- Specialty & Fine Chemicals

- High Temperature Resin Market

High Temperature Resin Market Size, Share, and Growth Forecast, 2026 - 2033

High Temperature Resin Market by Resin Type (Polyimide, Epoxy, Others), Application (Aerospace, Automotive, Others), End-user (Automotive & Transportation, Others), and Regional Analysis for 2026 – 2033

High Temperature Resin Market Size and Trends Analysis

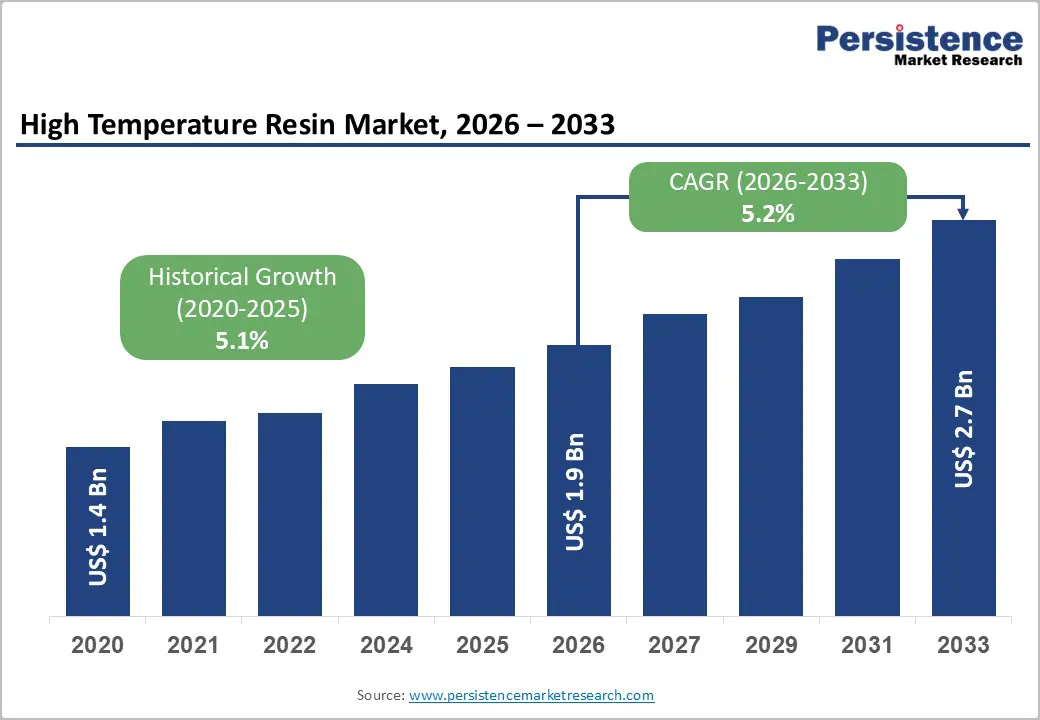

The global high temperature resin market size is likely to be valued at US$1.9 billion in 2026, and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of lightweight, heat-resistant composites in aerospace and automotive industries, rising demand for high-performance polymers in electric vehicles and electronics, and growing adoption of polyimide and fluoropolymer resins for extreme-temperature applications.

Growing demand for durable, flame-retardant, high temperature resin, especially in aerospace & defense and industrial manufacturing, is accelerating adoption across end-uses. Advances in low-VOC, recyclable formulations and reinforced grades are further boosting uptake by offering better thermal stability and regulatory compliance. Increasing recognition of high-temperature resin as critical for weight reduction, fuel efficiency, and component longevity in emerging EV, 5G, and sustainable aviation markets remains a major driver of market growth.

Key Industry Highlights:

