- Telecommunications

- Secure Mobile Communications Market

Secure Mobile Communications Market Size, Share, and Growth Forecast 2026 - 2033

Secure Mobile Communications Market by Solution Type (Hardware, Software, Services), by Technology (Encryption Protocols, Secure Voice Communication, Secure Messaging, Virtual Private Network, Secure Application Development, Others), Deployment Type (On-Premise, Cloud-Based, Hybrid), by Industry (Government, Military, Corporate, Healthcare, Finance), and Regional Analysis, 2026 - 2033

Secure Mobile Communications Market Size and Trend Analysis

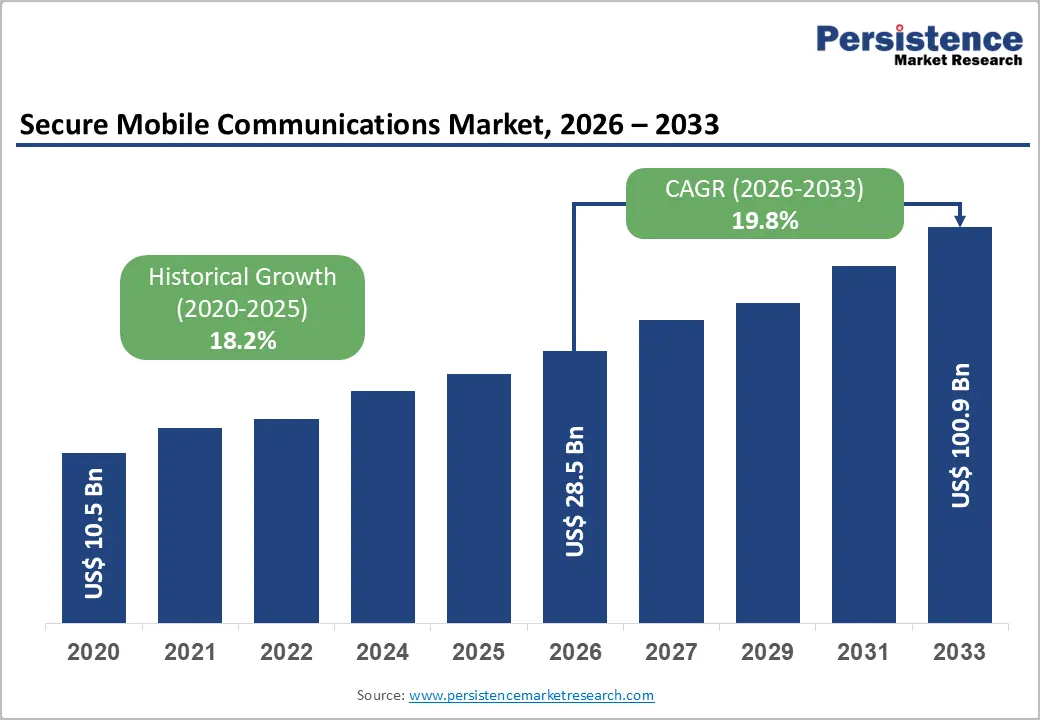

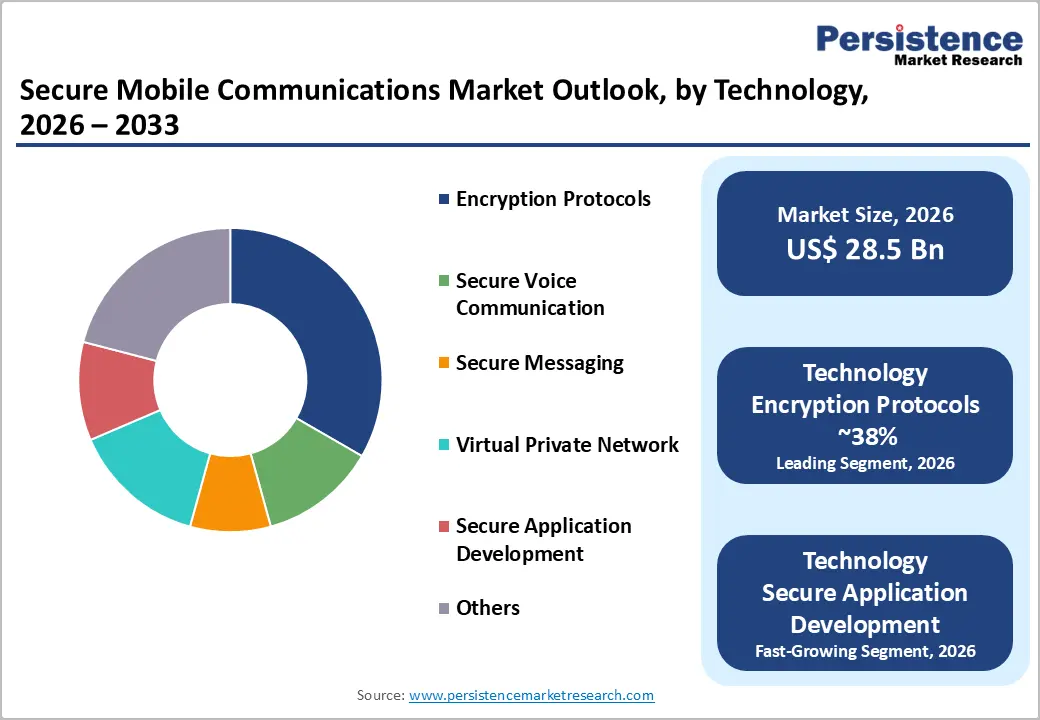

The global secure mobile communications market size is projected to reach US$ 28.5 billion in 2026 and is expected to grow to US$ 100.9 billion by 2033, registering a CAGR of 19.8% in the forecast period from 2026 to 2033.

