- Pharmaceuticals

- Psilocybin Assisted Therapy Market

Psilocybin Assisted Therapy Market Size, Share, and Growth Forecast, 2026 - 2033

Psilocybin Assisted Therapy Market by Formulation (Liquid, Tablet, Capsule, Powder, Injection), Patient Demographics (Adults, Adolescents, Elderly, Veterans), Application (Depression, Anxiety, Post-Traumatic Stress Disorder (PTSD), Substance Abuse, Obsessive-Compulsive Disorder (OCD)), and Regional Analysis for 2026 - 2033

Psilocybin Assisted Therapy Market Share and Trends Analysis

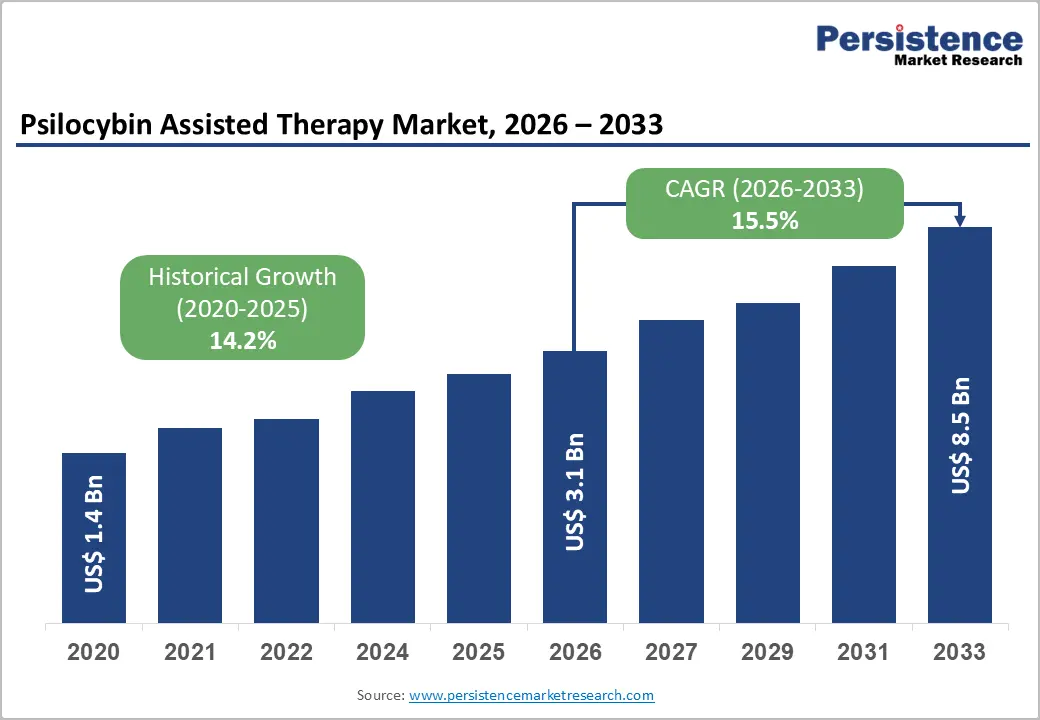

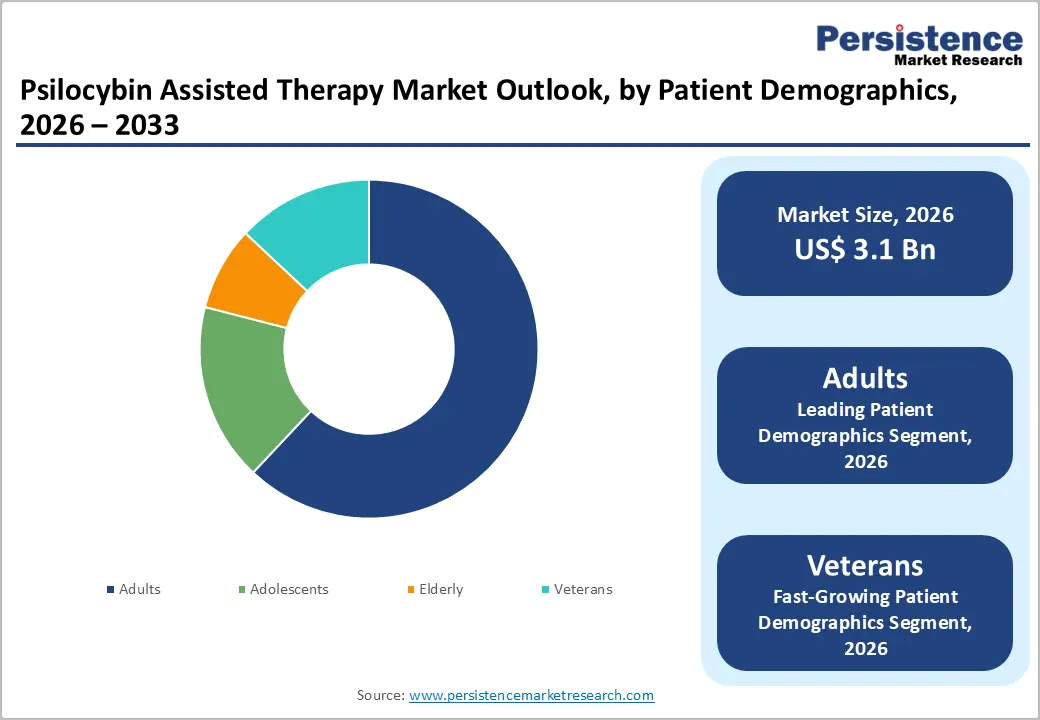

The global psilocybin assisted therapy market size is likely to be valued at US$ 3.1 billion in 2026, and is projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 15.5% during the forecast period 2026 - 2033.

Market expansion indicates an ongoing transformation in mental healthcare delivery models, where chronic mental health conditions increasingly require intervention pathways beyond conventional pharmacotherapy. The rising prevalence of treatment-resistant depression, anxiety disorders, and trauma-related conditions among adult and aging populations creates sustained demand for therapies that demonstrate durable clinical outcomes. Regulatory-backed clinical trials and government-supervised pilot programs strengthen clinical awareness, improving confidence among psychiatrists, psychologists, and institutional healthcare providers. Treatment adoption accelerates as standardized therapeutic protocols integrate psilocybin administration with structured psychological support, improving treatment adherence and outcome consistency. Advancements in formulation science, digital patient monitoring, and therapist-guided treatment platforms reduce variability in therapeutic delivery, supporting scalability across regulated healthcare environments.

