- Hardware & Software IT Services

- Secure Web Gateway Market

Secure Web Gateway Market Size, Share, and Growth Forecast 2026–2033

Secure Web Gateway Market by Component (Solutions, Services), by Deployment (Cloud-based, On-premises, Hybrid), by Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), Industry (BFSI, IT & Telecom, Government & Defense, Healthcare, Retail & E-commerce, Manufacturing, Education, Media & Entertainment, Others), by Regional Analysis, 2026–2033

Global Secure Web Gateway Market Size and Trend Analysis

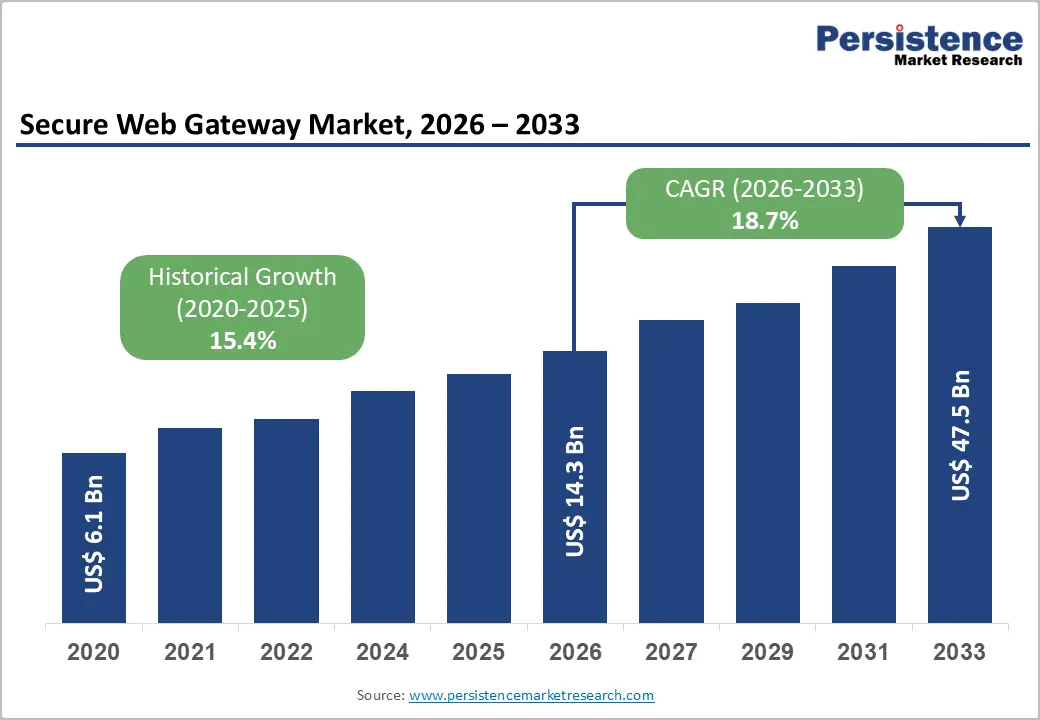

The global secure web gateway market size is expected to be valued at US$ 14.3 billion in 2026 and is projected to reach US$ 47.5 billion by 2033, growing at a CAGR of 18.7% between 2026 and 2033.

This trajectory reflects intensifying regulatory pressure around data privacy and acceptable-use compliance, the rapid migration of corporate workloads to cloud environments, and the persistent escalation of sophisticated web-borne threats, including malware, ransomware, and phishing campaigns. Enterprises are actively prioritizing Secure Web Gateway investments as a foundational layer within broader Security Service Edge (SSE) and Secure Access Service Edge (SASE) architectures, reinforcing long-term demand visibility throughout the forecast horizon.

Key Industry Highlights:

- Leading Component: Solutions dominate the market with over 70% share in 2026, valued at more than US$ 10.01 Bn, driven by strong enterprise demand for integrated capabilities such as URL filtering, SSL inspection, advanced threat protection, and data loss prevention (DLP).

- Leading Deployment: On-premises deployment holds over 30% market share in 2026, valued at more than US$ 4.29 Bn, due to strong demand from regulated industries requiring strict data control, customization, and compliance adherence.

