- Beverages

- Sparkling Tea Market

Sparkling Tea Market Size, Share, and Growth Forecast 2026 - 2033

Sparkling Tea Market by Tea Type (Green Tea, Black Tea, White Tea, Herbal Tea, Others), by Packaging (Glass Bottles, Cans, Plastic Bottles, Cartons), by Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Cafés & Restaurants), and Regional Analysis, 2026 - 2033

Sparkling Tea Market Share and Trends Analysis

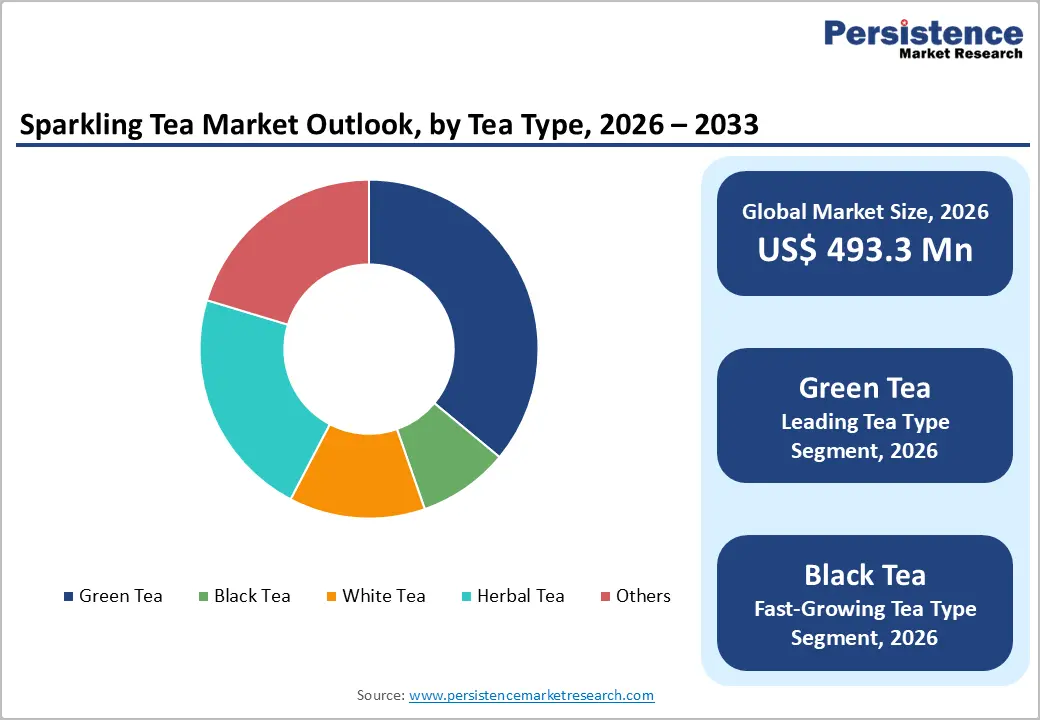

The global sparkling tea market size is expected to be valued at US$ 493.3 million in 2026 and projected to reach US$ 727.2 million by 2033, growing at a CAGR of 5.7% between 2026 and 2033. This robust growth trajectory is propelled by a rise in consumer demand for healthier, low-calorie beverage alternatives that combine the natural wellness benefits of tea with the refreshing effervescence of sparkling water.

The market expansion is underpinned by rising health consciousness, particularly among millennials and Generation Z demographics, the proliferation of ready-to-drink formats across retail channels, and heightened consumer awareness regarding the adverse health impacts of sugar-laden carbonated beverages. Sparkling tea offers a sophisticated drinking experience that retains the antioxidants, polyphenols, and natural flavors of traditional tea while providing the crisp, bubbly sensation consumers desire, positioning it as a compelling alternative to conventional sodas and energy drinks across both household and commercial consumption settings.

Key Industry Highlights:

