- Hardware & Software IT Services

- AI Sales Assistant Software Market

AI Sales Assistant Software Market Size, Share, and Growth Forecast 2026 - 2033

AI Sales Assistant Software Market by Deployment (Cloud, On-premise), Functionality (Lead Management, Sales Forecasting & Analytics, Customer Recommendation & Relationship Management, Automated Follow-Ups, Chatbots and Virtual Assistants, Proposal & quotation automation, Others), End-user (Retail and E-Commerce, BFSI, Healthcare, IT and Telecom, Manufacturing, Real Estate, Media & Entertainment, Professional Services & Consulting), and Regional Analysis, 2026 - 2033

AI Sales Assistant Software Market Size and Trend Analysis

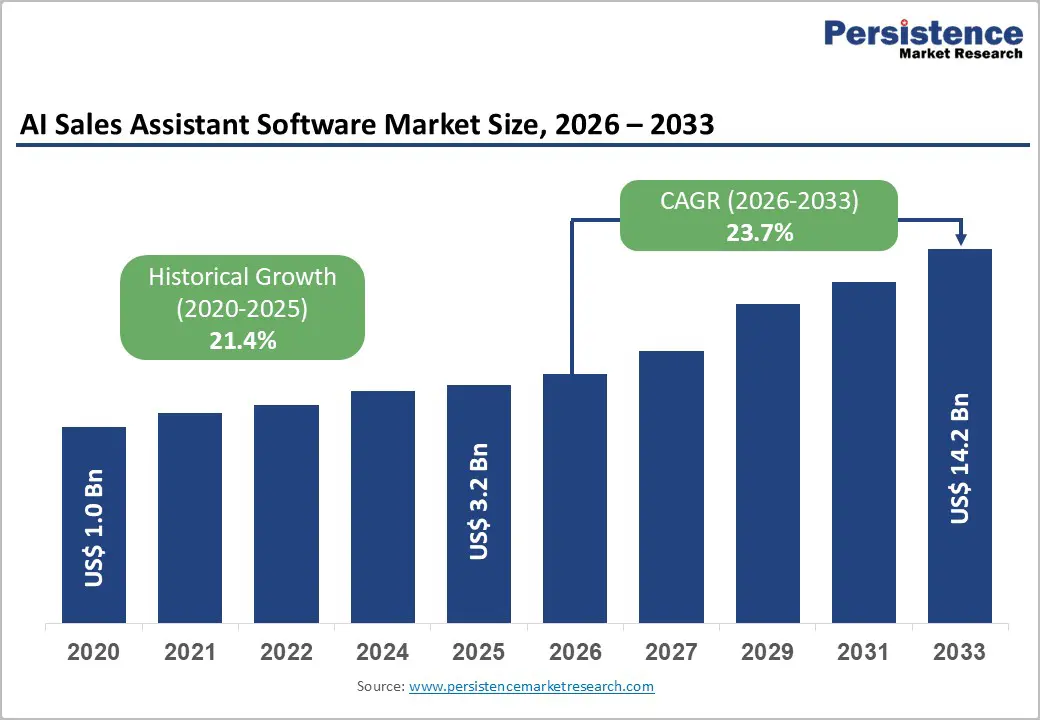

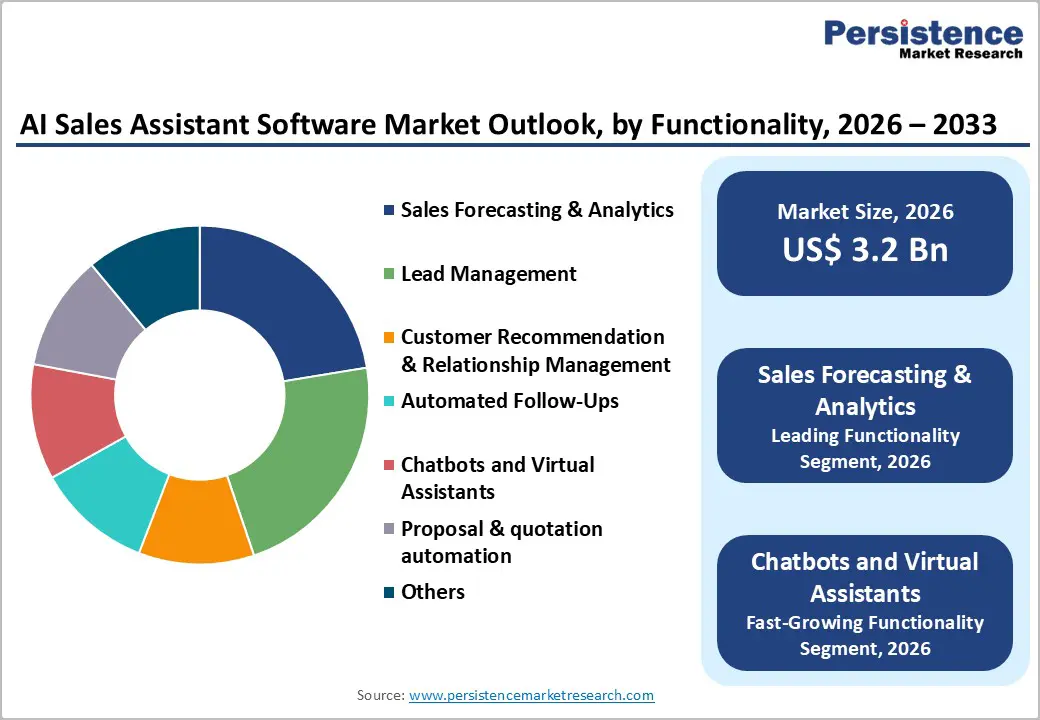

The global AI sales assistant software market size is likely to be valued at US$ 3.2 billion in 2026 and projected to reach US$ 14.2 billion by 2033, growing at a CAGR of 23.7% between 2026 and 2033.