Key Industry Highlights

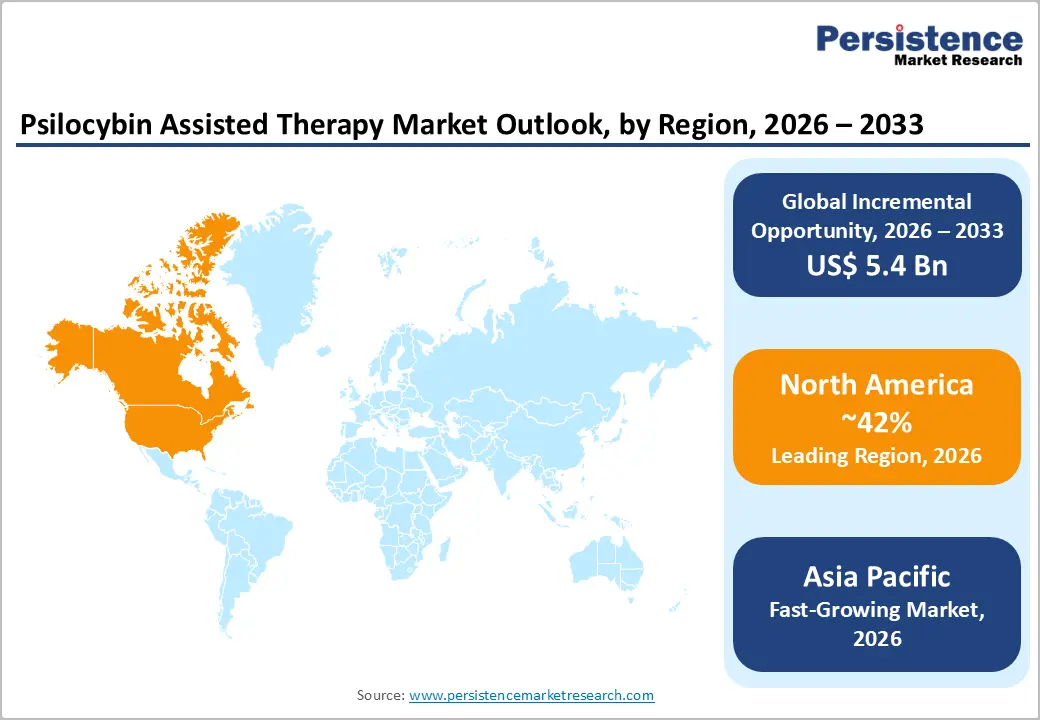

- Dominant Region: North America is expected to command approximately 42% in 2026, driven by an early adoption of regulated therapy protocols and a high concentration of specialized mental health centers.

- Fastest-growing Regional Market: The Asia Pacific market is forecasted to expand the fastest through 2033, fueled by the rising prevalence of mental health disorders and the strengthening of the healthcare infrastructure.

- Leading Patient Demographics: The adult segment is projected to hold about 62% of the revenue share in 2026, owing to a wide prevalence of treatment-resistant mental health conditions.

- Fastest-growing Patient Demographics: The veterans segment is forecasted to grow the fastest between 2026 and 2033, powered by targeted policy initiatives and government-backed healthcare programs.

| Key Insights | Details |

|---|---|

| Psilocybin Assisted Therapy Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 8.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 14.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Burden of Treatment-Resistant Mental Health Disorders

The increasing burden of treatment-resistant mental health disorders reflects a significant unmet clinical need that is reshaping priorities in mental healthcare. A substantial proportion of individuals diagnosed with major depressive disorder fail to respond adequately to standard therapies; research indicates that nearly 48% of depression patients do not respond after trying at least two antidepressants. This high rate of non-response amplifies distress and disability at the individual level and drives intensified clinical attention toward novel therapeutic modalities. Conventional pharmacological and psychotherapeutic approaches often provide only partial relief for these patients, leading to chronic symptoms, functional impairment and frequent healthcare utilization. Persistent symptoms also increase comorbidity with anxiety, post-traumatic stress disorder and substance use disorders, further complicating care pathways and elevating the overall societal burden.

Growing evidence suggests that alternative biological and psychological pathways can influence mental health outcomes, fueling interest in new interventions. Therapies targeting distinct neural circuits, such as serotonergic modulation with novel compounds, offer a departure from the monoamine-centric paradigm that underpins most standard treatments. Early clinical investigations into such approaches demonstrate rapid and sustained improvements in depressive symptoms among difficult-to-treat patients, underscoring their potential to fill critical gaps in current practice. Practitioners and healthcare decision makers view these emerging options as strategic responses to rising rates of non-response and relapse.

High Treatment Delivery Costs and Infrastructure Dependence

The primary restraint shaping the adoption of psilocybin-assisted therapies arises from the structurally intensive nature of therapeutic delivery, which embeds high operational complexity into every treatment cycle. Sessions require prolonged clinical engagement under supervised conditions, supported by preparatory screening, guided administration, and post-session integration. This format concentrates resource utilization into limited time windows, increasing dependence on specialized facilities rather than scalable outpatient models. Trained facilitators, clinical psychologists, and medical oversight personnel must remain continuously available, which constrains throughput and raises unit economics. Capital investment requirements extend beyond physical space to include compliance systems, monitoring equipment, and controlled handling protocols. Such cost structures reduce accessibility for payers and patients, narrowing uptake to well-funded institutions and research-aligned centers.