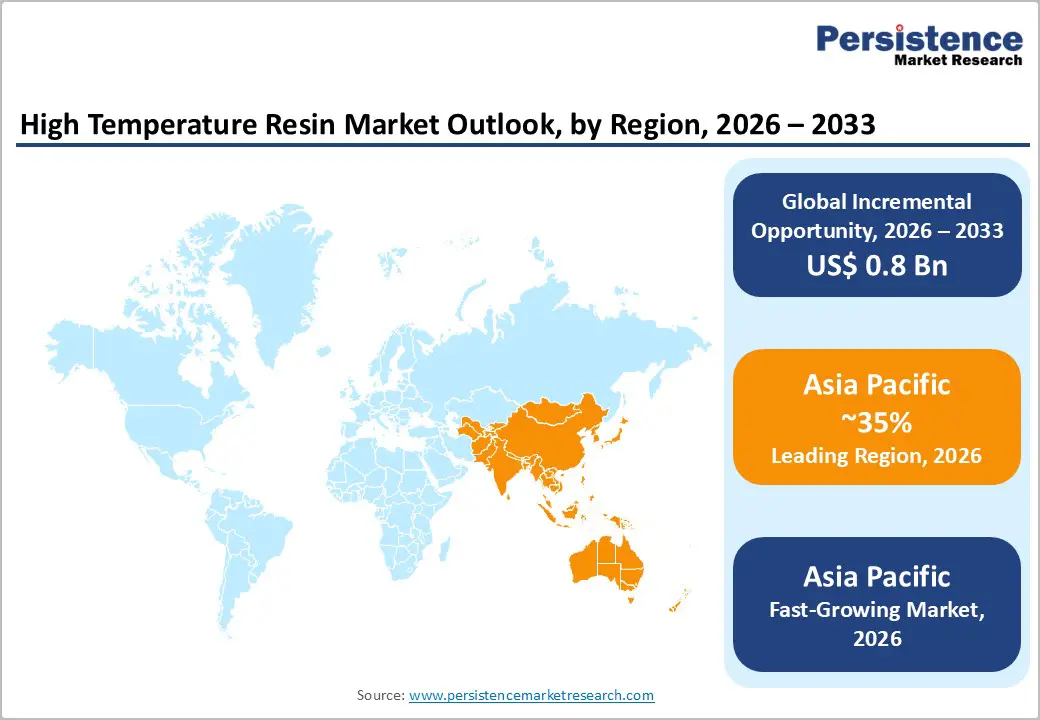

- Leading Region: Asia Pacific, anticipated to account for a 35% market share in 2026, due to its large and expanding manufacturing base in key end-use industries such as electronics, automotive, aerospace, and industrial equipment.

- Fastest-growing Region: Asia Pacific, fueled by rapid industrialization, rising demand for consumer electronics, expansion of electric vehicle production, and increased aerospace manufacturing activities.

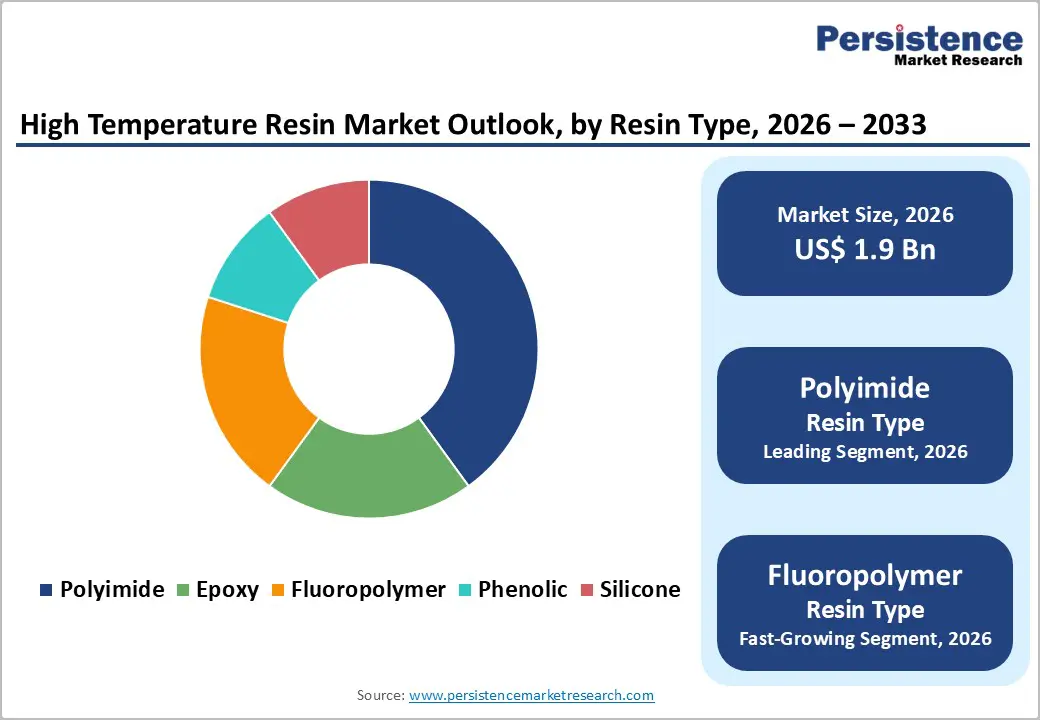

- Dominant Resin Type: Polyimide, to hold approximately 38% of the market share, as it offers the highest thermal stability and is preferred in aerospace and electronics.

