- Hardware & Software IT Services

- Sales Force Automation Market

Sales Force Automation Market Size, Share, and Growth Forecast, 2026 - 2033

Sales Force Automation Market by Solution (Software, Services), Deployment (Cloud-based / SaaS, On-premises), Application (Lead Management, Sales Forecasting, Order & Invoice Management, Contact Management, Territory Management, Analytics & Reporting, Others), Industry, and Regional Analysis for 2026 - 2033

Sales Force Automation Market Size and Trends Analysis

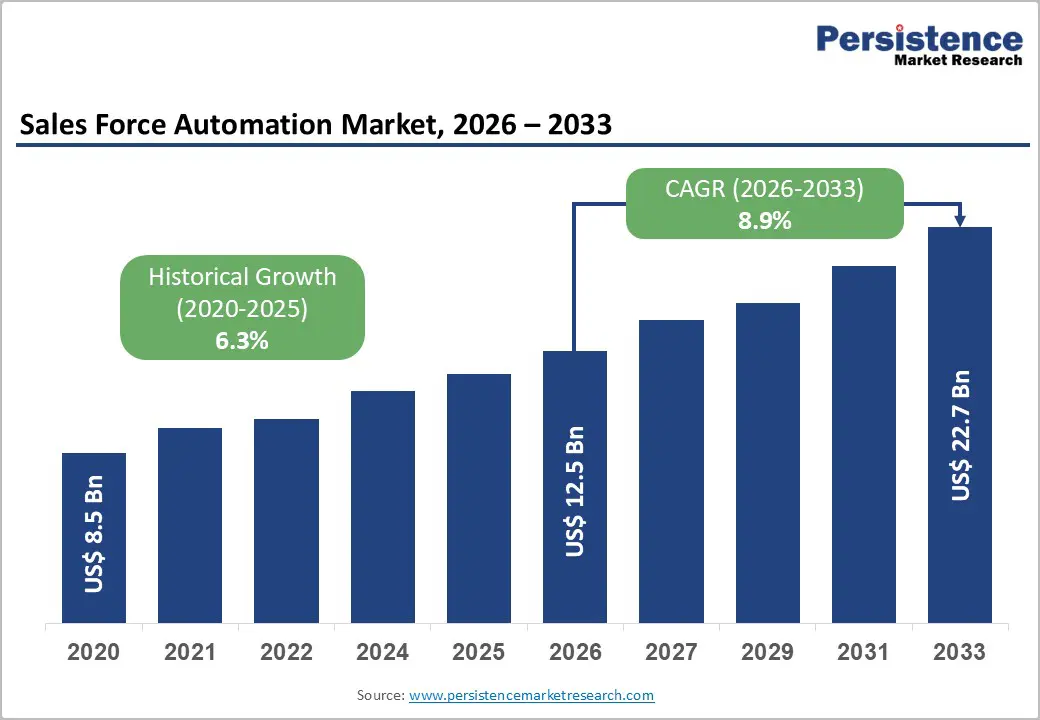

The global sales force automation market size is projected to rise from US$12.5 billion in 2026 to US$22.7 billion by 2033, growing at a CAGR of 8.9% during the forecast period from 2026 to 2033, reflecting the profound shift toward AI-powered sales processes, cloud-native architectures, and the critical business imperative of operational efficiency in an increasingly competitive, remote-first global marketplace.

The convergence of artificial intelligence adoption in sales functions, regulatory compliance requirements under frameworks such as GDPR, and the exponential growth of cloud computing adoption across enterprises collectively drive sustained market expansion.

Key Industry Highlights:

- Leading Solution: Software dominates the market with over 72% market share in 2026, valued at more than US$9.0 Bn, driven by the need for robust digital tools to automate sales processes, centralize customer data, and enable remote access. Services are the fastest-growing segment, with a 10.8% CAGR, driven by demand for implementation, customization, integration, and ongoing support to optimize SFA adoption.

- Leading Deployment: On-premises holds over 40% market share in 2026, valued at over US$ 5.0 Bn, preferred for control, security, and integration with legacy systems in highly regulated industries. Cloud-based deployment grows fastest at 14.2% CAGR, supported by scalability, remote collaboration, AI-driven insights, and lower infrastructure costs.