A second constraining force arises from regulatory and institutional uncertainty, which influences stakeholder risk tolerance. Classification under controlled substance frameworks imposes multilayer approval processes across clinical operations, ethics review, storage, and practitioner credentialing. This environment limits rapid geographic expansion and discourages smaller healthcare networks from participation. Workforce readiness remains uneven, with formal training standards still evolving, resulting in limited availability of qualified facilitators. Institutional review boards and hospital systems often apply conservative governance thresholds, extending implementation timelines. Public-sector caution and insurer hesitancy further restrict integration into standardized treatment pathways.

Integration into Institutional Mental Healthcare Systems

Expanding delivery through structured healthcare frameworks presents a significant growth avenue, enabling standardized protocols, optimized patient access, and improved outcome monitoring. Controlled clinical settings enable consistent dosing, supervision by trained professionals, and comprehensive follow-up, which enhances treatment credibility and regulatory compliance. Embedding therapy within established healthcare institutions also facilitates data collection for clinical studies, supporting evidence generation and reimbursement pathways. Hospitals and mental health clinics can leverage existing infrastructure to scale delivery efficiently while maintaining safety standards, reducing operational redundancies associated with standalone centers. This structured approach strengthens stakeholder confidence, including clinicians, payers, and regulatory bodies, which is critical for market maturation.

Institutional integration aligns with evolving healthcare policies and mental health initiatives. Insurance coverage and public health programs are more likely to support treatments offered within regulated systems, enhancing financial accessibility and patient reach. Collaborations with academic centers and research networks can drive innovation in treatment protocols, predictive analytics, and personalized care models. Institutional adoption also supports workforce development through formal training programs for facilitators, therapists, and support staff, ensuring high-quality service delivery.

Category-wise Analysis

Formulation Insights

The capsule segment is poised to lead with a forecasted 38% of the psilocybin-assisted therapy market revenue share in 2026, owing to consistent dosing accuracy, clinical familiarity, and ease of integration into supervised therapeutic protocols. Capsules allow precise quantification of active compounds, reducing variability across treatment cycles and ensuring reliable patient response. Their compatibility with established pharmaceutical standards supports streamlined regulatory approval and simplifies institutional adoption.

Storage and transportation are efficient due to stability under standard conditions, lowering logistical challenges. Clinicians benefit from predictable pharmacokinetics, which enhances safety monitoring. Patients experience consistent therapeutic effects, reinforcing trust and adherence

Liquid is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by dosing flexibility and rapid onset control. Liquid formulations enable individualized titration, allowing clinicians to adjust dosage in real time according to patient response, particularly in complex therapeutic plans. Technological advancements in stabilizing active compounds and masking taste improve patient acceptability and reduce treatment barriers. Rapid absorption characteristics support faster therapeutic onset, making liquids suitable for adaptive protocols requiring fine-tuned adjustments. Researchers increasingly adopt liquid formats for experimental and precision-focused interventions, accelerating evidence generation. Flexible administration routes, including oral drops or sublingual delivery, expand clinical utility.

Patient Demographics Insights

Adults are likely to be the leading segment with a projected 62% of the psilocybin-assisted therapy market share in 2026, due to high prevalence of treatment-resistant mental health conditions and strong engagement with structured therapy models. Growing exposure to workplace pressures, urbanization-related stress, and persistent anxiety disorders contributes to consistent demand. Adults are more likely to adhere to therapy schedules and utilize digital health tools, facilitating integrated care pathways and remote monitoring. Access through private insurance and employer-sponsored mental health programs enhances treatment affordability and adoption. Clinical settings favor adult populations for protocol standardization, and ongoing data collection strengthens evidence supporting efficacy and safety, sustaining market leadership.

Veterans are expected to witness the fastest growth between 2026 and 2033, powered by targeted policy initiatives addressing trauma-related disorders. Government-funded veteran healthcare programs prioritize innovative mental health interventions to treat post-deployment conditions such as PTSD and anxiety. Peer support networks within veteran communities enhance therapy acceptance and engagement, while specialized clinics provide structured treatment delivery. Dedicated research funding and strategic partnerships with mental health institutions drive program expansion. Increased awareness of evidence-based therapy outcomes encourages integration into veteran health benefits.

