- Testing, Inspection, & Certification

- Smart Helmet Market

Smart Helmet Market Size, Share, and Growth Forecast 2026-2033

Smart Helmet Market by Product (Full Helmet, Half Helmet, Smart Hard Hat), Features (Bluetooth communication system, Integrated Video cameras, Navigation, Others), End-user (Consumer Sector, Construction Sector, Industrial Sector, Others), and Regional Analysis for 2026-2033

Smart Helmet Market Share and Trends Analysis

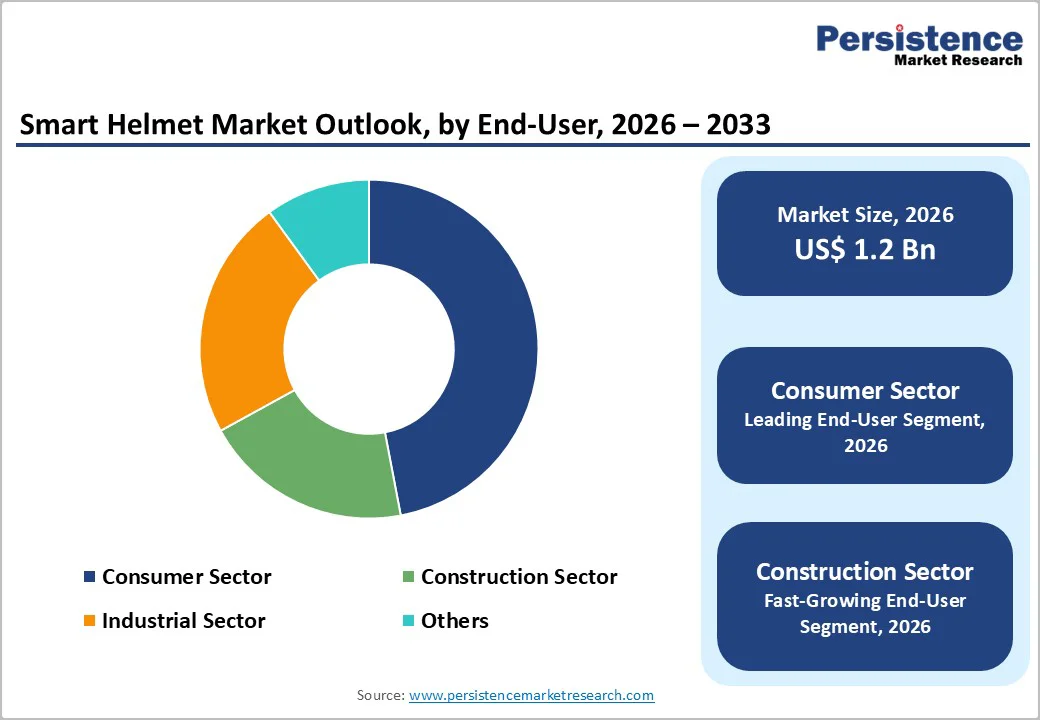

The global smart helmet market size is likely to be valued at US$ 1.2 billion in 2026, and is projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 14.5% during the forecast period 2026 - 2033. This growth is fueled by rising adoption of connected safety equipment, increasing road accident fatality rates, and stricter occupational safety regulations across construction and industrial sectors. Advances in IoT-enabled wearables, embedded sensors, and real-time communication systems are accelerating product penetration beyond motorcycling into industrial and enterprise use cases. Expanding urbanization, smart city initiatives, and rising consumer awareness of proactive safety solutions further reinforce long-term demand visibility

Key Industry Highlights

- Dominant Product: Full smart helmets are set to command around 55% revenue share in 2026, driven by higher ASPs and strong consumer adoption

- Fastest-growing Product: Smart hard hats are expected to register a CAGR of about 17% during the 2026–2033 forecast period on account of stringent construction site safety mandates.

- Leading Features: Bluetooth communication systems are likely to lead with about 39% share in 2026, while integrated video cameras are forecast to grow the fastest at a CAGR of 16% through 2033.

- End-User Dynamics: The consumer sector is expected to dominate with around 47% share in 2026, reflecting motorcycle premiumization trends, while the construction sector is anticipated to exhibit the highest CAGR of roughly 18% through 2033, driven by connected personal protective equipment (PPE) adoption.