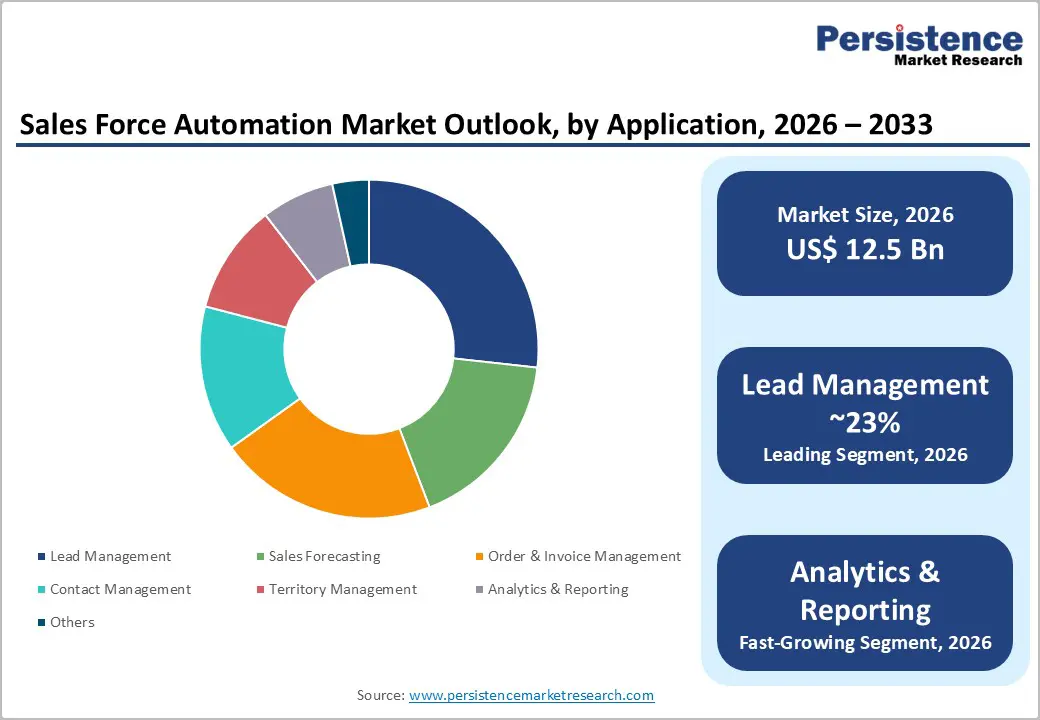

- Leading Application: Lead management commands more than 23% share in 2026, valued at over US$2.9Bn, driven by the need to efficiently capture, track, and convert leads across channels. Analytics & reporting is the fastest-growing application at 13.4% CAGR, as organizations adopt data-driven insights for forecasting, performance tracking, and compliance.

- Leading Industry: IT & Telecom holds the largest share at over 25% in 2026, valued at over US$ 3.1 Bn, due to complex sales operations, distributed teams, and digital transformation initiatives. Healthcare is the fastest-growing industry at 13.1% CAGR, driven by regulatory compliance, digital therapeutics, and the need for consultative, data-driven engagement with healthcare professionals.

