- Non-food Packaging

- Silo Bags Market

Silo Bags Market Size, Share, and Growth Forecast, 2026 - 2033

Silo Bags Market by Material Type (Polyethylene (PE), Polypropylene (PP), Others), Application (Grain & Oilseeds Storage, Forage Storage, Others), Capacity, and Regional Analysis for 2026 - 2033

Silo Bags Market Size and Trends Analysis

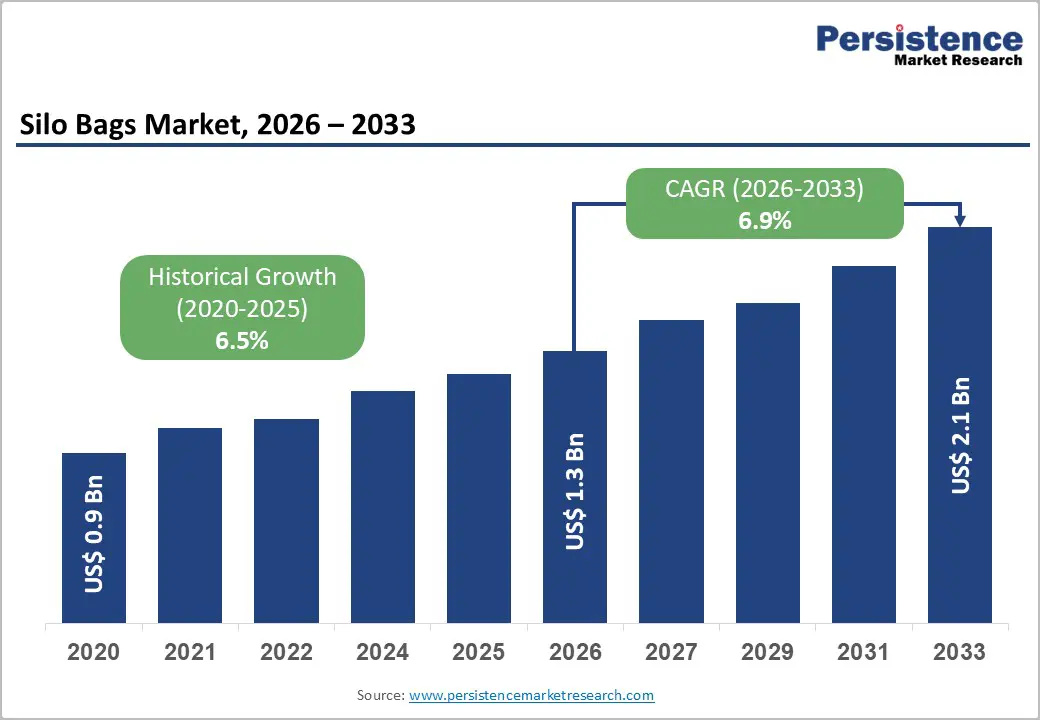

The global silo bags market size is likely to be valued at US$1.3 billion in 2026 and is expected to reach US$2.1 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by steady growth in global cereal and oilseed production, combined with structural constraints in permanent on-farm storage infrastructure and the increasing adoption of flexible, field-level storage solutions.

The market is primarily shaped by polyethylene (PE) dominance in film technology, rising use of silo bags for grain and oilseed storage, and larger farm operations shifting toward higher-capacity bags.

