- Industrial Goods & Service

- Steel Wire Rope Market

Steel Wire Rope Market Size, Share, and Growth Forecast, 2025 - 2032

Steel Wire Rope Market by Material (Carbon Steel, Stainless Steel, Alloy Steel, Others), Application (Construction, Automotive, Energy, Industrial, Agriculture, Others), and Regional Analysis for 2025 - 2032

Steel Wire Rope Market Share and Trends Analysis

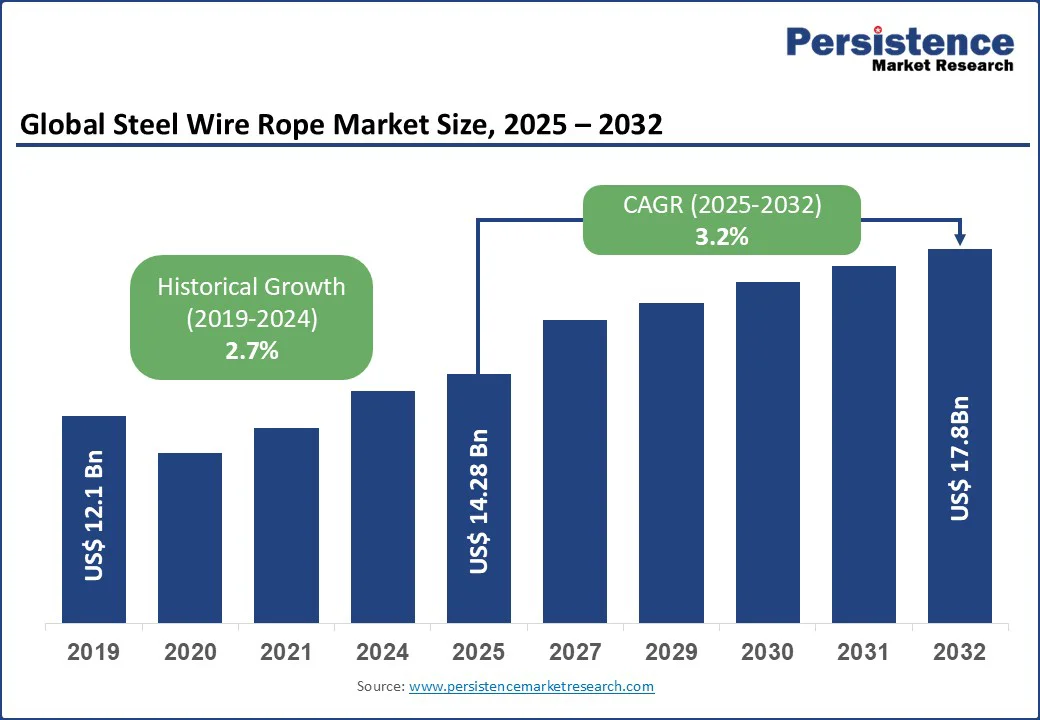

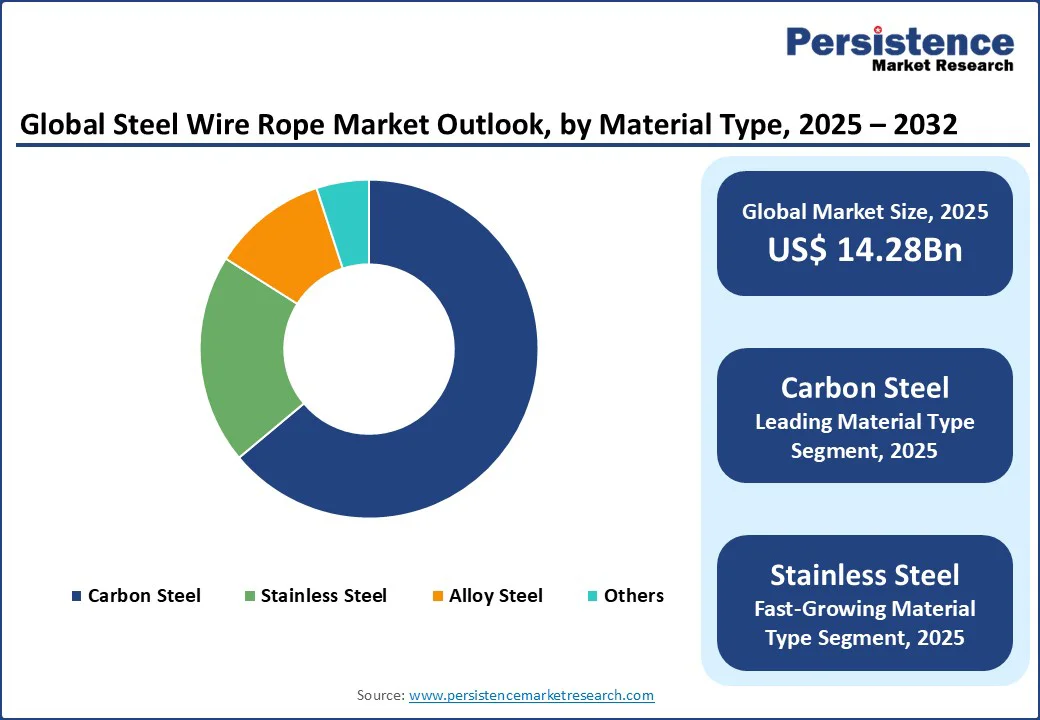

The global steel wire rope market size is likely to value at US$14.28 Bn in 2025 and reach US$17.8 Bn by 2032, growing at a CAGR of 3.2% during the forecast period from 2025 to 2032.

The steel wire rope industry is witnessing steady growth, driven by increasing demand from key industries such as construction, automotive, and energy, where high