- Medical Devices

- Spinal Cord Stimulators (SCS) Market

Spinal Cord Stimulators (SCS) Market Size, Share, and Growth Forecast, 2026 - 2033

Spinal Cord Stimulators (SCS) Market by Waveform (Conventional/Tonic, High-Frequency (10 kHz), Burst Stimulation, Closed-Loop/ECAP-Controlled, Hybrid Platforms), Power Source (Rechargeable Implantable Pulse Generators (IPGs), Non-Rechargeable IPGs, DRG Systems, External/Trial Stimulator Systems), Clinical Indication (FBSS, Complex Regional Pain Syndrome (CRPS), Painful Diabetic Neuropathy (PDN), Ischemic Limb Pain/Peripheral Vascular Disease, Cancer-Related Pain, Chronic Musculoskeletal & Mixed Neuropathic Pain), and Regional Analysis for 2026 - 2033

Spinal Cord Stimulators (SCS) Market Share and Trends Analysis

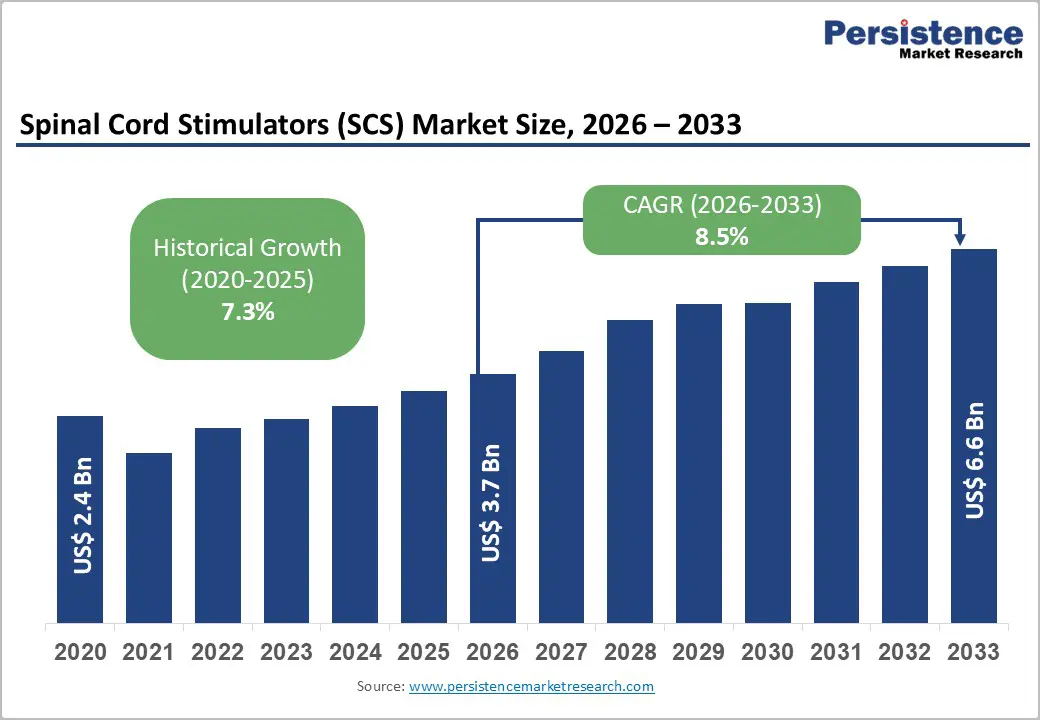

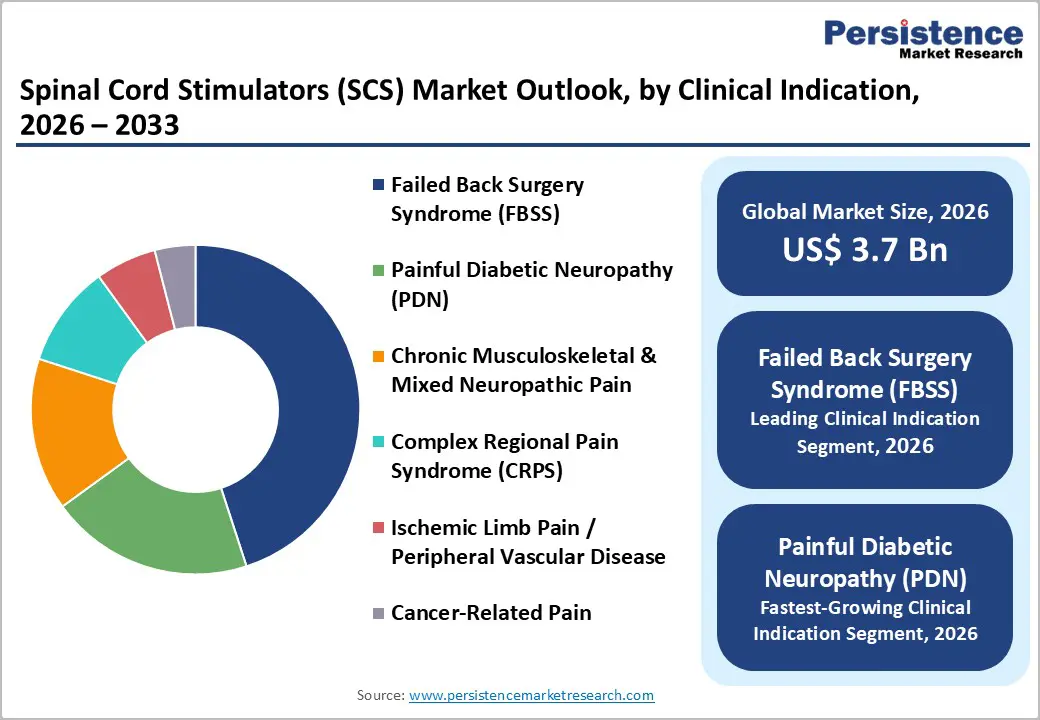

The global spinal cord stimulators (SCS) market size is likely to be valued at US$ 3.7 billion in 2026, and is projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 8.6% during the forecast period 2026 - 2033. Market expansion is fueled by differentiated technology, expanding reimbursement for neuropathic pain, and population aging across member countries of the Organization for Economic Co-operation and Development (OECD) and key emerging economies.

Adoption of high-frequency stimulation and closed-loop systems is strengthening pricing resilience, while new indications such as painful diabetic neuropathy (PDN) are widening the eligible patient base. Implantation volumes are also rising as procedures are shifting toward