Key Industry Highlights

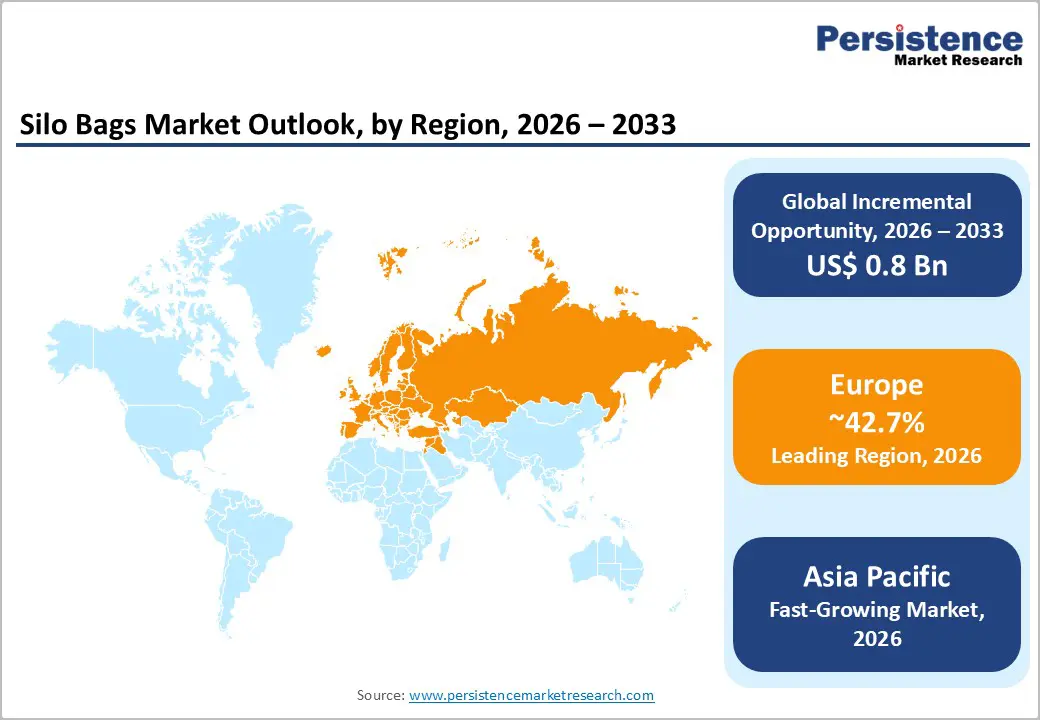

- Leading Region: Europe is anticipated to account for 42.7% of the global market share, driven by high agricultural productivity, dense grain and forage storage networks, strong regulatory compliance, and widespread adoption of premium multi-layer silo bag films across arable and dairy sectors.

- Fastest-growing Region: Asia Pacific, projected to record the highest growth rate through 2033, supported by expanding cereal production in China and India, increasing farm mechanization, improving rural storage infrastructure, and growing adoption of flexible storage solutions in export-oriented ASEAN markets.

- Investment Plans: Ongoing investments are focused on advanced multi-layer film extrusion, recyclability initiatives, and regional manufacturing expansion, particularly in Europe and Asia Pacific, as leading producers scale capacity to meet rising demand for durable and compliant silo bag solutions.

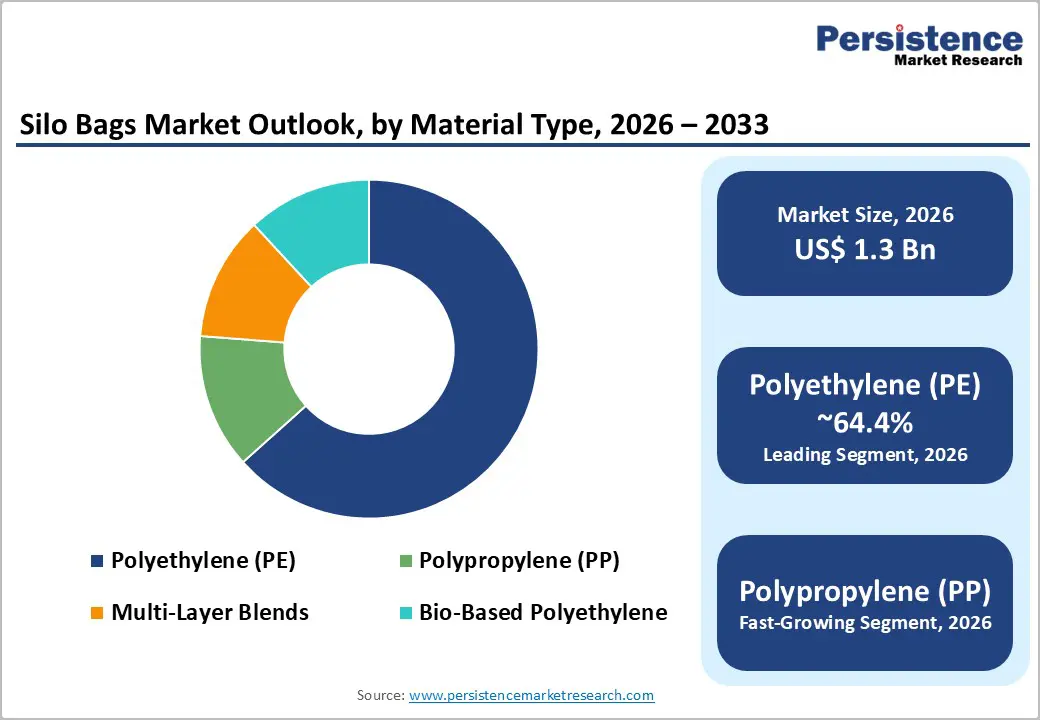

- Dominant Material Type: Polyethylene (PE) is anticipated to hold approximately 64.4% of the total market share, supported by its cost efficiency, processing flexibility, strong barrier performance, and compatibility with mechanized bagging systems.