- Fastest Growing Deployment: Cloud-based deployment is the fastest-growing segment, driven by the rapid adoption of SaaS, hybrid work models, and the need for scalable, location-independent security aligned with SASE architectures.

- Leading Enterprise Size: Large Enterprises dominate with over 64% market share in 2026, valued at more than US$ 9.15 billion, supported by complex IT environments, higher exposure to sophisticated cyber threats, and the need for centralized policy enforcement.

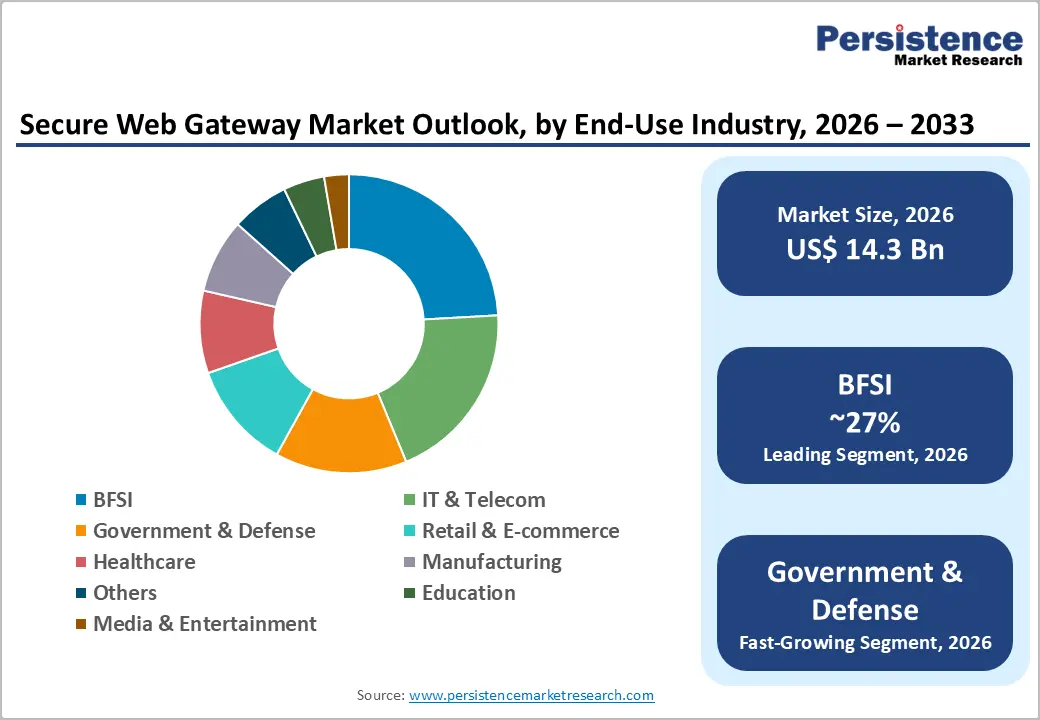

- Leading End-user: BFSI sector leads with approximately 27% market share in 2026, valued at around US$ 3.86 billion, driven by the need to protect sensitive financial data and comply with stringent regulations such as PCI-DSS, SOX, and DORA.