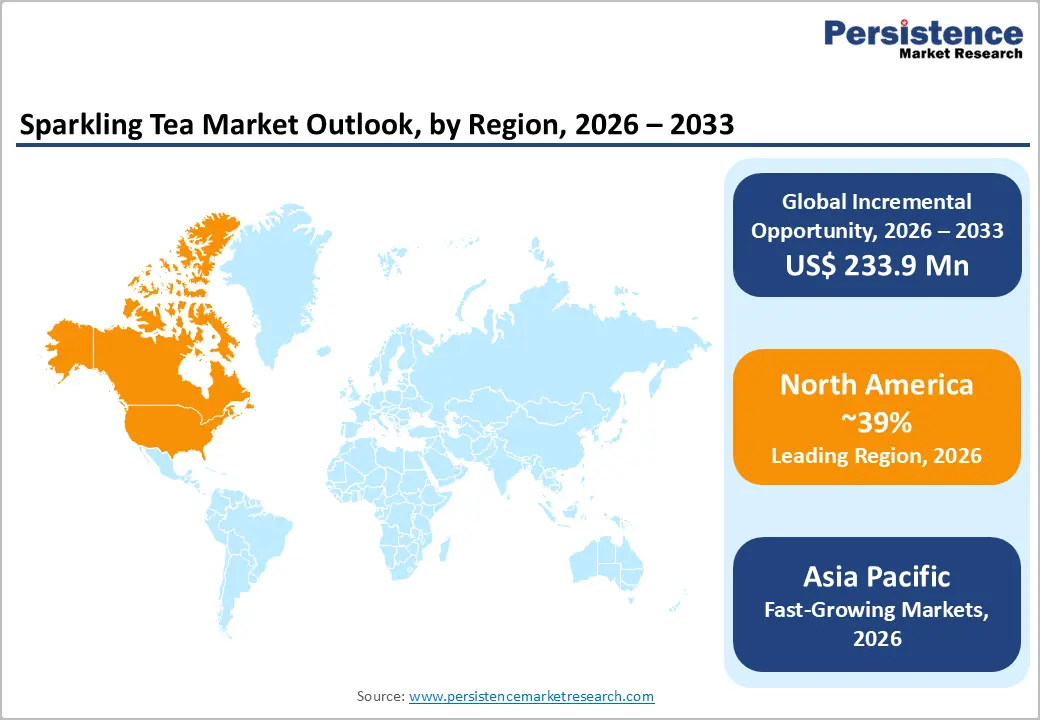

- Leading region: North America holds around 39% share of the global sparkling tea market in 2025, supported by strong health consciousness, high per capita beverage spending, and a well-developed ecosystem of supermarkets, natural food chains, and online platforms that collectively accelerate the adoption of premium non-alcoholic beverages.

- Fastest growing region: Asia Pacific is expected to register the highest growth rate through 2033, driven by large and youthful populations, rising incomes, deep-rooted tea cultures, and the strong performance of tea beverage leaders such as Nongfu Spring Co., Ltd., which demonstrate substantial demand for innovative tea-based drinks.

- Dominant segment from any category: By tea type, green tea leads with about 36% market share in 2025, benefiting from its well-established health halo, robust scientific backing around antioxidants and metabolism support, and a wide range of flavor extensions that resonate with both traditional tea drinkers and younger, trend-driven consumers.

- Fastest growing segment from any category: Black tea-based sparkling products are growing rapidly as consumers seek stronger flavor, higher natural caffeine content, and cold-brewed formats that deliver smooth, complex taste experiences, effectively bridging traditional iced tea and premium carbonated beverages.

| Key Insights | Details |

|---|---|

| Sparkling Tea Market Size (2026E) | US$ 493.3 Mn |

| Market Value Forecast (2033F) | US$ 727.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Drivers - Rising Health and Wellness Consciousness Driving Demand for Functional Beverages

The sparkling tea market is experiencing substantial momentum from the global shift toward health-conscious consumption patterns, with consumers increasingly prioritizing beverages that deliver functional benefits beyond basic hydration. Tea consumption worldwide has grown steadily, with premium and specialty tea segments recording strong growth rates as consumers seek out natural antioxidants and polyphenols. Growing concerns about obesity and diabetes linked to excessive sugar consumption, highlighted by leading health organizations, are prompting consumers to actively seek alternatives to traditional carbonated soft drinks. Sparkling tea addresses this demand by offering a naturally low-calorie option enriched with catechins and bioactive compounds found in tea leaves. Multiple clinical and epidemiological studies indicate that regular tea consumption is associated with improved cardiovascular health and metabolic function, further enhancing consumer confidence in tea-based beverages. This health-driven transition is particularly pronounced among urban, affluent consumers aged 18-45 who prioritize wellness-oriented lifestyle choices and are willing to pay premium prices for beverages perceived as healthful, natural, and functionally beneficial.

Proliferation of Ready-to-Drink Formats and Premiumization Trends

The beverage industry is witnessing a fundamental shift toward convenience-oriented ready-to-drink formats, with sparkling tea benefiting significantly from this transition. In key markets such as the U.S., ready-to-drink tea consumption has grown strongly over the past few years, reflecting changing consumer lifestyles characterized by on-the-go consumption patterns and time-constrained daily routines. The premiumization trend sweeping across the global beverage sector is particularly favorable for sparkling tea, as consumers increasingly associate sparkling formats with sophistication and quality.