- Leading Application: Aerospace, to contribute nearly 32% of the market revenue, due to extensive use in engine components and structural composites.

- Leading End-user: Aerospace & defense, to account for over 34% of the market revenue, due to stringent performance requirements in extreme conditions.

| Key Insights | Details |

|---|---|

| High Temperature Resin Market Size (2026E) | US$1.9 Bn |

| Market Value Forecast (2033F) | US$2.7 Bn |

| Projected Growth CAGR (2026-2033) | 5.2% |

| Historical Market Growth (2020-2025) | 5.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Lightweight, Heat-Resistant Materials in Aerospace and Electric Vehicles

The need for high-performance, lightweight, and heat-resistant materials in aerospace and electric vehicles (EVs) is growing rapidly due to increasing demands for efficiency, safety, and durability. In aerospace, reducing structural weight directly improves fuel efficiency and payload capacity, while heat-resistant materials are critical for components exposed to high temperatures, such as engines, turbine housings, and thermal insulation systems. Advanced polymers, composites, and metal alloys are being increasingly adopted to meet these requirements, as they provide a balance between strength, thermal stability, and reduced mass.

In EVs, lightweight materials are essential to offset the weight of batteries, improving driving range and overall efficiency. Heat-resistant materials are necessary for battery housings, electric motor components, and power electronics, which generate significant heat during operation. Using materials that can withstand high temperatures without deformation or degradation ensures the safety, reliability, and longevity of EV systems. The push for sustainability is also fueling demand for such materials, as lighter vehicles consume less energy and produce fewer emissions.

Increasing Replacement of Traditional Metals and Lower-Performance Polymers

The increasing replacement of traditional metals and lower-performance polymers is driven by the need for materials that offer better strength-to-weight ratios, durability, and thermal performance across industries such as automotive, aerospace, and electronics. Conventional metals, while strong and reliable, are often heavy and contribute to higher fuel consumption and energy use in vehicles and aircraft. Similarly, standard polymers may lack the thermal stability, mechanical strength, or chemical resistance required for high-performance applications. Manufacturers are increasingly turning to advanced composites, high-performance polymers, and lightweight alloys that provide superior functionality without adding excessive weight.

In automotive and electric vehicle sectors, lighter materials help improve efficiency, reduce emissions, and extend battery range, while maintaining structural integrity. Aerospace applications benefit from enhanced materials that withstand extreme temperatures, pressure, and mechanical stress, supporting safety and operational efficiency. High-performance polymers and reinforced composites also enable designers to consolidate multiple parts into single components, reducing assembly complexity and cost. The shift away from traditional metals and low-performance polymers is further accelerated by sustainability goals, as lighter and more durable materials contribute to lower energy consumption over a product’s lifecycle.

Barrier Analysis - High Raw Material Costs and Complex Synthesis Processes

High raw material costs and complex synthesis processes represent significant challenges in the adoption and production of advanced materials across industries such as automotive, aerospace, electronics, and energy. Many high-performance materials, including specialty polymers, composites, and metal alloys, rely on expensive feedstocks or rare elements that are subject to price fluctuations in global markets. The cost of these raw materials can substantially increase the overall production expenses, making products less competitive, especially in cost-sensitive markets.

In addition to material costs, the synthesis and manufacturing processes for advanced materials are often intricate and resource-intensive. For example, producing high-performance polymers or reinforced composites may involve multiple stages such as polymerization, curing, high-temperature treatments, or fiber integration. These processes require specialized equipment, skilled personnel, and strict quality control measures to achieve consistent properties and performance. Any deviations can lead to defects, reduced durability, or failure to meet safety standards, further increasing production risk and costs. The combination of expensive raw materials and complex production techniques can slow scaling, limit availability, and hinder widespread adoption.

Limited Scalability and Quality Control Challenges

The challenges of limited scalability and maintaining consistent quality pose significant barriers in the production and adoption of advanced materials such as high-performance polymers, composites, and specialty alloys. Many of these materials require intricate synthesis processes, precise temperature control, specialized equipment, and skilled operators to achieve the desired mechanical, thermal, or chemical properties. While small-scale production can be carefully monitored, scaling up to meet industrial or commercial demand introduces variability that can compromise material performance. For instance, inconsistencies in curing, fiber orientation, or chemical composition can reduce strength, thermal stability, or durability, impacting product reliability and safety.

Quality control becomes even more critical in industries like aerospace, automotive, and electronics, where material failure can lead to costly recalls, system malfunctions, or safety hazards. Implementing rigorous testing, inspection, and certification processes adds complexity, time, and cost to production. Furthermore, any deviation in process parameters during large-scale manufacturing can result in defective batches, making mass production unpredictable and financially risky.