This growth is driven by rising cybersecurity threats and stringent regulatory requirements across sectors. Governments, military organizations, healthcare organizations, and financial organizations are increasingly investing in secure communication solutions to protect against cyberattacks, data breaches, and espionage. The shift toward remote work and mobile-first operations, fueled by digital transformation, has further intensified demand for encrypted solutions, enabling secure access to sensitive networks from anywhere in the world.

Key Market Highlights

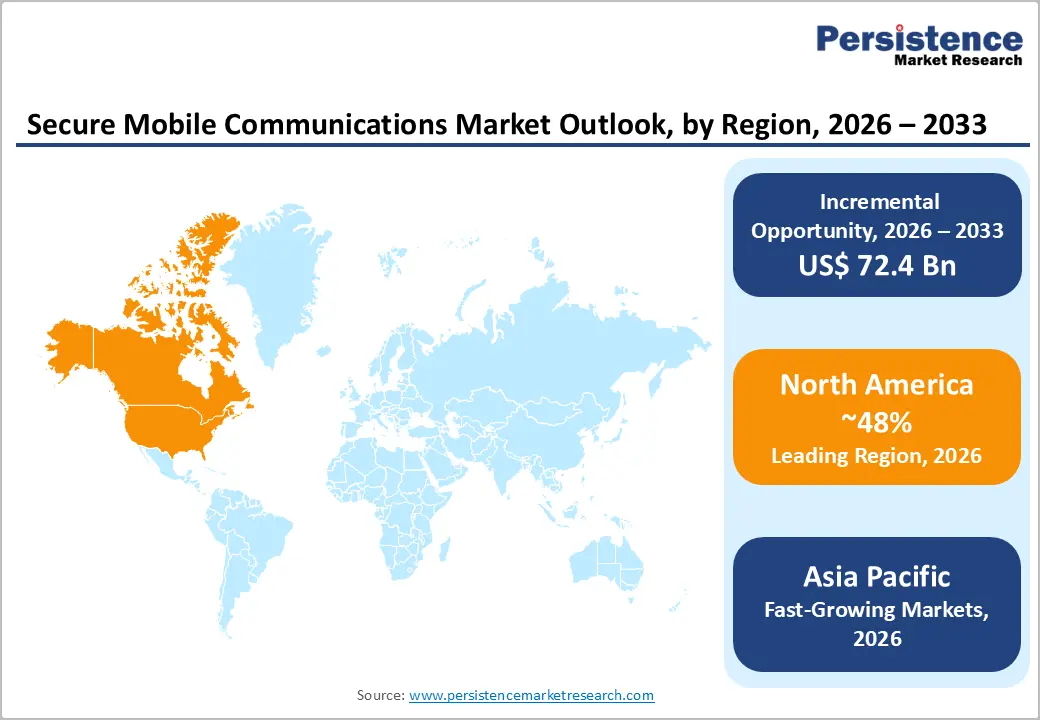

- Leading Region: North America leads with 48% market share, driven by government defense budgets, federal cybersecurity mandates, and enterprise security investments.

- Fastest-Growing Region: Asia Pacific grows fastest with 27% CAGR, fueled by digital transformation, rising defense spending, and expanding mobile penetration.

- Dominant Segment: Software solutions hold 45% market share, prioritized for scalable cloud platforms, encrypted messaging, and mobile device management systems.