Premium beverage categories have outpaced mass-market segments, with consumers demonstrating willingness to pay notable price premiums for products featuring artisanal ingredients, innovative flavor profiles, and sustainable packaging. Leading beverage manufacturers, including PepsiCo (through Lipton) and specialty brands like TÖST Beverages and Sound Sparkling Tea, are capitalizing on this trend by introducing diversified product portfolios featuring tea blends such as matcha, oolong, and hibiscus infusions combined with botanicals. This innovation pipeline, coupled with sophisticated branding and targeted marketing emphasizing authenticity and craftsmanship, is attracting discerning consumers and expanding market penetration across both retail and foodservice channels.

Restraints - High Production Costs and Premium Pricing Challenges

The sparkling tea market faces significant constraints related to elevated production costs stemming from premium ingredient sourcing, specialized processing requirements, and sophisticated packaging specifications. Unlike conventional carbonated beverages that utilize cost-effective synthetic flavorings and sweeteners, sparkling tea manufacturers often procure high-quality tea leaves from certified estates, including organic or fair-trade sources that command substantial price premiums.

Cold-brewing, fermentation, and gentle carbonation processes required to extract optimal flavor profiles and preserve delicate antioxidants necessitate longer production cycles and dedicated facilities, increasing operating expenditures. Specialty tea procurement costs have risen in recent years due to climate variability, production risks, and intensifying competition for high-grade leaves. These elevated input costs translate into retail prices that can be significantly higher than conventional carbonated soft drinks, potentially limiting market penetration among price-sensitive consumer segments and constraining volume growth in emerging markets where disposable incomes remain modest and value-oriented purchasing behavior is prevalent.

Intense Competition from Established Beverage Categories and Limited Consumer Awareness

Sparkling tea manufacturers confront formidable competition from well-entrenched beverage categories, including traditional carbonated soft drinks, energy drinks, flavored waters, and kombucha products that benefit from strong brand equity and extensive distribution networks. Major multinational corporations such as The Coca-Cola Company and PepsiCo command substantial shelf presence and marketing budgets, making it challenging for smaller sparkling tea brands to secure visibility and consumer mindshare. Consumer awareness of sparkling tea as a distinct category remains relatively low outside health-focused or trend-conscious segments, with many potential consumers unfamiliar with its taste profile, benefits, and occasions for use.

Building awareness requires sustained education, sampling, and promotional investments, which can be burdensome for emerging brands with constrained resources. Additionally, taste preferences vary widely; in traditional tea-drinking cultures, consumers may be skeptical of carbonated formats, while in markets dominated by sodas and energy drinks, sparkling tea may initially be perceived as niche or experimental, slowing category adoption.

Opportunity - Expanding Distribution Through E-Commerce and Direct-to-Consumer Channels

The rapid digitalization of retail commerce presents strong growth opportunities for sparkling tea brands to bypass some of the limitations of traditional brick-and-mortar distribution. Online beverage sales, including better-for-you and functional drinks, have grown sharply since 2020, supported by improvements in last-mile logistics and broader consumer comfort with ordering groceries online. E-commerce marketplaces and grocery delivery platforms allow sparkling tea brands to showcase full product ranges, share detailed ingredient and health information, and offer trial packs or variety bundles that encourage experimentation. Direct-to-consumer subscription models enable recurring revenue, strengthen brand-consumer relationships, and generate granular data on flavor preferences, consumption frequencies, and price sensitivity. Brands such as Minna (New Berlin Beverage Co.) and Saicho Sparkling Tea are leveraging online channels and social media campaigns to build communities around wellness, mindful drinking, and premium non-alcoholic experiences. Influencer partnerships and user-generated content on platforms like Instagram and TikTok further amplify the category’s visibility at relatively modest marketing costs compared to traditional advertising, creating a flywheel of awareness and trial that supports long-term market expansion.

