- Plastics, Polymers & Resins

- Anti-Fog Polycarbonate Films and Sheets Market

Anti-Fog Polycarbonate Films and Sheets Market

Anti-Fog Polycarbonate Films and Sheets Market by Thickness (Up to 0.5 mm, 0.5 mm to 2 mm, 2 mm to 5 mm, 5 mm to 7 mm, Above 7 mm), Grade Type (Optical Grade, Clear Grade), by Application (Lenses, Mirrors, Windows, Windshields, Display Panels, Roofing, Others), Industry (Automotive Industry, Food & Beverages, Electrical & Electronics, Others), Regional Analysis, 2025 - 2032

Anti-Fog Polycarbonate Films and Sheets Market Size and Trend Analysis

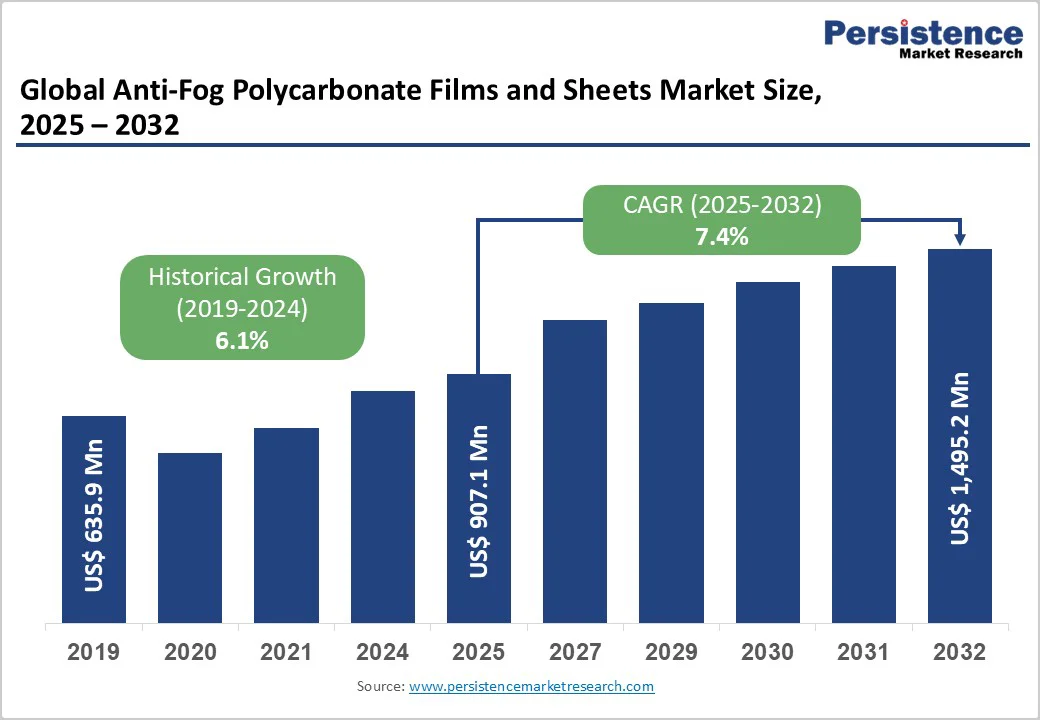

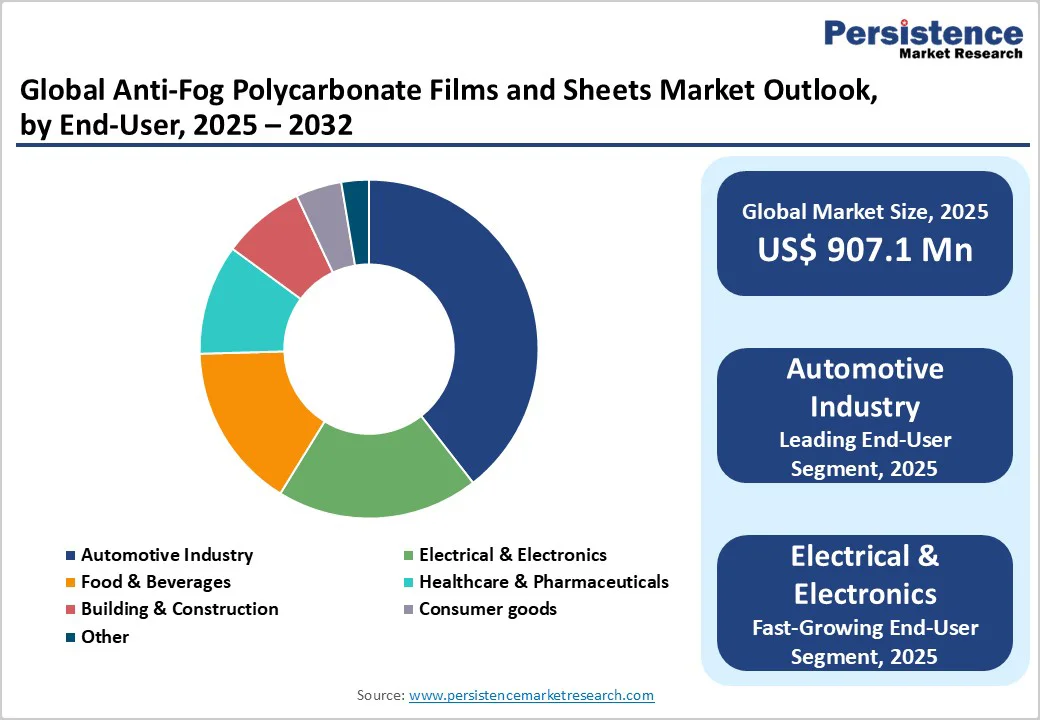

The global anti-fog polycarbonate films and sheets market size is likely to value at US$ 907.1 million in 2025 and is projected to reach US$ 1,495.2 million, growing at a CAGR of 7.4% between 2025 and 2032.

The market expansion is primarily driven by surging demand from the food packaging industry, where anti-fog properties ensure product visibility in refrigerated conditions, and the automotive sector's increasing adoption of advanced display panels and windshield technologies that enhance driver safety and visibility. The shift toward vehicle electrification and autonomous driving systems is creating substantial opportunities for high-performance anti-fog polycarbonate materials in automotive interior design and infotainment displays.

Key Market Highlights:

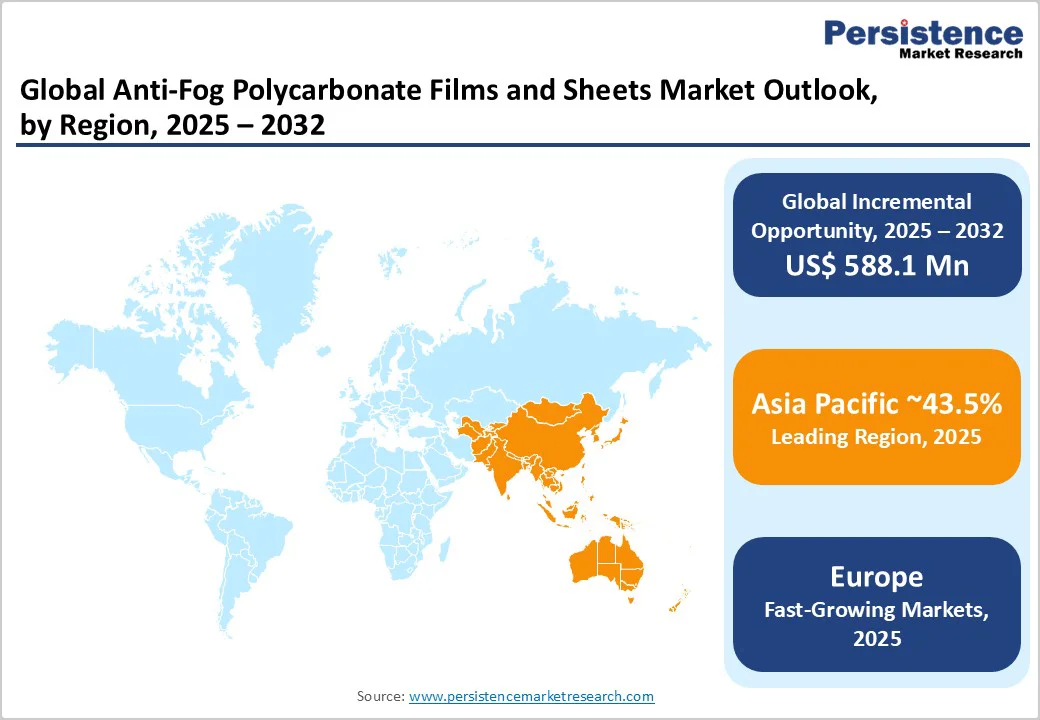

- Leading Region: Asia Pacific dominates the global market with a 43.2% share, driven by China’s vast automotive base and India’s rapid industrialization across construction, electronics, and vehicle sectors.

- Fastest-Growing Country: India records the fastest growth, supported by infrastructure development, expanding automotive production, and rising demand for energy-efficient building materials.

- Leading Thickness Segment: The 0.5-2 mm thickness range accounts for about 38% market share, favored for glazing, construction panels, and display applications due to strength and lightweight benefits.

- Fastest-Growing Grade: Optical grade materials lead in growth owing to superior clarity (90%+ transmission), low haze (<1%), and adoption in electronics, automotive, and medical devices.

- Emerging Opportunity: Recycled and bio-based polycarbonates such as Makrolon RP and ISCC PLUS certified grades cut carbon emissions by up to 60%, aligning with global sustainability directives.

| Key Insights | Details |

|---|---|

| Anti-Fog Polycarbonate Films and Sheets Market Size (2025E) | US$ 907.1 Mn |

| Market Value Forecast (2032F) | US$ 1,495.2 Mn |

| Projected Growth CAGR (2025 - 2032) | 7.4% |

| Historical Market Growth (2019 - 2024) | 6.1% |

Market Dynamics

Drivers - Rising Demand from the Food Packaging Industry Driving Market Expansion

The food and beverage industry serves as the primary growth driver for anti-fog polycarbonate films, contributing to over 65% of the global market demand. These films are vital in refrigerated and frozen packaging for perishable items such as fruits, vegetables, dairy, and ready-to-eat meals, as they prevent moisture buildup and maintain product visibility and freshness. Enhanced shelf life and hygiene standards make anti-fog films indispensable for modern retail and e-commerce grocery sectors.

Rising consumer demand for fresh, transparent, and visually appealing packaging has accelerated adoption across supermarkets and online platforms.

Automotive Industry Transformation Fueling Anti-Fog Polycarbonate Adoption

The automotive industry’s shift toward electrification and smart mobility is boosting the demand for anti-fog polycarbonate films and sheets. These materials are increasingly used in windshields, headlight covers, mirrors, and infotainment panels, where clarity and safety are paramount. Lightweight polycarbonate components reduce vehicle weight by up to 50% compared to glass, enhancing fuel efficiency by 25-35%.

As vehicle interiors evolve into connected, comfort-oriented spaces, optical-grade polycarbonate sheets are favored for touchscreens, heads-up displays, and interior design elements requiring high transparency and durability. With the growth of electric and autonomous vehicles, demand for anti-fog polycarbonate materials is set to expand steadily across automotive applications.