tensile strength and durability are critical. Steel wire ropes, known for their robustness, flexibility, and resistance to corrosion, are essential for lifting, hoisting, and suspension applications. The rise in global infrastructure projects, coupled with advancements in manufacturing technologies, supports market expansion.

Key Industry Highlights

- Investment Plans: China’s National Development and Reform Commission announced a 2022 plan to construct 461,000 km of highways by 2035, which is expected to boost demand for steel wire ropes in construction applications.

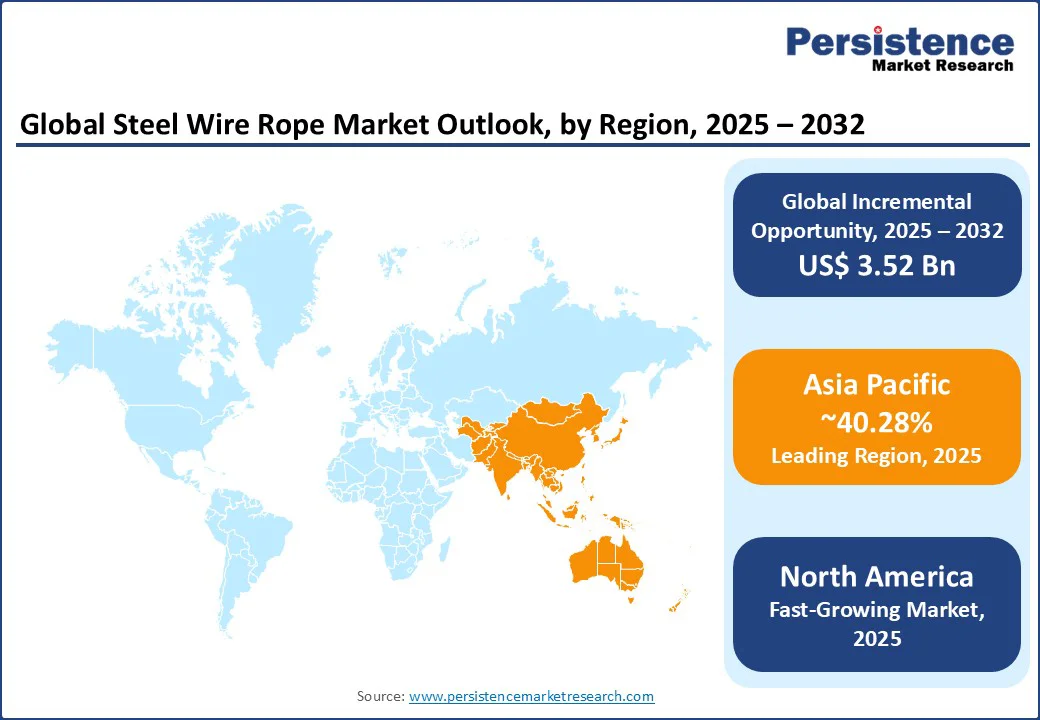

- Leading Region: Asia Pacific holds 67.24% market share in 2025, propelled by rapid urbanization, infrastructure investments, and high steel production in countries such as China and India.