- Leading Application: Grain and oilseed storage are estimated to represent roughly 49.4% of total market demand, driven by the need for low-capital, flexible storage during harvest peaks and logistics disruptions across major grain-producing regions.

| Key Insights | Details |

|---|---|

| Silo Bags Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Global Cereal and Oilseed Production Increasing Demand For Temporary Bulk Storage

Global cereal and oilseed production continues to expand in absolute tonnage, intensifying pressure on existing storage infrastructure during peak harvest periods. Seasonal harvesting cycles frequently create short-term storage deficits, particularly in regions with limited elevator capacity or delayed offtake logistics. In this context, silo bags serve as a cost-effective and rapidly deployable buffer storage solution. On-farm storage constraints heighten reliance on flexible systems that can be installed directly at harvest sites, reducing transport bottlenecks. From a market perspective, each incremental increase in harvested volumes directly translates into higher seasonal demand for silo bags, particularly in export-oriented agricultural regions.

Advancements in Film Technology: Improving Storage Performance and Reducing Spoilage

Material innovation has significantly enhanced the functional performance of silo bags. Multi-layer film structures, combined with advanced stabilizers and improved resin blends, have extended storage duration while minimizing oxygen and moisture ingress. These improvements reduce spoilage risk and make silo bags a viable alternative to traditional storage formats such as metal silos and bunkers for a broader range of crops. Enhanced UV resistance and mechanical strength increase reliability across diverse climatic conditions. As a result, larger commercial farms and contractors increasingly accept premium pricing for advanced film architectures, supporting margin expansion for manufacturers.

Structural Shifts in Farm Operations and Agricultural Logistics

Ongoing consolidation in farming operations and the rise of contract harvesting have reshaped post-harvest logistics. Larger enterprises prioritize storage systems that are scalable, mobile, and deployable close to the field, characteristics that favor silo bags. Flexible storage enables producers to stagger sales, manage price risk, and reduce congestion at centralized storage facilities. In regions with limited processing or cold-chain access, silo bags provide critical interim storage. These structural shifts support faster adoption of larger-capacity bags, particularly in the 200-300 metric ton and above segments.

Barrier Analysis - Resin Feedstock Price Volatility Impacting Cost Structures

Silo bags rely heavily on polymer resins, making production costs sensitive to fluctuations in energy and petrochemical markets. Sudden increases in resin prices compress manufacturer margins or result in higher product prices, which can delay purchasing decisions among cost-sensitive farmers. Historically, significant resin price spikes have translated into noticeable short-term increases in silo bag pricing, dampening demand elasticity in smaller farming operations. Mitigation strategies include long-term resin procurement contracts, material optimization, and value-added product positioning.

Regulatory Pressure on Agricultural Plastics

Environmental regulation targeting plastic usage and disposal presents a growing challenge, particularly in Europe and select Asia Pacific markets. Extended producer responsibility frameworks increase compliance costs related to collection, recycling, and reporting. Limited recycling infrastructure for used silo bags further complicates compliance. In the short term, regulatory costs can raise delivered product prices, potentially slowing adoption. Manufacturers adopting take-back programs, recyclable designs, and bio-based materials are better positioned to navigate this evolving regulatory landscape.

Opportunity Analysis - Circularity Initiatives and Bio-Based Material Adoption

The development of recyclable and bio-based polyethylene films represents a significant growth opportunity. Customers increasingly prioritize sustainability compliance, particularly in regulated markets. If circular material solutions achieve 10-15% adoption within Europe by 2030, this would create a premium subsegment valued in the tens of millions of dollars annually. Strategic partnerships with recyclers and agricultural cooperatives can accelerate adoption while securing long-term supply agreements and improving brand positioning.

