- IT and Telecommunication

- Secure Socket Layer (SSL) Certification Market

Secure Socket Layer (SSL) Certification Market Size, Share, and Growth Forecast 2026 - 2033

Secure Socket Layer (SSL) Certification Market by Product (Organization Validation (OV) SSL, Extended Validation (EV) SSL, Domain Validation (DV) SSL), by Application (SMEs, Large Enterprises, Government Agencies), by Regional Analysis, 2026-2033

Secure Socket Layer (SSL) Certification Market Size and Trend Analysis

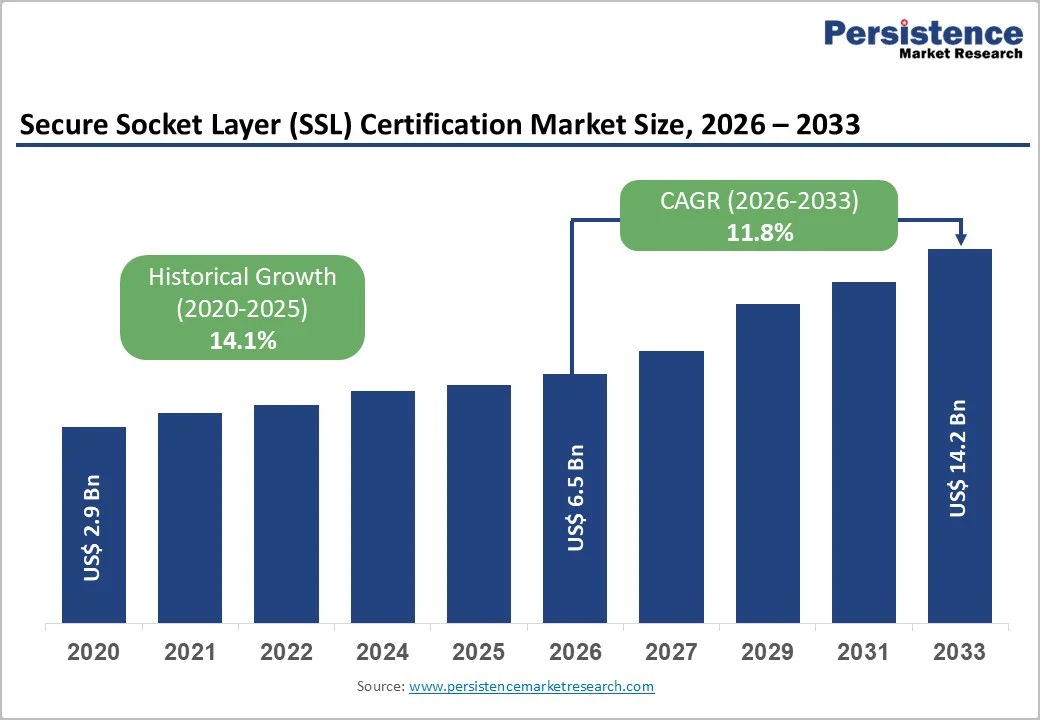

The global Secure Socket Layer (SSL) Certification market size is expected to be valued at US$ 6.5 billion in 2026 and projected to reach US$ 14.2 billion by 2033, growing at a CAGR of 11.8% between 2026 and 2033. The SSL certification market is experiencing unprecedented growth driven by escalating cybersecurity threats, stringent regulatory compliance mandates, and the accelerated adoption of cloud-based solutions across enterprises worldwide.

Organizations are increasingly recognizing that website security and data encryption have become fundamental business imperatives rather than optional features, with 87% of cyber threats now utilizing encrypted channels to evade traditional security measures. The widespread push toward universal HTTPS encryption has transformed SSL certificates from a niche security solution into foundational infrastructure, with 88.08% of websites globally now employing SSL/TLS protocols to secure data transmission.

