- Medical Devices

- Global Spinal Stenosis Implant Market

Global Spinal Stenosis Implant Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Spinal Stenosis Implant Market by Product (Fusion Implants, Interspinous Spacers, Motion-Preservation Devices, and Spinal Stimulators & Bone Growth Devices), by Application (Cervical, Lumbar, and Thoracic), by End User (Hospitals, Specialty Clinics, and Ambulatory Surgical Center), and Regional Analysis from 2026 to 2033.

Spinal Stenosis Implant Market Share and Trend Analysis

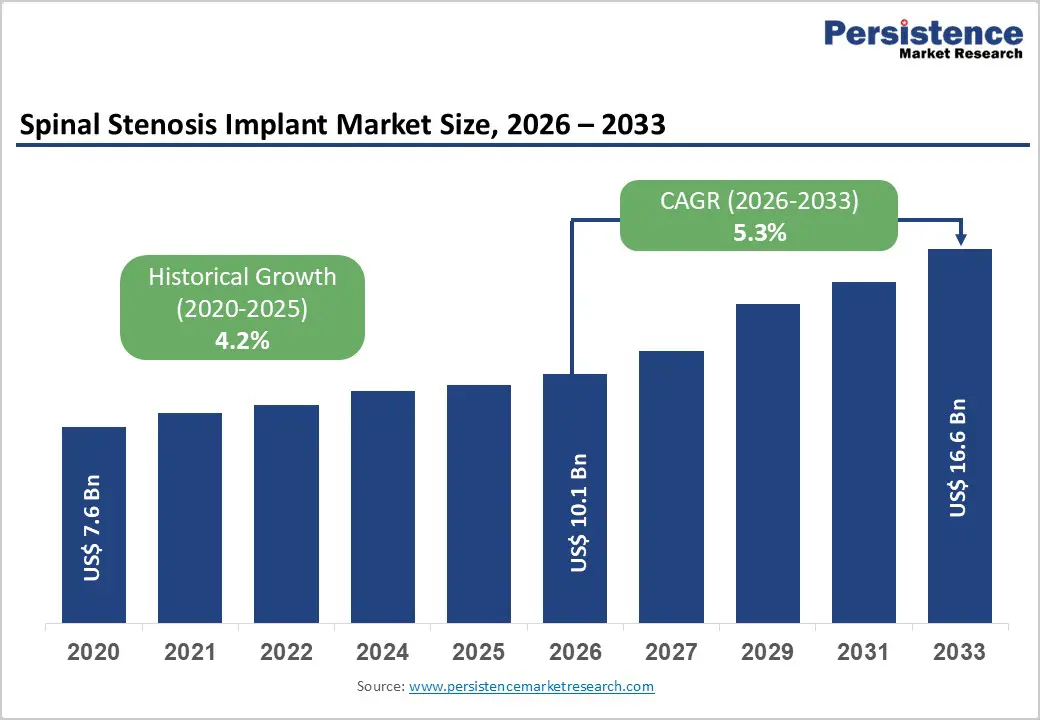

The global spinal stenosis implant market size is estimated to grow from US$ 10.1 Bn in 2026 to US$ 16.6 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for spinal stenosis implants is increasing steadily, driven by the rising prevalence of degenerative spine disorders affecting the cervical, lumbar, and thoracic regions. Aging populations, longer life expectancy, sedentary lifestyles, and increasing incidence of osteoarthritis, disc degeneration, and spinal instability are expanding the patient pool requiring surgical intervention. Spinal stenosis implants are widely used across hospitals, specialty spine centers, and ambulatory surgical facilities to restore spinal stability, relieve neural compression, and improve functional mobility through both open and minimally invasive procedures. Growing preference for surgical solutions that offer durable pain relief, improved neurological outcomes, and faster recovery is accelerating adoption. Increased awareness of early diagnosis, improved access to advanced imaging, and rising acceptance of minimally invasive spine surgery further support demand. Technological advancements such as improved biomaterials, enhanced fixation systems, motion-preservation designs, and navigation-assisted implantation are improving clinical outcomes and procedural efficiency. Additionally, strengthening healthcare infrastructure in emerging markets and rising investments in orthopedic and spine care services are reinforcing long-term global demand for spinal stenosis implants.

