- Chipsets & Processors

- Smart Machines Market

Smart Machines Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Smart Machines Market by Component (Hardware, Software, Services), Machine Type (Robots, Autonomous cars, Drones, Wearable devices, Others), by Technology (Cloud Computing technology, Big Data, Internet of Everything, Robotics, Cognitive Technology, Affective Technology), Regional Analysis, 2026 - 2033

Smart Machines Market Size and Trend Analysis

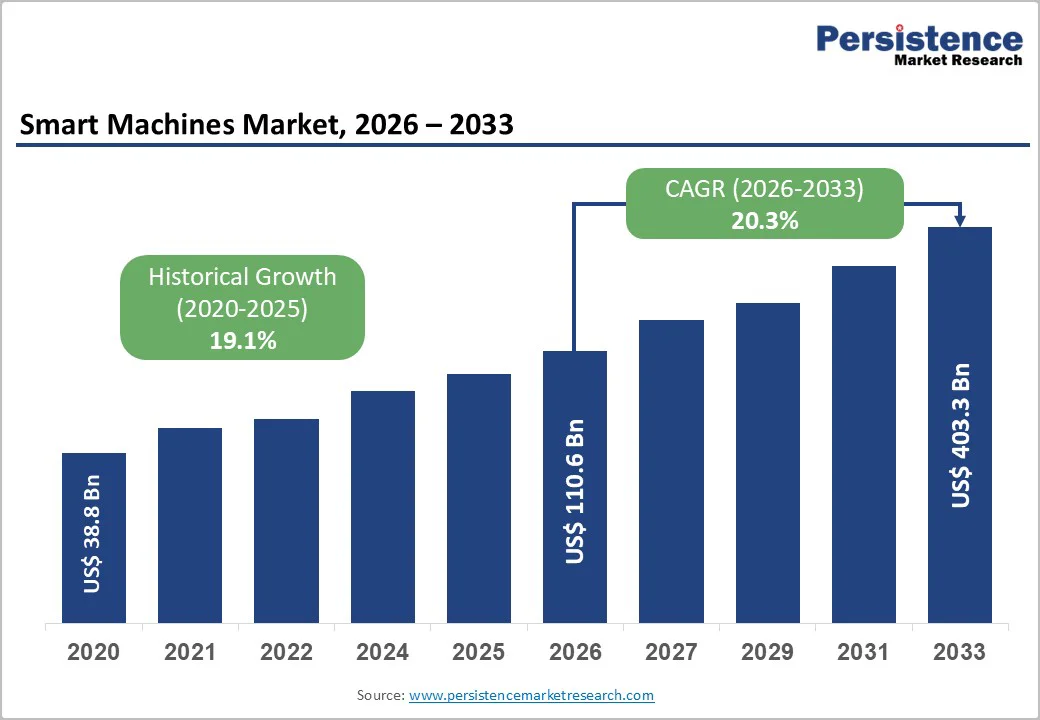

The global smart machines market size is likely to be valued at US$ 110.6 Billion in 2026 and is expected to reach US$ 403.3 Billion by 2033, growing at a CAGR of 20.3% during the forecast period from 2026 and 2033. Rapid adoption of intelligent automation across manufacturing, healthcare, and logistics drives this expansion, supported by advancements in AI, IoT, and robotics that enhance efficiency and decision-making.