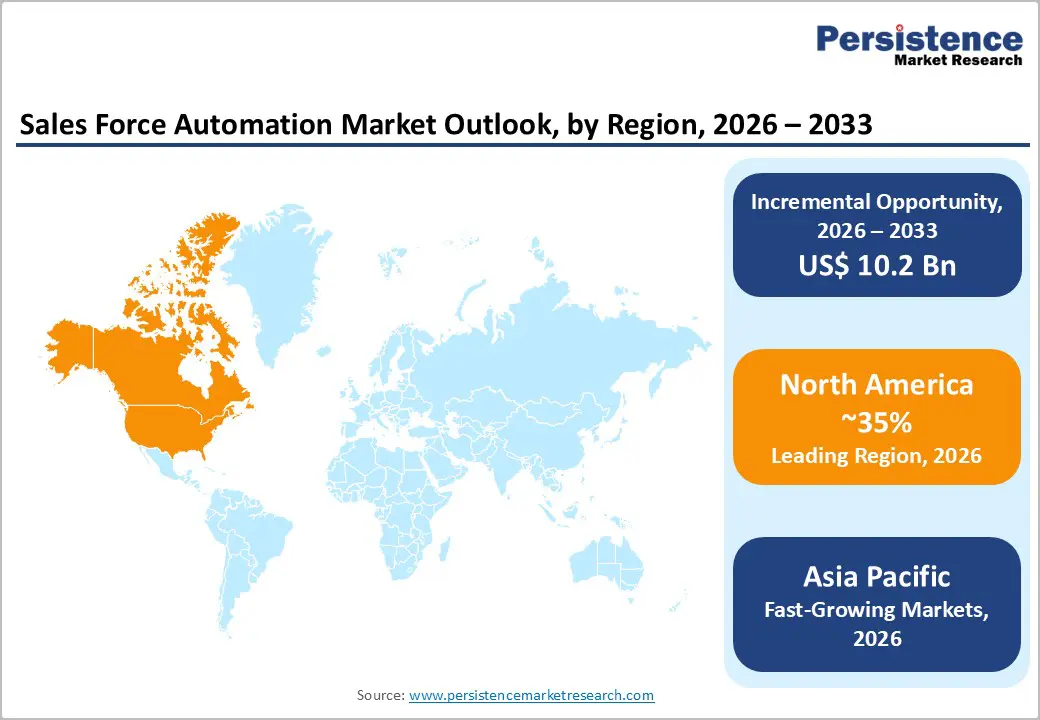

- Leading Region: North America leads with over 35% share in 2026, valued at US$ 4.4 Bn, supported by mature digital infrastructure, high cloud adoption, and enterprise investment in AI-enabled SFA. Asia Pacific grows fastest at 15.2% CAGR, driven by emerging market digitalization, manufacturing expansion, cloud adoption, and government initiatives. Europe holds over 21% share, driven by regulatory compliance, digital transformation, and enterprise adoption in finance, manufacturing, and professional services.

| Key Insights | Details |

|---|---|

| Sales Force Automation Market Size (2026E) | US$12.5 Bn |

| Market Value Forecast (2033F) | US$22.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Dynamics

Driver - AI and Machine Learning-Enabled Sales Transformation

The integration of AI and machine learning is fundamentally reshaping sales operations, making advanced Sales Force Automation a competitive necessity rather than a discretionary upgrade. Over 60% of sales organizations have already deployed AI-powered tools, with another 20% planning to adopt them in the near term, driven by measurable outcomes such as a 13-15% revenue uplift and a 10-20% improvement in sales ROI. AI-enhanced SFA platforms automate repetitive administrative tasks, significantly boosting sales productivity and enabling greater focus on relationship management and deal closures. Market leaders such as Salesforce demonstrate this shift, with over 80% of sales teams actively experimenting with or fully implementing AI-driven sales capabilities.

Remote Work Enablement and Omnichannel Sales Operations

The permanence of hybrid and remote work models has created sustained demand for SFA platforms supporting distributed sales teams. Modern SFA solutions deliver mobile-first interfaces, real-time pipeline visibility across multiple geographies, asynchronous collaboration capabilities, and unified customer communication logs accessible from any device. This deployment model enables organizations to hire talent regardless of geographic proximity and maintain operational continuity during external disruptions. The shift toward account-based selling and complex, multi-stakeholder deals requires sophisticated visibility and collaboration features that cloud-based platforms provide natively.

Restraint - Implementation Complexity and Organizational Change Management

Sales force automation projects represent substantial organizational change initiatives extending beyond technology deployment. Implementation timelines typically span 6-12 months for enterprise-scale deployments and require simultaneous process redesign, sales methodology adoption, and workforce capability development. Hidden costs emerge throughout initiatives, custom integrations with existing enterprise systems, data migration from legacy systems, training across dispersed sales organizations, and the opportunity cost of sales team productivity during transitions. Organizations frequently experience a 15-25% productivity decline during transition periods, creating barriers particularly for SMEs lacking sophisticated IT departments.

Data Security, Privacy Regulation, and Compliance Burden

Global data privacy regulations, particularly GDPR in Europe, impose substantial compliance obligations on implementations. Organizations must maintain data processing impact assessments, implement privacy-by-design principles, and enable rapid response to data subject access requests. GDPR non-compliance carries penalties of up to €20 million or 4% of annual revenue, creating significant financial risk. While major vendors have invested in compliance automation, these capabilities typically require additional investment, extending the total cost of ownership. Organizations operating across multiple jurisdictions face exponentially increased complexity.

Opportunities- Healthcare Vertical Expansion and Regulatory-Driven Digitalization

The increasing adoption of digital health records, e-prescriptions, and telehealth platforms is driving pharmaceutical, medical device, and healthcare IT companies to digitize sales workflows and physician engagement. Stringent regulations around data transparency, compliance tracking, and auditability are driving demand for SFA tools with built-in reporting, consent management, and compliance features. The expansion of specialty drugs, personalized medicine, and complex care pathways requires more consultative, data-driven sales approaches that SFA platforms enable. Healthcare providers’ shift toward value-based care models increases the need for analytics-led sales planning and account management.

