization measures, such as automated dosing, improved temperature control, and real-time monitoring, to enhance resource efficiency and sustain the relevance of batch dyeing within evolving compliance frameworks.

Digital printing is likely to be the fastest-growing processing segment, projected to expand at a CAGR of approximately 7.9% between 2026 and 2033. The growing need to reduce water consumption, lower energy usage, and shorten production turnaround times across textile value chains are factors benefiting this segment. Digital printing is offering superior scalability for short production runs, which aligns closely with the requirements of export-oriented apparel manufacturers serving fast fashion and customized product lines. As mills continue investing in digital infrastructure to improve responsiveness and reduce operational risk, digital printing is increasingly positioning itself as a complementary and, in select applications, a substitutive process to conventional dyeing methods.

Technology Insights

At approximately 71%, conventional wet dyeing technologies are projected to dominate the textile color market in 2026. Their continued prevalence is being supported by a large installed equipment base and relatively lower upfront capital requirements when compared with emerging alternatives. Traditional systems are remaining deeply embedded across global textile manufacturing operations, particularly in cost-sensitive regions where production scale and equipment utilization are critical. At the same time, manufacturers are increasingly implementing incremental upgrades such as improved liquor ratio control, automated chemical dosing, and enhanced effluent management to maintain regulatory compliance and extend the operational life of existing assets.

Waterless and low-water dyeing technologies are predicted to grow at the highest CAGR during the 2026-2033 forecast period. Technologies such as supercritical carbon dioxide dyeing and foam-based dyeing systems are gaining pilot-scale and early commercial adoption due to their ability to significantly reduce water consumption and effluent generation. Adoption remains most pronounced in Europe and Japan, where sustainability mandates, higher environmental compliance costs, and long-term operating savings strengthen the business case for these technologies. As regulatory pressure continues to intensify, low-water dyeing solutions are increasingly transitioning from experimental applications to strategically targeted investments within advanced textile manufacturing facilities.

Regional Insights

North America

North America is expected to account for approximately 12% of the global textile color market in 2026. The regional market is projected to expand at a modest rate through 2033, driven by the increasing adoption of digital textile printing, the gradual reshoring of niche and high-value textile production, and sustainability-led procurement strategies adopted by apparel and home textile brands. As brands are prioritizing shorter supply chains and greater production transparency, demand for advanced and compliant color solutions is steadily increasing across the region.

Regulatory compliance requirements and relatively high labor costs are continuing to favor automation and the use of high-value specialty colorants in North American textile operations. Manufacturers are increasingly investing in digitally enabled coloration systems and precision-controlled processes to improve productivity and reduce dependence on labor-intensive methods. This environment is supporting demand for pigment-based digital inks, specialty dyes with enhanced performance attributes, and integrated color management solutions.

Over the forecast period, the North American market is likely to remain focused on value-added applications rather than volume growth, reinforcing a steady but moderate expansion trajectory.

Europe

Europe is projected to account for approximately 21% of the global market for textile colors in 2026, with an estimated CAGR of nearly 4% through 2033. Market development is being shaped by a strong emphasis on regulatory compliance, circular textile initiatives, and water-efficient coloration practices. European textile producers and brands are increasingly aligning sourcing decisions with environmental and chemical safety standards, which is strengthening demand for compliant and traceable color solutions across the value chain.

Strict enforcement of the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) framework is continuing to influence product selection and supplier qualification in the region. Certified dyes and pigments that meet established environmental and human safety criteria are increasingly preferred, particularly among manufacturers of premium apparel, home textiles, and technical textiles. This regulatory environment is encouraging innovation in low-impact dye chemistries and recycled-content pigment systems, while also raising entry barriers for non-compliant suppliers.

As a result, the European textile colors market is remaining structurally stable, with growth being driven by value-added applications and sustainability-led differentiation rather than volume expansion.

Asia Pacific

Asia-Pacific dominates the textile color market, accounting for an estimated 55% of global revenue in 2026. Moreover, the market is projected to exhibit the highest CAGR of approximately 5.4% from 2026 to 2033. The region is continuing to function as the primary growth engine for the market, supported by large-scale textile capacity expansion and sustained export demand from global apparel and home textile brands. Manufacturing activity is remaining concentrated across major production hubs, bolstered by cost competitiveness, integrated supply chains, and access to skilled labor.