ambulatory surgical centers, which are improving cost efficiency and procedural throughput. Chronic pain continues to affect nearly 20% of adults worldwide, and neuropathic pain accounts for roughly 7-10% of the population in developed markets. Aging demographics are increasing the incidence of degenerative spine disorders and diabetes-related nerve damage, directly expanding the candidate pool for implantable neuromodulation.

Regulatory authorities are approving broader magnetic resonance imaging (MRI) compatibility and feedback-controlled stimulation technologies, which are enhancing physician confidence and refining patient selection. Health systems are prioritizing value-based pain management and opioid-sparing strategies, and this shift is positioning SCS as a durable therapy with measurable long-term economic value. Capital allocation is concentrating on waveform development, digital integration, and outpatient infrastructure. Competitive concentration remains high, with the four largest manufacturers accounting for more than 80% of global revenue, reinforcing scale advantages in research, regulatory compliance, and distribution.

Key Industry Highlights

- Leading Clinical Indication: Failed back surgery syndrome (FBSS) is anticipated to represent nearly 45% of global revenues in 2026, underpinned by established reimbursement pathways and long-standing clinical evidence.

- Fastest-growing Clinical Indication: Painful diabetic neuropathy (PDN) is set to record the highest 2026-2033 CAGR of nearly 12%, supported by rising global diabetes prevalence.