Opportunity Analysis - Development in Electronics and Semiconductor Sector

The development of the electronics and semiconductor sector is creating significant opportunities for the high-temperature resin market. As electronic devices, circuit boards, and semiconductor components become increasingly compact and powerful, the demand for materials that can withstand elevated temperatures, mechanical stress, and chemical exposure has grown. High-temperature resins are widely used in printed circuit boards (PCBs), encapsulation, insulation, and packaging of semiconductor devices to ensure reliability, prevent thermal degradation, and extend component lifespan.

The rapid adoption of advanced technologies, including 5G communication systems, high-performance computing, and electric mobility, is driving the need for thermally stable materials capable of operating under continuous high power and heat generation. Semiconductor manufacturing processes, such as wafer fabrication and high-temperature soldering, also require resins that can maintain structural integrity under extreme conditions. The trend toward miniaturization and higher component density in electronic devices has increased the complexity of thermal management, making high-temperature resins essential for insulation and protection.

Expansion of R&D for Enhanced Material Performance

Increasing investment in research and development (R&D) to improve material performance presents a major growth opportunity in the high-temperature resin market. Manufacturers and material scientists are increasingly investing in R&D to develop resins with superior thermal stability, mechanical strength, chemical resistance, and flame retardancy. These innovations allow high-temperature resins to meet the evolving demands of industries such as aerospace, automotive, electronics, and energy, where components are subjected to extreme operating conditions.

Advanced R&D efforts focus on creating formulations that can endure higher temperatures without degradation, maintain structural integrity under mechanical stress, and resist chemical or environmental exposure. For example, combining high-temperature resins with reinforcing fibers, fillers, or nanomaterials can improve thermal conductivity, strength, and durability, enabling their use in more demanding applications such as electric vehicle battery housings, aerospace engine components, or high-performance electronic devices. R&D also supports customization, allowing manufacturers to develop materials tailored for specific industrial needs, regulatory requirements, or performance standards.

Category-wise Analysis

Resin Type Insights

Polyimide is anticipated to dominate the market, accounting for approximately 38% of the market share in 2026. Its dominance is driven by exceptional thermal stability, chemical resistance, and mechanical strength. Its ability to withstand continuous high temperatures without degradation makes it ideal for demanding applications in aerospace, electronics, and automotive sectors. Polyimide is widely used in flexible printed circuit boards, insulation films, and advanced composites, where reliability under extreme conditions is critical. Kapton® polyimide films serve as dielectric substrates in flexible printed circuits and high-density interconnects, and they are used extensively in spacecraft thermal blankets, satellite components, and advanced electronic devices that must withstand harsh thermal environments.

Fluoropolymer represents the fastest-growing resin type, due to exceptional chemical resistance, thermal stability, and low friction properties, which make it ideal for demanding applications across industries. Unlike many conventional polymers, fluoropolymers maintain performance in extreme temperatures, corrosive environments, and high-wear environments, supporting their use in coatings, wiring insulation, seals, and high-temperature gaskets. Growth in sectors such as semiconductors, automotive EV components, and chemical processing equipment is increasing demand for fluoropolymers. Chemours Company’s Teflon® brand of fluoropolymer resins, Teflon® PTFE (polytetrafluoroethylene), and related fluoropolymers are widely used for high-temperature, chemical-resistant coatings, sealants, and insulating films across industries such as electronics, automotive, and chemical processing.

Application Insights

The aerospace industry is expected to dominate the market, contributing nearly 32% of revenue in 2026, due to remaining the primary application for engine parts, structural composites, and large high-temperature programs requiring extreme thermal and mechanical performance. Their strong integration, trained fabricators, and ability to handle high-value or certified blends drive higher consumption. Aerospace sectors are leading polyimide rollouts as well as administering emerging fluoropolymer trials. For example, large OEMs routinely use high temperature resin in turbine components while also participating in lightweight blend trials, ensuring parts receive specialized, heat-resistant solutions with high standards.

The automotive segment is the fastest-growing application, driven by its strong EV powertrain presence and expanding role in battery enclosures, connectors, and under-hood components. They offer convenient, quick, and accessible thermal stability, attracting manufacturers who prefer lightweight, durable settings. Increased outreach programs, electrification focus, and wider availability of routine and premium resins further accelerate uptake, boosting rapid adoption across both passenger and commercial vehicle segments. For example, automotive brands such as BASF SE provide walk-in lines for EV-grade resins, making high-temperature protection more accessible to global populations while reducing pressure on metal alternatives.