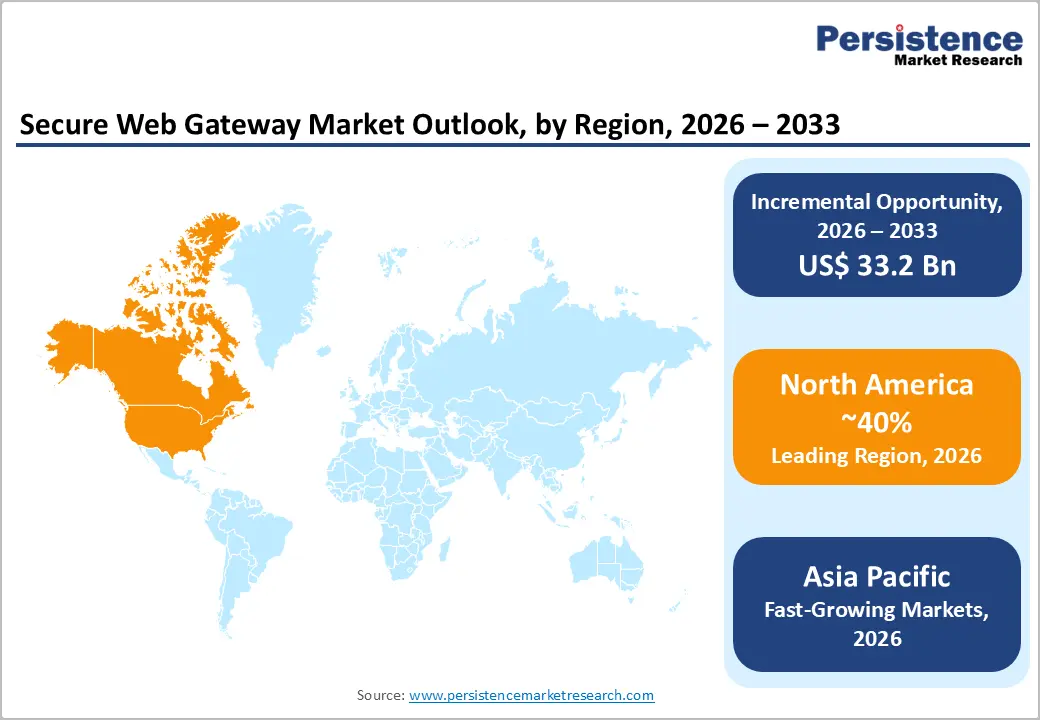

- Leading Region: North America leads with over 40% market share in 2026, valued at more than US$ 5.72 billion, supported by a mature cybersecurity ecosystem, strong regulatory frameworks, and the presence of leading vendors.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a CAGR of 24.1%, driven by rapid cloud adoption, expanding digital economies in China, India, and Southeast Asia, and tightening data protection regulations.

Market Dynamics

Drivers – Sophistication of Web-Borne Cyber Threats

The most immediate commercial consequence of rising cyber threat volumes is that organisations no longer treat web filtering as a peripheral IT function; it is now a board-level risk imperative. Web-based attacks, including credential phishing, drive-by downloads, and command-and-control traffic, account for a disproportionate share of enterprise breach entry points, compelling security teams to deploy advanced Secure Web Gateway solutions with real-time threat intelligence and SSL/TLS inspection capabilities. Regulatory frameworks such as the EU's NIS2 Directive, HIPAA in the United States, and the UK's Cyber Essentials Plus scheme are mandating demonstrable web security controls, creating a compliance-driven procurement cycle that sustains market demand regardless of broader IT budget pressures.

Accelerated Adoption of Cloud Infrastructure and Hybrid Work Models

The shift toward hybrid and remote work, which became entrenched following the 2020–2022 global workplace disruption, fundamentally changed how enterprises must secure internet-bound traffic. Traditional perimeter-based security models relying on traffic backhauling through on-premises appliances introduce latency and complexity incompatible with distributed workforces accessing SaaS (Software-as-a-Service) applications directly from unmanaged networks. Cloud-delivered Secure Web Gateway solutions address this gap by enforcing consistent policy at the point of cloud egress, regardless of user location, which explains the surge in cloud deployment adoption across mid-market and enterprise segments.

Restraints - High Implementation Complexity and Integration Challenges with Legacy Infrastructure

Large enterprises operating decades-old network architectures, including MPLS (Multiprotocol Label Switching) backbones, legacy firewalls, and on-premises identity management systems, encounter significant compatibility, configuration, and staff-retraining burdens during deployment. These integration challenges extend procurement cycles, inflate total-cost-of-ownership estimates beyond initial budget allocations, and generate hesitancy particularly among mid-market buyers with limited in-house security expertise. Vendors that fail to invest in simplified onboarding, pre-built integrations, and managed services capabilities risk losing deals to competitors with lower deployment friction, even when their core technology is superior.

Data Privacy Concerns and Regulatory Constraints Around SSL Inspection

Inspecting encrypted web traffic, essential for detecting malware hidden within HTTPS sessions, requires decrypting and re-encrypting user communications, an activity that conflicts with employee privacy regulations across multiple jurisdictions, including the General Data Protection Regulation (GDPR) in Europe and equivalent statutes in Brazil (LGPD) and California (CCPA). Organisations operating across multiple regulatory geographies must navigate inconsistent compliance requirements, creating legal risk that slows deployment decisions and sometimes results in constrained feature utilisation even after purchase. This disproportionately affects multinational enterprises and public sector organisations, where data handling accountability standards are strictest.