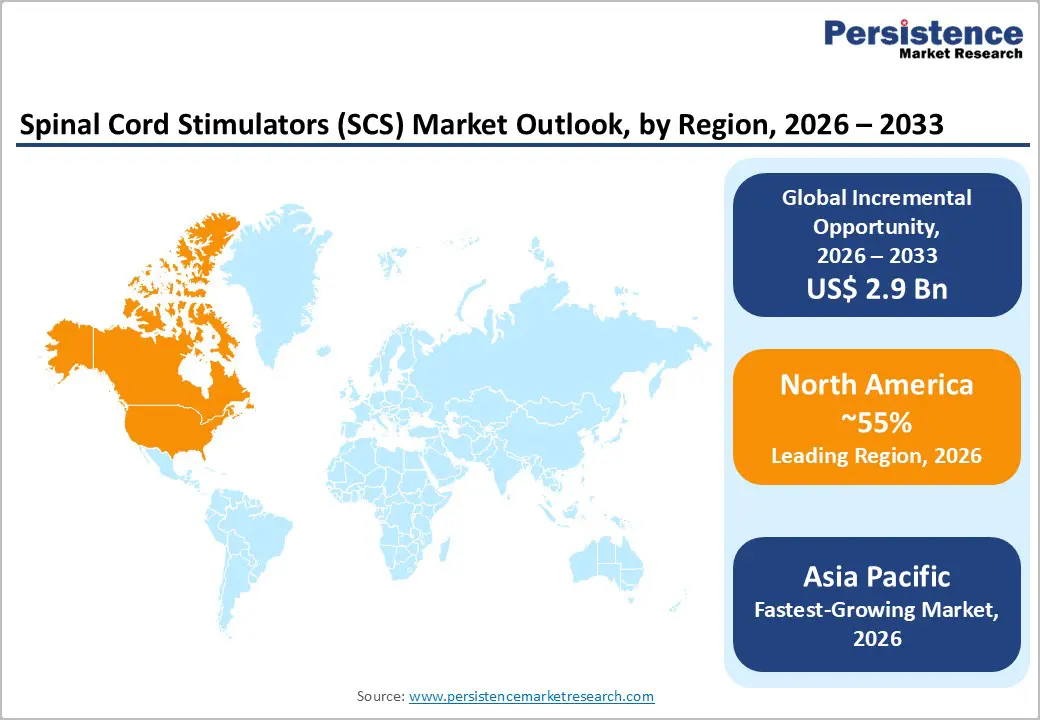

- Regional Dominance: North America is projected to hold an estimated 55% of the SCS market share in 2026, owing to comprehensive reimbursement coverage and mature implantation infrastructure.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market through 2033, with a projected CAGR of 11%, powered by increasing diabetes burden and private hospital expansion.

- Dominant Waveform: High-frequency spinal cord stimulators are expected to account for approximately 38% of market revenues in 2026, reflecting strong clinical adoption in neuropathic pain and sustained premium pricing.

- Fastest-growing Waveform: Closed-loop (ECAP-controlled) platforms are projected to expand at the highest CAGR of about 11% during 2026–2033, driven by outcome consistency and real-time feedback modulation.

- June 2025: Researchers at Chalmers University of Technology and the University of Auckland developed an ultra-thin electrical implant that delivers controlled stimulation directly at the spinal cord injury site and has shown improved locomotion and sensation recovery in preclinical models.

| Key Insights | Details |

|---|---|

|

Spinal Cord Stimulators (SCS) Market Size (2026E) |

US$ 3.7 Bn |

|

Market Value Forecast (2033F) |

US$ 6.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Reimbursed Neuropathic Indications

Regulators and public payers are recognizing spinal cord stimulation as a cost-offset intervention for refractory neuropathic pain. The Centers for Medicare and Medicaid Services (CMS) in the United States are expanding coverage criteria for chronic intractable pain, while European Health Technology Assessment (HTA) agencies are tightening reimbursement decisions around cost-utility benchmarks. These policy shifts are increasing the visibility of neuromodulation within structured pain management pathways.

Painful diabetic neuropathy is becoming a central growth catalyst as diabetes prevalence exceeds 10% across several developed economies. Clinical data indicate that up to half of long-standing diabetic patients develop neuropathy, creating a sizable population with persistent symptoms despite pharmacologic therapy. This epidemiological base is strengthening the economic rationale for durable implantable therapies that reduce the need for recurrent treatment cycles.

