- Specialty & Fine Chemicals

- Polyether Modified Polysiloxane Market

Polyether Modified Polysiloxane Market Size, Share, and Growth Forecast 2026 - 2033

Polyether Modified Polysiloxane Market by Product Type (Linear Polyether Modified Polysiloxane, Branched Polyether Modified Polysiloxane, Block Copolymer Polysiloxane, Graft Modified Polysiloxane, Specialty Variants), Form (Liquid, Emulsion, Powder, Pre-blended Formulations), Application, Industry, and Regional Analysis, 2026 - 2033

Polyether Modified Polysiloxane Market Size and Trend Analysis

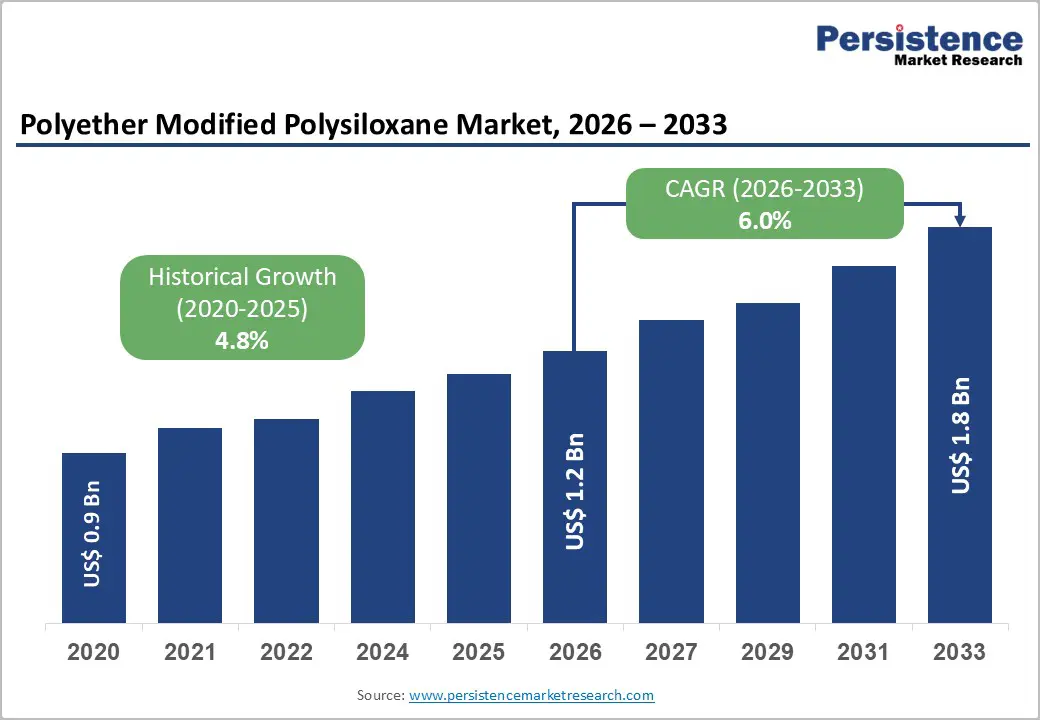

The global polyether modified polysiloxane market size is likely to be valued at US$ 1.2 billion in 2026 and is expected to reach US$ 1.8 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033.

This steady expansion is driven by rising demand for high-performance surfactants and surface-modification additives across paints & coatings, personal care & cosmetics, agriculture, textiles & leather, and industrial cleaning.