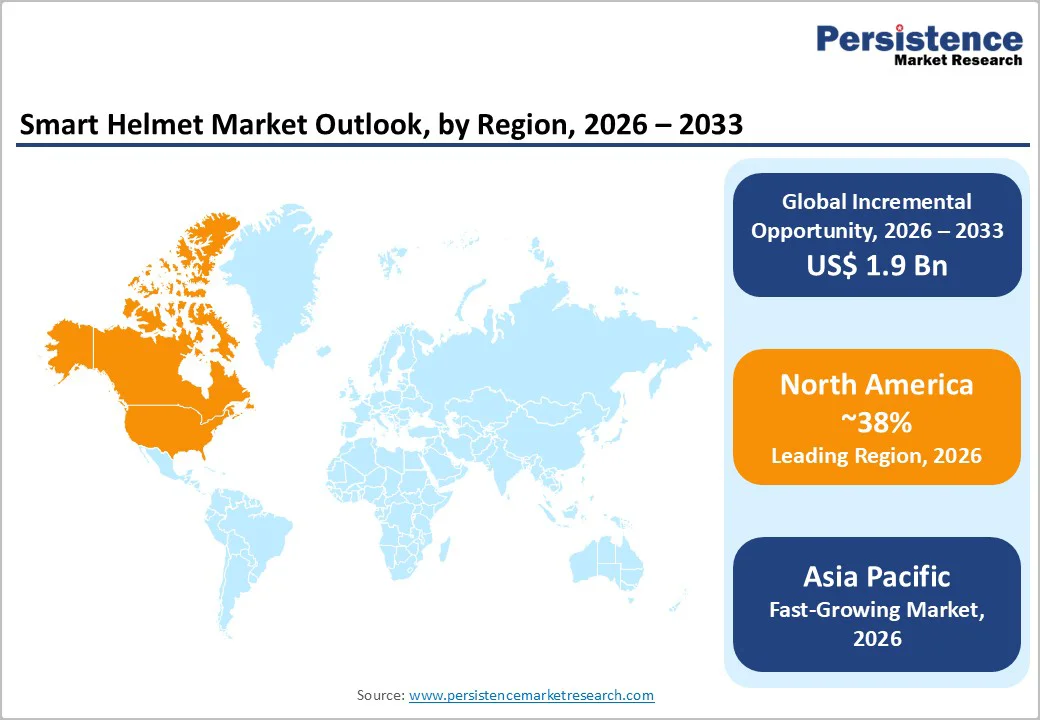

- Regional Leadership: North America is projected to lead with an estimated 38% share in 2026, supported by strict workplace and vehicular safety regulations and high technology adoption.

- Fastest-growing Market: The Asia Pacific market is expected to grow the fastest at a CAGR of about 16.5% through 2033, driven by massive two-wheeler sales in China and India.

- Competitive Trends: Governing dynamics include development in AI integration, enterprise partnerships, and regional expansions, strengthening product differentiation and accelerating adoption in high-growth markets.

- November 2025: Shoei launched the GT-Air 3 Smart Helmet, the world’s first fully integrated AR HUD helmet with nano-OLED display, mesh/cellular communication, noise-cancelling microphone, and a 10?hour battery.

| Key Insights | Details |

|---|---|

| Smart Helmet Market Size (2026E) | US$1.2 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulation-Driven Safety Demand Reinforced by Intelligent Helmet Adoption

According to the World Health Organization (WHO), road traffic crashes cause approximately 1.19 million deaths annually, with vulnerable road users accounting for more than half of all fatalities. Motorized two- and three-wheeler riders alone represent 21% of global deaths, rising to around 46% in Southeast Asia, underscoring the disproportionate risk faced by helmet-dependent users. In response, governments across major economies are tightening helmet safety regulations and enforcement, shifting the focus from basic compliance to enhanced rider protection and real-time risk mitigation, particularly in high-density urban and emerging mobility markets.

The growing workplace safety mandates in construction and industrial sectors are reinforcing demand for intelligent protective headgear. Smart helmets that integrate impact detection, location tracking, hazard alerts, and hands-free communication enable both riders and employers to actively manage safety rather than react to incidents. Supported by advances in embedded electronics and connectivity, these solutions are increasingly viewed as essential safety infrastructure, delivering measurable reductions in fatalities, downtime, and liability exposure. For example, in January 2025, Proxgy launched Hat+ Band and ProHat Band to convert standard industrial helmets into air-conditioned (Hat+) and smart helmets (ProHat) with 8-10 hour battery, targeting high-heat sectors such as mining, construction, and factories.