Opportunities - Convergence with SASE and Zero-Trust Network Access (ZTNA) Frameworks

SASE integrates Secure Web Gateway, Cloud Access Security Broker (CASB), Zero-Trust Network Access (ZTNA), and SD-WAN capabilities into a unified, cloud-delivered platform and vendors capable of offering Secure Web Gateway as part of a cohesive SASE stack command significantly higher contract values and stronger renewal economics than standalone gateway sellers. Enterprises seeking to consolidate their security vendor portfolios, reduce integration overhead, and achieve consistent policy enforcement across all traffic types represent an addressable buyer population that is actively budgeted and actively evaluating platform providers. Vendors should prioritise native SASE integration, co-sell partnerships with SD-WAN providers, and modular licensing models that allow buyers to expand from gateway entry points into full-stack SASE over time.

Edge Computing & Branch Office Transformation

The rise of edge computing and the transformation of branch offices is creating strong demand for decentralized security solutions, as enterprises move away from centralized data centers to distributed IT environments. With the adoption of SD-WAN and edge infrastructure, branch locations now access cloud applications directly rather than routing traffic through headquarters, increasing exposure to web-based threats. Secure Web Gateways (SWGs) are increasingly being deployed at the edge or delivered via the cloud to ensure consistent security policies across all locations. This shift creates an opportunity for vendors to offer integrated SWG + SD-WAN solutions that provide secure, low-latency connectivity.

Category-wise Analysis

Component Insights

Solutions segment accounts for 70.0% of the global Secure Web Gateway market in 2026, exceeding US$10.01 billion, driven by enterprises’ need to enforce web security policies, prevent data exfiltration, and mitigate increasingly sophisticated cyber threats. As organizations face rising risks from encrypted traffic, phishing, and cloud-based attacks, demand for integrated capabilities such as URL filtering, SSL inspection, advanced threat protection, and DLP has intensified. This has led to the adoption of unified secure web gateway platforms that consolidate multiple security functions, increasing average deal sizes and reinforcing the dominance of the solutions segment.

Services are growing at a significant rate due to the need to manage operational complexity and address cybersecurity talent shortages. Organizations, particularly SMEs and distributed enterprises, increasingly rely on managed security service providers (MSSPs) to deploy, monitor, and optimize solutions. As each new solution deployment requires ongoing policy tuning, threat monitoring, and compliance management, services revenue is expanding in a recurring, annuity-like model. While solutions continue to dominate in absolute revenue terms, services growth is being structurally supported by the increasing need for outsourced security operations.

Deployment Insights

On-premises segment accounts for over 30.0% market share in 2026, exceeding US$4.29 billion value, as enterprises’ need for strict data control, regulatory compliance, and internal policy enforcement. Organizations in highly regulated sectors such as BFSI and government continue to rely on on-premises deployments to ensure data residency, maintain visibility into encrypted traffic, and achieve deep customization of security policies. Significant legacy infrastructure investments and the need to integrate with existing security stacks reinforce continued preference for on-premises models.

Cloud-based deployment model is the fastest growing segment, driven by the need for scalable, location-independent security aligned with SaaS adoption and hybrid work environments. As enterprise traffic increasingly originates outside traditional network perimeters, organizations require security that can be delivered consistently across distributed users and devices. The shift toward SASE architectures reflects this need for cloud-native, edge-delivered protection. Improvements in SSL inspection, threat intelligence integration, and global point-of-presence coverage are reducing earlier concerns around visibility and control, accelerating enterprise confidence in cloud deployments.

Enterprise Size Insights

Large Enterprises account for more than 64.0% of the global Secure Web Gateway market in 2026, reaching over to US$ 9.15 billion, due to their need to secure highly complex, distributed IT environments and protect against large-scale cyber threats. With thousands of users, devices, and access points, large organizations face significant risk from web-borne attacks, where even a single compromised session leads to widespread lateral movement across the network. This scale of exposure necessitates advanced web security capabilities, centralized policy enforcement, and continuous monitoring, justifying substantial investment in solutions.