Key Industry Highlights:

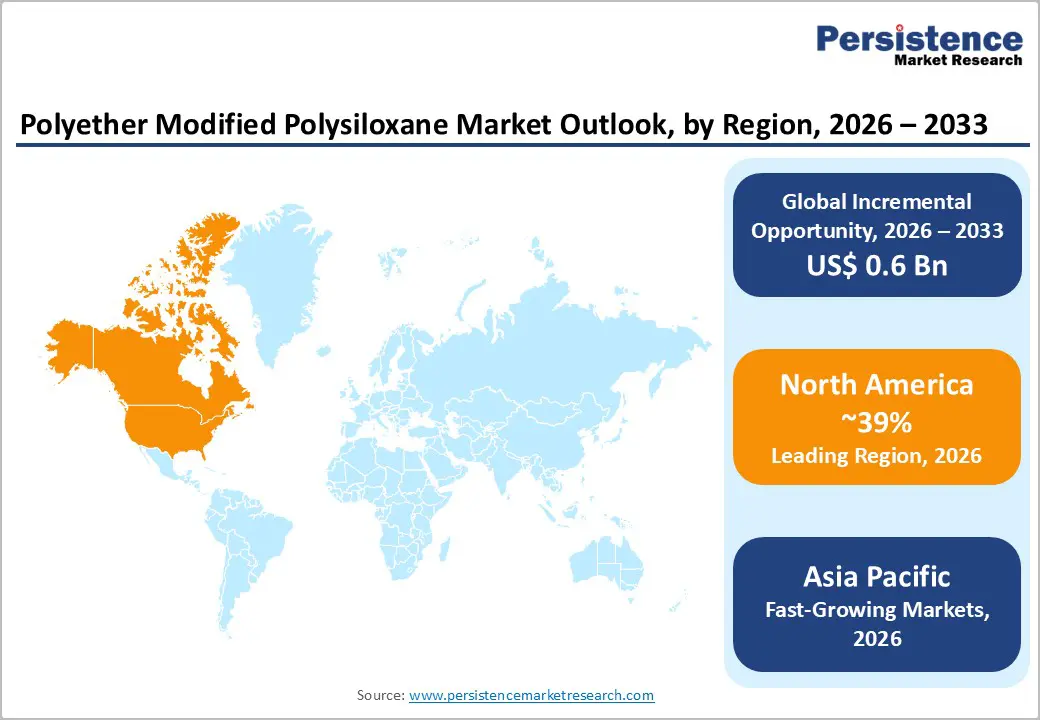

- Regional Leadership: North America leads the polyether modified polysiloxane market holding 39% share, supported by stringent environmental regulations, advanced coatings and personal-care industries, and strong agrochemical demand that favors high-performance silicone surfactants.

- Fastest-growing Market: Asia Pacific is the fastest-growing region with a rising CAGR of 8.7%, driven by industrialization, urbanization, and expansion of manufacturing hubs in China, India, and ASEAN economies, all of which require advanced surface-modification additives.

