- Specialty & Fine Chemicals

- Specialty Chemicals Market

Specialty Chemicals Market Size, Share, and Growth Forecast, 2025 - 2032

Specialty Chemicals Market by Product Type (Agrochemicals, Dyes and Pigments, Construction Chemicals, Specialty Polymers, Textile Chemicals, Base Ingredients, Surfactants, Functional Ingredients, Water Treatment, Others), Application (Institutional & Industrial Cleaners, Rubber Processing Chemicals, Construction Chemicals, Food & Feed Additives, Cosmetic Chemicals, Oilfield Chemicals), and Regional Analysis for 2025 - 2032

Specialty Chemicals Market Size and Trends Analysis

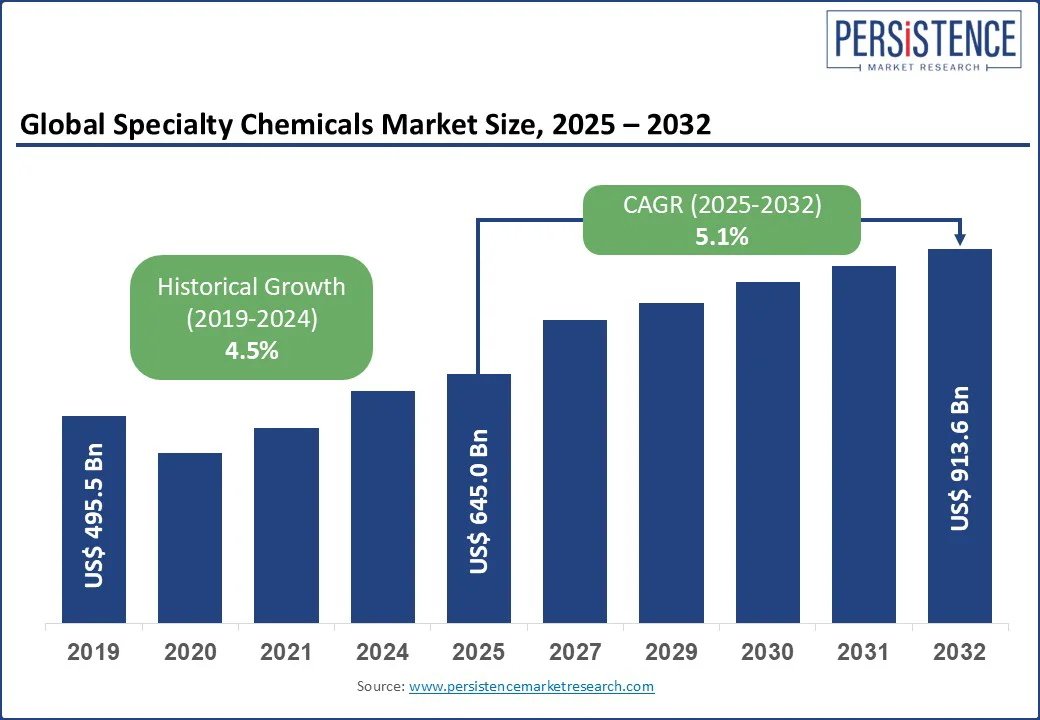

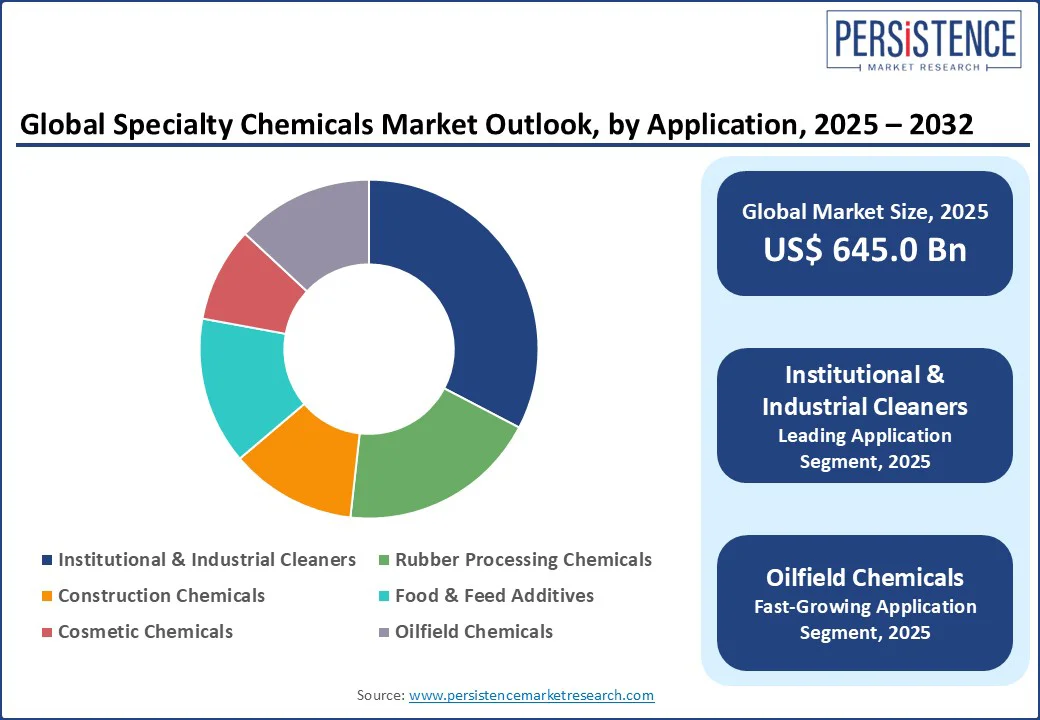

The global specialty chemicals market size is likely to be valued at US$ 645.0 Bn in 2025 and is expected to reach US$ 913.6 Bn by 2032, registering a CAGR of 5.1% during the forecast period 2025 - 2032.