Key Industry Highlights

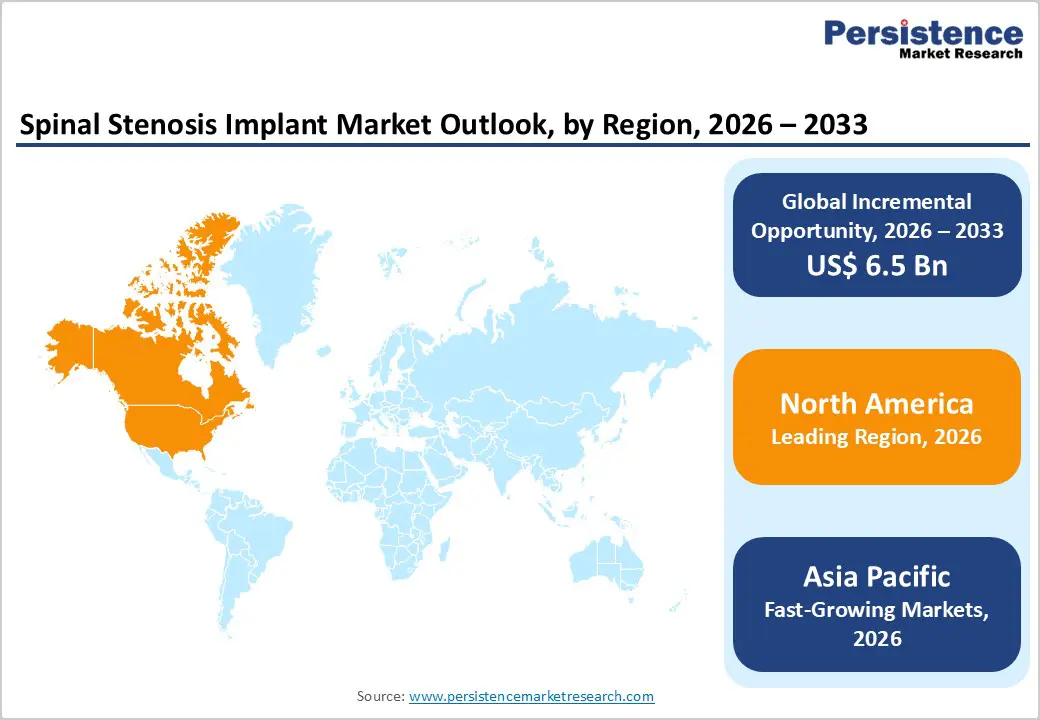

- Leading Region: North America holds the largest share at 47.3%, supported by advanced spine care infrastructure, high diagnosis rates of degenerative spinal disorders, strong hospital procurement systems, and widespread adoption of technologically advanced spinal implants.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to improving healthcare access, rising burden of spinal degenerative diseases, aging populations, expansion of private hospitals, and growing medical tourism for orthopedic and spine procedures.