Application Insights

The depression segment is slated to hold a dominant position, with an anticipated 41% of market share in 2026, driven by high unmet clinical need and limitations of conventional antidepressant therapies. Persistent treatment-resistant cases create sustained demand for alternative interventions offering durable symptom relief. Clinicians increasingly adopt structured therapeutic protocols supported by specialized training programs, enhancing treatment credibility and safety. Digital referral systems and centralized specialist networks facilitate streamlined patient intake and continuity of care. Integration with mental health institutions allows consistent monitoring, data collection, and outcome evaluation.

The post-traumatic stress disorder (PTSD) segment is forecasted to be the fastest-growing application segment between 2026 and 2033, boosted by institutional adoption within trauma-focused care systems. Populations including military personnel, first responders, and disaster survivors are contributing to the rising demand. Technology-enabled platforms support real-time monitoring, personalized dosing, and outcome tracking, increasing treatment efficiency. Integration into trauma care centers facilitates access to multidisciplinary teams, ensuring comprehensive patient management. Policy initiatives and dedicated funding for PTSD interventions accelerate program rollout. Peer-support frameworks, combined with structured therapy protocols, enhance patient engagement.

Regional Insights

North America Psilocybin Assisted Therapy Market Trends

North America is expected to hold the largest share at approximately 42% in 2026, fueled by an advanced healthcare infrastructure and early adoption of regulated psilocybin therapy protocols. Leadership is supported by a dense network of specialized mental health centers equipped to deliver controlled therapeutic sessions under the supervision of trained clinicians. Availability of robust clinical trial networks enables rapid evidence generation, strengthening credibility among healthcare providers and payers.

Limited regulatory approvals for medical use create structured pathways for institutional integration, facilitating patient access. Insurance coverage and employer-sponsored mental health programs improve financial feasibility, expanding reach among adults with treatment-resistant conditions. Digital monitoring tools enhance adherence and outcome tracking, while established pharmaceutical manufacturing ensures reliable supply and standardized dosing.

Dominance is reinforced through strategic partnerships with academic institutions and research networks, driving innovation in precision dosing, personalized therapy models, and treatment efficacy analytics. Collaboration with technology platforms allows real-time patient monitoring and adaptive protocol adjustments, increasing clinical efficiency. Public awareness initiatives and advocacy by professional bodies improve acceptance among clinicians and patients, supporting uptake in structured care settings.

High urban population density and extensive mental health service penetration create concentrated demand hubs, optimizing resource utilization. Institutional capacity for extended therapy sessions, combined with formal ethical and safety oversight, ensures operational sustainability.

Europe Psilocybin Assisted Therapy Market Trends

Europe demonstrates steady growth potential in the psilocybin therapy market, driven by strong regulatory frameworks and increasing integration of innovative mental health treatments into public healthcare systems. Early adoption is supported by progressive clinical research policies and established psychiatric institutions capable of conducting controlled therapeutic interventions. National health services in several countries are actively exploring alternative treatment modalities for treatment-resistant depression and anxiety disorders, creating structured pathways for therapy implementation.

High clinician awareness, professional training programs, and centralized referral networks enhance adoption efficiency. Urban centers with dense populations of adults experiencing chronic stress and mental health disorders create concentrated demand clusters, allowing service providers to optimize resource utilization.

Market expansion is further reinforced by a focus on technology-enabled delivery models and patient monitoring frameworks. Digital platforms facilitate preparatory consultations, session scheduling, and post-therapy integration, improving treatment adherence and scalability. Investment in pharmaceutical manufacturing and quality assurance ensures consistency in dosing and reliable supply, reducing operational challenges for healthcare institutions. Public awareness campaigns, supported by advocacy groups and professional associations, are gradually increasing societal acceptance of alternative therapies. Collaborations with academic centers and cross-border research initiatives enable continuous protocol refinement, precision dosing, and outcome analytics.

Asia Pacific Psilocybin Assisted Therapy Market Trends

The Asia Pacific market is anticipated to be the fastest-growing market for psilocybin-assisted therapies through 2033, supported by the rising prevalence of stress-related and treatment-resistant mental health conditions, coupled with expanding healthcare infrastructure. Rapid urbanization, increasing workforce pressures, and growing recognition of alternative therapies are creating significant demand for innovative interventions. Government-backed initiatives to strengthen mental health services and regulatory frameworks are gradually opening pathways for clinical trials and structured therapy delivery, further accelerating adoption.