Key Market Highlights

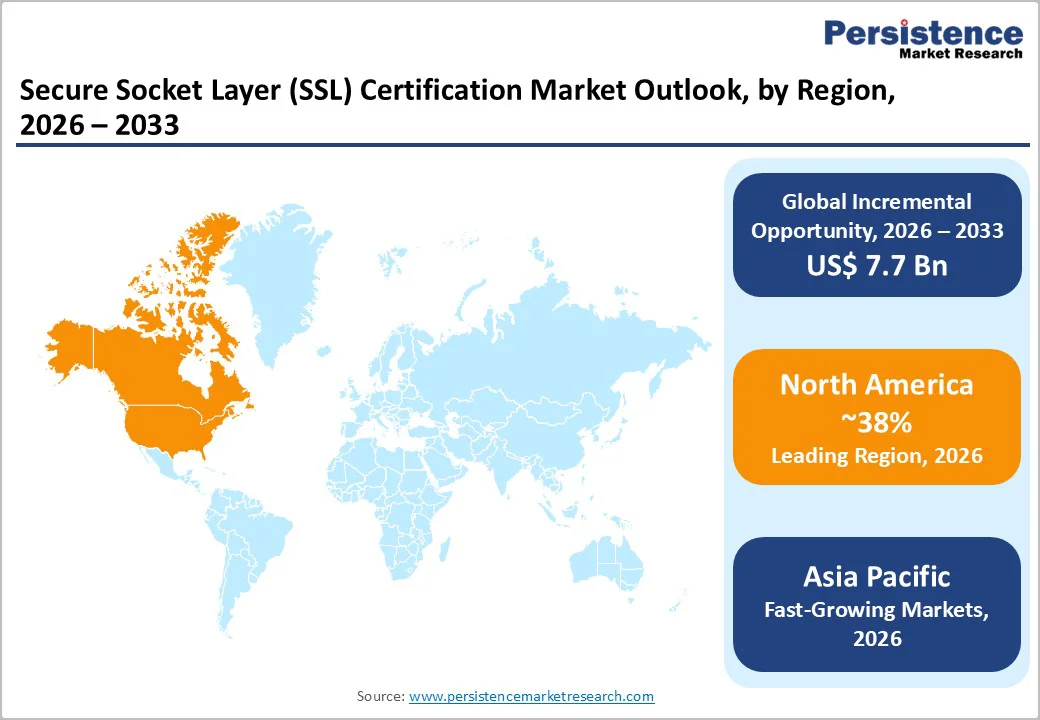

- Leading Region: North America leads the SSL certification market with around 38% share, supported by strict data protection regulations, advanced IT infrastructure, and high digital adoption across regulated industries.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, expanding at a 14.5% CAGR during 2026–2033, driven by rapid e-commerce growth, fintech expansion, and government-led digitalization initiatives.