Cost and Operational Complexity Limiting Mass Adoption

Despite clear safety and connectivity advantages, high upfront costs remain a major constraint on large-scale smart helmet adoption. Conventional helmets are commonly priced in the US$ 40–120 range, while smart helmets typically cost US$ 80–150 for entry-level models and US$150–300 for mid-range variants, with premium configurations exceeding US$ 300–500 per unit. This two-to-fourfold price differential, driven by embedded sensors, connectivity hardware, certification, and software integration, limits uptake in price-sensitive emerging markets, where basic helmets still dominate volume sales and regulatory enforcement is uneven. Longer product lifecycles further reduce replacement-driven demand.

Operational limitations also weigh on adoption, particularly in enterprise environments. Battery constraints under continuous GPS, communication, or video use restrict full-shift deployment in industrial settings, while maintenance and software updates increase total ownership costs. At the same time, enterprises face growing concerns around data privacy, cybersecurity, and workforce monitoring, especially under strict data protection regimes. These factors add implementation complexity and slow large-scale rollouts, as many small and mid-sized organizations lack the digital infrastructure required to manage connected safety equipment securely and effectively.

Embedding of Smart Helmets in Smart Infrastructure and Urban Mobility Ecosystems

In 2025, major urban infrastructure and metro rail projects in Asia and the Middle East deployed smart hard hats to enhance worker safety and regulatory compliance. Equipped with real-time location tracking, fall detection, and hazard alerts, these helmets enabled site managers to respond immediately to incidents and restrict access to high-risk zones. Integration with digital dashboards improved monitoring of compliance and site analytics, streamlining insurance claims and minimizing liability. The success of these deployments mirrors innovations like Rapture Innovation Labs’ Sonic Lamb technology, which originated from smart helmet audio solutions, demonstrating how immersive, sensor-driven feedback can enhance worker awareness and safety.

Electric two-wheeler manufacturers in India and Southeast Asia have also begun bundling connected smart helmets with new vehicle launches. Features included automatic crash alerts, GPS-based emergency response, ride data sharing, and navigation support, providing commuters with enhanced safety and convenience. Startups such as Rapture Innovation Labs highlight how advanced audio and haptic feedback technologies can integrate seamlessly into urban mobility wearables, creating opportunities for fleet management, insurance integration, and recurring service revenue. By linking safety with digital services, these deployments illustrated a scalable growth model across consumer mobility and enterprise applications, signaling strong market expansion potential.

Category-wise Analysis

Product Insights

Full helmets are expected to dominate in 2026, accounting for approximately 55% of the smart helmet market revenue share in 2026. Their closed-shell design provides higher safety ratings and allows seamless integration of advanced electronics, including cameras, heads-up displays, and communication systems. This makes them the preferred choice for premium motorcycle riders and long-distance commuters who prioritize safety and functionality. The combination of regulatory compliance, consumer preference for advanced protection, and compatibility with emerging smart features ensures that full helmets maintain their leadership position across both mature and developing markets. Widespread availability and established consumer trust further reinforce their dominant revenue share.

Smart hard hats are anticipated to grow the fastest at an approximate CAGR of 17% through 2033, driven by their increasing adoption in construction and industrial sectors. Rising workplace safety mandates, enterprise digitization, and large-scale infrastructure projects, particularly in Asia Pacific and the Middle East, are key growth enablers. In June 2025, for instance, Bell Helmets expanded its lineup to include smart hard hat variants with biometric monitoring and IoT connectivity, highlighting cross-segment innovation and enhancing real-time safety and workforce monitoring. Bulk procurement by employers, coupled with features like hazard alerts, GPS tracking, and fall detection, is making smart hard hats a critical enterprise solution.