Geographic Expansion in Asia Pacific Markets and Product Innovation

The Asia Pacific region represents a particularly attractive growth frontier for the sparkling tea market, combining deep-rooted tea-drinking traditions with rapidly rising disposable incomes and openness to new beverage formats. Major economies such as China, Japan, and India are experiencing robust increases in packaged tea and ready-to-drink tea sales, offering a natural springboard for sparkling tea introductions. Nongfu Spring Co., Ltd., for example, has reported strong growth in its tea beverage segment, illustrating the scale of consumer demand for innovative tea-based drinks in China. As urbanization accelerates and modern retail formats expand across Southeast Asia, more consumers encounter premium, international-style beverages in supermarkets, convenience stores, and cafés. At the same time, product innovation is enabling sparkling tea to appeal to diverse taste preferences and health priorities. Companies are experimenting with cold-brew sparkling teas, fermented styles inspired by kombucha, and blends incorporating botanicals, adaptogens, or superfruit juices. Such innovation allows brands to position products around energy, relaxation, immunity, or digestive health themes, aligning with broader functional beverage trends and opening multiple positioning platforms across price tiers and channels.

Category-wise Insights

Tea Type Insights

Green tea dominates the sparkling tea market by tea type, commanding around 36% market share in 2025, driven by strong consumer recognition of its perceived health benefits and light, refreshing taste profile that pairs well with carbonation. Green tea is naturally rich in catechins such as EGCG, which have been widely studied for potential roles in supporting cardiovascular health, metabolism, and antioxidant protection. These associations have been popularized in both scientific and mainstream media, reinforcing green tea’s reputation as a “better-for-you” base for modern ready-to-drink beverages.

Brands including Teatulia and Ito En, Ltd. have developed sparkling variants of classic and flavored green teas, ranging from matcha-based drinks to jasmine and citrus-infused options, which appeal to both traditional tea drinkers and younger consumers seeking lighter, less sweet alternatives to sodas. At the same time, black tea is emerging as the fastest-growing tea type segment in sparkling formulations, as its fuller body and higher caffeine content resonate with consumers looking for more robust flavor and a gentle energy lift, especially in cold-brewed and lightly sweetened formats that bridge the gap between iced tea and sparkling soft drinks.

Packaging Insights

Glass bottles currently lead the sparkling tea market in packaging, accounting for an estimated 42% share in 2025, reflecting their association with premium quality, purity, and sustainability. Glass is chemically inert and offers excellent barrier properties, helping preserve delicate tea flavors, aromas, and functional components without the risk of off-tastes or migration. Consumers often perceive glass-packaged beverages as higher-end and more natural, and this perception aligns well with sparkling tea’s positioning as a sophisticated, health-forward drink. Premium and heritage brands such as Fortnum & Mason, Fentimans Ltd., and TÖST Beverages rely heavily on distinctive glass bottle designs to communicate artisanal credentials and stand out on the shelf. However, aluminum cans are registering the fastest growth, driven by portability, lighter weight, rapid chilling, and high recyclability. New can launches, including TÖST Beverages’ 250 ml formats, illustrate how brands are using cans to access on-the-go occasions, outdoor events, and venues where glass is restricted. High recycling rates for aluminum in many developed markets also align cans with circular economy and sustainability narratives, which strongly influence younger consumers’ purchasing decisions.

Distribution Channel Analysis

Supermarkets and hypermarkets represent the leading distribution channel for sparkling tea, with an estimated 38% market share in 2025, supported by their scale, wide assortment, and ability to introduce new categories to mainstream consumers. Large retail chains such as Walmart, Kroger, Tesco, and Carrefour have steadily expanded shelf space for better-for-you and premium beverages, positioning sparkling tea alongside kombucha, flavored waters, and functional drinks within health-oriented or natural beverage sections. These retailers use end-cap displays, promotions, and in-store sampling to drive trial and build familiarity with sparkling tea among regular grocery shoppers.

At the same time, online retail is the fastest-growing channel, supported by grocery delivery apps, dedicated beverage e-tailers, and brand-owned online stores. Platforms such as Amazon Fresh and various regional e-commerce players offer filters for organic, low-sugar, or plant-based beverages, making it easier for health-conscious consumers to discover sparkling tea. This channel also allows for more detailed storytelling about sourcing, ingredients, and health attributes than is possible on a physical shelf, supporting premium positioning and cross-border reach for niche brands.

Regional Insights

North America Sparkling Tea Market Trends and Insights

North America holds a leading position in the global sparkling tea market with around 39% share in 2025, driven by a combination of high disposable incomes, strong health and wellness orientation, and rapid adoption of premium non-alcoholic beverages. The U.S. accounts for the bulk of regional demand, supported by well-established ready-to-drink tea and functional beverage categories. The long-standing partnership between PepsiCo and Unilever for Lipton ready-to-drink teas provides a powerful distribution backbone, while innovative niche brands such as Sound Sparkling Tea, Minna, and Brew Dr. Kombucha have successfully positioned sparkling tea as a clean-label, low-sugar, and sophisticated alternative to sodas and alcoholic drinks.