Key Industry highlights

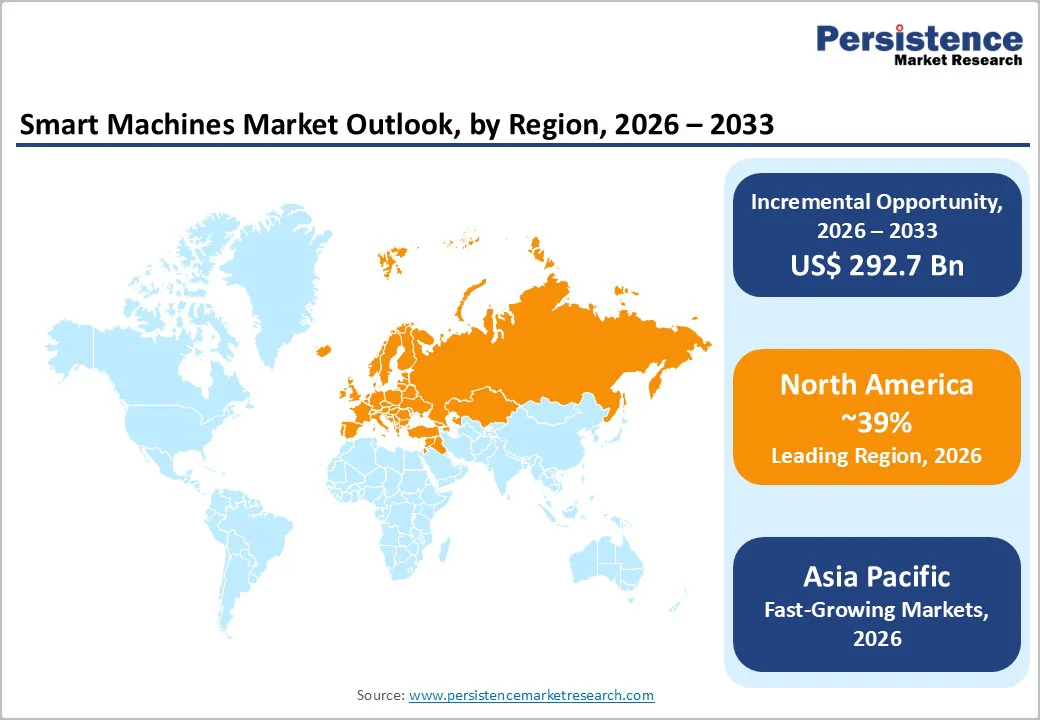

- Leading Region: North America dominates as the leading region having 41%, due to U.S. tech hubs and 14% robot order growth in automation-heavy industries.

- Fastest Growing Region: Asia Pacific emerges fastest-growing from China-Japan manufacturing boom and 15.7% smart factory expansion.