- Fastest Growing Segment: Post-Quantum Cryptographic Algorithms are the fastest-growing with 37.6% CAGR through 2030, driven by quantum computing threats and government migration mandates.

- Key Market Opportunity: Quantum-safe cryptography migration services and solutions offer significant growth as organizations implement post-quantum standards, consulting, hardware, and software updates by 2035.

| Key Insights | Details |

|---|---|

|

Secure Mobile Communications Market Size (2026E) |

US$ 28.5 billion |

|

Market Value Forecast (2033F) |

US$ 100.9 billion |

|

Projected Growth CAGR(2026-2033) |

19.8% |

|

Historical Market Growth (2020-2025) |

18.2% |

Market Dynamics

Market Growth Drivers

Escalating Sophistication of Cyber Threats and Rising Mobile Data Breaches Fueling Enterprise Adoption of Secure Communications

Organizations are grappling with an unprecedented surge in advanced cyber attacks, including spear-phishing, malware, and persistent threats targeting mobile devices. The Cybersecurity and Infrastructure Security Agency (CISA) reports that commercial spyware operators increasingly exploit encrypted messaging apps across multiple regions. Government agencies, defense contractors, and corporations recognize that mobile communication channels are prime targets for cyber espionage and require immediate mitigation measures.

This heightened risk of sensitive information compromise has accelerated investments in enterprise-grade encryption solutions. Businesses are adopting secure voice, messaging, and data communication systems employing military-grade encryption protocols. By ensuring data integrity and confidentiality during transmission and storage, organizations across industries strengthen their cybersecurity posture, mitigate threats, and maintain operational continuity in an increasingly mobile-dependent business environment.

Stringent Global Regulatory Compliance and Data Protection Mandates Driving Enterprise Investments in Encrypted Mobile Communications

Global regulatory frameworks such as GDPR, HIPAA, PCI DSS, and emerging national cybersecurity standards compel organizations to adopt robust encryption for all sensitive communications. GDPR enforcement has led to widespread use of secure enterprise messaging applications with end-to-end encryption, audit trails, and complete transparency. Healthcare providers must comply with HIPAA rules by encrypting protected health information during transmission and storage, while financial institutions must follow PCI DSS guidelines to safeguard transaction communications.

These legal and compliance pressures translate into mandatory technology investments, creating sustained demand for secure communication solutions. Enterprises, government agencies, and regulated industries are increasingly deploying encrypted voice, messaging, and data systems to ensure privacy, compliance, and trust in mobile-first business models while mitigating regulatory and reputational risks across global operations.

Market Restraints

High Capital Investment Requirements and Complex Integration Challenges Slowing Secure Mobile Communication Deployment

Implementing enterprise-grade secure mobile communication solutions demands significant investment in hardware, software licenses, employee training, and ongoing maintenance. Organizations must integrate new security systems with legacy infrastructure, which requires specialized IT expertise and often causes operational disruptions during rollouts. SMEs face particular challenges due to constrained budgets and limited cybersecurity resources, making large-scale deployments difficult.

The complexity of integrating secure platforms with unified communications, mobile device management, and enterprise resource planning systems further increases implementation timelines and total cost of ownership. As a result, many budget-constrained organizations delay or abandon modernization initiatives. These financial and technical barriers remain significant restraints to market growth despite the pressing need for enhanced mobile security.

Limited End-User Adoption Due to Usability Concerns and Device Compatibility Issues

End-users often resist enterprise-mandated secure communication apps because they introduce additional steps for authentication, key management, and device verification, which disrupt daily workflows. Compatibility challenges also arise when employees use multiple device types, operating systems, and versions, leading to fragmented secure communication environments and operational friction.

Moreover, spyware campaigns targeting encrypted messaging apps like Signal, WhatsApp, and Telegram have eroded user confidence in platform security. Organizations frequently encounter employee pushback, shadow IT usage of consumer apps, and reluctance to adopt new workflows. This limited adoption reduces the overall effectiveness of security solutions, creating a barrier to realizing the full benefits of enterprise-grade encrypted communication systems.

Market Opportunities

Emerging Opportunities in Quantum-Safe Cryptography and Post-Quantum Secure Communication Solutions

The advent of quantum computing poses a significant threat to traditional encryption methods, creating an urgent market opportunity for providers of post-quantum cryptography. The UK's NCSC mandates organizations to complete quantum-safe migration discovery by 2028, prioritize critical migrations by 2031, and fully transition by 2035. Similarly, U.S. NIST guidelines require phasing out 112-bit security algorithms and adopting quantum-resistant systems by 2035.