AI-Driven Sales Analytics and Revenue Intelligence Convergence

AI-powered sales analytics and revenue intelligence are transforming by turning large volumes of customer and pipeline data into predictive, actionable insights. Integration of AI enables real-time forecasting, deal scoring, churn prediction, and next-best-action recommendations, improving win rates and sales productivity. Convergence with digital monetization enables SFA platforms to directly link sales performance to subscription pricing, usage-based billing, and customer lifetime value metrics. This integration supports data-driven pricing optimization, cross-sell/upsell identification, and revenue leakage prevention. Enterprises increasingly view SFA not just as a productivity tool but as a revenue-optimization engine, driving higher adoption and spend across mid-market and large organizations.

Category-wise Analysis

Solution Insights

Software dominates the global market, capturing more than 72% of the market share in 2026, with a value exceeding US$9.0 Bn, as organizations increasingly require robust digital tools to automate and streamline sales processes. Software solutions centralize customer and sales data, provide real-time visibility into pipelines, and reduce manual tasks, thereby boosting productivity and accuracy across sales teams. Cloud-based and SaaS models make these tools easy to deploy, scalable, and accessible remotely, meeting the growing demand for flexible, data-driven operations.

Services demonstrate the highest growth rate, at a 10.8% CAGR, due to organizations increasingly requiring end-to-end support for the implementation, customization, and integration of SFA tools with existing CRM and ERP systems. Businesses need training, consulting, and managed services to ensure user adoption and optimize workflows. Ongoing technical support and upgrades are essential to handle complex sales processes, regulatory compliance, and evolving customer engagement strategies. This rising demand for expert-driven, tailored solutions is driving rapid growth in the services segment.

Deployment Insights

On-premises holds over 40% market share in 2026, with a value exceeding US$5.0 Bn, due to many organizations still prioritizing control, security, and customization to meet their specific operational and regulatory needs. It gives enterprises complete control over sensitive customer and sales data, which is critical in highly regulated industries such as finance and healthcare that must comply with strict data protection requirements. They also allow deeper integration with legacy systems and tailored workflows, which large enterprises often require to align SFA with complex internal processes.

Cloud-based solutions are expected to grow at the highest rate, with a CAGR of 14.2%, driven by the need for real-time access to sales data from anywhere, enabling remote teams to collaborate efficiently. Companies seek scalable solutions that require minimal upfront IT investment, thereby reducing maintenance and infrastructure costs. The growing demand for automatic updates, seamless integration with CRM and marketing tools, and enhanced data security further accelerates cloud adoption. Cloud platforms support AI-driven insights and analytics, meeting the need for smarter, faster sales decision-making.

Application Insights

Lead management is expected to account for more than 23% in 2026, with a value exceeding US$2.9B, as businesses prioritize the efficient capture, tracking, nurturing, and conversion of leads across multiple channels, which directly impacts sales growth and revenue. Lead management tools help sales and marketing teams collaborate, prevent loss of potential customers, and improve conversion rates through automation and data-driven follow-ups. This focus on structured lead handling and prioritization of high-value prospects enhances sales efficiency and return on investment.

Analytics & reporting are expected to grow at a CAGR of 13.4%, due to the need for data-driven insights to optimize sales strategies and improve forecasting accuracy. Businesses require real-time performance tracking, visibility into customer behavior, and identification of high-potential leads. Regulatory compliance and accountability pressures are also driving adoption, as companies must monitor sales activities and outcomes efficiently. The growing complexity of multi-channel sales processes makes advanced analytics essential for decision-making and resource allocation.

Industry Insights

IT & Telecom has the largest market share at over 25% in 2026, with a value exceeding US$3.1 Bn, as these sectors have highly complex, large-scale sales operations that require real-time tracking, centralized customer data, and automated workflows to remain competitive. They rely on SFA to manage distributed sales teams, automate lead and opportunity tracking, and integrate sales, billing, and support systems to ensure seamless service delivery. Rapid digital transformation and the push for cloud-based, mobile sales tools in IT & Telecom drive higher adoption to improve efficiency and customer engagement.