Healthcare systems are also quantifying the financial burden associated with opioid dependence, emergency admissions, and long-term disability. Governments are funding opioid reduction frameworks and encouraging alternatives that demonstrate sustained outcomes. Payers are modeling lifetime cost scenarios and are increasingly valuing reductions in hospital utilization, medication consumption, and productivity losses.

In response, manufacturers are designing trials that measure quality-adjusted life years (QALYs) and healthcare resource utilization endpoints rather than only short-term pain scores. This evidence alignment is expanding reimbursement confidence and widening the pool of eligible patients.

Convergence of High-Frequency and Closed-Loop Systems

High-frequency stimulation at 10 kilohertz and evoked compound action potential (ECAP)-based closed-loop systems are redefining therapeutic precision in SCS. Closed-loop platforms are continuously adjusting output amplitude in response to real-time spinal cord feedback, which is stabilizing neural activation despite posture changes and physiological variability. Clinical studies report higher responder rates in selected neuropathic cohorts than with conventional tonic stimulation.

This shift toward feedback-controlled modulation is strengthening outcome predictability and reducing the variability that has historically limited broader payer confidence. As evidence continues to accumulate, physicians are refining patient selection protocols and are increasingly incorporating waveform selection into individualized treatment planning.

Digital integration is accelerating this transition. Remote programming tools are reducing the need for frequent in-person adjustments and are easing operational burden on pain clinics. The migration of implantation procedures to ambulatory surgical centers is lowering total procedural costs by an estimated 15-25% compared with inpatient hospital settings, improving economic feasibility for both providers and payers. Manufacturers are investing in multi-waveform platforms that allow clinicians to switch between stimulation paradigms within a single device. This programmable flexibility is expanding therapy customization and is enabling more precise titration over time. Technology differentiation therefore sustains premium pricing structures and limits commoditization pressure in a market where hardware performance and clinical evidence remain key competitive variables.

High Upfront Device and Procedure Cost

Total implantation cost per patient usually ranges from approximately US$ 30,000 to US$ 60,000 in most developed healthcare systems. Although long-term cost-effectiveness analyses are demonstrating reductions in medication use, hospital visits, and indirect productivity losses, the initial capital requirement remains substantial. Public hospitals and payer-funded systems are evaluating large device expenditures within fixed annual budgets, which is slowing approval cycles. In several European countries, reimbursement negotiations are extending procurement timelines as authorities are reassessing cost-utility thresholds. This capital intensity is limiting faster penetration in publicly funded systems where expenditure controls are tightening.

Hospital administrators are applying stricter purchasing scrutiny as value-based reimbursement frameworks are expanding. These frameworks require robust real-world evidence, which is increasing post-market surveillance and registry costs for manufacturers. Companies are investing more in health economics and outcomes research to justify pricing decisions, thereby increasing overall commercialization expenditures. In emerging markets, limited insurance coverage and high out-of-pocket costs further restrict access. Without structured financing mechanisms, installment-based payment models, or bundled reimbursement pathways, adoption outside North America and Western Europe is progressing gradually.

Clinical Variability and Explant Rates

Patient response variability continues to challenge the growth of the spinal cord stimulators market. Non-responder rates are estimated at approximately 20-30%, depending on the clinical indication and patient selection criteria. In certain cohorts, explantation rates are approaching 10-15% within five years of implantation, often due to inadequate pain relief or complications. These outcome variations are increasing payer scrutiny and reinforcing the demand for measurable, long-term effectiveness data. Health technology assessment bodies and private insurers are closely examining the durability of response before approving broader coverage expansions. As reimbursement models shift toward performance-based evaluation, variability in therapeutic response is becoming a central risk factor in economic assessments.

Patient selection protocols are becoming more refined, yet referral pathways remain inconsistent across geographies. Awareness among primary care physicians and general practitioners is uneven, limiting early identification of eligible candidates. Procedural expertise also varies by center, and operator proficiency directly influences clinical outcomes. Training requirements for neuromodulation implantation are substantial, which is raising entry barriers for new implanters and slowing expansion into secondary cities and emerging regions. Manufacturers are introducing predictive analytics tools and algorithm-based programming systems to improve candidate stratification and post-implant optimization. Despite these advancements, outcome predictability is still evolving and continues to influence payer confidence and provider adoption rates.