The specialty chemicals market has experienced steady growth, driven by increasing demand from end-use industries such as institutional cleaning, agriculture, and automotive, advancements in sustainable technologies, and a rising focus on high-performance materials.

Key Industry Highlights:

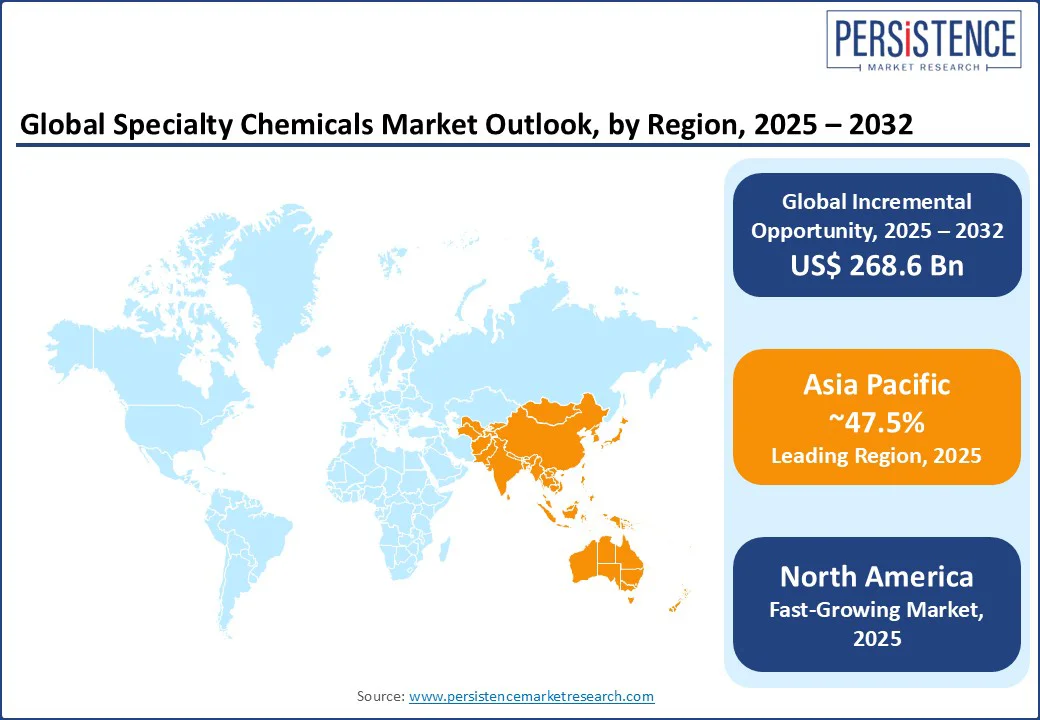

- Leading Region: Asia Pacific holds a 47.5% market share in 2025, driven by rapid industrialization, population growth, and expanding manufacturing sectors.

- Fastest-growing Region: North America, fueled by robust R&D investments, increasing demand for sustainable chemicals, and expanding industrial and healthcare sectors in the U.S.

- Dominant Product Type: Agrochemicals account for nearly 26.35% of the Specialty Chemicals market share, driven by their critical role in enhancing agricultural productivity amid global food demand.

- Leading Application Type: Institutional & Industrial Cleaners lead with a 32.5% share, reflecting high demand in healthcare, hospitality, and industrial sectors globally.