Small and Medium Enterprises (SMEs) represent the fast-growing segment, driven by the need for enterprise-grade security without the burden of high upfront costs or dedicated security teams. The adoption of cloud-delivered solutions, offered through subscription-based pricing models, enables SMEs to access advanced threat protection, URL filtering, and data security capabilities with minimal infrastructure requirements. As cyber threats increasingly target smaller organizations and regulatory expectations expand, SMEs are prioritising scalable and easy-to-deploy security solutions. While large enterprises continue to dominate in absolute spending, SME growth is being driven by rising awareness, affordability, and the need to transition from basic network security to more comprehensive web protection.

Industry Insights

BFSI accounts for approximately 27.0% of market share in 2026 driven by the critical need to protect highly sensitive financial data and comply with stringent regulatory frameworks. Financial institutions operate in an environment where web-based threats such as phishing, credential theft, and data exfiltration can have immediate financial and systemic consequences. Compliance mandates, including PCI-DSS, SOX, DORA, and central bank cybersecurity guidelines, effectively require the deployment of advanced web security controls.

Government & Defense is the fast-growing segment, due to the need to defend against increasingly sophisticated state-sponsored cyber threats and to secure critical national infrastructure. Governments worldwide are implementing zero-trust security frameworks and emphasizing digital sovereignty, requiring strict control over data flows and user access across distributed environments. These needs are accelerating the adoption of solutions that provide centralized policy enforcement, visibility into encrypted traffic, and protection for remote and mobile workforces.

Regional Insights

North America Secure Web Gateway Market Trends and Insights

North America dominates the secure web gateway market with over 40.0% global share in 2026, valued at more than US$ 5.72 billion, firmly establishing itself as the leading regional market. This leadership is driven by a high concentration of technology-intensive enterprises and the world’s most mature cybersecurity spending ecosystem. A strong regulatory framework, including mandates such as HIPAA, SOX, CCPA, and the NIST Cybersecurity Framework, ensures consistent demand across key sectors. The presence of leading cybersecurity vendors and a well-developed partner ecosystem accelerates solution adoption. Growth is fueled due to the increasing adoption of cloud-delivered SASE models and AI-integrated threat detection capabilities.

The U.S. secure web gateway market accounts for approximately 87.0% of market share in 2026, over US$ 4.98 billion by value, due to the country’s role as both the largest consumer and innovation hub. The demand is supported by the presence of Fortune 500 companies, federal zero-trust security mandates, and extensive compliance requirements across industries. A robust Managed Security Service Provider (MSSP) ecosystem is enabling broader adoption among mid-sized enterprises.

Europe Secure Web Gateway Market Trends and Insights

Europe accounts for over 26.0% of the global Secure Web Gateway (SWG) market in 2026, reaching US$ 3.72 billion, driven primarily by one of the world’s most stringent regulatory ecosystems. Frameworks such as GDPR, NIS2 Directive, and DORA are transforming SWG adoption from a discretionary IT spend into a compliance necessity across enterprises. Rising digital sovereignty concerns are pushing demand for EU-based data residency solutions. NIS2 enforcement timelines will further accelerate adoption across both large enterprises and previously underpenetrated segments.

Germany holds the largest share at over 23.0%, reaching a value of US$0.86 billion, supported by its strong industrial base and high exposure to cyber risks in manufacturing and financial services. Strict frameworks such as BSI guidelines and BDSG reinforce compliance-driven demand. The United Kingdom reaching value of US$0.71 billion by 2026, led by its mature financial ecosystem and proactive cybersecurity strategies under the National Cyber Strategy and NCSC guidance. France accounts for approximately US$0.56 billion in value by 2026, where government-led initiatives, including ANSSI regulations and national cyber strategies, are driving steady adoption, particularly across public sector and regulated industries.

The Rest of Europe contributes over 20.0% market share with a surpassing value of US$ 0.74 billion in 2026, encompassing emerging high-growth markets such as the BENELUX, Nordics, and Poland etc. These countries are witnessing a transition from traditional perimeter security to advanced SWG solutions, largely driven by NIS2 compliance requirements. The Netherlands benefits from its position as a data centre hub, while Poland shows strong uptake due to manufacturing and IT services expansion.