Penetration of Painful Diabetic Neuropathy in Emerging Markets

Across the Asia Pacific, diabetes prevalence has risen meteorically over the past few decades, and this epidemiological trend is reshaping the addressable market for SCS. India and China together account for more than 200 million individuals living with diabetes, and a significant proportion of long-standing patients develop neuropathic complications. As healthcare systems are strengthening chronic disease management programs, the identification of advanced neuropathic pain cases is improving. This demographic and clinical expansion is creating a structurally large patient base that remains underpenetrated relative to North America and Western Europe.

Urban private hospital networks across major cities in Asia Pacific are expanding interventional pain and neuromodulation capabilities. Southeast Asian medical tourism corridors are attracting international patients who are seeking lower procedural costs without compromising specialist expertise. Manufacturers that are introducing mid-tier rechargeable implantable pulse generators with localized pricing strategies are improving affordability while preserving margin discipline. Structured physician training initiatives are increasing procedural competence, and targeted payer education programs are supporting reimbursement decisions.

Digital Health Integration and Remote Monitoring Revenue Streams

Remote programming and data-driven therapy optimization are expanding the economic profile of spinal cord stimulation beyond a single procedural event. Cloud-enabled platforms are enabling continuous patient monitoring and longitudinal outcome tracking. As healthcare systems are formalizing telehealth reimbursement pathways, neuromodulation providers are integrating remote diagnostics into standard care protocols. Clinicians are adjusting stimulation parameters without requiring frequent in-clinic visits, which is improving workflow efficiency and patient convenience. This digital capability is strengthening long-term engagement between manufacturers, providers, and patients while supporting more consistent therapy management.

Subscription-based remote monitoring models are creating incremental, high-margin revenue streams layered on top of device sales. Continuous device telemetry is supporting predictive maintenance, earlier detection of performance deviations, and more precise therapy adjustments. Manufacturers that are embedding artificial intelligence-assisted titration tools are enhancing clinical differentiation by reducing manual programming variability. These software-enabled capabilities are also improving the generation of real-world evidence, which supports payer negotiations and value-based contracts. As this technological convergence is advancing, the SCS market is transitioning from a predominantly hardware-driven model toward an integrated hardware and software ecosystem with recurring revenue characteristics and higher lifetime customer value.

Category-wise Analysis

Waveform Insights

High-frequency stimulation at 10 kilohertz is expected to lead in 2026, accounting for approximately 38% of the spinal cord stimulators market revenue share. These systems deliver paresthesia-free pain relief, and clinical studies demonstrate stronger outcomes in selected neuropathic pain populations compared with conventional tonic stimulation.

Physicians are increasingly selecting high-frequency platforms because they improve patient comfort and reduce the need for repeated parameter adjustments. Premium pricing structures are sustaining revenue leadership, as payers are recognizing durable response rates in specific indications such as painful diabetic neuropathy and persistent spinal pain syndrome. Adoption is also expanding within ambulatory surgical centers, where streamlined programming protocols and shorter optimization cycles are supporting operational efficiency.

Closed-loop systems are poised to become the fastest-growing waveform between 2026 and 2033. These platforms use ECAP feedback to continuously adjust stimulation intensity in response to physiological changes. Hospitals and specialist centers are prioritizing technologies that demonstrate consistent, measurable outcomes, particularly in value-based reimbursement environments. Regulatory approvals are expanding into additional markets, widening geographic access. Manufacturers are investing in algorithm refinement, data analytics, and clinician training to improve therapeutic predictability. As evidence accumulates and payer confidence strengthens, closed-loop stimulation is differentiating itself through performance stability and long-term economic value.