Emerging private healthcare networks and digital platforms enhance patient access, enabling remote monitoring, preparatory sessions, and post-treatment follow-up. Investment in local pharmaceutical manufacturing ensures reliable supply chains, supporting standardized dosing and scalable service delivery.

Growth is reinforced by technology integration, including telehealth-assisted therapy, adaptive dosing analytics, and digital outcome tracking, which improve clinical efficiency and patient adherence. Training programs for mental health professionals and targeted awareness campaigns enhance acceptance among both providers and patients. Rising disposable incomes and expanding insurance coverage in urban centers make therapy more financially accessible, while metropolitan clinical trial hubs accelerate evidence generation and protocol standardization. Cross-border collaborations with international research institutions drive knowledge transfer, enhance therapy optimization, and improve efficacy assessment.

Competitive Landscape

The global psilocybin assisted therapy market reflects a moderately fragmented structure, with influence distributed among specialized biotechnology firms, clinical service providers, and academic spin-offs. Key players, including Compass, AtaiBeckley, Helus Pharma, and Definium Therapeutics, leverage proprietary psilocybin formulations, controlled distribution channels, and licensed clinical networks to establish a strong presence. Strategic focus on clinical validation, regulatory alignment, and therapist training strengthens credibility and facilitates institutional adoption. Biotechnology firms drive innovation through compound development, dosage optimization, and stability improvements, while clinical service providers concentrate on structured therapy delivery and patient management.

Competitive positioning emphasizes regulatory compliance, robust clinical evidence, and consistent facilitator training frameworks. Firms prioritize scalable production, quality assurance, and intellectual property protection to secure operational stability. Research collaborations and clinical networks optimize therapy protocols and support data-driven outcome monitoring, reinforcing institutional and patient confidence. Training programs for therapists ensure standardized, high-quality delivery, while advocacy and engagement with regulatory bodies enhance reimbursement and insurance integration opportunities.

Key Industry Developments

- In September 2025, Medibank expanded its partnership with Emyria, Australia's sole psychedelic therapy provider, to cover psilocybin-assisted treatments for treatment-resistant depression (TRD) alongside prior MDMA-assisted PTSD therapy. This nearly doubles Emyria’s addressable market, validates its clinic model, and supports national rollout backed by strong PTSD data.

- In August 2025, a study published in Translational Psychiatry found that psilocybin-assisted therapy could be a cost-effective treatment for adults with treatment-resistant depression over 12 months, compared with standard third-line care, when total treatment cost is kept at about US$ 5,000 or less, showing favorable quality-adjusted life-year gains and economic value.

- In April 2025, New Mexico (NM)'s Medical Psilocybin Act legalized regulated medical psilocybin access for PTSD, treatment-resistant depression, substance use disorders, and end-of-life care. NM Dept. of Health aims for initial treatment settings by late 2026 with US$ 1 million funding, rulemaking underway for clinicians and producers, and an advisory board developing protocols/data collection.

Companies Covered in Psilocybin Assisted Therapy Market

- LCompass

- AtaiBeckley Inc.

- Helus Pharma

- Definium Therapeutics, Inc.

- Stella MSO LLC

- Seelos Therapeutics, Inc.

Frequently Asked Questions

The global psilocybin assisted therapy market is projected to reach US$ 3.1 billion in 2026.

Increasing prevalence of mental health disorders, growing clinical evidence, regulatory support, and widening adoption of alternative therapies are driving the market.

The market is poised to witness a CAGR of 15.5% from 2026 to 2033.

Key market opportunities include integration of psilocybin therapies into institutional mental healthcare, expansion in treatment-resistant patient populations, insurance coverage adoption, and development of innovative formulations and delivery methods.

Some of the key market players include Compass, AtaiBeckley Inc., Helus Pharma, Definium Therapeutics, Inc., Stella MSO LLC, and Seelos Therapeutics, Inc.