- Advanced Materials

- Geotextiles Market

Geotextiles Market Size, Share, and Growth Forecast 2026 - 2033

Geotextiles Market by Material Type (Natural - Jute, Coir; Synthetic - Polypropylene, Polyester, Polyethylene, Others), Product Type (Non-woven - Light Weight, Medium Weight, Heavy Weight, Paving Fabrics; Woven - Slit Tape Woven, High Strength Woven; Knitted), Application (Erosion Control, Reinforcement, Drainage System, Lining System, Asphalt Overlays, Separation & Stabilization, Silt Fences), Industry, and Regional Analysis, 2026 - 2033

Geotextiles Market Size and Trend Analysis

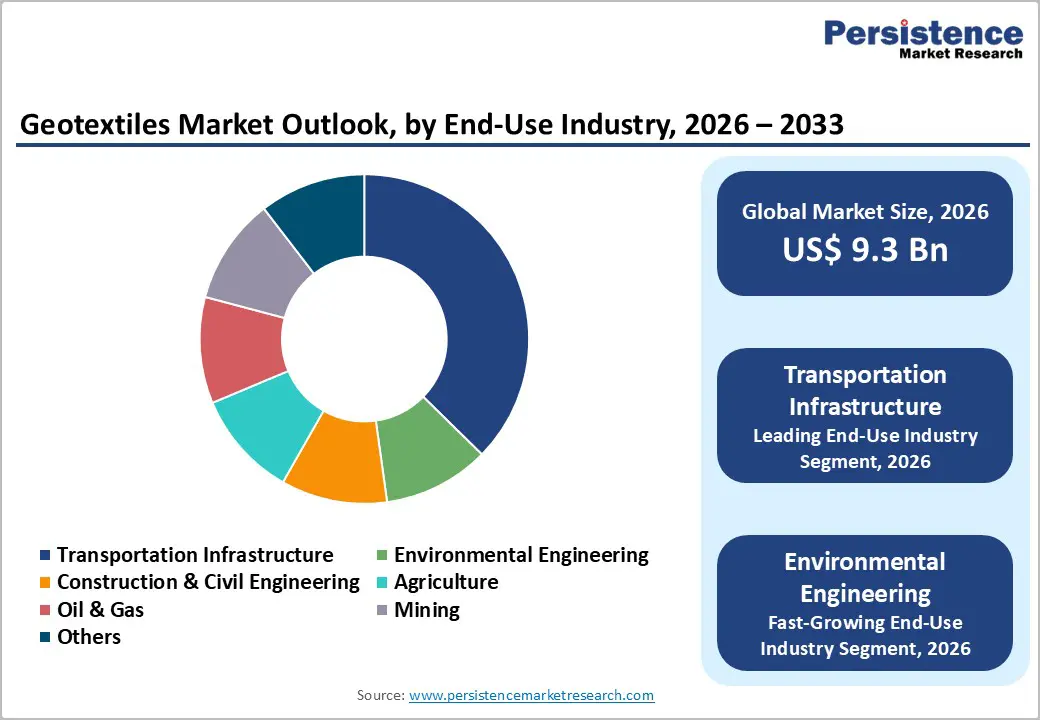

The global geotextiles market size is expected to be valued at US$ 9.3 billion in 2026 and is projected to reach US$ 14.5 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

The market’s robust expansion is primarily anchored in accelerating global infrastructure investment, tightening environmental compliance mandates, and growing recognition of geotextiles as indispensable engineered solutions in civil construction and environmental management. Governments across North America, Europe, and the Asia Pacific are channeling record levels of public spending into transportation networks, flood control systems, and waste containment facilities, all major application domains for geotextile products. Simultaneously, rising soil erosion concerns and the widespread adoption of geosynthetics in sustainable construction are creating sustained, multi-year demand cycles for both woven and non-woven geotextile solutions across developed and emerging economies.