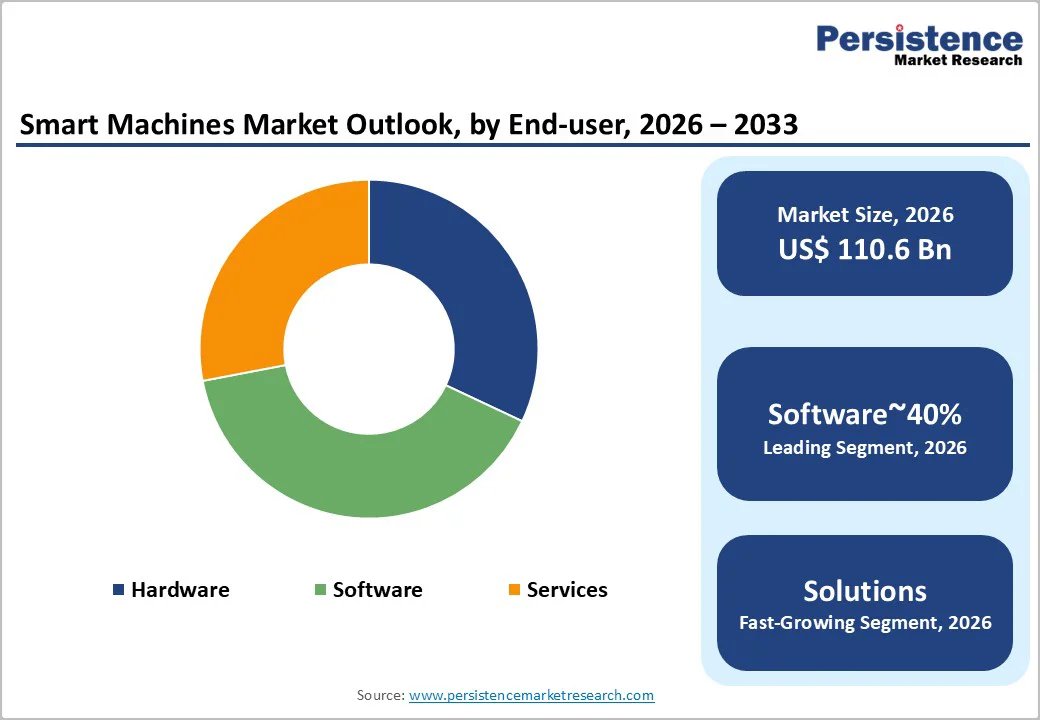

- Leading Segment: Software prevails as the dominant component for AI-driven intelligence across 40% applications.

- Fastest growing Segment: Robots grow fastest in machine type via 35% industrial flexibility and order surges.

- Key Opportunity: Healthcare robotics adoption accelerates as AI-driven systems improve clinical efficiency, reduce administrative burden, and enhance patient outcomes.

| Key Insights | Details |

|---|---|

|

Smart Machines Market Size (2026E) |

US$ 110.6 Billion |

|

Market Value Forecast (2033F) |

US$ 403.3 Billion |

|

Projected Growth CAGR(2026-2033) |

20.3% |

|

Historical Market Growth (2020-2025) |

19.1% |

Market Dynamics

Driver - Automation-driven robotics significantly improve manufacturing efficiency, reduce energy use, cut cycle times, and address persistent labor shortages

Automation in manufacturing is a major driver of the Smart Machines Market, enabling factories to perform repetitive and complex tasks with higher speed, precision, and efficiency. A strong example is ABB Limited’s announcement at the China International Industry Fair (CIIF) 2025, where it introduced the IRB 6750S shelf robot. This robot is designed for installation at elevated production-line positions and offers full vertical and horizontal motion, making it ideal for space-constrained facilities.

When powered by ABB’s OmniCore platform, the robot delivers a 20% reduction in energy consumption while achieving path accuracy of 0.9 mm and position repeatability of 0.06 mm. ABB also highlighted that integrating Automatic Path Planning Online technology can reduce cycle times by up to 50% in material handling and spot welding. In parallel, GE Appliances reported in November 2025 that automation investments enabled production of many appliances in under two labor hours, a 50% reduction compared to 25 years ago. These examples demonstrate how automation boosts throughput, offsets labor shortages, and improves overall factory productivity.

Growing Adoption of Autonomous Systems Boosts Productivity by Enabling Robots to Perform Complex Tasks with Minimal Human Intervention

Rising demand for autonomous systems is accelerating growth in the Smart Machines Market as industries increasingly deploy robots in hazardous, high-precision, and labor-intensive environments. Sectors such as logistics, agriculture, and healthcare are adopting autonomous machines to address workforce shortages while improving operational efficiency. Advances in artificial intelligence, computer vision, and sensor technologies allow robots to operate independently with minimal human supervision, driving productivity improvements of nearly 25% in several industries.

According to the International Federation of Robotics, global robot installations rebounded by 13%, supported by growing adoption in healthcare and service applications that significantly reduce response times. In March 2025, Google DeepMind launched its Gemini Robotics models, built on Gemini 2.0 with physical action capabilities. These models enable robots to perform complex, multi-step tasks such as precision packing and origami folding. Notably, the system demonstrated strong generalization across different robotic platforms, including humanoid and industrial arms, achieving two to three times higher task success rates and reinforcing the productivity benefits of autonomous systems.

Restraint - High Upfront Automation Costs Limit Smart Machine Adoption, Especially Among Small and Medium-Sized Enterprises With Constrained Capital

High initial investment costs remain a significant restraint on Smart Machines Market adoption, particularly for small and medium-sized enterprises with limited capital resources. The cost of deploying advanced automation systems includes not only robotic hardware but also software licenses, system integration, facility upgrades, and ongoing maintenance. In many cases, total implementation expenses run into several million dollars, creating a strong financial barrier for smaller firms.