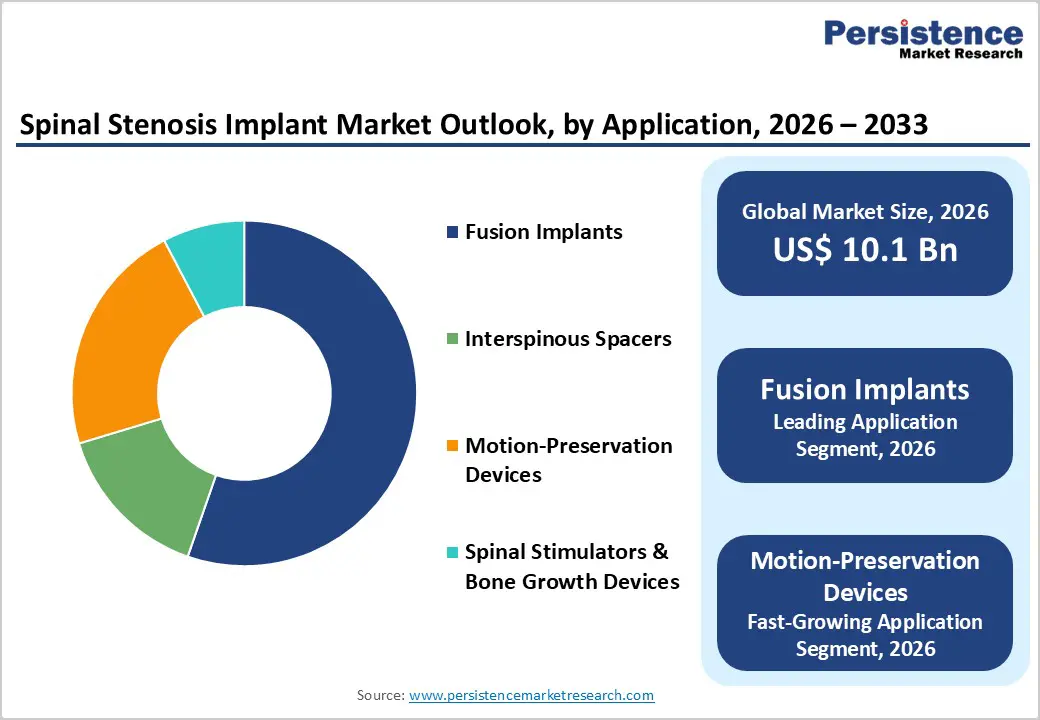

- Leading Product Segment: Fusion implants dominate the market due to high clinical utilization in moderate to severe spinal stenosis cases, proven long-term outcomes, and strong surgeon reliance on fusion-based stabilization procedures.

- Fastest-Growing Product Segment: Motion-preservation devices are growing rapidly as minimally invasive spine surgeries increase and treatment paradigms shift toward preserving spinal mobility while reducing adjacent segment degeneration.

- Leading End User Segment: Hospitals remain the top segment, driven by high surgical volumes, availability of specialized spine surgeons, and management of complex and multilevel spinal stenosis cases.

- Fastest-Growing End User Segment: Ambulatory surgical centers are scaling quickly as minimally invasive spine procedures move toward outpatient settings with shorter hospital stays and lower overall treatment costs.

| Key Insights | Details |

|---|---|

|

Spinal Stenosis Implant Market Size (2026E) |

US$ 10.1 Bn |

|

Market Value Forecast (2033F) |

US$ 16.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Dynamics

Driver – Increasing Burden of Degenerative Spine Disorders and Shift Toward Surgical Intervention

Market growth is strongly supported by the rising global incidence of degenerative spinal conditions, particularly spinal stenosis, driven by aging populations and longer life expectancy. Age-related disc degeneration, facet joint hypertrophy, and ligament thickening significantly increase the prevalence of cervical and lumbar stenosis, expanding the addressable patient pool requiring surgical intervention. As symptoms progress from chronic back pain to neurological impairment, implant-based procedures become a preferred treatment option to restore spinal stability and decompress neural structures.

Advancements in spinal implant technology, including improved fusion systems and motion-preservation devices, have enhanced surgical precision and clinical outcomes, encouraging wider adoption among spine surgeons. Growing acceptance of minimally invasive spine surgery further accelerates demand, as these procedures reduce hospital stays, blood loss, and recovery time. Increasing awareness among patients regarding the benefits of early surgical management is also contributing to higher procedure volumes. In parallel, expanding access to advanced diagnostic imaging has improved detection rates, particularly in developed healthcare systems. Collectively, these factors are driving sustained growth in implant utilization across hospitals and specialized spine centers worldwide.