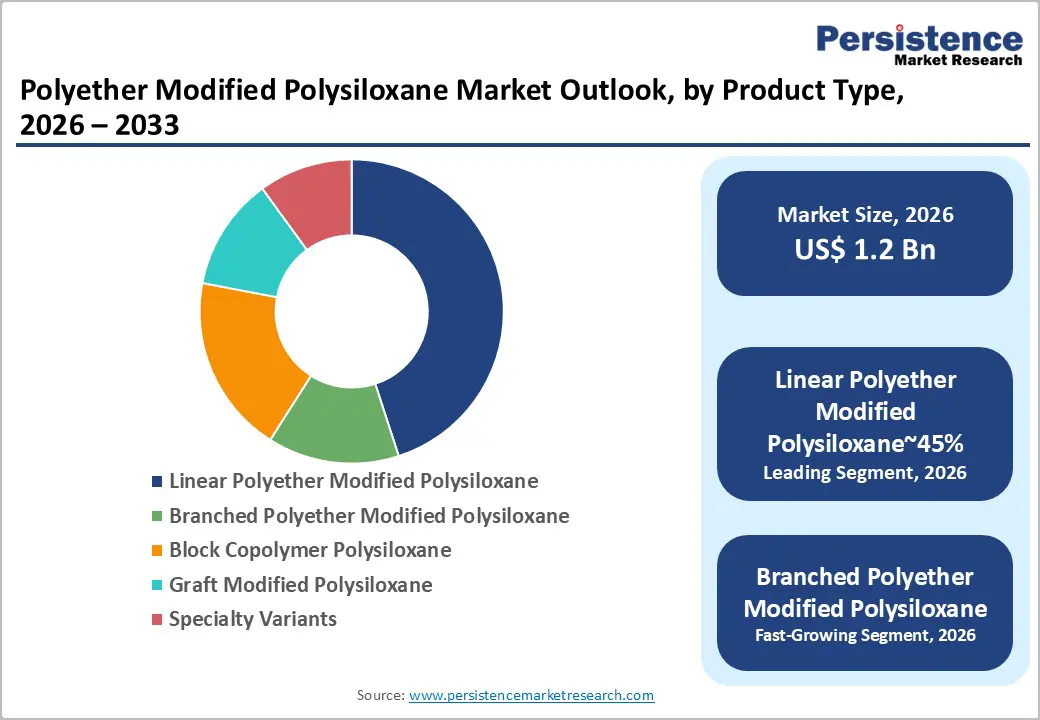

- Dominant Product: The linear polyether-modified polysiloxane segment dominates the product category, accounting for approximately 45% of global demand due to its well-defined molecular architecture, predictable performance, and broad compatibility across coatings, personal care, and industrial formulations.

- Fastest-growing Product: The defoamers & antifoaming agents segment is one of the fastest-growing, driven by the increasing need for high-efficiency foam-control additives in latexes, paints, adhesives, cleaning products, and fermentation processes.

- Key Opportunity: The integration of polyether-modified polysiloxanes into agrochemical adjuvants and electronics-grade coatings represents a major long-term opportunity, as formulators seek high-efficiency surfactants that enhance performance, sustainability, and process efficiency.

| Key Insights | Details |

|---|---|

| Polyether Modified Polysiloxane Market Size (2026E) | US$ 1.2 Billion |

| Market Value Forecast (2033F) | US$ 1.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.0% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Rising Use of High-Performance Silicone Surfactants Across Coatings, Personal Care, Agriculture, and Industrial Formulations

A key driver of the polyether-modified polysiloxane market is the rising need for high-performance surfactants and surface-active additives across industries such as paints and coatings, personal care, agriculture, and industrial cleaning. These silicone-based additives offer superior wetting, foam control, emulsification, and levelling compared with conventional surfactants, thereby enabling manufacturers to achieve smoother finishes, better dispersion, and improved product stability. In agrochemical formulations, they enhance spray spreading and leaf coverage, thereby improving effectiveness while reducing chemical use.

As production of formulated products continues to grow worldwide due to urban development, industrial expansion, and product innovation, demand for advanced performance additives is increasing steadily. Manufacturers are actively adopting these surfactants to meet rising quality expectations and efficiency standards. This growing reliance on high-performance formulations is expected to significantly support the long-term growth of the polyether-modified polysiloxane market.

Environmental Regulations Driving Strong Shift Toward Low-VOC and Eco-Friendly Silicone-Based Additives

Environmental regulations focused on reducing VOC emissions and harmful surfactants are strongly driving the adoption of polyether-modified polysiloxanes. Authorities such as the European Chemicals Agency and the U.S. Environmental Protection Agency are restricting the use of several traditional surfactants due to environmental and health risks. As a result, industries like coatings, adhesives, and cleaning products are shifting toward silicone-based additives that deliver strong performance with lower environmental impact.

These polysiloxanes perform effectively in water-based and low-VOC systems while minimizing foam and surface defects. Industry reports highlight their growing role in green formulations that meet regulatory standards without sacrificing product quality. As sustainability becomes a central focus across manufacturing sectors, demand for environmentally compliant surfactants is expected to increase, making polyether-modified polysiloxanes a preferred solution for future formulation development.