Restraints - Environmental Sustainability Concerns Limiting Market Growth

The non-biodegradable nature of traditional anti-fog polycarbonate films and sheets poses a major restraint to market expansion amid tightening global environmental regulations. Governments are introducing policies to reduce plastic use and promote biodegradable alternatives, creating pressure on manufacturers to innovate sustainable solutions. Growing concerns over plastic waste accumulation and its environmental impact have increased scrutiny from regulatory authorities and green organizations.

This evolving regulatory climate is driving substantial R&D investment toward bio-based polycarbonates and recyclable anti-fog materials. However, such innovations demand significant capital and technical resources. Rising consumer preference for eco-friendly products is also influencing market dynamics, potentially limiting demand for conventional anti-fog polycarbonate variants that lack sustainability credentials.

High Production Costs Constraining Market Accessibility

The high cost of production for anti-fog polycarbonate films and sheets is a significant barrier, particularly across cost-sensitive industries and emerging markets. Polycarbonate inherently carries higher raw material costs than acrylic, polyethylene, or glass, while the addition of anti-fog coatings further increases expenses. Manufacturing these materials requires advanced processes, precision coating technology, and strict quality control, all of which drive up capital investment.

These elevated costs result in pricing pressures, restricting widespread adoption where cheaper substitutes can suffice. Additionally, anti-fog coatings can deteriorate under UV exposure or repeated cleaning, raising maintenance requirements. Ensuring long-term performance often demands premium pricing, which can hinder market penetration in budget-conscious applications.

Opportunity - Circular Economy Initiatives Creating New Growth Avenues

The shift toward circular economy principles are unlocking major opportunities in the anti-fog polycarbonate films and sheets market as sustainability becomes a key differentiator. Manufacturers are investing in chemical and mechanical recycling technologies to produce high-quality recycled polycarbonate with properties equivalent to virgin materials.

Covestro’s Makrolon RP series, developed through partnerships with Neste and Borealis, incorporates at least 25% alternative raw materials and reduces carbon footprint by up to 60%, aligning with EPEAT and EU End-of-Life Vehicle Directive standards.

Mechanical recycling success in consumer electronics, achieving up to 95% recycled polycarbonate content, further validates the feasibility of circular solutions. ISCC PLUS certification enhances transparency across value chains, enabling credible sustainability claims. These developments offer manufacturers strong opportunities for premium positioning, eco-conscious branding, and competitive differentiation in markets with strict sustainability mandates.

Asia Pacific Urbanization and Infrastructure Development Driving Regional Growth

Asia Pacific is emerging as the fastest-growing region for anti-fog polycarbonate films and sheets, driven by rapid urbanization, robust infrastructure development, and expanding manufacturing capabilities. The region represents over 43% of the global polycarbonate market, with strong contributions from China, India, and Japan. India’s market, growing at an average annual rate of 11,495.2% (2013-2024), is supported by booming construction and automotive sectors utilizing polycarbonate for roofing, glazing, and lightweight vehicle components.

China’s large-scale urban infrastructure projects and dominance in automotive manufacturing, accounting for over 29% of global production, are fueling material demand for transparent, durable, and thermally efficient applications. The region’s electronics manufacturing ecosystem further expands opportunities, while rising disposable incomes and supportive government infrastructure policies make the Asia Pacific the key growth hub for the forecast period.

Category-wise Insights

Thickness Analysis

The 0.5 mm to 2 mm thickness segment leads the anti-fog polycarbonate films and sheets market, accounting for around 38% of total revenue. This range offers the ideal combination of flexibility and strength, making it suitable for automotive glazing, construction windows, and display protection.

Its lightweight nature, about 50% less than glass, improves fuel efficiency while providing 250 times higher impact resistance. Energy-efficient multiwall configurations with U-values as low as 1.78 W/m²K further enhance their utility in sustainable architecture.

The sub-1 mm films segment is witnessing the fastest growth, driven by rising demand in food packaging and medical device applications. These thinner films deliver high optical clarity exceeding 90% and superior anti-fog performance, ensuring product visibility in refrigerated packaging and precision in medical imaging environments.