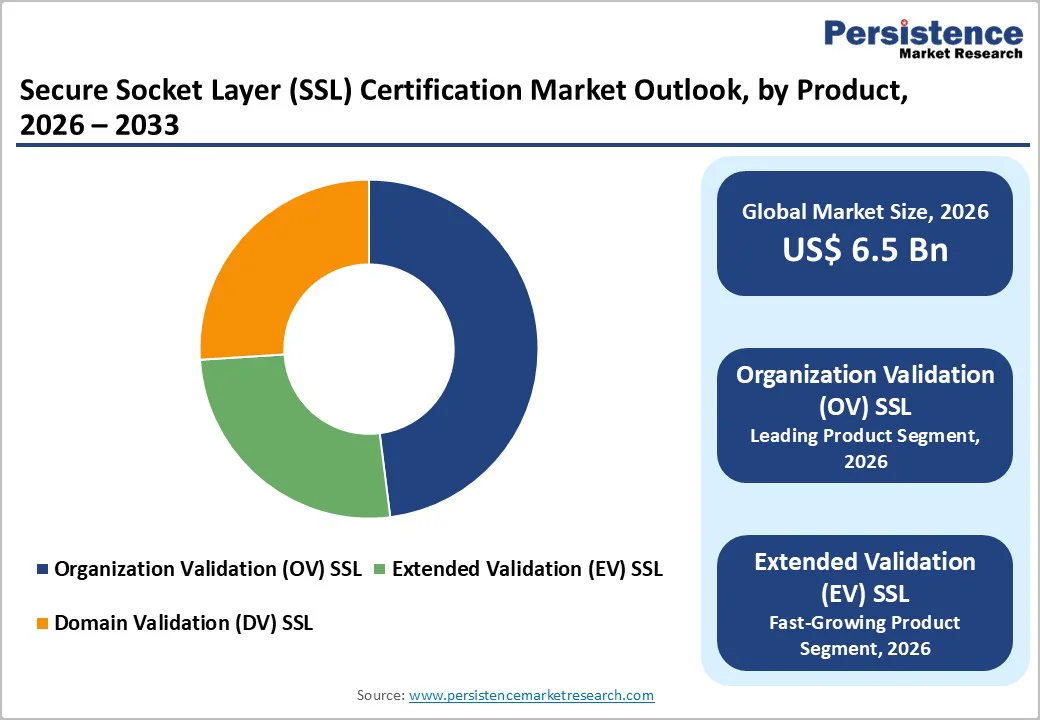

- Dominant Segment: Organization Validation (OV) SSL certificates dominate with approximately 45% market share, as enterprises prefer a balance between security assurance and organizational credibility.

- Fastest-Growing Segment: Extended Validation (EV) SSL certificates are the fastest-growing segment at a 12.8% CAGR, driven by rising demand for high-trust digital transactions in finance, e-commerce, and government services.

- Key Market Opportunity: AI-enabled and automated certificate lifecycle management presents the strongest opportunity, with growing enterprise adoption aimed at reducing downtime, ensuring compliance, and improving operational efficiency.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 6.5 Billion |

| Market Value Forecast (2033F) | US$ 14.2 Billion |

| Projected Growth CAGR (2026-2033) | 11.8% |

| Historical Market Growth (2020-2025) | 14.1% |

Market Dynamics

Market Growth Drivers

Increasing Cyber Threats and Data Breach Incidents

The surge in cyber-attacks and data breaches has emerged as the primary catalyst propelling SSL certificate adoption across all organizational sizes and sectors. Recent research indicates that 725 data breaches affected 61.9 million patient records in healthcare alone during 2024, while the European Banking Authority’s annual risk assessment revealed that 89% of successful cyber attacks on financial services involved inadequate transport layer security. Organizations are increasingly mandated by regulators to implement robust encryption standards to protect sensitive customer information during transmission.

The Payment Card Industry Data Security Standard (PCI DSS) version 4.0, implemented in 2024, strengthened encryption requirements by mandating TLS 1.2 or higher for all card data transmission, creating immediate demand for enterprise-grade SSL certificates. This regulatory enforcement, combined with the astronomical costs of data breaches averaging millions of dollars in remediation and legal expenses, has convinced organizations that SSL certificate investment is economically justified and strategically essential for maintaining business continuity and customer confidence.

Cloud Computing Adoption and Digital Transformation Initiatives

The exponential growth of cloud computing has fundamentally transformed SSL certificate requirements across enterprise infrastructure. 94% of organizations with over 1,000 employees have now adopted cloud solutions, with enterprise cloud adoption continuing to accelerate globally. Each cloud migration project typically requires 15-20 SSL certificates for various microservices, APIs, and user interfaces, creating a multiplication effect that dramatically increases overall certificate demand. Government digitalization programs, including the OECD Digital Government Index 2024 showing 78% of government services now delivered online, have necessitated comprehensive SSL implementation across public sector digital platforms.

The India Digital Initiative and similar transformation programs across ASEAN nations are driving widespread SSL adoption requirements among government agencies, educational institutions, and private enterprises seeking to secure digital service delivery. Multi-cloud adoption remains prevalent with the average enterprise utilizing 2.02 cloud providers, while SaaS adoption has reached over 60% of organizations using more than 25 SaaS applications, each requiring secure encrypted connections and SSL-backed authentication mechanisms.

Market Restraints

Certificate Management Complexity and Operational Challenges

The increasing number of SSL certificates deployed across organizations has created substantial operational complexity in managing certificate lifecycles. Nearly 30% of security incidents stem directly from expired or misconfigured SSL certificates, representing a critical operational challenge for enterprises managing hundreds or thousands of certificates across distributed infrastructure. Traditional manual certificate management processes have become unscalable as maximum validity periods are reducing from one year to six months by 2026 and eventually to 47 days by 2029, requiring organizations to implement monthly renewal cycles instead of annual processes.

The certificate renewal process demands significant IT resources for tracking expiration dates, managing validation procedures, and coordinating deployments across multiple environments and cloud providers. Organizations lack centralized visibility across certificate inventories, with enterprises often unaware of all certificates deployed across their infrastructure, creating security blind spots and compliance vulnerabilities. The complexity is magnified in hybrid and multi-cloud environments where certificates are distributed across different providers and regions, making consistent management and compliance verification exceedingly difficult without specialized automation solutions.