Restraints – High Procedure Costs, Surgical Risks, and Limited Access to Advanced Spine Care

The market expansion is constrained by the high cost associated with spinal implant procedures and related surgical care. Implant pricing, combined with operating room expenses, post-operative rehabilitation, and extended recovery periods, can limit affordability, particularly in cost-sensitive and underinsured populations. Surgical risks such as infection, implant failure, adjacent segment degeneration, and revision surgery concerns may also affect patient and physician decision-making.

Variability in surgical outcomes based on surgeon expertise and hospital infrastructure further impacts adoption, especially in regions with limited access to specialized spine surgeons. In low- and middle-income countries, shortages of trained professionals and advanced surgical facilities restrict procedural volumes. Additionally, stringent regulatory requirements for implant approval, clinical validation, and material compliance increase development costs and time-to-market for manufacturers. Conservative treatment approaches, including physical therapy and pain management, may delay or reduce surgical intervention in early-stage patients. Together, these challenges can slow market penetration and limit growth potential in certain regions and patient segments.

Opportunity – Expansion of Minimally Invasive Spine Surgery and Growth in Emerging Healthcare Markets

Significant growth opportunities are emerging from the rapid adoption of minimally invasive spine surgery techniques and expanding healthcare infrastructure in emerging economies. Surgeons increasingly favor implants compatible with less invasive approaches due to benefits such as reduced tissue disruption, faster recovery, and lower complication rates. This shift is creating strong demand for next-generation fusion systems and motion-preservation implants optimized for precision-guided procedures.

Emerging markets across Asia Pacific, Latin America, and the Middle East present substantial untapped potential as investments in hospitals, specialty spine centers, and surgical training programs increase. Rising awareness of spinal disorders, improved access to diagnostic imaging, and growing medical tourism are further boosting procedure volumes. Technological innovation focused on lightweight materials, enhanced biomechanics, and patient-specific implant designs is improving long-term outcomes and broadening clinical indications. Strategic collaborations between manufacturers, hospitals, and research institutions are accelerating product adoption and surgeon education. As healthcare systems prioritize advanced musculoskeletal care, these factors are expected to unlock sustained long-term growth opportunities.

Category-wise Analysis

By Product, Fusion Implants Lead Due to Proven Clinical Outcomes and Long-Term Spinal Stability

Fusion implants are projected to dominate the global spinal stenosis implant market in 2026, accounting for a revenue share of 55.3%. Their leadership is primarily driven by strong clinical acceptance, proven long-term outcomes, and their effectiveness in stabilizing the spine following decompression procedures. Fusion implants are widely used in moderate to severe cases of spinal stenosis where structural stability and pain relief are critical. Surgeons prefer these implants due to predictable fusion rates, well-established surgical techniques, and broad compatibility with minimally invasive and open surgical approaches. Technological advancements in materials, including titanium and PEEK-based systems, have improved biomechanical performance and reduced complication rates. Additionally, increasing procedure volumes among aging populations and higher adoption in hospitals and specialty spine centers continue to support strong demand. Ongoing innovations focused on reducing surgical time, enhancing fixation strength, and improving patient recovery are expected to reinforce the dominance of fusion implants throughout the forecast period.

By Anatomical Area, Cervical Segment Leads Due to High Disease Prevalence and Early Surgical Intervention

The cervical segment is expected to dominate the global spinal stenosis implant market in 2026, capturing a revenue share of 30.0%. This leadership is driven by the high prevalence of cervical spinal stenosis, particularly among aging populations experiencing degenerative disc disease, osteophyte formation, and spinal cord compression. Cervical stenosis often presents with neurological symptoms such as numbness, weakness, and gait instability, prompting earlier diagnosis and surgical intervention compared to other anatomical regions. Implant-based surgical solutions are commonly employed to decompress neural structures while maintaining spinal alignment and mobility. Advances in cervical fusion systems and motion-preservation implants have further expanded treatment options. Growing awareness among clinicians and patients regarding early surgical management to prevent irreversible neurological damage supports consistent procedural volumes. As cervical spine conditions increasingly require timely intervention, this anatomical segment is expected to maintain its leading position in the market.