Accelerating digital transformation across enterprises, combined with the growing demand for automation and personalization in sales workflows, is driving robust market expansion. Rising adoption of cloud-based SaaS solutions among small and medium-sized businesses, coupled with generative AI breakthroughs that enable sophisticated natural language processing and conversational commerce capabilities, has accelerated market penetration.

Key Industry Highlights:

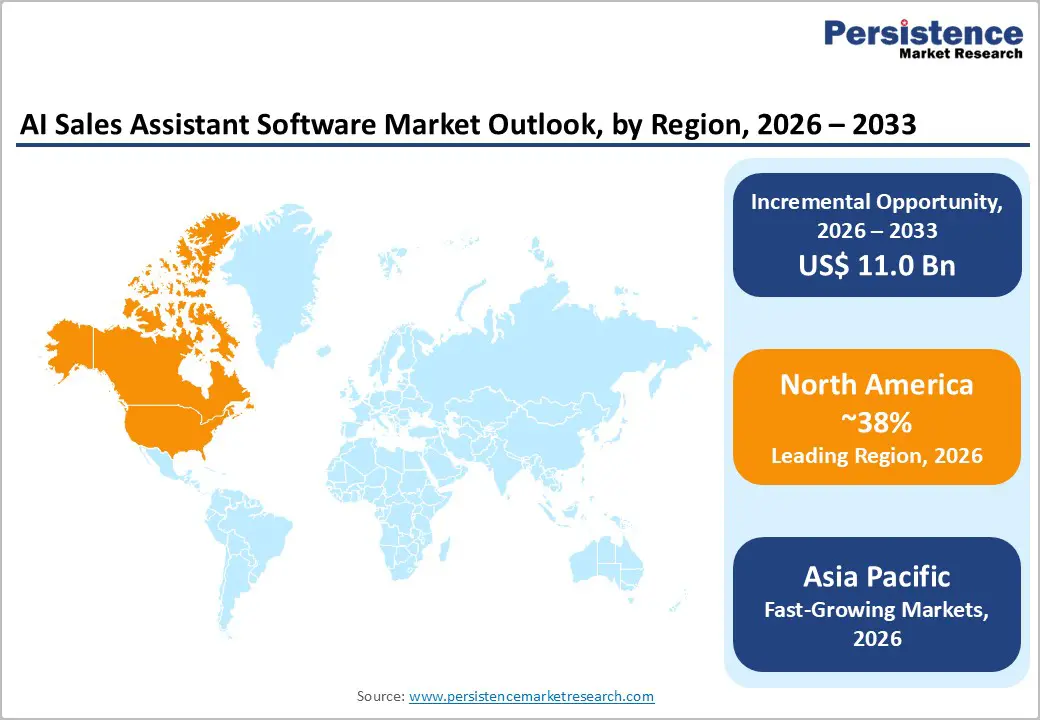

- Leading Region: North America commands the largest regional market share of approximately 38% in 2025, driven by concentrated venture capital investment, substantial enterprise technology spending, and leadership from global AI software companies including Salesforce, HubSpot, and Microsoft providing foundation AI models and comprehensive SaaS platforms.

- Fastest Growing Region: Asia-Pacific represents the fastest-growing regional market, expanding at approximately 28% CAGR between 2026 and 2033, propelled by explosive e-commerce growth in China and India, expanding cloud adoption among small and medium-sized businesses, and accelerating digital transformation across retail and telecommunications sectors.