Healthcare is expected to grow at a CAGR of 13.1% due to the need for providers and pharmaceutical companies to manage an increasingly complex network of doctors, hospitals, and patients efficiently. The sector demands real-time tracking of sales interactions, compliance with strict regulatory standards, and personalized engagement with healthcare professionals. The rise of digital therapeutics, telemedicine, and data-driven patient care necessitates SFA tools to streamline operations, enhance CRM, and improve decision-making.

Regional Insights

North America Sales Force Automation Market Trends

North America holds over 35% share in 2026, reaching US$ 4.4 Bn value driven by advanced digital infrastructure, high cloud adoption over 90% of enterprises, and mature enterprise software procurement. The U.S., as the largest regional market, benefits from regulatory support, venture capital investment in emerging technologies, and the concentration of Fortune 500 companies that deploy SFA as a strategic necessity. Industries such as financial services, healthcare, retail, and technology lead in the adoption of sophisticated platforms. Fragmented state, e.g., CCPA and federal regulations, have prompted vendors to integrate compliance and data governance, creating barriers to entry that favor established players.

Asia Pacific Sales Force Automation Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 15.2%, driven by emerging market digitalization, manufacturing expansion, and cloud infrastructure adoption. India leads regional growth, fueled by SME cloud adoption, government digital initiatives, and sectoral expansions in software, logistics, and financial services. Japan’s consensus-driven organizational culture drives demand for SFA tools focused on customer relationship management and team collaboration, in contrast to North America’s efficiency-driven approach. China offers significant opportunities due to manufacturing growth, e-commerce expansion, and supportive industrial policies, collectively making the region highly heterogeneous with diverse SFA adoption patterns.

Europe Sales Force Automation Market Trends

Europe is expected to hold more than a 21% share by 2026, driven by advanced digital transformation, strict regulatory frameworks, and a concentration of enterprise customers in finance, manufacturing, and professional services. Growth is slower than in North America due to conservative technology adoption and higher implementation costs from compliance requirements like GDPR, which has made SFA essential for managing customer data and audit trails. Germany leads the region, supported by strong manufacturing and IT sectors, followed by France and the U.K. Vendors are innovating with privacy-enhanced solutions, sustainability reporting, and explainable AI, aligning with European priorities in data protection, responsible AI, and sustainability.

Competitive Landscape

The sales force automation (SFA) market is largely fragmented, with numerous players ranging from global software giants to niche solution providers. Companies adopt a multi-pronged competition strategy focusing on continuous product innovation, integrating AI and analytics for smarter sales insights, and expanding cloud-based and mobile offerings. Many emphasize strategic partnerships and acquisitions to broaden their client base and geographic reach. Competitive pricing, robust after-sales services, and industry-specific customization help them differentiate in a crowded market.

Key Industry Developments

- In December 2025, Salesforce’s SFA solutions, including Agentforce Life Sciences and Agentforce 360, were selected by Novartis to unify and automate customer engagement across sales, marketing, patient services, and medical teams. The global rollout over five years aims to simplify workflows, enhance compliance, and enable more strategic, data-driven interactions with patients and healthcare professionals.

- In June 2025, Salesforce unveiled its Summer ‘25 release, introducing enhanced Agentforce capabilities that integrate AI agents to streamline workflows, improve CRM data accuracy, and provide personalized sales coaching. The update includes multimodal support, web search access, and expanded sales automation features across multiple languages and channels. These advancements aim to boost efficiency and enrich customer and employee experiences.

Companies Covered in Sales Force Automation Market

- Salesforce, Inc.

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- HubSpot, Inc.

- Zoho Corporation Pvt. Ltd.

- SugarCRM Inc.

- Infor, Inc.

- Aptean, Inc.

- Pegasystems, Inc.

- Freshworks Inc.

- Insightly, Inc.

- Others

Frequently Asked Questions

The global sales force automation market is projected to be valued at US$12.5 Bn in 2026.

Enterprises need to improve sales productivity, shorten sales cycles, and gain real-time visibility into pipelines and customer interactions are a key driver of the market.

The market is expected to witness a CAGR of 8.9% from 2026 to 2033.

AI-driven predictive sales analytics, mobile-first SFA adoption among SMEs, and deeper integration with CRM, marketing automation, and customer engagement platforms across emerging digital economies are creating strong growth opportunities.

Salesforce, Inc., Microsoft Corporation, Oracle Corporation, SAP SE, HubSpot, Inc., Zoho Corporation Pvt. Ltd. are among the leading key players.