By End User, Hospitals Lead Due to High Surgical Volumes and Advanced Spine Care Infrastructure

Hospitals are projected to dominate the global spinal stenosis implant market in 2026, accounting for a revenue share of 62.1%. This dominance is attributed to high patient inflow, availability of experienced spine surgeons, and access to advanced diagnostic imaging and surgical infrastructure. Hospitals routinely manage complex spinal stenosis cases, including multilevel disease, revision surgeries, and patients with comorbidities that require comprehensive perioperative care. Strong adherence to clinical protocols, infection control standards, and post-operative rehabilitation pathways further supports consistent implant utilization. While ambulatory surgical centers and specialty clinics are expanding rapidly, hospitals continue to lead due to their ability to handle high-risk procedures and provide integrated multidisciplinary care. Increasing spinal surgery volumes among elderly populations, rising hospital-based minimally invasive spine procedures, and continued investment in advanced surgical technologies ensure sustained leadership of hospitals within the end-user landscape.

Region-wise Insights

North America Spinal Stenosis Implant Market Trends

The Europe spinal stenosis implant market is expected to grow steadily, supported by well-established healthcare systems, standardized clinical guidelines, and strong regulatory oversight. Countries such as Germany, the U.K., France, Italy, and Spain account for a significant share of regional demand due to aging demographics and increasing incidence of degenerative spinal conditions. European healthcare providers emphasize early diagnosis and evidence-based treatment, driving consistent utilization of spinal implants. Adoption of minimally invasive surgical techniques is increasing, particularly in tertiary hospitals and specialized spine centers. Strict compliance with medical device regulations encourages the use of high-quality, clinically validated implant systems.

Expansion of outpatient spine services and cross-border healthcare access further supports procedural growth. Additionally, ongoing investments in healthcare infrastructure and surgeon training programs contribute to sustained demand. These factors collectively support stable, long-term growth of the spinal stenosis implant market across Europe.

Europe Spinal Stenosis Implant Market Trends

The Europe spinal stenosis implant market is expected to grow steadily, supported by strong regulatory oversight, standardized clinical guidelines, and widespread access to urology services across countries such as Germany, the U.K., France, Italy, and Spain. The region benefits from an aging demographic profile, which is closely associated with higher prevalence of urethral strictures and lower urinary tract disorders. Public and private healthcare systems emphasize early diagnosis and minimally invasive management, driving consistent demand for urethral dilation procedures.

European healthcare providers place strong emphasis on device safety, material quality, and compliance with medical device regulations, favoring adoption of high-quality disposable and reusable dilators. Expansion of outpatient urology clinics and ambulatory surgical centers is improving procedural accessibility. Additionally, cross-border healthcare and medical tourism in select European countries are contributing to procedural volumes. These factors are expected to support sustained, long-term market growth across the region.

Asia Pacific Spinal Stenosis Implant Market Trends

The Asia Pacific spinal stenosis implant market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by improving healthcare infrastructure and rising prevalence of spinal degenerative disorders. Countries such as China, India, Japan, South Korea, and Australia are witnessing increased diagnosis rates due to better access to imaging technologies and growing awareness of spinal health.

Rapid population aging, urbanization, and lifestyle-related musculoskeletal issues are contributing to higher procedural demand. Expansion of private hospitals, specialty spine centers, and ambulatory surgical facilities is improving access to advanced spinal surgeries. The entry of regional manufacturers and availability of cost-effective implant systems are enhancing affordability in price-sensitive markets. Government initiatives aimed at strengthening surgical capacity and growing medical tourism further support market expansion. With improving clinical expertise and acceptance of implant-based spinal care, Asia Pacific is expected to emerge as the fastest-growing regional market.

