- Medical Devices

- Temperature Monitoring System Market

Temperature Monitoring System Market Size, Share, and Growth Forecast, 2025 - 2032

Temperature Monitoring System Market by Component Type (Thermometers, Data Loggers, Software, Other Components), Application (Food and Beverage, Healthcare, Pharmaceutical, Industrial), End-Use (Manufacturing, Healthcare and Lifesciences, Food and Beverage, Aerospace and Defense), and Regional Analysis for 2025 - 2032

Temperature Monitoring System Market Size and Trends Analysis

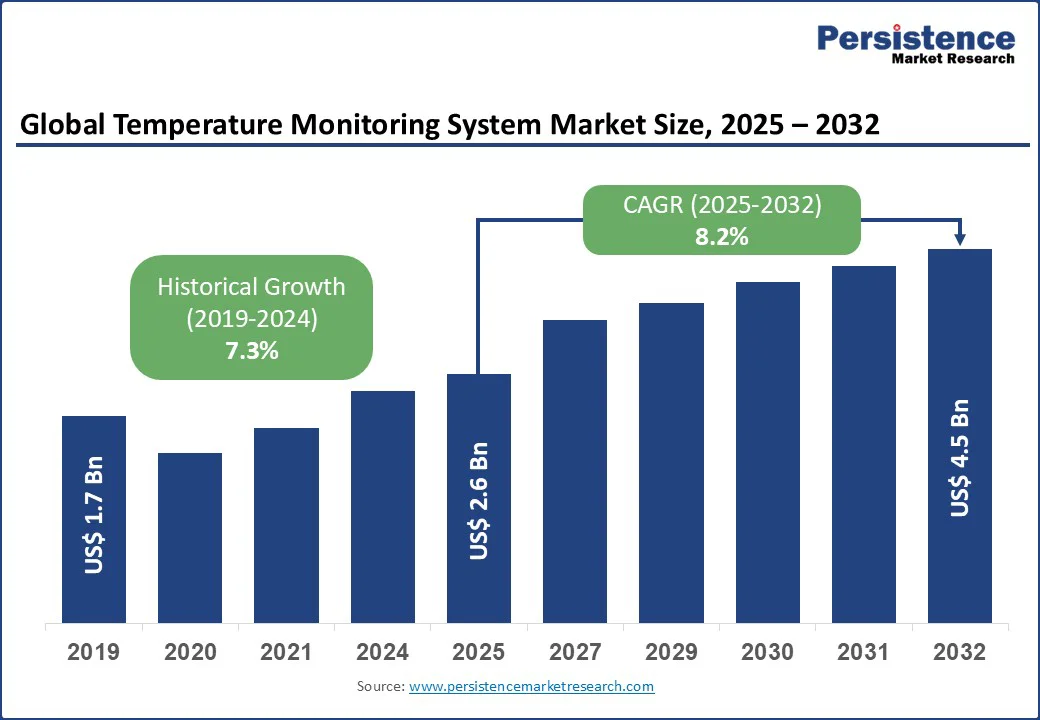

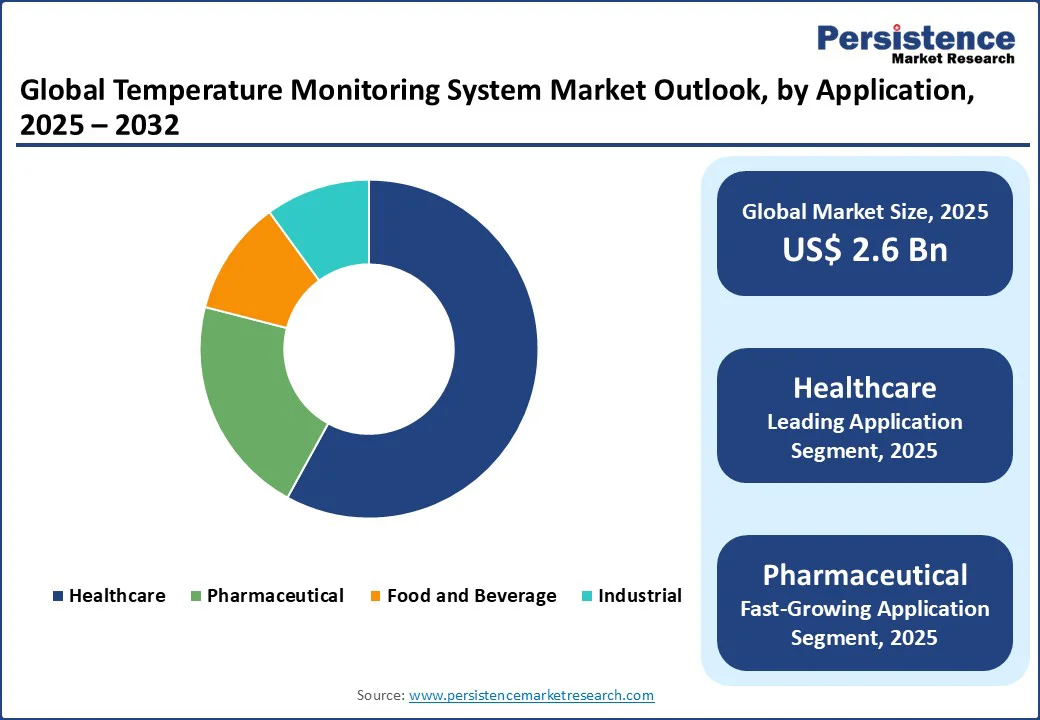

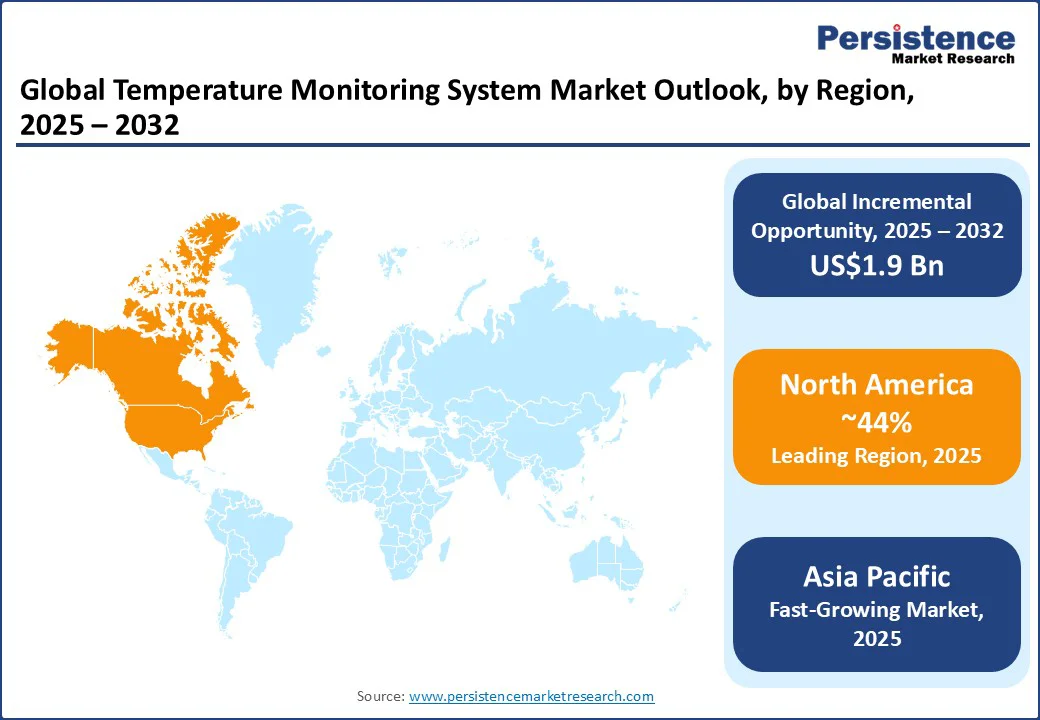

The global temperature monitoring system market size is likely to value at US$ 2.6 Bn in 2025 and is epxected to reach US$ 4.5 Bn by 2032, registering a CAGR of 8.2% during the forecast period from 2025 to 2032.