Key Industry Highlights:

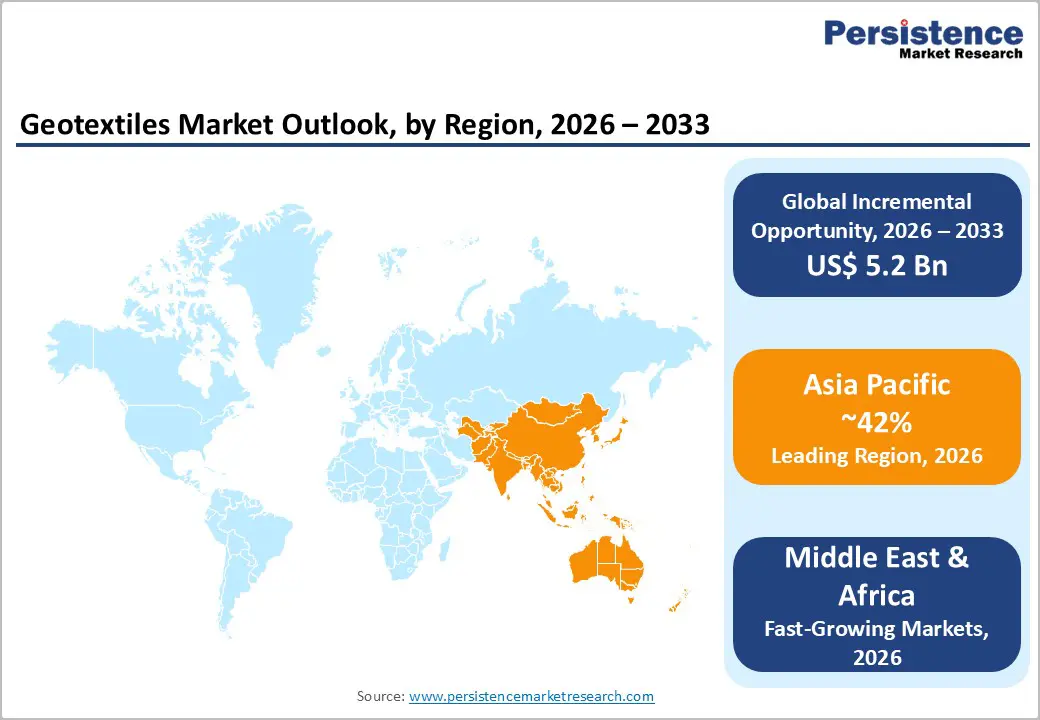

- Leading Region: Asia Pacific leads the global Geotextiles market, holding approximately 42% of global market share in 2025, driven by China’s infrastructure-led economic policy, India’s Bharatmala Pariyojana highway program, and rapid ASEAN urbanization, generating broad-based geotextile demand across transportation and environmental engineering applications.

- Fastest Growing Region: Middle East & Africa is the fastest-growing regional market for geotextiles during 2026 - 2033, fueled by large-scale urban infrastructure programs under Saudi Vision 2030, growing road network investment in Sub-Saharan Africa, and increasing geotextile adoption in arid-zone irrigation and desertification control projects.

- Dominant Segment: Polypropylene-based synthetic geotextiles dominate the Material Type segment with approximately 65% market share in 2025, underpinned by cost efficiency, chemical resistance, and versatile manufacturability into both woven and non-woven product forms for transportation and drainage infrastructure applications.

- Fastest Growing Segment: Non-woven geotextiles represent the leading and broadly adopted product type with approximately 55% share in 2025, reflecting their multi-functional applicability across filtration, drainage, and separation requirements in transportation infrastructure, the largest end-use industry worldwide.