Leading companies like Thales, IBM, and STC Group are pioneering quantum-resistant encryption technologies and collaborations, preparing telecommunications and enterprise sectors for post-quantum security. Organizations worldwide are initiating quantum-safe assessments, generating demand for consulting, software upgrades, hardware replacements, and managed services. This emerging market presents substantial revenue growth potential for solution providers specializing in quantum-resistant secure communication technologies.

Expanding Market Potential Driven by Remote Work and Distributed Workforce Adoption

The global shift toward remote and hybrid work models is significantly increasing demand for secure mobile communication solutions. With over 80% of organizations adopting BYOD policies, and 70% of BYOD cases involving unmanaged devices, enterprises must provide secure access to corporate systems while maintaining compliance and protecting sensitive data.

This trend is driving adoption of cloud-based unified endpoint management, secure mobile applications, and encrypted voice and video conferencing solutions. Companies like BlackBerry are enhancing their secure communication suites to support mission-critical enterprise communications for distributed teams. Cloud-native, scalable solutions are becoming a preferred choice, offering convenience, cost-efficiency, and robust security, particularly for mid-market and geographically dispersed organizations seeking alternatives to complex on-premises infrastructure.

Category-wise Analysis

Solution Type Insights

The Software segment leads the secure mobile communications market with approximately 45% market share, driven by encrypted messaging apps, secure collaboration platforms, and mobile device management software. Hardware solutions, including secure phones and hardware security modules, remain critical for government and military users requiring certified cryptography, while services support implementation, consulting, and maintenance needs across industries.

The fastest-growing segment is Cloud-based software solutions, offering flexibility, rapid deployment, and simplified licensing. These solutions appeal to mid-market and enterprise organizations seeking scalable, low-maintenance communication security without heavy infrastructure investment. Continuous updates, ease of integration, and adaptability to evolving encryption standards position software solutions as the preferred choice for enterprises modernizing mobile communication security infrastructure.

Technology Insights

Encryption Protocols dominate with roughly 38% market share, covering AES and RSA implementations widely adopted in enterprise deployments. Secure messaging applications, VPNs, and secure voice/application development serve diverse enterprise, government, and military needs.

The fastest-growing technology segment is Post-Quantum Encryption and advanced cryptographic solutions, which are gaining traction as enterprises become increasingly aware of future quantum threats. Organizations are increasingly adopting secure messaging and encryption platforms with next-generation algorithms to protect sensitive information, ensuring readiness for evolving cybersecurity landscapes and compliance with emerging global encryption standards.

Deployment Type Insights

Cloud-based deployment leads with around 44% market share, reflecting demand for scalable, managed solutions requiring minimal IT infrastructure. On-premise and hybrid deployments serve government, military, and regulated enterprise needs without specifying shares.

The fastest-growing deployment segment is Cloud-native secure communication solutions, attracting organizations seeking rapid deployment across distributed locations. Cloud platforms enable secure endpoint management, encrypted collaboration, and unified communications while minimizing IT overhead, making them particularly appealing for mid-market enterprises and large organizations pursuing cost-effective, scalable, secure communication strategies.

Industry Insights

The Government sector leads with approximately 42% market share, encompassing federal agencies, defense, law enforcement, and intelligence organizations. Military, corporate, healthcare, and finance segments also implement secure communication solutions to protect sensitive information, intellectual property, and transactions.

The fastest-growing industry segment is Corporate and technology enterprises, driven by digital transformation initiatives and the adoption of remote work. Organizations are rapidly deploying secure mobile communication platforms to protect intellectual property, enable encrypted collaboration, and ensure regulatory compliance while supporting distributed teams and cloud-based workflows. This segment offers significant opportunities for solution providers targeting enterprise modernization and mobile security.

Regional Insights

North America Secure Mobile Communications Market Trends

North America dominates the global secure mobile communications market with approximately 48% share, driven by advanced technological infrastructure, substantial government defense budgets, and a concentration of leading solution providers. Aggressive U.S. cybersecurity mandates, including Executive Memo M-22-09 and CISA BOD 25-01, require encryption of data in transit and at rest. High smartphone penetration, reaching 97% among consumers aged 18–49, further fuels demand for secure mobile applications across enterprise and consumer segments.

The region’s innovation ecosystem, centered in Silicon Valley, Boston, and Seattle, attracts venture capital investment in secure-communication startups and established players such as BlackBerry, Cisco, Apple, and IBM. Enterprise BYOD adoption exceeds 80%, with 70% of devices unmanaged, driving the deployment of mobile device management and secure messaging platforms. Government certification requirements, such as FedRAMP, FIPS 140-2, and NSA Type 1, sustain demand for compliant solutions.