Restraints - High Raw Material Prices and Complex Manufacturing Processes Increasing Cost Pressure for Silicone Surfactant Producers

One major challenge facing the polyether-modified polysiloxane market is the high cost of silicone raw materials and complex manufacturing processes. Key inputs such as siloxane monomers, functional silanes, and polyether components are sensitive to energy prices, supply fluctuations, and geopolitical factors, which can create cost instability for producers. Additionally, the specialized chemical reactions required for production demand precise conditions, advanced catalysts, and multiple processing steps, increasing both capital investment and operating expenses.

These higher production costs often translate into premium pricing, limiting adoption in cost-sensitive industries such as bulk cleaners, low-margin coatings, and commodity agrochemicals. In emerging economies where price control is critical, manufacturers may prefer cheaper alternatives. Unless production efficiencies improve or raw material prices stabilize, cost pressure will continue to restrict market penetration in lower-value applications.

Formulation Challenges and Compatibility Risks Limiting Adoption among Smaller and Cost-Sensitive Manufacturers

Another restraint is the technical complexity involved in using polyether-modified polysiloxanes within multi-ingredient formulations. Because these additives are highly active at surfaces, even small formulation changes can cause foaming, instability, or separation if not carefully balanced. Compatibility problems may occur when mixed with certain solvents, resins, or ionic surfactants, leading to haze, reduced performance, or product failure.

This requires strong formulation expertise, extensive testing, and often customized solutions. Smaller manufacturers and regional formulators may lack the technical resources to manage these challenges efficiently. As a result, adoption can be slower in markets with limited technical support. While larger producers offer formulation guidance and ready-to-use blends, the overall complexity remains a barrier to broader market penetration, particularly for new or low-budget formulators.

Market Opportunities

Expanding Agricultural Applications Boosting Demand for Advanced Wetting and Spreading Silicone Surfactants

A major growth opportunity lies in the increasing use of polyether-modified polysiloxanes in agricultural formulations. These additives act as powerful wetting agents, spreaders, emulsifiers, and defoamers in pesticides, herbicides, and foliar nutrients. Research shows that silicone surfactants significantly improve spray coverage and droplet retention on plant surfaces, boosting effectiveness while reducing chemical volumes. This supports sustainable farming practices and integrated pest-management strategies.

Countries such as India, China, and Brazil are actively promoting precision agriculture and high-efficiency crop protection solutions, which is accelerating demand for advanced formulation additives. As global food demand rises and regulators push for lower chemical usage, agrochemical producers are increasingly adopting performance-enhancing surfactants. This makes agriculture one of the fastest-growing segments for polyether modified polysiloxanes, offering strong long-term revenue potential.

Growing Use in Electronics, Automotive, and Advanced Coatings Creating High-Value Market Opportunities

Another strong opportunity comes from expanding use in electronics, automotive, and high-performance coatings. In electronics manufacturing, these additives improve wetting, defoaming, and film uniformity in photoresists, encapsulants, and dielectric coatings, thereby supporting the fabrication of miniaturized and high-precision components. In automotive coatings, they enhance surface leveling and flow while controlling foam in water-based and high-solid systems. This helps manufacturers meet strict VOC regulations and durability requirements.

Advanced industrial coatings also rely on these surfactants to achieve smooth finishes and high production efficiency. Industry reports indicate rising adoption in premium-coating segments, where performance is more important than cost. With growth in electric vehicles, electronics manufacturing, and smart technologies worldwide, demand for specialty silicone additives is expected to increase steadily, creating attractive opportunities for polyether-modified polysiloxane producers.

Category-wise Analysis

By Product Type Insights

The linear polyether modified polysiloxane segment holds the largest market share, accounting for roughly 45% of global demand. This dominance is driven by its stable molecular structure, reliable performance, and broad compatibility across many formulations. Linear variants allow precise control of solubility, surface activity, and foam behavior, making them ideal for coatings, agrochemicals, personal care, and industrial cleaning products. Manufacturers prefer these materials due to their predictable results and ease of formulation.