- Key Opportunity: A key market opportunity lies in the development of biodegradable and sustainable geotextile products, particularly jute and coir-based solutions, positioned to capitalize on growing green procurement mandates, EU Green Deal funding streams, and climate adaptation investment that are expected to drive premium demand through 2033.

| Key Insights | Details |

|---|---|

| Geotextiles Market Size (2026E) | US$ 9.3 Billion |

| Market Value Forecast (2033F) | US$ 14.5 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.5% |

| Historical Market Growth (2020 - 2025) | 5.9% |

DRO Analysis

Drivers - Rising Global Infrastructure Investment Driving Sustained Geotextile Procurement

Large-scale public infrastructure programs across major economies are establishing a powerful and enduring demand foundation for the geotextiles market. In the United States, the Infrastructure Investment and Jobs Act (IIJA) of 2021 committed US$ 1.2 trillion over a decade toward road rehabilitation, bridge repair, and water systems, all critical application areas for geotextile-based separation, filtration, and drainage solutions. Across the European Union, the Trans-European Transport Network (TEN-T) program has earmarked over €330 billion for multimodal transport corridor development through 2030. In India, the National Infrastructure Pipeline (NIP) with a projected outlay of approximately US$ 1.4 trillion is accelerating highway and railway construction under programs such as Bharatmala Pariyojana, generating massive, structured demand for geosynthetic reinforcement and subgrade stabilization materials. These multi-year government-backed programs are translating directly into consistent procurement of geotextile products, reducing demand volatility and encouraging long-term capacity investments by manufacturers.

Stringent Environmental Regulations Mandating Erosion and Sediment Control

Regulatory enforcement of erosion control and sediment management standards is creating non-discretionary demand for geotextile products globally. In the United States, the Environmental Protection Agency (EPA) mandates the deployment of best management practices (BMPs), including silt fences, erosion control blankets, and turf reinforcement mats made from geotextile materials, on all construction sites disturbing one acre or more of land under the National Pollutant Discharge Elimination System (NPDES) permit program. The European Union’s Water Framework Directive similarly enforces strict controls on sediment discharge into surface water bodies. According to the Food and Agriculture Organization (FAO), approximately 24 billion tonnes of fertile soil are lost worldwide each year due to erosion, compelling governments and civil engineering agencies to mandate geotextile-based protection systems for public works. This regulatory backdrop is institutionalizing the use of geotextiles across construction, infrastructure, and environmental remediation applications, providing a structurally supportive demand environment for the forecast period.

Restraints- Raw Material Price Volatility Compressing Manufacturer Margins

A significant proportion of geotextiles is manufactured from petroleum-derived synthetic polymers, particularly polypropylene and polyester, making the industry highly vulnerable to fluctuations in crude oil and petrochemical prices. Between 2021 and 2023, global polypropylene spot prices increased by over 30% at peak levels before retracing, disrupting cost structures and supply chain planning for manufacturers. According to the U.S. Energy Information Administration (EIA), crude oil price volatility has remained structurally elevated, driven by geopolitical instability and supply management by OPEC+. This price instability directly undermines the ability of mid-sized and smaller geotextile manufacturers to offer competitive pricing on long-term procurement contracts, constraining both their revenue growth and their capacity to reinvest in R&D. The resulting margin compression can also limit the ability to invest in product innovation and sustainable material transitions.

Environmental and Disposal Concerns Surrounding Synthetic Geotextile Products

Growing scrutiny over microplastic pollution and the end-of-life disposal of synthetic geotextiles is emerging as a meaningful commercial and reputational constraint for the industry. Polypropylene and polyester geotextiles are non-biodegradable and have limited practical recyclability, raising concerns among environmental regulators and sustainability-focused procurement agencies. The European Environment Agency (EEA) has flagged synthetic polymer waste as a priority concern under the EU Circular Economy Action Plan. Several European national governments and municipalities are progressively introducing green procurement criteria that either restrict or penalize the use of non-recyclable synthetic geotextiles in publicly funded infrastructure projects. This regulatory and reputational pressure is beginning to influence tendering specifications, particularly in Scandinavia and Northern Europe, creating commercial headwinds for conventional synthetic geotextile producers that have not yet diversified into sustainable product lines.