As a result, many organizations prioritize short-term liquidity and operational stability over long-term efficiency gains, even though automation can improve productivity by up to 20%. The challenge is further intensified by rising interest rates and cautious capital spending environments, which make financing large technology projects more difficult. Until costs decline or financing models become more flexible, high capital requirements will continue to slow market penetration among smaller manufacturers.

Lack of Skilled Talent and Complex System Integration Slow Smart Machine Deployment And Increase Operational Disruption Risks

Skill shortages and system integration challenges present major obstacles to the widespread adoption of smart machines. Around 70% of organizations report difficulties in finding or training personnel capable of managing AI-enabled and digitally connected machinery. Advanced systems require expertise in robotics, data analytics, cloud platforms, and cybersecurity, which many traditional manufacturing workforces currently lack. In addition, integrating smart machines with legacy infrastructure often requires extensive retrofitting, software customization, and process redesign. These efforts can increase downtime by 20% during transition periods, disrupting production schedules and affecting profitability.

Cybersecurity concerns further complicate deployment, particularly in regulated industries where data protection and system reliability are critical. As factories become more connected, the risk of cyber threats increases, requiring additional investment in security frameworks and compliance measures. Together, workforce capability gaps and integration complexity raise deployment risks and costs, slowing the pace of smart machine adoption despite clear long-term efficiency and productivity benefits.

Opportunity - Healthcare Robotics Adoption Accelerates as AI-Driven Systems Improve Clinical Efficiency, Reduce Administrative Burden, and Enhance Patient Outcomes

Healthcare robotics represents a strong growth opportunity for the Smart Machines Market, driven by aging populations, workforce shortages, and the need for higher precision in clinical care. Autonomous and AI-powered systems are increasingly used in surgery, diagnostics, patient monitoring, and hospital logistics, helping improve outcomes by up to 30%. According to the Association for Advancing Automation, life sciences and healthcare-related robotics orders grew by approximately 35%, reflecting rising demand for smart medical devices.

In 2025, Microsoft expanded its Dragon Copilot AI clinical assistant in October, which introduced the first commercially available ambient experience for nursing workflows. The solution integrates trusted clinical content from partners such as Elsevier and Wolters Kluwer directly into daily operations. Microsoft also launched healthcare agent capabilities for appointment scheduling and patient triaging, significantly reducing administrative burdens. Deployed securely through Microsoft Cloud for Healthcare, the system demonstrated reductions in clinician documentation time and improved patient responsiveness by up to 87%, highlighting the transformative potential of smart machines in healthcare.

Cloud-based Platforms Enable Real-Time Analytics, Predictive Maintenance, And Scalable Intelligence Across Connected Smart Machine Ecosystems

Cloud-based smart infrastructure is creating strong growth opportunities by enabling scalable, real-time processing of vast volumes of data generated by smart machines. Cloud adoption allows manufacturers to perform advanced analytics, predictive maintenance, and remote monitoring, reducing maintenance costs by nearly 25%. In 2025, Google Cloud launched its Manufacturing Data Engine and Manufacturing Connect solutions to unify data from traditionally siloed factory systems. These platforms integrate real-time data ingestion through Pub/Sub, advanced analytics via BigQuery, and machine learning using Vertex AI, enabling manufacturers to deploy AI models in weeks rather than months.

Google Cloud also introduced machine-level anomaly detection using time-series analysis of vibration, noise, and temperature data, allowing faster identification of equipment issues. AI-powered expert assistants built on Gemini Enterprise help diagnose machine failures in minutes instead of days. Supported by partners such as Intel, C3 AI, and Splunk, these solutions bridge factory-floor and cloud environments, delivering closed-loop AI that enhances efficiency, reduces downtime, and improves decision-making across manufacturing operations.