Accessories Insights

Bluetooth communication systems are projected to lead the accessories segment, accounting for roughly 40% of the revenue share in 2026. They are highly favored for hands-free communication, rider-to-rider connectivity, and voice-assisted navigation, making them indispensable for urban commuters and professional riders alike. Integration with helmets ensures safety without compromising convenience, while wide compatibility with smartphones and navigation systems drives sustained adoption. For example, in November 2025, Sena Technologies showcased its Specter Modular Smart Helmet at EICMA, featuring enhanced connectivity with Mesh 3.0 and high-fidelity audio, reinforcing the value of advanced communication systems in modern smart helmets. The high attach rate of Bluetooth systems across consumer helmets solidifies their leadership, supported by growing demand for connected and interactive riding experiences.

Integrated video cameras are expected to be the fastest-growing accessory at a CAGR of about 16% through 2033, as demand rises for incident documentation, training, and real-time monitoring in industrial, law enforcement, and fleet applications. Falling sensor costs, cloud storage integration, and enterprise demand for compliance and operational insights are accelerating adoption. These cameras transform smart helmets into multifunctional devices, enabling employers and fleet operators to monitor activity, enhance accountability, and improve safety outcomes. With expanding use cases and ongoing technological advancements, integrated video cameras are emerging as a high-growth, strategic accessory segment with strong long-term market potential.

End-User Insights

The consumer sector is likely to remain the largest end-user of smart helmets, accounting for approximately 47% of the revenue share in 2026. This growth is supported by rising motorcycle ownership, urban commuting trends, and premiumization, with riders increasingly valuing features such as navigation, emergency alerts, and hands-free communication. Enhanced safety awareness and lifestyle-oriented technology adoption further reinforce demand among urban commuters and recreational motorcyclists. The segment benefits from broad market reach, established distribution networks, and sustained consumer interest, ensuring continued revenue leadership in the global market.

The construction sector is anticipated to represent the fastest-growing end-user segment, projected to expand at a CAGR of roughly 18% through 2033, driven by enterprise safety programs and stricter regulatory compliance. Smart helmets enable employers to monitor worker safety, reduce accident-related costs, and meet compliance KPIs, making them integral to modern occupational safety strategies. Large infrastructure projects, particularly in Asia Pacific and the Middle East, are accelerating adoption through bulk procurement and enterprise deployment. This end-user segment is poised to increase its market share to over 30% by 2033, reflecting strong long-term growth potential.

Regional Insights

North America Smart Helmet Market Trends

North America is likely to secure approximately 38% of the smart helmet market share in 2026, with the United States functioning as the primary contributor. Growth is driven by stringent workplace safety regulations, high consumer spending on premium motorcycle gear, and robust adoption of smart hard hats in construction and utilities. A strong innovation ecosystem, supported by wearable technology development, advanced manufacturing capabilities, and high insurance penetration, further strengthens market leadership. Federal and state-level mandates ensure compliance, while early adopter consumers reinforce revenue stability. The combination of enterprise deployment and premium consumer adoption makes North America a mature yet dynamic market.

The promising trajectory of the regional market is further bolstered by venture funding, public-private safety initiatives, and a culture of technology adoption, which continually accelerates smart helmet integration across mobility and industrial sectors. Premiumization trends, coupled with rising interest in connected safety solutions, create opportunities for product differentiation and recurring service models. Enterprise programs in construction and industrial safety continue to drive large-scale procurement, sustaining demand for smart hard hats. In sum, North America’s established regulatory framework, consumer awareness, and innovation-led ecosystem ensure its continued dominance in global market share and steady growth.

Europe Smart Helmet Market Trends

Europe is likely to remain a mature, innovation-driven, and stable market, contributing a significant portion of smart helmet market revenues, led by Germany, the U.K., France, and Spain. Harmonized safety standards under ECE R22.06, coupled with GDPR-compliant data frameworks, guide product design and industrial adoption. Growing workplace digitization initiatives in manufacturing and construction drive enterprise deployment of smart helmets. European buyers emphasize certification, data security, and sustainable product design, which shapes competitive differentiation and premium pricing.

Smart helmet adoption in Europe is growing steadily, with industrial and urban mobility sectors both contributing to demand. Enterprises leverage connected helmets for operational safety, incident reporting, and workforce monitoring, aligning with strict regulatory oversight. The focus on compliance, technology integration, and eco-friendly manufacturing supports steady adoption across the region. While the growth rate of the Europe market is moderate compared to the Asia Pacific market, the stable regulatory environment established by the European Union (EU) and high-value enterprise contracts create long-term revenue opportunities and a strong platform for innovation-led expansion.