Bundled Services and Digital Monitoring Integration

Bundling silo bags with mechanized loading and unloading systems, digital moisture sensors, and temperature monitoring solutions increases the overall value proposition. Integrated offerings reduce spoilage risk, lower labor requirements, and improve inventory control. Adoption of bundled solutions across 15-25% of large-scale farm installations could increase average revenue per installation by 20-40%, generating recurring service-based income streams and strengthening customer retention.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) is anticipated to retain a dominant position, accounting for approximately 64.4% of the market share over the forecast period. Its leadership is anchored in cost efficiency, processing flexibility, and consistent mechanical performance across wide temperature ranges, making it suitable for diverse climatic conditions. High-density and linear low-density polyethylene grades are commonly used, with multi-layer PE constructions incorporating oxygen- and moisture-barrier layers increasingly preferred for grain and silage storage. These designs help preserve grain quality by limiting aerobic degradation during long storage cycles. Established raw material supply chains, recyclability familiarity, and full compatibility with mechanized bagging and extraction equipment further reinforce PE’s position, particularly across Europe, North America, and Argentina, where silo bag adoption is mature.

Polypropylene (PP) and engineered polymer blends represent the fastest-growing material segment, with adoption anticipated to expand steadily through 2033. PP-rich films offer higher tensile strength, improved puncture resistance, greater thermal stability, and reduced creep under load, making them attractive for high-capacity or extended-duration storage. Demand is strongest among large commercial farms, grain contractors, and export-oriented operators that prioritize durability and reduced failure risk over upfront material cost. For example, PP-based and hybrid films are increasingly used in high-temperature regions and intensive forage operations where bag deformation risks are higher. As advanced extrusion and co-polymer blending technologies scale, cost differentials are narrowing, supporting accelerated PP penetration into premium silo bag applications.

Application Insights

Grain and oilseed storage is anticipated to remain the leading application segment, accounting for roughly 49.4% of the market share. Major crops stored include maize, wheat, soybeans, barley, and rapeseed, particularly in regions facing seasonal harvest surges and constrained elevator capacity. Silo bags offer a flexible, low-capital alternative to permanent silos, enabling farmers to manage post-harvest bottlenecks and price volatility more effectively. Their use is well-established across North America, Eastern Europe, and South America, where silo bags are integrated into modern grain handling and logistics systems. The ability to deploy storage directly at the field level reduces transportation pressure and supports just-in-time marketing strategies.

Forage storage is likely to be the fastest-growing application segment and is expected to gain incremental market share through the forecast period. Growth is driven by livestock intensification, rising demand for high-quality silage, and increasing focus on feed-loss reduction in dairy and beef operations. Sealed silo bags help preserve nutritional value by limiting oxygen ingress and moisture variability, which is critical for consistent animal performance. Forage applications typically require thicker films, higher puncture resistance, and superior barrier performance, driving demand for premium-grade materials and multi-layer constructions. Adoption is expanding rapidly in Europe and Asia Pacific, where dairy herd sizes are increasing and on-farm feed storage infrastructure is being modernized, supporting higher margins for manufacturers serving this segment.

Regional Insights

North America Silo Bags Market Trends - High-Value Adoption Driven by Large-Scale Farming, Overflow Storage, and Performance Films

North America represents a high-value market, shaped by large-scale commercial farming, advanced mechanization, and a strong focus on operational efficiency. Adoption of multi-layer polyethylene (PE) silo bags and value-added agronomic services, such as monitoring, handling equipment, and after-use collection, is widespread. The U.S. leads regional demand, supported by strong grain and oilseed output for crops such as maize, soybeans, and wheat, along with well-developed on-farm storage and logistics infrastructure. Silo bags are increasingly used as a strategic overflow solution during peak harvests and rail or elevator congestion, particularly in the Midwest and Great Plains.

Canada shows steady adoption, especially in Prairie provinces, where cold-climate performance is critical. Demand favors films engineered for low-temperature flexibility and puncture resistance, supporting longer winter storage cycles. Suppliers such as Berry Global and RKW Group have strengthened their North American agricultural film portfolios in recent years, focusing on enhanced barrier properties and recyclability. Brands such as Silostop have expanded technical advisory services in the region, reinforcing best-practice usage and reducing spoilage risk. Regulatory frameworks across the U.S. and Canada emphasize voluntary stewardship and recycling programs rather than strict mandates, allowing sustainability initiatives, such as used-film collection partnerships, to scale without constraining adoption.

Europe Silo Bags Market Trends - Regulation-Intensive Market Led by Premium Films, Traceability, and Recycling Compliance

Europe is projected to account for 42.7% of market share in 2026, reflecting its highly productive agricultural base, dense storage networks, and strong regulatory emphasis on traceability and environmental compliance. Countries including Germany, France, Spain, and the U.K. dominate regional demand, supported by intensive cereal cultivation and advanced dairy operations. Silo bags are widely deployed for grain, oilseeds, and forage storage, particularly in regions where land constraints and strict zoning limit the expansion of permanent silos. High yields and fragmented farm structures further reinforce demand for flexible, field-level storage solutions.