The temperature monitoring system market has experienced robust growth, driven by increasing demand for precise temperature control across various industries, including healthcare, food and beverage, pharmaceuticals, and industrial applications.

The rising adoption of automation, advancements in sensor technology, and stringent regulatory requirements for temperature-sensitive products are key factors propelling market expansion. Additionally, the growing focus on maintaining product quality, safety, and compliance with international standards has heightened the need for advanced temperature monitoring systems.

Key Industry Highlights:

- Leading Region: North America, holding a 44% market share in 2025, driven by advanced technological infrastructure, stringent regulatory standards, and high adoption in healthcare and pharmaceutical sectors.

- Fastest-growing Region: Asia Pacific, fueled by rapid industrialization, expanding healthcare infrastructure, and increasing investments in cold chain logistics.

- Dominant Component Type: Data Loggers, commanding nearly 42% market share, reflecting their critical role in real-time monitoring and compliance with regulatory standards.

- Leading Application: Healthcare, accounting for over 58% of market revenue, driven by the need for precise temperature monitoring in hospitals and laboratories.

|

Global Market Attribute |

Key Insights |

|

Temperature Monitoring System Market Size (2025E) |

US$2.6 Bn |

|

Market Value Forecast (2032F) |

US$ 4.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.3% |

Market Dynamics

Driver - Increasing Demand for Cold-chain Logistics

The increasing demand for cold chain logistics across industries such as pharmaceuticals, food and beverages, and biotechnology is driving the temperature monitoring systems market. Cold chain logistics ensures that temperature-sensitive products, including vaccines, biologics, perishable foods, and specialty chemicals, are stored and transported under strict temperature-controlled conditions. With the rising global trade of perishable goods and the expansion of pharmaceutical distribution networks, the need for reliable and real-time temperature monitoring has become critical.

Regulatory authorities such as the FDA, WHO, and EMA impose stringent guidelines for maintaining temperature integrity during storage and transit, further driving the adoption of advanced monitoring solutions. Moreover, the rapid expansion of e-commerce-driven grocery delivery and the surge in vaccine distribution post-pandemic have accelerated the growth of cold chain logistics worldwide. For instance, during the COVID-19 vaccine rollout, pharmaceutical companies and logistics providers relied heavily on IoT-enabled data loggers and cloud-based monitoring platforms to ensure vaccines were maintained within the required temperature range, highlighting the indispensable role of advanced monitoring systems. As a result, demand for IoT-enabled and cloud-based solutions continues to rise, ensuring compliance, reducing wastage, and enhancing supply chain transparency.

Restraint - High Initial Costs and Maintenance Challenges

The high initial investment and ongoing maintenance requirements associated with advanced monitoring solutions. Modern systems often integrate IoT, cloud computing, AI, and wireless connectivity to provide real-time temperature tracking, but these features significantly increase upfront costs for installation, calibration, and integration with existing infrastructure. Small and medium-sized enterprises (SMEs), particularly in developing economies, often find it difficult to justify these expenses, especially when dealing with narrow profit margins.

Temperature monitoring systems require periodic calibration, sensor replacement, and software updates to maintain accuracy and compliance with regulatory standards. This adds to long-term operational costs, making the systems less attractive for cost-sensitive users. For instance, pharmaceutical cold chain providers often face high maintenance expenses to ensure continuous compliance with FDA and WHO guidelines, which can deter smaller players from adopting sophisticated monitoring technologies. These financial barriers may slow widespread adoption, particularly in emerging markets.

Opportunity - Integration of IoT and AI Technologies

The integration of IoT (Internet of Things) and AI (Artificial Intelligence) technologies presents a significant growth opportunity for the temperature monitoring system market. IoT-enabled devices allow real-time data collection and remote monitoring, ensuring that temperature-sensitive products in pharmaceuticals, food, and biotechnology are consistently tracked across the supply chain. When combined with AI, these systems can analyze vast amounts of sensor data, predict potential equipment failures, and trigger proactive maintenance, thereby minimizing downtime and losses.