Opportunities - Accelerating Adoption of Sustainable and Biodegradable Geotextile Solutions

The global pivot toward sustainable construction practices is unlocking a significant growth opportunity for biodegradable and natural geotextile products, particularly those derived from jute and coir. These natural fiber-based geotextiles offer performance comparable to synthetics in slope stabilization and erosion control, while biodegrading after their functional life, generating no polymer waste. The United Nations Environment Program (UNEP) and national green building councils are actively promoting the integration of natural and renewable construction materials. In India, the Jute Manufacturers Development Council (JMDC), under the Ministry of Textiles, has funded pilot projects to deploy jute geotextiles for road embankment reinforcement under state and central government highway programs. As LEED and BREEAM green certification frameworks progressively incorporate geosynthetic sustainability criteria, demand for eco-certified geotextile alternatives is projected to grow substantially through 2033, providing manufacturers who invest early in natural fiber product lines with a durable competitive advantage.

Climate Resilience Infrastructure Investment: Creating New Application Frontiers

The intensifying frequency and severity of extreme weather events is driving a structural increase in government and institutional investment in climate adaptation infrastructure, generating high-value new demand for geotextiles in flood defense, coastal erosion mitigation, and stormwater management systems. According to the World Meteorological Organization (WMO), the global incidence of weather-related disasters has increased by over 5 times over the past 50 years, compelling governments to prioritize climate-resilient construction. In Europe, the EU Flood Risk Management Directive and the European Climate Adaptation Strategy are directing dedicated funding toward riverbank reinforcement and nature-based flood protection solutions where geotextiles play a structural role. In the United States, the U.S. Army Corps of Engineers has substantially expanded its use of geotextile containment units and tube systems in shoreline protection and levee rehabilitation projects. These climate-driven infrastructure mandates are expected to establish a durable new demand tier for high-performance woven and composite geotextile products through the forecast period.

Category-wise Analysis

Material Type Insights

Synthetic geotextiles dominate the material type, accounting for 65% of the global geotextiles market share in 2025. Within the synthetic segment, polypropylene (PP)-based geotextiles hold the largest share, owing to their exceptional chemical resistance, low moisture absorption, high tensile strength, and significantly lower cost profile compared to polyester and polyethylene alternatives. Polypropylene geotextiles are extensively specified in road base stabilization, drainage layer construction, and erosion control applications, the highest-volume end-use areas globally. According to the International Geosynthetics Society (IGS), polypropylene consistently accounts for the majority of raw material consumption in global geosynthetic manufacturing. The material’s versatility in both woven and non-woven manufacturing processes across a broad weight spectrum further entrenches its commercial dominance. Meanwhile, polyester geotextiles are the fastest-growing sub-segment, driven by their superior strength-to-weight ratio and growing adoption in high-load reinforcement applications in challenging geotechnical environments.

Product Type Insights

Non-woven geotextiles lead the product category, holding a 55% share in 2025. Their market leadership stems from their exceptional breadth of functional application, filtration, drainage, separation, and cushioning, which aligns directly with the most prevalent requirements in transportation infrastructure and civil construction projects. Produced by needle-punching or thermal bonding, nonwoven geotextiles offer high conformability to irregular subgrade surfaces, superior isotropic filtration characteristics, and cost competitiveness for medium load requirements. The American Association of State Highway and Transportation Officials (AASHTO) has standardized the specification of non-woven geotextiles in pavement drainage systems and subgrade separation layers across U.S. highway projects, institutionalizing their procurement across state transportation agencies. Their wide availability across light, medium, and heavyweight variants further broadens their applicability, reinforcing category leadership. Knitted geotextiles represent the fastest-growing product type, driven by emerging applications in coastal engineering and retaining wall systems.