- Fastest-growing Region: North America is the fastest-growing region, driven by robust construction and mining sectors in the U.S. and Canada, supported by advanced industrial infrastructure.

- Dominant Material Type: Carbon Steel, accounting for nearly 63.8% of the market share, due to its cost-effectiveness and high tensile strength for heavy-duty applications.

- Leading Application: Construction, contributing over 39.28% of market revenue, driven by global infrastructure development and urbanization trends.

|

Global Market Attribute |

Key Insights |

|

Steel Wire Rope Market Size (2025E) |

US$ 14.28Bn |

|

Market Value Forecast (2032F) |

US$ 17.8Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.7% |

Market Dynamics

Driver: Growing Infrastructure and Construction Activities Fuel Market Expansion

The global steel wire rope market is experiencing significant growth due to the surge in infrastructure and construction activities worldwide. Steel wire ropes are critical in construction for lifting heavy materials, suspending scaffolding, and supporting structures such as suspension bridges. According to the World Bank, global infrastructure investment needs are expected to reach $94 trillion by 2040, with a significant portion allocated to emerging economies.

In the Asia Pacific, China’s Belt and Road Initiative and India’s Smart Cities Mission drive demand for high-strength ropes in construction applications. The American Society of Civil Engineers reports that 6,23,000 of U.S. bridges require repair or replacement, further increasing the need for durable steel wire ropes. Companies such as Bridon-Bekaert reported a sales increase in construction-grade ropes in 2024. Government-led initiatives and rising urbanization are expected to ensure sustained demand, positioning construction as a key driver of market growth through 2032.

Restraint: Volatility in Raw Material Prices and Competition from Synthetic Ropes

The steel wire rope market faces challenges due to fluctuating raw material prices and growing competition from synthetic ropes. Steel production relies heavily on iron ore and energy, both of which are subject to price volatility. In 2023, iron ore prices fluctuated, impacting production costs for manufacturers.

This volatility increases pricing pressures, particularly for smaller players, limiting their ability to compete. Additionally, synthetic ropes, such as those made from polyolefin fibers, are gaining traction due to their lighter weight and comparable strength. Limited standardization in some regions and concerns over corrosion in harsh environments further hinder adoption, particularly in cost-sensitive markets, restraining overall market growth.

Opportunity: Rising demand in the Renewable Energy and Electric Vehicle Sectors

The increasing focus on renewable energy and electric vehicles (EVs) presents significant opportunities for the steel wire rope market. Steel wire ropes are essential in renewable energy projects, such as offshore wind farms, for anchoring and lifting applications. The International Energy Agency projects global renewable energy capacity to grow by 2.7 times by 2030, with offshore wind investments driving demand for high-strength ropes.

In the EV sector, steel wire ropes are utilized in manufacturing processes and the assembly of battery components. Companies such as WireCo WorldGroup are innovating with corrosion-resistant ropes for renewable energy applications, aligning with the growing trend towards sustainability. Government incentives, such as the EU’s Green Deal, further encourage investments in green technologies, creating opportunities for manufacturers to develop advanced, eco-friendly steel wire ropes to meet evolving industry needs through 2032.

Category-wise Analysis

Material Type Insights

- Carbon steel holds the largest market share, approximately 63.8% in 2025, due to its high tensile strength and cost-effectiveness. Widely used in construction and industrial applications, carbon steel wire ropes are favored for their durability and ability to withstand heavy loads. Companies such as ArcelorMittal and Nippon Steel Corporation lead with extensive portfolios, catering to demand in infrastructure and mining sectors across North America and the Asia Pacific.

- Stainless steel is the fastest-growing material segment, driven by its superior corrosion resistance, making it ideal for marine and oil & gas applications. Its adoption is rising in harsh environments, such as offshore drilling, with brands like Kobe Steel expanding their offerings in coastal regions of Europe and the Asia Pacific, supported by growing demand for durable, long-lasting ropes.

Application Insights

- The construction sector accounts for over 39.28% of market revenue in 2025, driven by global infrastructure projects and urbanization. Steel wire ropes are critical for lifting heavy materials and supporting structures such as suspension bridges. Major players such as Bridon-Bekaert supply high-strength ropes for projects in the U.S. and China, where government investments in highways and bridges fuel demand.