Regional Insights

North America High Temperature Resin Market Trends

North America is driven by the region’s advanced aerospace and electronics manufacturing, strong research and development capabilities, and high public awareness of lightweighting benefits. Production systems in the U.S. and Canada provide extensive support for high temperature resin programs, ensuring wide accessibility across aerospace, automotive, and electronics populations. Increasing demand for polyimide, convenient, and easy-to-process forms is further accelerating adoption, as these formats improve performance and reduce barriers associated with metal substitution.

Innovation in high temperature resin technology, including stable reinforced, improved medical-grade delivery, and targeted lightweight enhancement, is attracting significant investment from both public and private sectors. Government initiatives and FAA/DOE campaigns continue to promote use against weight risks, fuel efficiency concerns, and emerging electrification threats, creating sustained market demand. The growing focus on automotive grades and specialty uses, particularly for aerospace & defense and others, is expanding the target applications for high temperature resin.

Europe High Temperature Resin Market Trends

Europe's growth is propelled by increasing awareness of lightweighting benefits, strong regulatory systems, and government-led aerospace electrification programs. Countries such as Germany, France, the U.K., and Italy have well-established manufacturing frameworks that support routine high temperature resin use and encourage the adoption of innovative material delivery methods, including polyoxymethylene and fluoropolymers. These high-performance formulations are particularly appealing for aerospace populations, regulation-conscious OEMs, and electronics users, improving efficiency and coverage rates.

Technological advancements in high temperature resin development, such as enhanced reinforcement, application-targeted delivery, and improved medical grades, are further boosting market potential. European authorities are increasingly supporting research and trials for resins against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-weight options is aligned with the region’s focus on preventive CO2 reduction and electrification. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in compounding and novel variants to increase efficacy.

Asia Pacific High Temperature Resin Market Trends

Asia Pacific is projected to dominate and be the fastest-growing market, capturing 35% share in 2026, driven by rising automotive and electronics awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting resin campaigns to address vehicle and device growth and emerging high-heat needs. High temperature resin is particularly attractive in these regions due to its cost-effective administration, ease of molding, and suitability for large-scale automotive and electronics drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-process high temperature resin, which can withstand challenging operating conditions and minimize performance dependence. These innovations are critical for reaching domestic OEMs and improving overall component coverage. Growing demand for automotive, electronics & electrical, and aerospace & defense applications is contributing to market expansion. Public-private partnerships, increased manufacturing expenditure, and rising investment in resin research and compounding capacity are further accelerating growth. The convenience of resin delivery, combined with improved thermal stability and reduced risk of failure, positions it as a preferred choice.

Competitive Landscape

The global high temperature resin market features competition between established chemical giants and emerging specialty polymer suppliers. In North America and Europe, Solvay S.A. and Henkel AG & Co. KGaA lead through strong R&D, distribution networks, and OEM ties, bolstered by innovative polyimide and fluoropolymer programs.

In Asia Pacific, Mitsubishi Chemical Group and DIC Corporation advance with localized solutions, enhancing accessibility. Reinforced delivery boosts mechanical performance, cuts weight risks, and enables mass integrations across components. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Medical-grade formulations solve biocompatibility issues, aiding penetration in healthcare applications.

Key Industry Developments:

- In May 2025, Cambium launched its ApexShield™ 1000 high-temperature resin system, designed to enhance production speed for carbon-carbon (C/C) composite components used in hypersonic glide bodies, rocket nozzle extensions, and ablative applications like solid rocket motor nozzles and ship-based vertical launch tubes.

- In January 2025, SIOResin® SIO-517, a room-temperature curing silicone resin, was introduced. It provided a unique balance of high hardness and toughness, forming a dense, durable coating that protected surfaces from environmental damage while maintaining resilience under extreme conditions.

Companies Covered in High Temperature Resin Market

- Dow Corning Corporation

- Henkel AG & Co. KGaA

- Mitsui Chemicals, Inc.

- Solvay S.A.

- DIC Corporation

- Dupont

- Hexion

- BASF SE

- Huntsman Corporation

- Wacker Chemie AG

- Aditya Birla Chemicals

- Koninklijke Ten Cate B.V.

Frequently Asked Questions

The global high temperature resin market is projected to reach US$1.9 billion in 2026.

Lightweighting in the aerospace and automotive industries and metal-to-plastic conversion are key drivers.

The high temperature resin market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Next-generation high-temperature composites and sustainable resin platforms are key opportunities.

Solvay S.A., Henkel AG & Co. KGaA, Mitsubishi Chemical Group, DuPont, and BASF SE are the key players.