Category-wise Insights

Component Analysis

Software leads the component segment of the Smart Machines Market, accounting for approximately 40% of total market share. This dominance is driven by software’s critical role in enabling artificial intelligence, machine learning, analytics, and autonomous decision-making. Software platforms process vast amounts of operational data, allowing smart machines to perform precision tasks, adapt to changing conditions, and optimize performance in real time. Industry analyses suggest that software powers nearly 60% of smart functionalities in modern manufacturing environments. Compared to hardware, software offers greater flexibility, scalability, and upgrade potential, making it a preferred investment for organizations seeking long-term value.

Major players such as IBM Corporation and Microsoft Corporation continue to introduce advanced AI-driven platforms that enhance system interoperability and operational intelligence. These innovations allow manufacturers to improve efficiency, reduce errors, and respond faster to market demands, reinforcing software’s position as the backbone of smart machine ecosystems across industries.

Machine Type Analysis

Robots dominate the machine type segment of the Smart Machines Market, holding approximately 35% market share due to their broad applicability across industries. Robots are widely used in assembly lines, logistics operations, quality inspection, and hazardous environments where precision and safety are critical. Their flexibility allows deployment across multiple tasks, contributing to strong adoption in industrial settings. Industry data shows a 20.5% prevalence of robotic systems, supported by 14.1% growth in North American robot orders. Companies such as ABB Limited and Rethink Robotics have expanded multi-purpose robotic solutions that enhance productivity while reducing operational risk.

Advances in collaborative robots further support adoption by enabling safe human-machine interaction on factory floors. As industries continue to automate complex workflows, robots remain the most visible and impactful smart machine category, driving efficiency improvements and supporting scalable manufacturing and logistics operations worldwide.

Technology Analysis

Cloud computing holds the leading position in the technology segment of the Smart Machines Market, with an estimated 30% market share. Its dominance is driven by the need for scalable data storage, real-time analytics, and seamless integration with IoT-enabled machines. Cloud platforms allow manufacturers to collect, process, and analyze data from multiple locations, supporting predictive maintenance and operational optimization. Industry estimates indicate that cloud technologies account for nearly 29.8% of value share in advanced smart systems.

Leading technology providers such as Google Inc. offer robust cloud platforms capable of handling massive datasets while enabling AI-driven insights. Cloud computing also reduces infrastructure costs by eliminating the need for extensive on-premises hardware, making advanced analytics accessible to a broader range of organizations. As digital transformation accelerates, cloud-based technologies remain essential for enabling intelligent, connected, and responsive smart machine ecosystems.

Regional Insights

North America Smart Machines Trends

North America leads the Smart Machines Market, supported by strong innovation ecosystems and high levels of investment in automation and artificial intelligence. In the United States, robot orders increased by 8.8% in Q3 2024, reaching a valuation of $475 million, according to the Association for Advancing Automation. Growth is driven by adoption across non-automotive sectors such as pharmaceuticals and life sciences, which recorded 35% expansion. Regulatory frameworks, including NIST standards, support secure and standardized implementation of smart technologies.

In April 2025, IBM Corporation announced a $150 billion investment across the U.S. over five years, with over $30 billion allocated to research, development, and manufacturing of advanced computing systems. IBM highlighted that more than 70% of global transaction value is processed through its U.S.-manufactured mainframes. These investments reinforce North America’s leadership in smart machine innovation across manufacturing, healthcare, and industrial applications.

Europe Smart Machines Trends

Europe continues to advance in smart machine adoption, driven by Germany’s Industrie 4.0 initiative and strong collaboration between industry and government. Approximately 62% of German companies already use Industrie 4.0-related technologies, supporting 10.3% growth in smart factory deployments. ABB Limited plays a key role in this transformation and was recognized as a Leader in the 2025 Gartner Magic Quadrant for Global Industrial IoT Platforms. Its Genix Industrial IoT and AI Suite enables IT and operational technology integration, supporting autonomous operations through digital twins and advanced analytics. In September 2025, ABB introduced Genix Copilot and Metrics Hub, providing real-time, AI-driven insights for engineers and executives.