Application Insights

Erosion control is the dominant application segment, capturing approximately 28% of the total geotextiles share in 2025. This leadership position reflects the acute global need to address soil degradation and sediment runoff across construction sites, agricultural land, highway embankments, riverbanks, and coastal zones. The FAO estimates that approximately 24 billion tonnes of fertile soil are lost to erosion worldwide each year, driving significant public and private investment in geotextile-based erosion management systems. In the U.S., the EPA’s NPDES stormwater permit program mandates the use of erosion control best management practices on all regulated construction sites, creating a robust regulatory pull for geotextile erosion control blankets (ECBs), silt fences, and turf reinforcement mats. Geotextiles used in erosion control applications demonstrate superior cost-effectiveness compared to hard engineering alternatives such as concrete revetments, further supporting segment leadership. Drainage System applications represent the fastest-growing segment, driven by expanding urban stormwater infrastructure investments globally.

End-Use Industry Analysis

Transportation Infrastructure is the leading end-use industry segment, accounting for approximately 38% of global geotextiles demand in 2025. Roads, highways, railways, airports, and port infrastructure represent the largest single consumer base for geotextile products, deploying them across subgrade separation, drainage layer construction, slope reinforcement, and pavement system applications. According to the World Bank, developing countries alone require an estimated US$ 1-1.5 trillion in annual infrastructure investment to sustain economic growth, with road and rail networks accounting for the majority of this requirement. In the U.S., the Federal Highway Administration (FHWA) references geotextile specifications in pavement design guidelines, standardizing their adoption across federally funded transportation projects. In India, the Bharatmala Pariyojana program, targeting 65,000 km of new highway construction, is creating sustained, multi-year procurement volumes for woven and non-woven geotextiles. Environmental Engineering represents the fastest-growing end-use segment, driven by growing waste containment and remediation project pipelines globally.

Regional Insights

North America Geotextiles Market Trends and Insights

North America holds a dominant position in the global geotextiles market, underpinned by the United States’ mature infrastructure base, well-established regulatory framework, and robust construction activity. The Infrastructure Investment and Jobs Act (IIJA) continues to unlock federal funding streams for highway rehabilitation, stormwater infrastructure, and flood control projects, each representing significant demand drivers for geotextile products. The U.S. Army Corps of Engineers remains one of the world’s largest institutional consumers of geotextile materials, deploying them extensively in levee reinforcement, coastal protection, and dredged material containment applications.

Canada is similarly witnessing growing geotextile adoption, particularly in pipeline burial protection, oil sands site containment in Alberta, and highway construction in northern climates where geotextile-based frost protection layers are widely used. Compliance requirements under Environment and Climate Change Canada (ECCC) are encouraging industrial operators to deploy geotextile containment liners and filtration systems at resource extraction sites. Regional innovation is also accelerating, with manufacturers developing freeze-thaw resistant geotextile grades tailored to North American climatic conditions, reinforcing the region’s technology leadership in specialty geosynthetics.

Europe Geotextiles Market Trends and Insights

Europe represents a mature yet technologically innovative geotextiles market, with Germany, the United Kingdom, France, and the Netherlands as leading national contributors. The region operates under a harmonized regulatory framework anchored by the EU Construction Products Regulation (CPR), which mandates performance certification for geosynthetic materials deployed in public infrastructure projects. The European Geosynthetics Society (EGS) plays an active role in promoting standardized testing and application guidelines, facilitating the consistent adoption of geotextile solutions across member states.

Germany hosts leading global geotextile manufacturers including NAUE GmbH & Co. KG and HUESKER Group, reinforcing the country’s status as both a production hub and a technology innovator. The EU Green Deal and the European Climate Adaptation Strategy are channeling investment toward flood resilience and nature-based coastal protection infrastructure, creating demand for geotextile-based containment and erosion management solutions. France and Spain are witnessing increased geotextile adoption in high-speed rail corridor development and motorway reinforcement programs. The United Kingdom’s post-Brexit infrastructure acceleration initiatives are further contributing to regional demand, particularly in drainage and separation applications.