Availability of Free SSL Certificates and Market Commoditization

The emergence of Let’s Encrypt as a dominant free certificate authority has fundamentally altered SSL certificate market dynamics and revenue models for commercial certificate providers. Let’s Encrypt currently maintains approximately 63.4% market share of all SSL certificates, having issued over 400 million active certificates with more than 299 million SSL certificates tracked on the internet as of January 2025. This free alternative has severely impacted the commercial SSL certificate market, particularly for basic Domain Validation (DV) certificates, as organizations increasingly question the rationale for paying $50-200 annually for functionality available at no cost.

The commoditization of basic SSL certificates has compressed profit margins for traditional certificate authorities, forcing them to focus on premium validation tiers like Extended Validation (EV) and Organization Validation (OV) certificates that command higher price points. Small and medium enterprises, representing a significant growth segment, predominantly prefer cost-effective DV certificates due to budget constraints, further constraining revenue opportunities for paid certificate providers and slowing overall market monetization despite growing adoption volumes.

Market Opportunities

Post-Quantum Cryptography and Quantum-Safe Transition

The anticipated threat posed by quantum computing has created a significant market opportunity for certificate authorities and PKI infrastructure providers offering post-quantum cryptography (PQC) solutions. NIST finalized foundational post-quantum cryptography standards in 2024, with enterprises beginning mass PQC assessments in 2025 to address twin deadlines for cryptographic migration and shorter certificate lifespans. Major technology platforms including Apple iMessage, Cloudflare, and Google Chrome have begun quietly rolling out PQC protection, signaling the beginning of industry-wide cryptographic transformation.

Organizations face a monumental task in assessing cryptographic inventories and building quantum-resistant infrastructure, with 90% of organizations allocating budgets for this transition, representing a substantial revenue opportunity for certificate authorities offering PQC-enabled certificates and migration consulting services. Standards bodies including IETF and the CA/Browser Forum are actively moving through standardization processes, with formal definitions for PQC versions of all major certificate types expected by the end of 2026. This transition represents a multi-year technical and financial commitment across all sectors, creating sustained demand for new certificate issuances, consulting services, and infrastructure upgrades to support quantum-safe communications.

Artificial Intelligence and Automated Certificate Lifecycle Management

The integration of artificial intelligence and machine learning into certificate management workflows represents one of the fastest-growing market segments, with 63% of global enterprises expected to integrate AI into certificate management by mid-2026. AI-powered tools are transforming traditional manual certificate management into intelligent, automated workflows that reduce human error, prevent service disruptions, and ensure continuous compliance with security policies. Machine learning models can now scan entire certificate inventories in milliseconds, identifying expired keys, chain errors, weak cipher suites, and anomalies that could indicate spoofing or misconfiguration long before they trigger browser security warnings.

Predictive certificate renewal workflows powered by AI reduce SSL-related downtime by up to 38% in enterprise environments while decreasing SSL-related incidents by 40% compared to manual oversight approaches. The shift toward shorter certificate validity periods makes automation increasingly essential, with organizations facing monthly renewal requirements by 2029 rather than annual processes, making manual management economically unfeasible at scale. Organizations implementing AI-driven certificate lifecycle management can save approximately 25% in maintenance overhead within two years while freeing security professionals to focus on strategic initiatives rather than routine certificate administration, creating compelling business cases for AI investment in certificate infrastructure.

Category-wise Insights

Organization Validation (OV) SSL Analysis

Organization Validation (OV) SSL certificates represent the leading segment in the SSL certification market, commanding approximately 45% market share in 2025, based on their balanced approach to security and business credibility requirements. OV certificates dominate enterprise adoption because they encrypt data while simultaneously verifying the requesting organization’s legitimacy, building measurable trust among users and stakeholders who increasingly demand organizational authentication beyond simple domain ownership verification. OV certificates have become the standard security offering for e-commerce sites handling sensitive customer data, financial institutions managing transaction processing, and enterprises delivering digital services where organizational trust directly impacts conversion rates and customer retention.