- Emerging Opportunity: The shift toward bio-based and eco-friendly chemicals is opening new avenues, with investments in green technologies boosting market expansion.

|

Global Market Attribute |

Key Insights |

|

Specialty Chemicals Market Size (2025E) |

US$ 645.0 Bn |

|

Market Value Forecast (2032F) |

US$ 913.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.5% |

Market Dynamics

Driver - Rising Demand from End-Use Industries and Technological Advancements Push Demand

The global increase in demand from key end-use industries, particularly institutional and industrial cleaning, agriculture, and automotive, is a primary driver of the specialty chemicals market. The growing global population has heightened the need for food security, with the Food and Agriculture Organization projecting a significant increase in agricultural output in the coming decades, driving demand for agrochemicals such as pesticides and fertilizers.

The institutional and industrial cleaning sector, valued at several tens of billions of U.S. dollars, is propelled by stringent hygiene standards in healthcare, hospitality, and manufacturing, necessitating advanced cleaning chemicals. In the U.S., automotive production recovery has increased demand for specialty polymers, reducing vehicle weight and enhancing fuel efficiency, as per the American Chemistry Council.

Technological advancements in sustainable formulations are accelerating market growth. For instance, Evonik’s bio-based surfactants reduce carbon emissions compared to traditional alternatives, aligning with environmental regulations and consumer preferences.

A recent study highlighted that innovative water treatment chemicals improve purification efficiency, boosting adoption in industrial applications. Nanotechnology and smart materials further enhance specialty chemicals’ use in electronics, enabling durability and miniaturization in high-tech devices.

Government initiatives supporting sustainable manufacturing drive market expansion. China’s latest Five-Year Plan promotes green chemistry, increasing access to eco-friendly cleaning and agricultural chemicals. In North America, the Inflation Reduction Act incentivizes R&D in bio-based chemicals, encouraging companies such as DuPont to innovate, thereby supporting market growth.

Restraint - Stringent Regulations and Raw Material Price Volatility Restrict Adoption

Stringent environmental regulations, such as the EU’s REACH and U.S. EPA guidelines, pose significant barriers to the specialty chemicals market, particularly in developed regions. These frameworks require extensive testing and compliance, increasing production costs and delaying product launches.

Volatility in raw material prices, especially petrochemical feedstocks affected by oil price fluctuations, further complicates market dynamics. A recent Deloitte survey reported a notable rise in raw material costs due to geopolitical tensions, impacting profitability for manufacturers in the Asia Pacific and Latin America.

The complexity of supply chains and reliance on fossil fuels also hinder growth. In resource-limited regions such as parts of Africa and rural India, high costs deter investment in advanced specialty chemicals, limiting market penetration. Additionally, the high R&D expenses for sustainable alternatives restrict expansion in developing markets, highlighting the need for cost-effective solutions.

Opportunity - Innovation in Bio-Based Products and Emerging Markets Boosts Consumption

The development of bio-based and sustainable specialty chemicals offers significant growth opportunities, particularly in institutional cleaning, textiles, and agriculture. These renewable formulations address environmental concerns and align with consumer preferences for green products.

For example, DuPont’s Sorona, a plant-based polymer, is gaining traction in apparel and automotive applications for its sustainability and performance. The rise in demand for eco-friendly cleaning chemicals, driven by post-pandemic hygiene awareness, further boosts market potential, especially in the healthcare and hospitality sectors.

Emerging markets in the Asia Pacific and Latin America present substantial growth avenues. Rapid industrialization in countries such as India and Brazil drives demand for specialty chemicals in cleaning and oilfield operations. A recent industry report noted that bio-based agrochemicals improved crop yields in pilot programs, spurring demand for innovative solutions.

Digital platforms for supply chain optimization, such as BASF’s AI-driven analytics, enhance market accessibility by reducing logistical costs in emerging markets.

Category-wise Analysis

By Product Type

The global specialty chemicals market is segmented into agrochemicals, dyes and pigments, construction chemicals, specialty polymers, textile chemicals, base ingredients, surfactants, functional ingredients, water treatment, and others.

Agrochemicals dominate, holding approximately 26.35% of the Specialty Chemicals market share in 2025, due to their critical role in boosting agricultural productivity to meet global food demand. Advanced agrochemicals, such as BASF’s targeted pesticides, are widely adopted for their efficiency.

Water Treatment is the fastest-growing segment, driven by rising demand for clean water solutions in industrial and municipal applications. Innovations in coagulants and disinfectants, such as Kemira’s advanced formulations, enhance purification processes and compliance with environmental standards, boosting adoption in high-demand regions.