Clinical Indication Insights

Failed back surgery syndrome, also referred to as persistent spinal pain syndrome, is likely to dominate by capturing approximately 45% of the SCS market revenue share in 2026. This indication has an established reimbursement framework across North America and Western Europe, which is sustaining procedural stability. Clinical evidence supporting SCS in post-surgical refractory pain has accumulated over decades, reinforcing physician confidence. Referral pathways between spine surgeons and pain specialists are well developed, which ensures consistent patient flow. Hospitals are continuing to prioritize FBSS candidates because outcomes are more predictable relative to newer indications. As a result, this segment is generating steady implantation volumes and maintaining its dominant contribution to overall revenue.

Painful diabetic neuropathy is slated to register the highest 2026-2033 CAGR of around 12%. Global diabetes prevalence is rising, particularly in Asia Pacific and parts of the Middle East. A significant proportion of long-standing diabetic patients develop neuropathic complications that remain inadequately controlled by pharmacologic therapy. Clinical trials are increasingly demonstrating the benefit of neuromodulation in refractory PDN populations. Payers are evaluating long-term economic impact and are recognizing reductions in medication use and healthcare resource consumption. As awareness among endocrinologists and pain specialists continues to expand, referral volumes for PDN candidates are increasing, which is accelerating adoption across multiple regions.

Regional Insights

North America Spinal Cord Stimulators (SCS) Market Trends

North America is anticipated to command an estimated 55% of the spinal cord stimulation market share in 2026. The U.S. dominate regional sales, supported by mature reimbursement pathways and a well-established neuromodulation infrastructure. Coverage stability under the CMS and alignment with major private insurers are sustaining predictable procedural volumes. The region has developed a dense network of trained implanters, ambulatory surgical centers, and tertiary hospitals, which is enabling efficient patient throughput and technology diffusion. High awareness among pain specialists and spine surgeons is further reinforcing consistent adoption.

Migration of implantation procedures toward ambulatory surgical centers is reducing overall treatment costs and improving facility utilization. This shift is supporting margin stability for providers while maintaining payer confidence. Competitive concentration remains elevated, with leading manufacturers investing heavily in waveform innovation and digital connectivity to preserve share. Product launch cycles are shorter in the United States relative to most other regions, which is accelerating uptake of high-frequency and closed-loop platforms. Companies that are prioritizing clinical education, health economics data generation, and real-world outcome registries are strengthening their position in this performance-driven and reimbursement-sensitive market environment.

Europe Spinal Cord Stimulators (SCS) Market Trends

Europe is expected to hold about 25% of the SCS market value in 2026. Western Europe is contributing the majority of regional demand, with Germany, the United Kingdom, and France leading procedural volumes. Structured HTA processes are shaping reimbursement decisions and enforcing pricing discipline across national health systems. Public procurement models are requiring strong cost-utility evidence, which is influencing market access timelines and contract negotiations. As a result, growth is progressing at a measured pace compared with North America, where reimbursement decisions are often decentralized.

Budgetary constraints within publicly funded healthcare systems are moderating rapid expansion, yet demographic and policy factors are supporting sustained demand. Aging populations are increasing the prevalence of degenerative spine conditions and neuropathic pain syndromes. Several European governments are implementing opioid reduction strategies, which are encouraging the adoption of non-pharmacologic interventions such as neuromodulation. Clinical centers of excellence are expanding implantation capacity, particularly in Germany and the Nordic region. Manufacturers that are engaging early with HTA agencies, generating robust real-world evidence, and aligning pricing models with national cost-effectiveness thresholds are strengthening their long-term positioning across this regulated and outcomes-driven environment.

Asia Pacific Spinal Cord Stimulators (SCS) Market Trends

The Asia Pacific market is projected to expand at a CAGR of about 11% through 2033, making it the fastest-growing market for spinal cord stimulators. Rising diabetes prevalence across large population centers is increasing the incidence of painful diabetic neuropathy and other chronic neuropathic conditions. Private hospital networks are expanding interventional pain management capabilities, particularly in metropolitan areas. Japan and Australia are functioning as mature neuromodulation markets with stable reimbursement pathways and established specialist infrastructure. In contrast, China and India are scaling more gradually due to variability in insurance coverage and regional reimbursement policies.