Application-wise Insights: Large Enterprises

Large Enterprises represent the dominant application segment in the SSL certification market, capturing approximately 52% market share in 2025, driven by their requirement for advanced SSL solutions supporting multi-domain protection and comprehensive identity assurance across complex digital infrastructure. Large enterprises increasingly deploy zero-trust security architectures requiring mutual TLS authentication for all service-to-service communications, dramatically multiplying SSL certificate requirements across microservices, APIs, cloud applications, and edge computing environments.

Enterprises managing thousands of certificates have become early adopters of AI-powered certificate lifecycle management solutions, automation platforms, and centralized certificate inventory management tools that prevent the service disruptions and security incidents associated with manual certificate administration. Fortune 500 companies including JPMorgan Chase, Bank of America, and Wells Fargo have collectively deployed over 50,000 SSL certificates across their digital infrastructure, according to certificate transparency logs, exemplifying the scale and strategic importance of SSL certificate management in large enterprise environments.

Regional Insights

North America Secure Socket Layer (SSL) Certification Market Trends and Insights

North America commands the largest regional share of the global SSL certification market at approximately 38%, fueled by strict data protection regulations including GDPR compliance requirements for organizations handling European customer data, HIPAA encryption mandates for healthcare providers, and PCI DSS requirements for payment processing entities. The United States leads the SSL industry with over 26 million SSL certificates deployed across its digital infrastructure, reflecting the mature adoption of encryption standards across financial services, healthcare, e-commerce, and government sectors. Regulatory frameworks including the Federal Financial Institutions Examination Council (FFIEC) guidance mandate strong encryption for financial customer data transmission, while the Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency (CISA) requires federal agencies to implement TLS 1.2 or higher for all external communications.

The region demonstrates strong innovation ecosystem dynamics with leading certificate authorities including DigiCert, GlobalSign, Sectigo, and emerging providers establishing significant market presence and competitive differentiation through advanced automation capabilities and zero-trust security model support. Healthcare digitalization accelerated following pandemic-driven telemedicine adoption, with the Department of Health and Human Services reporting 3,800% increase in telemedicine utilization during 2020-2021, creating massive demand for HIPAA-compliant SSL implementations across patient portals and remote care delivery platforms.

Europe Secure Socket Layer (SSL) Certification Market Trends and Insights

Europe maintains strong SSL certification market presence driven by comprehensive data protection frameworks including GDPR and advanced regulatory harmonization across European Union member states. The European Banking Authority’s Payment Services Directive 2 (PSD2) requires strong customer authentication for electronic payments, driving SSL certificate adoption across fintech and banking sectors throughout the continent. Germany, the United Kingdom, France, and Spain lead European adoption with sophisticated cybersecurity ecosystems and stringent compliance requirements creating sustained demand for enterprise-grade SSL solutions among financial institutions, healthcare providers, and government agencies.

European Central Bank implemented new signature certificates for euro short-term rate (€STR) financial data dissemination, strengthening digital trust in financial systems and demonstrating government-level commitment to secure digital infrastructure. Open banking initiatives across European markets have created new API security requirements, with financial institutions implementing comprehensive certificate strategies protecting customer data during third-party integrations. DEKRA introduction of Digital Trust Services combining cybersecurity, functional safety, and AI testing reflects European emphasis on comprehensive digital trust solutions beyond basic SSL certification.

Asia Pacific Secure Socket Layer (SSL) Certification Market Trends and Insights

Asia Pacific represents the fastest-growing SSL certification regional market with approximately 20% share and CAGR of 14.5% during 2026-2033, driven by rapid digital transformation, e-commerce expansion, and government-led cybersecurity awareness programs across the region. Countries including China, India, Japan, and Southeast Asian nations are experiencing unprecedented digital economy growth, with e-commerce penetration creating substantial demand for payment security solutions and consumer-facing website encryption. India’s Digital India initiative, coordinated by the Ministry of Electronics and Information Technology, promotes SSL adoption across government services and private sector organizations. India’s IT services sector, representing over 7.4% of GDP according to NASSCOM data, drives significant SSL certificate demand to protect client data and maintain international security certifications.