Asia Pacific Geotextiles Market Trends and Insights

Asia Pacific is the leading regional market for geotextiles, accounting for approximately 42% of global demand in 2025, and is expected to sustain its dominant position through 2033. The region’s growth trajectory is anchored in massive infrastructure development programs across China, India, Indonesia, and Vietnam. China’s 14th Five-Year Plan (2021-2025) directed substantial investment into national highway expansion, high-speed rail, and hydraulic infrastructure, all major demand generators for geotextile reinforcement, drainage, and erosion control products.

India stands out as one of the fastest-growing individual country markets within Asia Pacific, driven by the Bharatmala Pariyojana highway development program, the Sagarmala port modernization initiative, and the Jal Shakti Mission for water conservation, all creating substantial demand for woven and non-woven geotextile products. The ASEAN bloc’s rapid urbanization and industrial site development are similarly driving demand for geotextile-based containment and separation solutions. Asia Pacific’s cost-competitive manufacturing base, particularly in India and China, supports local production economics that sustain regional price competitiveness and enable aggressive export market penetration by domestic producers.

Competitive Landscape

The global geotextiles market exhibits a moderately consolidated structure, with a mix of multinational manufacturers and regional specialists competing on performance, pricing, and application-specific solutions. Market participants differentiate through advanced material technologies, compliance with international quality standards, and strong engineering support capabilities tailored to infrastructure and environmental projects. While large players benefit from integrated operations and global supply chains, regional firms maintain competitiveness through cost efficiency and localized expertise.

Key business strategies center on expanding presence in high-growth regions such as Asia and the Middle East, where infrastructure investments remain robust. Companies are increasingly focusing on sustainable product development, including biodegradable and eco-friendly geotextiles, to align with evolving environmental regulations. Additionally, firms are investing in digital tools for design optimization and material selection, enhancing customer engagement. Strategic collaborations, acquisitions, and capacity expansions are also being pursued to strengthen distribution networks and diversify application portfolios.

Key Developments

- March 2025: NAUE GmbH & Co. KG expanded its geosynthetics production capacity at its Espelkamp facility in Germany to address rising European demand for high-performance geotextiles in flood protection and climate adaptation infrastructure projects.

- January 2024: Officine Maccaferri S.p.A. launched an upgraded line of woven geotextile reinforcement solutions targeting high-growth infrastructure markets in Southeast Asia and the Middle East, extending its geographic diversification strategy.

- October 2023: Fibertex Nonwovens A/S entered into a strategic partnership with a Scandinavian civil engineering consultancy to co-develop EU Green Deal-compliant, recyclable geotextile solutions, reinforcing its sustainability-driven competitive positioning in European markets.

Companies Covered in Geotextiles Market

- Koninklijke Ten Cate B.V.

- GSE Holdings, Inc.

- NAUE GmbH & Co. KG

- Officine Maccaferri S.p.A.

- Low and Bonar PLC

- Propex Operating Company, LLC

- Fibertex Nonwovens A/S

- TENAX Group

- AGRU America

- Global Synthetics

- HUESKER Group

- TYPAR

- Machina-TST

- Gayatri Polymers & Geo-synthetics

- Strata Geosystems (India) Pvt. Ltd.

- TenCate Geosynthetics Asia

- Terram Geosynthetics

- Carthage Mills

- Maccaferri Industrial Group

Frequently Asked Questions

The global Geotextiles market is projected to reach US$ 9.3 billion in 2026.

Demand is driven by infrastructure investments, environmental regulations, and growing applications in erosion control, drainage, and soil reinforcement.

Asia Pacific leads the market, driven by strong infrastructure development and rapid urbanization.

Growth opportunities lie in biodegradable and sustainable geotextiles such as jute and coir-based products.

Key players include Koninklijke Ten Cate, NAUE, HUESKER, Maccaferri, Fibertex, Propex, GSE Holdings, TENAX, AGRU America, and Gayatri Polymers.