Market Competitive Landscape

The global spinal stenosis implant market is highly competitive, with strong participation from companies such as B. Braun SE, BD, Cook, MED pro Medical BV, and Teleflex Inc. Abbott, Stryker, ATEC Spine, Inc, Aurora Spine, Inc, and B. Braun SE. These players leverage extensive global distribution networks, strong brand recognition, and diversified spine-focused product portfolios to address the growing demand for safe, effective, and minimally invasive solutions for spinal stenosis treatment.

Their offerings emphasize implant durability, biomechanical stability, precision engineering, patient safety, surgical ease, and compatibility across multiple clinical applications including lumbar and cervical spinal stenosis management, decompression procedures, and motion-preservation interventions. Continuous technological innovation, regulatory approvals, long-term clinical evidence, compliance with sterilization and biocompatibility standards, and adherence to international quality and manufacturing norms remain critical for sustaining competitive positioning in the global spinal stenosis implant market.

Key Industry Developments:

- In December 2025, Companion Spine LLC, a French–American spine implant specialist, announced the completion of its previously disclosed acquisition of Paradigm Spine GmbH, including its subsidiaries and all related global business operations, from Xtant™ Medical Holdings, Inc. The transaction includes the Coflex® Interlaminar Stabilization® device and the CoFix® Posterior MIS Fusion System, strengthening Companion Spine’s portfolio in motion-preservation and minimally invasive spinal fusion technologies.

- In August 2025, UC San Diego Health performed the world’s first custom anterior cervical spine surgery, utilizing a combination of artificial intelligence and 3D printing to design and manufacture a patient-specific spinal implant for use in cervical fusion surgery.

- In September 2024, Medtronic plc announced at the 39th NASS Annual Meeting in Chicago the commercial launch of new software, hardware, and imaging solutions to enhance AiBLE™, its integrated ecosystem for navigation, robotics, AI, and spine implants. The company also revealed a partnership with Siemens Healthineers to expand access to advanced pre- and post-operative imaging key milestone in expanding motion-preserving treatment options in the U.S. market.spinal stenosis and spondylolisthesis technologies for spine care.

- In July 2023, Premia Spine successfully performed the first U.S. surgical procedure using its TOPS System, a motion-preservation spinal implant, following FDA approval. The system offers patients with a non-fusion alternative for treating back and leg pain, marking a

- In July 2022, Aurora Spine Corporation announced that the FDA granted clearance for a new lumbar spinal stenosis indication for its ZIP™ family of minimally invasive spine (MIS) implants. This expanded indication adds to the device’s existing approvals for degenerative disc disease, spondylolisthesis, trauma, and tumors, enabling physicians to treat a broader patient population experiencing back and leg pain associated with spinal canal narrowing.

Companies Covered in Global Spinal Stenosis Implant Market

- Abbott

- Stryker

- ATEC Spine, Inc

- Aurora Spine, Inc

- B. Braun SE

- Boston Scientific Corporation

- Centinel Spine®, LLC

- Globus Medical

- Johnson & Johnson

- Joimax® GmbH

- Medtronic

- Orthofix Medical Inc.

- Paradigm Spine GmbH

- SpineGuard

- Others

Frequently Asked Questions

The global spinal stenosis implant market is projected to be valued at US$ 10.1 Bn in 2026.

The global spinal stenosis implant market is driven by the growing aging population and increasing prevalence of degenerative spinal disorders, advancements in minimally invasive surgical techniques and implant technologies, and rising healthcare awareness and infrastructure worldwide.

The global spinal stenosis implant market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Key opportunities include expansion into emerging healthcare markets and the development of advanced minimally invasive and AI-enabled surgical implant solutions.

Abbott, Stryker, ATEC Spine, Inc, Aurora Spine, Inc, and B. Braun SE are some of the key players in the body spinal stenosis implant market.