The regulatory environment, including clear labeling rules overseen by federal agencies, supports transparency around ingredients and nutrition, which is important for health-conscious shoppers. Additionally, the “sober curious” and mindful drinking movements are encouraging consumers to seek complex, adult-oriented non-alcoholic options suitable for social occasions, dinners, and celebrations. Sparkling tea fits this need by offering layered flavors and a premium feel without alcohol. Retail ecosystems in the U.S. and Canada, spanning national supermarket chains, natural and organic retailers such as Whole Foods Market and Sprouts Farmers Market, and rapidly growing online grocery platforms, give brands multiple pathways to reach target consumers. Specialty cafés and restaurants also play a role, featuring sparkling tea as an elevated non-alcoholic pairing option, which further enhances category visibility and consumer trial.

Asia Pacific Sparkling Tea Market Trends and Insights

Asia Pacific is projected to be the fastest-growing region for sparkling tea, with expected growth rates that outpace global averages over the forecast period. The region combines deep-seated cultural affinity for tea with demographic and economic trends favorable to modern beverage innovation. In China, large players such as Nongfu Spring Co., Ltd. have demonstrated the enormous potential of ready-to-drink tea and tea-based beverages, and their strong performance in tea drinks highlights the readiness of local consumers to embrace new tea formats, including sparkling variants. High urbanization, expanding middle classes, and increasingly busy lifestyles are driving demand for convenient, on-the-go beverages that still align with traditional tastes and health perceptions.

Competitive Landscape

The global sparkling tea market is moderately fragmented, with a mix of established beverage manufacturers and emerging premium brands competing for market share. Competition is driven by product innovation, clean-label formulations, organic ingredients, and unique flavor combinations. Companies are focusing on low-sugar, functional, and non-alcoholic variants to align with rising health and wellness trends. Premium packaging and positioning as an alternative to carbonated soft drinks or alcoholic beverages are key differentiation strategies. Distribution expansion through supermarkets, specialty stores, and e-commerce platforms is intensifying rivalry.

Key Market Developments

- In January 2026, Twinings added a new peach-flavoured variant called Revive to its ready-to-drink Sparkling Tea portfolio, combining green tea with peach, apple juice and elderflower, offering a low-calorie, no added sugar option to expand its functional sparkling tea range.

Companies Covered in Sparkling Tea Market

- TÖST Beverages

- Sound Sparkling Tea

- Minna (New Berlin Beverage Co.)

- Teatulia

- Brew Dr. Kombucha

- Fentimans Ltd.

- Saicho Sparkling Tea

- Nongfu Spring Co., Ltd.

- Fortnum & Mason

- PepsiCo

- Unilever (Lipton)

- Ito En, Ltd.

- Others

Frequently Asked Questions

The global sparkling tea market is expected to be valued at US$ 493.3 million in 2026 and is projected to reach US$ 727.2 million by 2033, reflecting a forecast CAGR of 5.7% during 2026-2033 as consumers increasingly shift from sugar-laden carbonated soft drinks to healthier, tea-based sparkling beverages.

Key growth drivers include rising health and wellness awareness, growing concern over sugar intake and related chronic diseases, the rapid expansion of ready-to-drink and on-the-go consumption patterns, premiumization of non-alcoholic beverages, and the influence of the “sober curious” movement, which is encouraging consumers to seek sophisticated, low- or no-alcohol alternatives such as sparkling tea.

North America currently leads the sparkling tea market, supported by high disposable incomes, strong health consciousness, advanced retail and e-commerce infrastructure, and the presence of both major beverage corporations and innovative niche brands.

The most significant opportunity lies in leveraging e-commerce and direct-to-consumer channels, along with digital marketing and subscription models, to rapidly build awareness, trial, and loyalty for sparkling tea. This is complemented by the vast untapped potential in Asia Pacific, where strong tea culture, rising incomes, and modernizing retail ecosystems create fertile ground for innovative sparkling tea offerings tailored to local tastes and health expectations.

Key players in the sparkling tea industry include global beverage leaders such as PepsiCo and Unilever (Lipton), regional powerhouses like Nongfu Spring Co., Ltd. and Ito En, Ltd., and specialized premium brands including TÖST Beverages, Sound Sparkling Tea, Minna (New Berlin Beverage Co.), Teatulia, Brew Dr. Kombucha, Fentimans Ltd., Saicho Sparkling Tea.