By Application Type

The Specialty Chemicals market is divided into institutional & industrial cleaners, rubber processing chemicals, construction chemicals, food & feed additives, cosmetic chemicals, and oilfield chemicals. Institutional & Industrial Cleaners lead with a 32.5% share in 2025, driven by high demand in healthcare, hospitality, and manufacturing sectors, with global cleaning chemical spending exceeding US$ 50 billion annually. These chemicals ensure compliance with stringent hygiene standards, supporting their dominance.

Oilfield Chemicals are the fastest-growing segment, fueled by increasing energy exploration and recovery needs. The success of enhanced oil recovery techniques, supported by specialized surfactants and inhibitors, drives demand in advanced drilling operations, particularly in North America and the Middle East.

Regional Insights

North America Specialty Chemicals Market Trends

In North America, the U.S. holds a significant share of the global specialty chemicals market, driven by high industrial demand and advanced manufacturing infrastructure. Demand for specialty polymers and cleaning chemicals is rising, particularly in automotive and healthcare sectors, where high-performance materials and hygiene solutions are critical. Leading brands such as DuPont and Dow offer innovative solutions to meet these needs.

Consumer preferences are shifting toward sustainable and bio-based chemicals, with companies such as Huntsman incorporating AI-driven formulations to enhance efficiency and safety. Stringent EPA regulations promote the adoption of low-VOC and eco-friendly components, while R&D incentives under the Inflation Reduction Act encourage investment in advanced products, supporting market expansion.

Europe Specialty Chemicals Market Trends

Europe’s market is led by Germany, the U.K., and France, driven by regulatory support and high industrial volumes. Germany holds a significant share, supported by strong sales from brands such as BASF and Lanxess. The EU’s REACH regulation fosters innovation and compliance, encouraging the adoption of advanced surfactants and water treatment chemicals in major facilities.

In the U.K., market growth is driven by demand for sustainable cleaning and cosmetic chemicals. Products such as Croda’s bio-based ingredients are gaining popularity for their eco-friendly profiles. France is witnessing increased demand for water treatment chemicals, with companies such as Solvay offering specialized solutions. Regulatory support for sustainable manufacturing enhances market prospects across Europe.

Asia Pacific Specialty Chemicals Market Trends

Asia Pacific holds the largest share of the global specialty chemicals market, led by China, India, and Japan, and continues to be the fastest-growing region. In India, increasing agricultural requirements and supportive government initiatives, such as Make in India, are driving strong demand for cost-effective agrochemicals and cleaning chemicals, with companies such as UPL playing a dominant role.

China’s market growth is fueled by large-scale industrial expansions and a strong presence in specialty polymers, where industry leaders such as Sinopec set the pace. Japan, meanwhile, is carving a niche in high-precision specialty chemicals for electronics manufacturing, with Shin-Etsu Chemical gaining market traction.

Across the region, rising investments in infrastructure development, coupled with the rapid adoption of digital procurement platforms, are further accelerating market expansion and industry modernization.

Competitive Landscape

The global specialty chemicals market is highly competitive, with global and regional players competing on innovation, pricing, and sustainability. The rise of bio-based and high-performance chemicals intensifies competition, as companies aim to meet stringent environmental standards and industry demands. Strategic partnerships, mergers, and regulatory approvals are key differentiators.

Key Developments

- May 2025: By producing a broad variety of liquid and powder crop protection formulations, the Bharuch facility will greatly increase Safex's ability to satisfy the growing demand from India's major agricultural regions. The new capacity will add an initial production capacity of 30 MT per day for liquid formulations, scalable up to 80 MT per day. The current capacity is 23,335 MT for liquid products and 51,395 MT of total production, including liquid, powder, and granules across facilities in India.

- August 2025: Lanxess revised its 2025 profit outlook downward due to continued weak demand, supply chain disruptions, and tariff pressures, reflecting broader challenges in the European specialty chemicals sector.

Companies Covered in Specialty Chemicals Market

- Solvay

- Evonik Industries AG

- Clariant AG

- Akzo Nobel N.V.

- DuPont

- Kemira Oyj

- Lanxess

- Croda International Plc

- Huntsman International LL

- The Lubrizol Corporation

- Albemarle Corporation

Frequently Asked Questions

The specialty chemicals market is projected to reach US$ 645.0 Bn in 2025.

Rising demand from end-use industries, technological advancements, and government sustainability initiatives are the key market drivers.

The specialty chemicals market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Innovation in bio-based products and growth in emerging markets are the key market opportunities.

Solvay, Evonik Industries AG, and DuPont are among the key market players.