Asia Pacific Smart Helmet Market Trends

Asia Pacific is projected to be the fastest-growing regional market for smart helmets, boasting an estimated 2026-2033 CAGR of 16.5%, driven by China, India, Japan, and ASEAN countries. High two-wheeler density, rising construction activity, and cost-competitive manufacturing ecosystems enable rapid scale-up of both consumer and industrial smart helmet segments. Expanding middle-class populations, growing urban mobility requirements, and increasing adoption of electric scooters and enterprise PPE programs further stimulate demand. Bundling smart helmets with new mobility solutions and integrating advanced features such as GPS tracking and hazard alerts are creating scalable adoption channels across consumer and industrial sectors.

Government-led infrastructure investments and regulatory initiatives, such as the September 2025 Safe Helmets for Asia Pacific (SHAP) Initiative at the Asian Development Bank in Manila, have accelerated enterprise deployment by harmonizing helmet safety regulations, awareness, and certification standards across ASEAN countries. Local manufacturing partnerships and original equipment manufacturer (OEM) collaborations reduce costs and expand reach. Combined with affordable solutions, large populations, and digital infrastructure adoption, these factors position Asia Pacific as a high-growth hub, ensuring sustained adoption, strong penetration, and regional leadership in global smart helmet trends

Competitive Landscape

The global smart helmet market structure is moderately consolidated, led by key players such as Bell Helmets, Shoei, HJC, and Livall who control a substantial share of revenue. These companies leverage strong brand recognition, wide distribution networks, and integrated hardware-software solutions to maintain leadership. Continuous R&D investments drive innovation in IoT-enabled sensors, communication systems, and AI-based safety features. Regulatory compliance expertise and premium product offerings further strengthen their position. Their dominance spans both consumer and enterprise segments, ensuring broad market coverage.

Regional and niche players, including LS2, Sena Technologies, and Livall, focus on specialized applications such as smart hard hats or urban commuter helmets, maintaining strong presence in select geographies. High development costs, integration complexity, and data privacy concerns limit new entrants. However, software-driven solutions and cloud-based analytics create opportunities for emerging technology firms. Strategic partnerships and collaborations are increasingly used to enhance product capabilities. Market consolidation is expected to grow through acquisitions and alliances, expanding geographic and technological reach.

Key Industry Developments

- In November 2025, at EICMA 2025, TVS partnered with Swiss startup Aegis Rider to debut a next-generation AR HUD helmet. Featuring spatially anchored navigation, hazard alerts, and real-time motorcycle data, the carbon fiber helmet demonstrated connectivity with smartphones and motorcycles while complying with ECE 22.06 and DOT safety standards.

- In October 2025, Steelbird launched the SBH-32 Aeronautics Bluetooth smart helmet, featuring Bluetooth 5.2 with 48-hour talk time/110-hour standby, dual DOT/BIS homologation, aerodynamic PC-ABS shell, Pinlock-ready visor, and removable washable padding. It also includes air vents, wind deflector, rear spoiler, reflective elements, and Double D-Ring fastener for riders seeking performance in all conditions.?

- In May 2025, GoPro partnered with AGV to integrate action camera technology directly into motorcycle helmets. This collaboration enables high-quality video capture within the helmet shell, representing a first-of-its-kind move toward fully integrated imaging smart helmets for both safety and recording purposes.

Companies Covered in Smart Helmet Market

- Shoei Co., Ltd.

- Sena Technologies

- Forcite Helmet Systems

- CrossHelmet Inc.

- LIVALL

- Honeywell International

- 3M Company

- DAQRI

- Schuberth GmbH

- Bell Helmets

- Reevu Ltd.

- Jarvish Inc.

- Lumos Helmet

- Beijing Babaali Technology

Frequently Asked Questions

The global smart helmet market is projected to reach US$ 1.2 billion in 2026.

Key market drivers include rising road safety concerns, stringent workplace safety regulations, rapid adoption of connected mobility solutions, and enterprise safety program expansions

The market is poised to witness a CAGR of 14.5% from 2026 to 2033.

Opportunities exist in developing smart hard hats for infrastructure projects, integration with fleet management and insurance platforms, and adoption in electrified urban mobility ecosystems.

Shoei, Sena Technologies, Forcite Helmet Systems, CrossHelmet, LIVALL, and Honeywell are some of the key players in the market.