Regulatory harmonization initiatives are streamlining device approval processes in several countries, which is reducing time to market for advanced waveform systems. Governments are modernizing medical device evaluation frameworks and strengthening post-market surveillance standards, which is improving clinical confidence. Investment in physician training programs and international collaboration with experienced centers is expanding procedural expertise. Market stakeholders operating in the region are devising pricing structures to local income levels and partnering with private insurers to gain wider access to patients and healthcare facilities.

Competitive Landscape

The global spinal cord stimulators market structure is highly consolidated, with Medtronic, Boston Scientific, Abbott, and Nevro collectively controlling approximately 80-85% of total revenue. Competitive dynamics are centered on technology differentiation rather than price-based competition. Innovation is focusing on waveform advancement such as high-frequency and closed-loop stimulation, expanded magnetic resonance imaging compatibility, and integrated digital connectivity. These performance attributes are shaping purchasing decisions in both hospital and ambulatory surgical center settings. This concentration is reinforcing scale advantages in research investment, regulatory compliance, global distribution, and clinical education.

Barriers to entry remain substantial. Regulatory approval processes are demanding robust clinical evidence, particularly for novel waveform technologies and expanded indications. Post-market surveillance obligations are increasing development timelines and compliance costs. Physician training requirements and established referral networks are creating ecosystem-based competitive advantages that are difficult to replicate quickly. Capital intensity in manufacturing, quality systems, and reimbursement support infrastructure further limits new entry. Merger and acquisition (M&A) activity is primarily targeting specialized neuromodulation technologies, digital platforms, and niche innovation capabilities rather than broad consolidation plays. As outcome-based reimbursement models continue evolving, competition is increasingly defined by clinical durability, health economic data strength, and long-term service integration rather than device hardware alone.

Key Industry Developments

- In November 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance for expanded home use of Onward Medical’s ARC-EX SCS, allowing adults with chronic, incomplete spinal cord injury to use the non-invasive device outside clinical settings to improve hand strength and sensation. This marks a significant expansion of the therapy’s indication beyond clinics to patient homes, enlarging the market opportunity and offering greater access to rehabilitative stimulation for individuals with long-term neurological deficits.

- In September 2025, the ImPRESS trial under the Royal National Orthopaedic Hospital in the U.K. began implanting spinal cord stimulation and nerve stimulation devices in people with paralysis to evaluate whether targeted electrical stimulation can improve bladder and bowel control, addressing persistent dysfunction that affects quality of life for many spinal cord injury patients. The hospital plans to recruit additional subjects, with results expected in 2027, marking a potential expansion of neuromodulation beyond pain management into restorative functional applications.

- In April 2025, Abbott introduced a new delivery system designed to streamline electrode placement during dorsal root ganglion (DRG) stimulator implantation, aiming to improve procedural efficiency and lead positioning accuracy. This innovation supports shorter operative times and may enhance overall clinical workflow for complex peripheral target stimulation.

Companies Covered in Spinal Cord Stimulators (SCS) Market

- Medtronic plc

- Boston Scientific Corporation

- Abbott Laboratories

- Nevro Corp.

- Saluda Medical Pty Ltd

- LivaNova PLC

- Nalu Medical, Inc.

- Mainstay Medical Holdings plc

- Biotronik SE & Co. KG

- Aleva Neurotherapeutics SA

- Stimwave Technologies Incorporated

- Synapse Biomedical Inc.

- Beijing PINS Medical Co., Ltd.

- MicroPort Scientific Corporation

Frequently Asked Questions

The global spinal cord stimulators (SCS) market is projected to reach US$ 3.7 billion in 2026.

Population aging across member countries of OECD economies, widening adoption of high-frequency stimulation and closed-loop systems, emergence of new indications such as PDN, and heightening prevalence of chronic pain worldwide are driving the market.

The market is poised to witness a CAGR of 8.6% from 2026 to 2033.

Approval by regulatory authorities of broader MRI compatibility and feedback-controlled stimulation technologies and prioritization of value-based pain management and opioid-sparing strategies by health systems are unlocking lucrative opportunities.

Medtronic, Boston Scientific Corporation, Abbott Laboratories, Nevro Corp., and Saluda Medical are some of the key players in the market.