Singapore’s Smart Nation program includes cybersecurity components mandating SSL implementation across government digital services, while the Monetary Authority of Singapore’s Technology Risk Management Guidelines require financial institutions implementing strong encryption. Southeast Asian countries experience accelerating SSL adoption driven by online retail expansion, with regional e-commerce growing exponentially and creating urgent need for consumer confidence-building security measures.

Competitive Landscape

Market Structure Analysis

The SSL certification market demonstrates fairly concentrated structure with six certificate authorities collectively issuing approximately 90% of all SSL certificates deployed globally. Let’s Encrypt dominates the overall market with 63.4% share as of June 2025, while GlobalSign maintains 23.1% share, and Sectigo holds 6.2% share, with GoDaddy Group and DigiCert Group capturing 4.1% and 2.8% respectively, leaving smaller authorities including Actalis, Certum, Secom Trust, and SSL.com each holding less than 1% individual market share. The concentration is less dramatic among top 1,000 most popular websites, where GlobalSign has achieved dominant positioning with certificate authorities competing intensely on advanced features, enterprise support, and specialized solutions rather than basic domain validation services. Market consolidation continues with major players expanding through strategic acquisitions and technological alliances, as evidenced by SSL.com acquisition of VikingCloud’s digital certificate customer portfolio in November 2025, and J.P. Morgan’s migration from Entrust to DigiCert for host-to-host SSL support, reflecting ongoing vendor consolidation and capability-driven switching.

Key market differentiation strategies employed by leaders include AI-powered certificate lifecycle management automation, post-quantum cryptography support, zero-trust security architecture integration, and expanded service portfolios beyond basic certificate issuance. DigiCert achieved record growth in FY2025 with 67% increase in customers purchasing both certificates and additional security services, reflecting successful product expansion strategy and cross-selling effectiveness. Emerging business model trends include managed service provider partnerships, cloud-native certificate management platforms optimized for containerized environments and DevOps integration, and subscription-based pricing models replacing traditional per-certificate pricing. Regional providers including Tencent Cloud in China and Alibaba Cloud in broader Asia are gaining traction by offering localized support, competitive pricing aligned with regional purchasing power, and integration with local payment and compliance ecosystems. Smaller specialized providers including ZeroSSL, SSL.com, and cloud-native platforms are capturing market segments through focused differentiation on cost-effectiveness, automation-first approaches, and specific use case optimization rather than attempting to compete on broad feature sets.

Key Market Developments

- November 2025: SSL.com, a Houston-based Certification Authority, acquired VikingCloud’s digital certificate customer portfolio, expanding its United States customer base and enhancing service continuity for certificate users while consolidating market position among regional providers offering competitive pricing and specialized support services.

- October 2025: J.P. Morgan updated Host-to-Host SSL support infrastructure by switching Certificate Authorities from Entrust to DigiCert, reflecting ongoing adaptations in financial sector PKI infrastructure and demonstrating market dynamics where enterprise customers continuously evaluate provider capabilities and business continuity positioning based on evolving security requirements.

- September 2025: DigiCert reported significant cybersecurity M&A activity with 40 deals announced during the period, indicating heightened consolidation and investment throughout the certificate management and enterprise PKI ecosystem as market participants seek expanded capabilities, geographic reach, and technology differentiation through strategic acquisitions and partnerships.

Companies Covered in Secure Socket Layer (SSL) Certification Market

- Asseco Data Systems S.A.

- ACTALIS S.p.A.

- GlobalSign

- Comodo Security Solutions Inc.

- Entrust Corporation

- IdenTrust Inc.

- GoDaddy Operating Company, LLC

- Secom Trust

- StartCom

- Symantec

- Let’s Encrypt

- Network Solutions

- TWCA

- Trustwave

- T-Systems

- DigiCert Inc.

- Sectigo

- SSL.com

- Cloudflare

- Amazon Web Services (AWS)

Frequently Asked Questions

The global SSL Certification Market is expected to reach approximately US$ 6.5 billion in 2026.

Rising cyber-attacks, stringent data protection regulations, expanding cloud adoption, and government digitalization initiatives are the key demand drivers.

North America is expected to lead the market with around 38% share during the forecast period.

AI-driven and automated certificate lifecycle management represents the largest growth opportunity.

Major players include Let’s Encrypt, GlobalSign, Sectigo, GoDaddy, and DigiCert, alongside emerging providers such as Cloudflare and ZeroSSL.