Technical industry guidance shows strong adoption in water-based systems where consistent wetting and defoaming are critical. While branched and specialty structures are gaining interest for niche applications, linear products remain the backbone of the market. Their balance of performance, cost efficiency, and formulation simplicity ensures continued leadership across most mainstream applications.

By Form Insights

Liquid polyether-modified polysiloxanes constitute the largest segment, accounting for approximately 55% of total market demand. Their popularity stems from ease of handling, rapid mixing, and direct compatibility with liquid formulations used in coatings, agrochemicals, cosmetics, and cleaning products. Liquids can be precisely dosed and dispersed without special processing, saving time and reducing manufacturing complexity.

They perform particularly well in high-shear mixing environments where quick wetting and foam control are required. Formulation platforms consistently highlight liquid silicone surfactants as the preferred choice for scalable industrial production. As industries continue to prioritize operational efficiency and flexible formulation processes, demand for liquid forms is expected to remain strong. This segment will likely continue dominating the market due to its convenience and performance advantages.

By Application Insights

Defoamers and antifoaming agents account for the largest application segment, representing about 35% of global polyether modified polysiloxane demand. Foam control is critical across industries such as paints, adhesives, cleaning chemicals, fermentation, and coatings, where excess foam can disrupt production and lower product quality. These silicone-polyether additives combine strong foam-breaking power with excellent dispersibility, enabling rapid bubble collapse and long-term foam suppression.

Research articles confirm their superior efficiency compared to conventional defoamers, especially in water-based systems. As manufacturers aim to improve process efficiency, reduce downtime, and maintain consistent product quality, demand for high-performance defoaming solutions continues to rise. This makes foam control one of the most stable and high-volume applications supporting overall market growth.

Regional Insights

North America Polyether Modified Polysiloxane Market Trends

North America, led by the United States, represents a strong market driven by advanced industries and strict environmental regulations. VOC limits enforced by federal and state agencies have encouraged widespread adoption of low-emission silicone surfactants in coatings and industrial formulations. The region has a strong presence of major chemical producers offering high-performance additives to automotive, agrochemical, and personal care sectors. Well-established R&D centers and formulation support platforms accelerate product innovation and customized solutions.

U.S. manufacturers increasingly rely on silicone additives to achieve regulatory compliance while maintaining premium product performance. With continuous investment in advanced manufacturing and sustainable chemistry, North America remains a key revenue market. Ongoing product upgrades in coatings, agriculture, and industrial chemicals are expected to sustain steady growth in polyether-modified polysiloxane demand.

Europe Polyether Modified Polysiloxane Market Trends

Europe’s market growth is shaped by strong chemical safety regulations and sustainability initiatives. REACH compliance and environmental restrictions are pushing manufacturers to replace traditional surfactants with silicone-based alternatives that offer better performance and lower environmental impact. Countries such as Germany, France, and the UK are major users, particularly in water-based coatings, industrial cleaners, and personal care products.

European manufacturers focus heavily on low-VOC formulations that deliver smooth finishes and long-term durability. Industry associations promote standardized testing and transparent sustainability practices, increasing acceptance of silicone additives across borders. As the EU Green Deal promotes environmentally responsible manufacturing, demand for efficient and eco-friendly surfactants continues to rise. Polyether-modified polysiloxanes are increasingly positioned as key enablers of compliant, high-performance formulations across European industries.

Asia Pacific Polyether Modified Polysiloxane Market Trends

Asia-Pacific is the fastest-growing regional market, driven by rapid industrialization, expanding manufacturing hubs, and rising demand for advanced formulations. China, India, Japan, and Southeast Asian countries are heavily investing in coatings, electronics, agrochemicals, and automotive production. Government programs promoting green manufacturing and high-efficiency products are supporting the adoption of silicone-based surfactants.

Regional manufacturers are expanding production capacity to meet domestic demand and capitalize on export opportunities, benefiting from cost advantages and robust supply chains. Industrial parks and technology clusters across the region are driving demand for performance additives in modern manufacturing processes. As the Asia Pacific continues to strengthen its role as a global production center, demand for polyether-modified polysiloxanes is expected to grow rapidly, making it a key strategic market for suppliers.