Grade Type Analysis

Optical Grade polycarbonate dominates the market with about 42% share, propelled by its unmatched clarity (>90% light transmission) and minimal haze (<1%). It is widely used in smartphones, automotive infotainment systems, AR/VR headsets, and medical imaging devices, where optical precision and impact resistance are critical. The material’s durability, 250 times stronger than glass, makes it ideal for high-performance, safety-critical applications.

The UV-stabilized and coated grade segment is expanding fastest, owing to increasing outdoor and automotive use. Advanced coatings like UV-blocking, anti-reflective, and anti-fog layers enhance durability and clarity under challenging conditions, driving adoption in automotive exteriors, architectural facades, and outdoor electronic displays.

Application Analysis

Display panels represent the leading and fastest-growing application, projected to grow at a positive CAGR. Their dominance stems from the global surge in smartphones, tablets, and automotive displays requiring clarity and anti-fog reliability. The trend toward flexible and foldable screens further strengthen this segment’s growth potential.

In the automotive industry, integration of multiple touch displays and digital dashboards fuels rising demand for anti-fog polycarbonate films. Manufacturers like Teijin are scaling production for in-vehicle electronics, while smart home and IoT applications continue to expand the material’s footprint in emerging display technologies.

Industry Analysis

The automotive industry remains the dominant industry segment, capturing around 35% share. Its transformation toward electrification, lightweight design, and safety advancements is accelerating polycarbonate adoption in windshields, headlight covers, and infotainment displays. The material’s light weight and impact resistance support improved fuel efficiency and enhanced visibility.

The Electronics and Electrical sector is the fastest-growing Industry, driven by the proliferation of display panels, touchscreens, and smart devices. Polycarbonate’s anti-fog and optical properties make it indispensable in high-precision electronic components, fostering continuous demand from the expanding consumer electronics and IoT ecosystems.

Regional Insights

North America Anti-Fog Polycarbonate Films and Sheets Market Trends

North America accounts for around 24% of the global anti-fog polycarbonate films and sheets market in 2024, reflecting steady demand supported by its strong automotive, food packaging, and construction industries. The United States leads regional adoption, driven by automotive lightweighting initiatives and strict safety regulations promoting anti-fog materials in glazing, displays, and lighting systems. The region’s well-established cold chain infrastructure and preference for transparent packaging also sustain robust consumption across the food and beverage sector.

Major players such as 3M, Plaskolite, and Trinseo are advancing innovations in anti-fog coatings, sustainable formulations, and high-performance polycarbonate materials. Additionally, energy-efficient construction practices and the growing trend of green buildings are reinforcing the region’s market strength, making North America a key hub for premium anti-fog polycarbonate applications.

Europe Anti-Fog Polycarbonate Films and Sheets Market Trends

Europe holds approximately 28% of the global market share in 2024, underpinned by its leadership in sustainability-driven innovation, stringent environmental regulations, and strong automotive manufacturing base. Countries such as Germany, the UK, France, and Spain remain leading consumers, supported by active implementation of the EU Circular Economy Action Plan and the revised End-of-Life Vehicle Directive that emphasize recycled and bio-based material use.

Collaborations such as Covestro and Brett Martin’s Makrolon RE bio-circular initiative, which delivers near carbon-neutral polycarbonate sheets, highlight the region’s shift toward circular materials. Demand from Europe’s construction, packaging, and healthcare sectors continues to grow, particularly for transparent, safe, and recyclable polycarbonate films, aligning with evolving sustainability targets and consumer expectations.

Asia Pacific Anti-Fog Polycarbonate Films and Sheets Market Trends

Asia Pacific dominates the global anti-fog polycarbonate films and sheets market with an estimated 43.5% share in 2024, making it both the largest and most dynamic regional market. China anchors this leadership position as the world’s largest automotive and electronics manufacturer, driving large-scale consumption of polycarbonate materials for display systems, glazing, and structural components. Expanding infrastructure and smart city projects further amplify material utilization in roofing and façade applications.