With global clothing brands becoming increasingly dependent on the Asia Pacific for raw materials, the demand for textile color solutions is likely to skyrocket in line with production volumes and process upgrades. Government-led modernization programs are further strengthening regional growth prospects. Countries such as India, China, and Vietnam are actively supporting upgrades in the textile sector through policy instruments including export incentives, technology upgradation funds, and production-linked investment schemes.

These initiatives are encouraging mills to adopt higher-efficiency dyeing processes, compliant color chemistries, and digitally enabled production systems. At the same time, regulatory enforcement on wastewater discharge and chemical management is intensifying across the region, thereby accelerating the transition toward low-impact dyes and advanced coloration technologies. Throughout the 2026-2033 forecast period, Asia-Pacific is well positioned to remain the focal point for capacity investments and technology adoption, positioning the region as the central driver of both volume growth and incremental value creation in the textile colors market.

Competitive Landscape

The global textile colors market structure portrays a picture of moderate fragmentation, with the top ten players collectively holding nearly half of the total revenue. Competitive intensity is continuing to increase as leading manufacturers are prioritizing research and development investment, application-level technical support, and regulatory alignment rather than relying solely on production scale. Large multinational suppliers are increasingly positioning themselves as solution partners by offering compliant formulations, process optimization support, and documentation aligned with international chemical management standards.

This approach is strengthening long-term customer relationships and enabling greater pricing discipline in an otherwise cost-sensitive market environment. Regional and local producers are continuing to compete effectively in commodity dye segments, particularly in price-driven domestic markets. However, these players are becoming increasingly exposed to compliance-related cost escalation as environmental enforcement and chemical safety requirements tighten across key manufacturing regions.

Rising expenditure on effluent treatment, certification, and audit readiness is placing pressure on margins and limiting reinvestment capacity for smaller firms. As a result, competitive differentiation is progressively shifting away from price-led competition toward regulatory readiness and technical capability, which is likely to accelerate consolidation and reshape competitive positioning over the forecast period.

Key Industry Developments

- In January 2026, Konica Minolta launched O’ROBE, an inline pretreatment ink for reactive dye textile printing that integrates pretreatment directly into the printing process for its Nassenger series of inkjet textile printers. The new product is designed to improve operational efficiency, cut environmental impact, and enhance profitability for dyeing and finishing companies by eliminating separate fabric coating and drying steps in conventional pretreatment workflows.

- In November 2025, True Colors Limited entered a distribution agreement with Spain’s Innovaciones Técnicas Aplicadas a Cerámicas Avanzadas (ITACA) to supply ITACA’s digital textile printing consumables across India. The partnership will see True Colors import and stock products in Surat, strengthen its machine-paper-ink ecosystem, and support after-sales technical service, targeting India’s rapidly expanding digital textile printing market.

- In September 2025, MS Printing Solutions and JK Group introduced a new MP Series of five multi-pass digital textile printers featuring advanced design, durability, and simplified maintenance. The series includes models from MP3000 to MP5000, featuring enhanced capabilities such as high-speed printing up to 630 m²/hour, up to 16 print heads, and integrated automatic color management, targeting a range of applications, from sublimation paper to direct-to-fabric printing.

Companies Covered in Textile Colors Market

- Archroma Management GmbH

- LANXESS AG

- Huntsman Corporation

- DyStar Group

- BASF SE

- Kiri Industries Ltd.

- Zhejiang Longsheng Group Co., Ltd.

- Sudarshan Chemical Industries Ltd.

- Clariant AG

- Atul Ltd.

- Colourtex Industries Pvt. Ltd.

- Toyo Ink SC Holdings Co., Ltd.

- Kronos Worldwide, Inc.

Frequently Asked Questions

The global textile colors market is projected to reach US$ 11.8 billion in 2026.

Massive textile production in Asia Pacific, sustained substitution of conventional dyes with reactive and pigment-based systems, and the scaling of digital textile printing in fast fashion, home textiles, and customized apparel are driving the market.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Regulatory tightening on chemical usage in the textile industry and accelerating adoption of digital and low-impact coloration technologies are creating lucrative market opportunities.

Archroma Management GmbH, LANXESS AG, Huntsman Corporation, DyStar Group, and BASF SE are some of the key players in the market.