Competitive Landscape

The global polyether modified polysiloxane market is moderately consolidated, with several multinational chemical leaders holding strong positions alongside numerous regional players. Major companies such as Dow, Shin-Etsu, Wacker Chemie, Momentive, Evonik, Elkem, and Siltech focus on innovation, large-scale production, and application-specific solutions. These firms invest heavily in R&D to fine-tune molecular structures for targeted performance across coatings, personal care, agriculture, and electronics.

Many also provide formulation support and customized blends to strengthen customer relationships. Meanwhile, regional manufacturers in the Asia Pacific and Latin America compete on pricing and localized supply, increasing competition in standard product categories. Strategic partnerships, technical services, and performance-driven product development are becoming key competitive tools. Overall, innovation capability and customer collaboration are shaping long-term market leadership.

Key Developments:

- In October, 2024: Dow Inc. introduced a new low-foam polyether modified polysiloxane for water-based architectural and industrial coatings, delivering improved defoaming, leveling, and formulation compatibility while complying with stringent low-VOC requirements in North America and Europe, enhancing performance in environmentally regulated markets.

- In March, 2025: Shin-Etsu Chemical Co., Ltd. expanded production capacity for specialty silicone surfactants, including polyether modified polysiloxanes, at its Japanese facility to meet rising demand in high-performance coatings, electronics, and personal care applications across Asia and global markets.

- In July, 2025: Evonik Industries AG formed a strategic partnership with an Indian agrochemical formulator to supply high-performance polyether modified polysiloxane adjuvants that improve spray-droplet spreading and pesticide performance, supporting sustainable agriculture initiatives in the region.

Companies Covered in Polyether Modified Polysiloxane Market

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Elkem ASA

- Evonik Industries AG

- Siltech Corporation

- Innospec Inc.

- BRB International BV

- Jiangxi Hito Chemical Co., Ltd.

- Supreme Silicones

- Guangzhou Tinci Materials Technology Co., Ltd.

- Hubei Xinsihai Chemical Engineering Co., Ltd.

- Gelest Inc.

- AB Speciality Silicones

- Siltech International Inc.

- Jiahua Chemicals Inc.

- SiSiB Silicones (Nanjing) Co., Ltd.

- 3M Company

Frequently Asked Questions

The global polyether modified polysiloxane market is projected to reach US$ 1.8 Billion by 2033, growing at a CAGR of 6.0% from 2026 to 2033, driven by rising demand for high-performance surfactants, stringent environmental regulations, and expansion in agriculture, coatings, and electronics.

Key demand drivers include increasing need for high-performance surfactants and defoamers, stringent environmental regulations on VOCs and hazardous surfactants, and growth in formulated products such as paints & coatings, personal care & cosmetics, agrochemicals, and industrial cleaning.

The linear polyether modified polysiloxane segment dominates the product-type category, accounting for around 45% of global demand due to its well-defined molecular structure, predictable surface activity, and broad compatibility in coatings, personal care, and industrial formulations.

North America leads the polyether modified polysiloxane market, supported by stringent environmental regulations, advanced coatings and personal-care industries, and strong agrochemical demand that favor high-performance silicone surfactants.

A Key growth opportunity lies in the integration of polyether modified polysiloxanes into agrochemical adjuvants and electronics-grade coatings, where they enhance spray-droplet spreading, film uniformity, and process efficiency while aligning with sustainability and performance requirements.

Leading players include Dow Inc., Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, Momentive Performance Materials Inc., Elkem ASA, Evonik Industries AG, Siltech Corporation, Innospec Inc., BRB International BV, Jiangxi Hito Chemical Co., Ltd., Supreme Silicones, Guangzhou Tinci Materials Technology Co., Ltd., Hubei Xinsihai Chemical Engineering Co., Ltd., Gelest Inc., and AB Speciality Silicones, among others.