India represents the fastest-growing market within the region, fueled by industrial expansion, automotive manufacturing, and rising electronics production. Japan’s advanced technology sectors also contribute significantly to the demand for high-precision optical-grade polycarbonate. The presence of leading global producers such as SABIC, Covestro, Teijin, and Mitsubishi Gas Chemical ensures a robust regional supply chain, positioning Asia Pacific as the global hub for anti-fog polycarbonate innovation and production.

Competitive Landscape

The global anti-fog polycarbonate films and sheets market features a moderately fragmented competitive landscape, with numerous global and regional manufacturers operating across diversified application segments.

Market concentration remains balanced as companies compete through innovations in sustainability, coating performance, and material durability. Industry participants are increasingly focusing on differentiation through proprietary anti-fog technologies, improved optical properties, and value chain partnerships that ensure consistent supply and market reach.

A strong emphasis on circular economy initiatives and sustainable material development defines current competition. Manufacturers are investing significantly in chemical and mechanical recycling to produce high-quality recycled polycarbonate with verified sustainability credentials.

Ongoing R&D efforts target advancements in bio-based feedstocks, high-performance coating systems, and extrusion technologies that reduce environmental impact while enhancing product functionality and market competitiveness.

Key Market Developments:

- In June 2024, Teijin Limited launched a new production line for Panlite polycarbonate sheets and films at its Matsuyama plant, Ehime, with a 1,350-ton annual capacity. The facility targets automotive interior and in-vehicle electronic components, aiming for ¥2.5 billion in sales by fiscal 2027.

- In June 2024, Mitsubishi Gas Chemical Company obtained ISCC PLUS certification for polycarbonate resin production at its Kashima Plant, enabling sustainable polycarbonate manufacturing via mass balance. The certification covers multiple group companies, reinforcing a fully integrated biomass-based polycarbonate supply chain.

- In August 2025, Brett Martin and AmeriLux International established the American Polycarbonate Company, a 500,000 sq ft joint venture facility in De Pere, Wisconsin. Scheduled for 2026, it will produce multiwall and corrugated polycarbonate sheets for construction, agriculture, and architectural applications.

Companies Covered in Anti-Fog Polycarbonate Films and Sheets Market

- SABIC

- Covestro AG

- Plaskolite LLC

- Excelite Plastic Limited

- WeeTect Inc

- Arla Plast AB

- Palram Industries Ltd

- Brett Martin Ltd

- Trinseo SA

- Teijin Limited

- Mitsubishi Gas Chemical Company Inc

- Kafrit Group

- 3M Company

- Ningbo Zhongding Plastic Co Ltd

- UG-Plast Inc

- Rowland Technologies Inc

- Gallina India

- Işık Plastik

- Koscon Industrial SA

- MGC Filsheet Co Ltd

- Kashima Polymers Corporation

- Mitsubishi Engineering-Plastics Corporation

- American Polycarbonate Company

Frequently Asked Questions

The global anti-fog polycarbonate films and sheets market is likely to value at US$ 907.1 billion in 2025 and is projected to reach US$ 1,495.2 billion by 2032, expanding at a robust CAGR of 7.4% during the forecast period.

Rising demand from the food packaging, automotive, and construction sectors drives growth due to fog prevention, lightweight, and energy-efficient properties.

The 0.5 mm to 2 mm thickness segment dominates with 38% share due to its strength, flexibility, and lightweight performance.

Asia Pacific leads with 43.2% share, driven by strong automotive, electronics, and construction industries.

Sustainable and recycled polycarbonate materials present major opportunities aligned with the circular economy and green regulations.

Leading players include SABIC, Covestro, Teijin, Mitsubishi Gas Chemical, 3M, Plaskolite, Palram, Brett Martin, WeeTect, and others.