Demonstrations at Hannover Messe 2025 showcased cloud-powered energy management systems for multi-site optimization. Supported by widespread 5G coverage and initiatives like Plattform Industrie 4.0, Europe has positioned itself as a global leader in cyber-physical systems integration.

Asia Pacific Smart Machines Trends

Asia Pacific is the fastest-growing region in the Smart Machines Market, driven by large-scale manufacturing, government initiatives, and rapid technology adoption. China’s Made in China 2025 strategy emphasizes smart manufacturing through widespread deployment of industrial robots, AI systems, and real-time data analytics. AI is increasingly used as a factory operating layer, optimizing energy use, predicting maintenance needs, and improving production efficiency. Japan strengthens regional leadership through advanced robotics innovation.

At the International Robot Exhibition 2025, Yamaha Motor introduced new collaborative and SCARA robots, including the YK1200XG with a 50 kg payload capacity. Techman Robot showcased AI-powered inspection technologies that reduced setup time by 90% and supported zero-defect manufacturing. Combined with India’s cost advantages and ASEAN’s manufacturing hubs, Asia Pacific benefits from both scale and innovation. This convergence positions the region as a key growth engine for intelligent machines and autonomous systems globally.

Competitive Landscape

The Smart Machines Market exhibits moderate consolidation, with leading players controlling largest share of market share through strong research capabilities and ecosystem development. Major companies such as IBM Corporation and Google Inc. focus on integrating artificial intelligence, cloud platforms, and automation technologies to differentiate their offerings. Strategic partnerships, platform-based solutions, and expansion into as-a-service business models are increasingly used to enhance scalability and customer reach. Mergers and acquisitions help companies strengthen regional presence and expand technological capabilities. As competition intensifies, vendors emphasize adaptability, interoperability, and end-to-end solutions that deliver measurable efficiency gains. This evolving competitive landscape reflects the market’s shift toward intelligent, connected, and service-oriented smart machine solutions across industries.

Key Market Developments

- In March, 2025: Google DeepMind debuted Gemini Robotics models enabling autonomous robots to perform complex tasks like precise packing and origami folding. The vision-language-action model adapted across different robot embodiments, including Apptronik's Apollo humanoid robot, achieving 2x-3x higher success rates in end-to-end control tasks.

- In June, 2025: ABB launched three industrial robots—IRB 6730S, IRB 6750S, and IRB 6760—alongside the Flexley Mover P603 autonomous mobile robot with 1,500 kg payload capacity. Powered by OmniCore controller, the robots deliver 20% energy consumption reduction and path accuracy of 0.9 mm, supporting smart factory automation.

- In May, 2025: IBM advanced quantum-centric computing at Think 2025, unveiling integration of quantum and classical systems for operational AI. The company announced a 2029 roadmap for fault-tolerant quantum computers, combining hybrid computing architecture for solving complex manufacturing optimization and chemistry problems.

Companies Covered in Smart Machines Market

- Alchemy API Inc.

- Apple Inc.

- Digital Reasoning

- Google Inc.

- IBM Corporation

- Narrative Science Inc.

- Microsoft Corporation

- BAE Systems

- Creative Virtual

- Rethink Robotics

- ABB Limited

- Digital Reasoning Systems Inc.

- Creative Virtual Ltd.

- General Electric Co.

- Rockwell Automation Inc.

Frequently Asked Questions

The market is expected to grow from US$ 110.6 Billion in 2026 to US$ 403.3 Billion by 2033 at 20.3% CAGR.

Automation in manufacturing and autonomous robots address labor shortages, enhancing efficiency by 25-30% via AI and IoT.

Robots command 35% share due to versatile industrial uses and 14% order growth.

North America leads with U.S. innovation and $475 million Q3 2024 robot orders.

Healthcare robotics grows fastest, improving outcomes 30% amid pharma demand surges.