- The energy sector is the fastest-growing application, propelled by rising investments in renewable energy and oil & gas exploration. Steel wire ropes are used in offshore wind farms and drilling rigs, with companies such as WireCo WorldGroup innovating for high-performance applications. Growth in the Asia Pacific and the Middle East, driven by energy infrastructure projects, supports the rapid expansion of this segment.

Regional Insights

Asia Pacific Steel Wire Rope Market Trends

Asia Pacific dominates the steel wire rope market, accounting for 67.24% in 2025, fueled by rapid urbanization, infrastructure investments, and high steel production in countries such as China and India. China, the world’s largest steel producer, contributes 54% of global steel output, per the World Steel Association, driving the availability of raw materials for wire ropes.

India’s infrastructure sector, supported by initiatives such as the Smart Cities Mission, boosts demand for construction-grade ropes. The region’s marine and mining industries also contribute, with companies such as Jiangsu Langshan and Tokyo Rope expanding their presence. Rising industrial manufacturing and government-led projects are expected to ensure the Asia Pacific’s rapid market growth through 2032.

North America Steel Wire Rope Market Trends

North America is the fastest-growing region, driven by robust demand from the construction and mining sectors in the U.S. and Canada, supported by advanced industrial infrastructure. According to the U.S. Census Bureau, the construction industry heavily relies on steel wire ropes for lifting and structural purposes.

Canada’s mining sector drives demand for durable ropes, per the Mining Association of Canada. Major players, such as Insteel Industries and WireCo WorldGroup, dominate with extensive distribution networks, catering to infrastructure projects including bridge repairs and high-rise constructions. Consumer preference for high-quality, corrosion-resistant ropes further strengthens North America’s market position.

Europe Steel Wire Rope Market Trends

Europe is the second-fastest-growing region for the steel wire rope market, driven by stringent safety regulations, rising demand in the automotive and maritime sectors, and infrastructure development in countries such as Germany and France. The European construction industry, valued at €1,683 billion in 2023 per the European Construction Industry Federation (FIEC), supports demand for steel wire ropes in bridge construction equipment and industrial applications.

Germany’s automotive sector, a key consumer of alloy steel ropes, benefits from players such as PFEIFER and Teufelberger. The EU’s Green Deal promotes renewable energy projects, increasing demand for corrosion-resistant ropes in offshore wind farms. Europe’s focus on sustainability and high-quality standards drives market growth, with companies innovating to meet regulatory and consumer demands.

Competitive Landscape

The global steel wire rope market is highly competitive, dominating through extensive product portfolios and global distribution networks. The steel wire rope market is characterized as a fragmented market based on competitors. This is due to the presence of numerous domestic and international players, ranging from large, established companies to smaller, regional manufacturers.

Regional players such as Jiangsu Langshan focus on localized offerings in the Asia Pacific. Companies are investing in advanced manufacturing technologies and corrosion-resistant coatings to enhance market share, driven by demand for high-performance ropes in the construction and energy sectors.

Industry Developments

- April 2025: WireCo introduced the CASAR LAZERLIFT, a new generation of rotation-resistant hoist ropes designed for large telescopic, crawler, and high-capacity tower cranes. These ropes offer superior spooling behavior and extended service life, making them ideal for demanding overhead crane operations.

- June 2024: Bridon-Bekaert introduced Dyform 36LR PI+, a compact multi-layer construction rope with an extruded plastic core, designed for high-performance lifting in renewable energy projects, strengthening its position in Europe and the Asia Pacific.

Companies Covered in Steel Wire Rope Market

- ArcelorMittal

- Bridon-Bekaert Ropes Group

- Heico Companies Metal Processing Group

- Optimus Steel

- HBIS GROUP

- KOBE STEEL

- WireCo World Group

- JFE Steel Corporation

- Nippon Steel Corporation

- Insteel Industries

- Others

Frequently Asked Questions

The Steel Wire Rope market is projected to reach US$14.28 Bn in 2025.

Growing infrastructure and construction activities, and expanding applications in renewable energy are the key market drivers.

The Steel Wire Rope market is poised to witness a CAGR of 3.2% from 2025 to 2032.

The rising demand in the renewable energy and electric vehicle sectors is the key market opportunity.

ArcelorMittal, Bridon-Bekaert, WireCo WorldGroup, and Nippon Steel Corporation are key market players.