AI algorithms can also optimize temperature control by learning usage patterns and environmental factors, improving both efficiency and energy consumption. For instance, IoT-connected sensors integrated with AI analytics are being adopted in pharmaceutical cold chain logistics to predict temperature excursions before they occur, ensuring regulatory compliance and product safety. This convergence of IoT and AI not only enhances transparency and automation but also supports scalability, making advanced monitoring solutions more attractive to global manufacturers, logistics providers, and healthcare institutions.

Category-wise Analysis

Component Type Insights

Data Loggers dominate the temperature monitoring system market, expected to account for approximately 42% of the market share in 2025. Their dominance stems from their widespread use in industries requiring continuous and accurate temperature monitoring, such as pharmaceuticals, healthcare, and food and beverage. Data loggers offer real-time data recording, storage, and remote access capabilities, making them essential for regulatory compliance and quality assurance. Their compatibility with IoT and cloud-based platforms further enhances their applicability across various industries.

The Software segment is the fastest-growing from 2025 to 2032, driven by the increasing adoption of cloud-based and AI-integrated monitoring solutions. Software platforms enable centralized data management, real-time analytics, and seamless integration with IoT devices, making them critical for large-scale operations.

Application Insights

Healthcare leads the temperature monitoring system market, holding a 58% share in 2025. The segment’s dominance is driven by the critical need for precise temperature control in hospitals, laboratories, and blood banks to ensure the safety of temperature-sensitive products such as vaccines, biologics, and diagnostic samples. Stringent regulatory requirements and the increasing prevalence of chronic diseases further boost the adoption of temperature monitoring systems in this segment.

The pharmaceutical segment is the fastest-growing, driven by the rising demand for temperature-sensitive drug storage and transportation. The global pharmaceutical cold chain market is expanding rapidly due to the increasing production of biologics and vaccines, which require strict temperature control.

End-Use Insights

Healthcare and life sciences dominate the market, accounting for approximately 40% of revenue in 2025. The segment’s leadership is driven by the critical role of temperature monitoring in ensuring the safety and efficacy of medical products, such as vaccines, blood, and biologics. Regulatory bodies such as the FDA and WHO emphasize stringent temperature control, further driving demand in this sector.

The food and beverage segment is the fastest-growing, fueled by the increasing need for cold chain logistics to ensure the safety and quality of perishable goods. The rise in global food trade, e-commerce, and consumer demand for fresh and frozen products is driving the adoption of temperature monitoring systems. The segment is particularly strong in emerging markets such as the Asia Pacific, where investments in cold chain infrastructure are accelerating.

Regional Insights

North America Temperature Monitoring System Market Trends

North America, holding a 44% market share in 2025, dominates the global temperature monitoring system market due to its advanced technological infrastructure, stringent regulatory standards, and high adoption in healthcare and pharmaceutical sectors. The U.S. market is particularly prominent, driven by the presence of leading players such as 3M, Emerson Electric, and Honeywell International. The U.S. accounts for over 80% of the regional market share, supported by a high prevalence of chronic diseases, robust cold chain logistics, and significant investments in healthcare R&D. According to the CDC, chronic diseases affect 60% of U.S. adults, increasing the demand for temperature-sensitive medical products and monitoring systems.

The U.S. benefits from advanced cold chain infrastructure, with companies investing heavily in IoT-enabled monitoring systems to comply with FDA regulations. Government initiatives, such as the FDA’s Drug Supply Chain Security Act (DSCSA), emphasize traceability and temperature control, further boosting market demand. Additionally, the growing adoption of automation in healthcare and food industries, coupled with favorable reimbursement policies, supports market growth. The aging population and rising healthcare expenditure continue to drive the need for temperature monitoring systems, solidifying North America’s leadership in the forecast period.