European buyers demonstrate a strong willingness to pay for premium, compliant films, favoring multi-layer constructions with improved oxygen barriers and mechanical strength. Manufacturers such as RKW Group and Trioworld have invested in agricultural film innovation and recycling-ready materials aligned with EU circular economy goals. Organized collection and recycling schemes, particularly in France and Germany, support stable market growth while raising compliance standards. Stringent regulatory requirements under EU packaging and waste directives increase entry barriers, favoring established players with certified products and traceable supply chains. This regulatory environment reinforces Europe’s leadership position while limiting low-cost competition from non-compliant imports.

Asia Pacific Silo Bags Market Trends-Fastest-Growing Volume Market Supported by Post-Harvest Loss Reduction and Rural Infrastructure

Asia Pacific is the fastest-growing regional market, driven by expanding cereal production, rising mechanization, and ongoing improvements in rural infrastructure. China and India account for the majority of incremental volume growth, supported by government-led initiatives to reduce post-harvest losses and improve on-farm storage capacity. In China, silo bags are increasingly used in major grain-producing provinces as a supplementary solution during procurement and transport delays. In India, adoption is rising among progressive farmers and agri-cooperatives handling wheat, maize, and oilseeds, particularly in regions facing inadequate warehouse capacity.

ASEAN countries, including Vietnam, Thailand, and Indonesia, are showing rapid uptake in export-oriented crop zones, where temporary storage is required to manage harvest season volatility. International suppliers such as IPESA and Silostop have expanded distributor networks and technical training programs across Asia Pacific, supporting correct installation and performance under humid conditions. Local film manufacturers are also scaling production, improving affordability and accelerating market penetration. Regulatory enforcement remains uneven across the region, creating both growth opportunities and sustainability challenges. While this variability can slow recycling adoption, it also enables faster volume expansion, positioning Asia Pacific as a critical long-term growth engine for the market.

Competitive Landscape

The global silo bags market exhibits moderate concentration, with global manufacturers serving premium segments and numerous regional players competing on price. Larger players leverage scale, advanced film technology, and integrated service offerings, while local suppliers focus on responsiveness and cost competitiveness. Competitive advantage increasingly depends on material innovation, sustainability compliance, and service integration.

Developments include expansion of multi-layer film production capacity, launch of recycling and take-back pilot programs in Europe, and partnerships between film manufacturers and mechanized bagging equipment providers. These initiatives enhance product differentiation, regulatory readiness, and customer lock-in.

Leading strategies center on innovation-driven differentiation, vertical service bundling, cost optimization, and sustainability positioning. Long-term resin sourcing, equipment partnerships, and regional customization are key competitive levers.

Key Industry Developments

- In September 2025, Trioworld Group initiated a pilot recyclable silo bag film program in select European countries under extended producer responsibility (EPR) frameworks to improve end-of-life management and support circular material flows.

- In August 2025, Silostop Ltd. partnered with a major mechanized bagging equipment manufacturer to offer integrated silo bag and loading/unloading solutions, strengthening its service portfolio for large-scale farming operations in the U.S. and Canada.

Companies Covered in Silo Bags Market

- IPESA Silo

- Berry Global Group, Inc.

- RKW Group

- Silostop Ltd.

- Trioworld Group

- Plastika Kritis S.A.

- Agriplast S.p.A.

- RPC BPI Group

- Coveris Holdings S.A.

- Polifilm Group

- Repsol Polímeros

- Ab Rani Plast Oy

- Al Pack Enterprises Ltd.

- Zill GmbH & Co. KG

- Grupo Armando Álvarez

- Shuangxing Plastic Group

- Hyplast NV

- Sigma Plastics Group

Frequently Asked Questions

The global silo bags market is valued at approximately US$1.3 billion in 2026.

By 2033, the silo bags market is expected to reach US$2.1 billion.

Key trends include wider adoption of multi-layer polyethylene films, increasing use of premium barrier and puncture-resistant materials, expansion of recycling and stewardship programs, and rising demand for forage and livestock feed storage applications. Technological improvements in extrusion and film durability are also enhancing storage performance.

By material type, polyethylene (PE) is the leading segment, accounting for approximately 64.4% of total market share, due to its cost efficiency, processing flexibility, and compatibility with mechanized bagging systems.

The global silo bags market is projected to grow at a CAGR of 6.9% between 2026 and 2033.

Major players include IPESA Silo, Berry Global Group, Inc., RKW Group, Silostop Ltd., and Trioworld Group.