Asia Pacific Secure Web Gateway Market Trends and Insights

Asia Pacific accounts for more than 24.0% of the global Secure Web Gateway market in 2026, valued at approximately US$ 3.43 billion, and is the fastest-growing region with a projected CAGR of 24.1% through 2033, driven by rapid cloud infrastructure expansion across China, India, and Southeast Asia, along with tightening regulatory frameworks such as India’s DPDP Act, China’s Cybersecurity Law, and Singapore’s Cybersecurity Act. The sharp increase in distributed workforces and internet-connected enterprise users is accelerating the need for consistent web security.

China holds the largest share in the region, over 33.0%, driven by strong government-led digital transformation initiatives and cybersecurity regulations such as MLPS 2.0. The demand is primarily institutional, supported by state-owned enterprises and financial institutions requiring advanced web filtering and data protection capabilities. Japan accounts for over US$ 0.51 Billion value in 2026, supported by its mature IT infrastructure and national cybersecurity strategy, particularly across the manufacturing and financial services sectors. Enterprises in Japan emphasize vendor stability, long-term support, and compliance with METI guidelines, ensuring steady demand.

India is expected to exceed the value of US$0.65 billion by 2026, & is among the fastest-growing countries, fueled by its expanding digital economy, implementation of the DPDP Act, and a large IT services workforce requiring secure cloud access. Growth is further supported by the rise of fintech, e-commerce, and SaaS adoption across enterprises and SMEs. South Korea contributes over 17.0%, driven by its highly digitalized economy and strict regulatory frameworks such as PIPA. Large conglomerates and government-led zero-trust initiatives are key demand drivers, with continued growth expected as cloud adoption expands across enterprise supply chains.

Competitive Landscape

The global secure web gateway market operates as a moderately consolidated competitive environment dominated by a tier of global platforms that compete primarily on technology depth, SASE integration breadth, and global cloud infrastructure scale. Below this platform tier, a secondary tier of specialised vendors competes on vertical-specific compliance capabilities, hybrid deployment flexibility, and established channel relationships. Differentiation increasingly flows from AI-driven threat detection, zero-day exploit response speed, and the granularity of real-time policy enforcement areas, where R&D investment velocity directly determines market share trajectory.

Key Developments:

- In March 2026: Palo Alto Networks launched Prisma AIRS 3.0, an advanced platform designed to secure autonomous AI systems by providing visibility, risk assessment, and real-time protection. The solution helps enterprises monitor and control AI agent behavior across applications and environments, addressing emerging risks like prompt injection and unauthorized actions.

- In June 2024: Broadcom Inc. announced that its Symantec Cloud Secure Web Gateway has achieved FedRAMP authorization, enabling secure deployment across U.S. government agencies. This milestone strengthens its position in the cloud-based Secure Web Gateway market while supporting adoption in highly regulated sectors.

Companies Covered in Secure Web Gateway Market

- Zscaler

- Cisco Systems

- Palo Alto Networks

- Netskope

- Fortinet

- Check Point Software Technologies

- Broadcom

- Cloudflare

- Forcepoint

- Trend Micro

- Sophos

- McAfee

- IBM

- Citrix

Others

Frequently Asked Questions

The global Secure Web Gateway market is valued at US$ 14.3 Billion in 2026 and is projected to reach US$ 47.5 Billion by 2033, expanding at a CAGR of 18.7%, driven by rising cloud adoption and the shift toward zero-trust and SASE architecture.

The increasing frequency and sophistication of web-based cyber threats, alongside the expansion of hybrid and remote work models. These are pushing enterprises to replace traditional perimeter security with cloud-delivered, identity-centric protection.

Solutions segment holds the largest share of over 70% in 2026, as enterprises prioritize advanced capabilities like URL filtering, threat protection, and data loss prevention. Continuous innovation and integration into SASE platforms further strengthen its dominance.

North America leads with more than 40% share & US$ 5.7 Bn value in 2026, supported by strong cybersecurity spending, and the presence of major security vendors. Regulatory pressure and high threat awareness also reinforce market leadership.

The rapid adoption of SASE frameworks, AI-driven threat detection, and securing edge environments and branch offices are creating opportunities for the secure web gateway market.