Europe Temperature Monitoring System Market Trends

Europe holds a significant share in the global temperature monitoring system market, driven by advanced technological adoption, stringent regulatory frameworks, and a focus on precision monitoring. Leading countries include Germany, the UK, and France. Germany benefits from its strong industrial base and leadership in pharmaceutical and healthcare technology, with companies such as Siemens AG investing in innovative monitoring solutions. The UK’s market is bolstered by government initiatives promoting digital healthcare and cold chain compliance. France’s market is supported by significant investments in healthcare infrastructure and sustainable manufacturing practices.

The European Medicines Agency (EMA) enforces strict guidelines on temperature control for pharmaceuticals, driving the adoption of advanced monitoring systems. The EU’s focus on sustainability and smart manufacturing further supports market growth, though compliance with complex regulations poses challenges. Europe’s temperature monitoring system market is projected to grow steadily from 2025 to 2032, driven by advancements in IoT and AI technologies.

Asia Pacific Temperature Monitoring System Market Trends

Asia Pacific is emerging as one of the fastest-growing regions in the temperature monitoring system market, fueled by rapid industrialization, increasing healthcare expenditure, and rising demand for cold chain logistics. Countries such as China, India, and Japan are key contributors, driven by growing investments in healthcare and food and beverage infrastructure. The region is witnessing a surge in demand for temperature-sensitive products, such as vaccines and perishable goods, due to changing consumer preferences and rising urbanization.

China leads the regional market, supported by government initiatives to modernize healthcare and expand cold chain logistics. India’s market is driven by increasing healthcare access and investments in pharmaceutical manufacturing. Japan’s advanced technological infrastructure and focus on precision monitoring further bolster regional growth. According to the WHO, the Asia Pacific accounts for a significant portion of the global vaccine market, driving demand for temperature monitoring systems. Rising healthcare spending, expanding cold chain networks, and growing awareness of regulatory compliance are positioning the Asia Pacific as a key growth engine for the market.

Competitive Landscape

The global temperature monitoring system market is characterized by intense competition, regional strengths, and a mix of international and local solution providers. In developed regions such as North America and Europe, large firms such as 3M, Emerson Electric, and Honeywell International dominate through scale, advanced R&D capabilities, and established partnerships across industries, including healthcare, pharmaceuticals, and food logistics. In the Asia Pacific, rapid industrialization, expanding cold chain infrastructure, and rising healthcare expenditures are attracting significant investments from both international players, such as Siemens AG and Omron Corporation, and regional manufacturers offering cost-effective solutions. Companies are increasingly focusing on IoT-enabled, AI-integrated, and cloud-connected systems as key differentiators, enabling real-time monitoring, predictive analytics, and stronger compliance with regulatory standards. Strategic collaborations with healthcare providers, pharmaceutical distributors, and logistics companies, along with acquisitions of smaller technology firms, are further intensifying the competitive landscape. Overall, the sector exhibits a dual nature: consolidated at the top by global giants such as 3M and Emerson Electric, while remaining fragmented among numerous regional and niche players catering to local needs and affordability-driven markets.

Key Developments

- In January 2024, Emerson Electric Co. launched a new IoT-enabled temperature monitoring system, enhancing real-time data analytics capabilities across various industries.

- In March 2024, Honeywell International Inc. entered into a strategic partnership with a leading logistics company to provide advanced temperature monitoring solutions designed for high-stakes environments such as cold chain logistics.

Companies Covered in Temperature Monitoring System Market

- 3M

- Emerson Electric Co.

- Siemens AG

- Honeywell International Inc.

- TE Connectivity

- Datalogic S.p.A.

- Omron Corporation

- Omega Engineering

- Schneider Electric

- Fluke Corporation

- Danaher Corporation

- Texas Instruments

- Sensirion AG

- Yokogawa Electric Corporation

- Others

Frequently Asked Questions

The global Temperature Monitoring System market is projected to reach US$ 2.6 Bn in 2025.

The increasing demand for cold chain logistics is a key driver.

The temperature monitoring system market is poised to witness a CAGR of 8.2% from 2025 to 2032.

Integration of IoT and AI technologies is a key opportunity.

3M, Emerson Electric, Siemens AG, Honeywell International, and Omega Engineering are key players.