Europe Secure Mobile Communications Market Trends

Europe holds approximately 25% of the global market and is projected to grow at a CAGR of 19%, driven by stringent GDPR requirements and high security standards for enterprise communication platforms. Germany, the UK, and France are key contributors, with enterprises investing in GDPR-compliant secure messaging apps offering end-to-end encryption, audit logs, and on-premises deployment options. Regulatory harmonization across EU member states enables standardized adoption of encryption and deployment of pan-European solutions.

Leading vendors such as Thales Group support government and military organizations requiring NATO-standard solutions. Post-quantum cryptography migration initiatives by the UK’s NCSC are accelerating European planning for quantum-safe communication infrastructure, creating growth opportunities for vendors offering quantum-resistant encryption technologies, migration consulting, and secure communication services tailored to evolving compliance and cybersecurity requirements.

Asia Pacific Secure Mobile Communications Market Trends

Asia Pacific exhibits the fastest growth, with a projected 27% market share and robust adoption driven by accelerating digital transformation. China leads with over 1.1 billion mobile subscribers and government-led digital security initiatives. Regional military and defense spending is increasing as India, Japan, South Korea, and Australia invest in indigenous secure communication networks. India’s defense sector is growing at a 10% CAGR through 2035, driven by rising budgets and initiatives such as “Make in India.”

Enterprise adoption is supported by smartphone penetration exceeding 80% in Singapore, Japan, and South Korea, as well as sophisticated security infrastructure across the financial services, manufacturing, and government sectors. Adoption of post-quantum cryptography, 5G deployment, and national cybersecurity programs in countries like Saudi Arabia are driving demand for quantum-safe communication solutions, creating significant opportunities for vendors in both commercial and government segments.

Competitive Landscape

The Secure Mobile Communications market exhibits a moderately consolidated structure, with leading players controlling roughly 35–40% of revenues through strong government relationships, extensive product portfolios, and global distribution networks. Dominant providers focus on serving government and military segments with certified secure solutions, while differentiating through integrated hardware-software platforms and advanced encryption capabilities tailored for defense and critical infrastructure.

Market leaders invest heavily in research and development, prioritizing post-quantum cryptography and AI-driven threat detection technologies. Emerging competitors target enterprise segments with user-friendly interfaces, simplified compliance, and cost-effective solutions, challenging incumbents by offering specialized, agile products that address evolving secure communication demands across industries.

Key Market Developments

- In December 2025, IBM and stc group announced expanded collaboration to prepare Saudi Arabia's telecommunications sector for quantum-safe cybersecurity solutions, leveraging IBM's quantum-resistant encryption capabilities to fortify data protection protocols against emerging quantum computing threats.

- In June 2024, Thales Group announced breakthrough in quantum-resistant encryption technology development, positioning the company as leader in quantum-safe communication solutions addressing future cryptographic challenges posed by quantum computing advancement.

- In April 2024, IBM unveiled new artificial intelligence-powered security platform for enhanced threat detection within enterprise communication systems, integrating machine learning algorithms to identify and respond to emerging cybersecurity threats in real-time across distributed communication networks.

Companies Covered in Secure Mobile Communications Market

- BlackBerry Limited

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Cisco Systems, Inc.

- Thales Group

- IBM Corporation

- Silent Circle LLC

- Wickr LLC

- KoolSpan Inc.

- Bittium Corporation

- Motorola Solutions, Inc.

- L3Harris Technologies, Inc.

- BAE Systems plc

- Raytheon Technologies Corporation

- Check Point Software Technologies Ltd.

- Signal, Telegram

- Rohde & Schwarz

- Airbus Defense and Space

- Salt Communications

Frequently Asked Questions

The secure mobile communications market is projected to reach US$ 100.9 billion by 2033, growing from US$ 28.5 billion in 2026 at a 19.8% CAGR, driven by cybersecurity threats, regulatory mandates, and remote work adoption.

Demand is driven by rising mobile cyber threats, strict regulatory compliance requirements, widespread BYOD and remote work adoption, and government mandates requiring encryption of data in transit and at rest.

Software solutions dominate with approximately 45% market share, supported by cloud-based deployment, scalability, continuous updates, and cross-platform compatibility.

North America leads the market with about 48% share, driven by federal cybersecurity mandates, high defense spending, enterprise BYOD adoption, and advanced mobile security infrastructure.

The key opportunity lies in quantum-safe cryptography migration, as governments mandate post-quantum encryption adoption between 2028 and 2035, driving demand for new solutions and services.