- Dominant Segment: Cloud-based deployment dominates and nearly accounts for 62% share in 2025, reflecting enterprise preference for scalable, flexible SaaS solutions, eliminating substantial capital infrastructure investments and enabling rapid, cost-effective implementation.

- Fastest-Growing Segment: Chatbots and virtual assistants represent the fastest-growing functionality segment, expanding at approximately 26% CAGR between 2026 and 2033, driven by breakthrough natural language processing advancements, generative AI capabilities, and enterprise recognition of conversational AI effectiveness in lead qualification and customer engagement.

- Key Opportunity: Retail and E-Commerce emerges as a key opportunity segment driven by consumer demand for hyper-personalized experiences, omnichannel commerce transformation, and retailers’ emphasis on automation-driven revenue optimization and customer lifetime value enhancement.

| Key Insights | Details |

|---|---|

| AI Sales Assistant Software Market Size (2026E) | US$ 3.2 billion |

| Market Value Forecast (2033F) | US$ 14.2 billion |

| Projected Growth CAGR (2026 - 2033) | 23.7% |

| Historical Market Growth (2020 - 2025) | 21.4% |

Market Dynamics Analysis

Drivers - Rise in Demand for Sales Automation and Efficiency Optimization

Organizations globally are prioritizing sales automation to eliminate time-consuming manual tasks that consume approximately 75% of sales representatives’ working hours, a critical productivity drain. AI Sales Assistant Software automates repetitive activities, including data entry, lead scoring, follow-up scheduling, proposal generation, and CRM data management, thereby reclaiming significant productive selling time. Companies deploying AI-driven lead scoring and automated follow-up systems experience average improvements of 25% in sales productivity and 25-35% increases in sales-qualified leads.

Early AI deployments in sales have boosted win rates by over 30%, illustrating AI’s capacity to dramatically enhance sales outcomes. Conversational AI platforms and chatbots now handle over 60% of routine customer inquiries autonomously, allowing sales representatives to focus on complex deal negotiations and relationship-building. This transformation in sales workflows, supported by investments in AI automation across diverse industries, is fundamentally reshaping how revenue teams operate and accelerating market expansion.

Rising Focus on Personalization and Customer Experience Enhancement at Scale

Modern buyers expect hyper-personalized interactions tailored to their specific needs, preferences, and purchase history, driving organizations to implement AI Sales Assistant Software for delivering customization at enterprise scale. AI-powered recommendation engines and customer relationship management systems analyze vast datasets encompassing customer behavior, purchase history, browsing patterns, and communication context to generate dynamic, personalized product suggestions and tailored messaging strategies. 91% of consumers are significantly more likely to engage with brands providing personalized recommendations, directly translating to improved conversion rates and customer lifetime value.

E-commerce platforms leveraging AI-powered product recommendation chatbots are experiencing revenue increases of up to 40% and conversion rate improvements of 15-20% compared to non-personalized approaches. AI chatbots integrated with Retail and E-Commerce platforms detect customer intents from conversational patterns and automatically recommend products aligned with identified preferences, resulting in measurable improvements in average order values and customer satisfaction. The capability to deliver consistent, personalized customer experiences across multiple touchpoints, including email, chat, voice, and social channels, has become a competitive imperative, driving widespread adoption of AI Sales Assistant Software across enterprise and mid-market organizations.

Restraints - Data Privacy, Security, and Regulatory Compliance Challenges

The increasing complexity of data protection regulations, including GDPR, the CCPA, and industry-specific compliance frameworks such as HIPAA in healthcare and financial regulations in the BFSI security sector, creates significant implementation barriers for AI Sales Assistant Software. Organizations must ensure that AI systems operate transparently, maintain explainability in decision-making processes, and comply with evolving data governance requirements across multiple jurisdictions.

The U.S. Treasury Department reported that AI systems in 2024 processed fraud-prevention and detection activities that required absolute regulatory compliance, underscoring the stringent requirements organizations must meet. Training data governance, algorithm transparency requirements, and audit trail maintenance for AI systems necessitate substantial investment in compliance infrastructure and third-party certifications. Non-compliance risks, including substantial financial penalties, reputational damage, and operational disruptions, deter risk-averse enterprises, particularly in regulated sectors. This regulatory complexity extends implementation timelines and increases the total cost of ownership for AI sales assistant software deployments.

Scarcity of Specialized Talent and High Implementation Costs

The acute shortage of data scientists, machine learning engineers, and AI specialists with expertise in sales applications limits the pace of AI sales assistant software deployments, particularly in mid-market and smaller organizations. Organizations require technical personnel capable of training custom AI models, integrating systems with existing CRM platforms, managing data pipelines, and maintaining ongoing model performance and accuracy.

Implementation costs, encompassing infrastructure, training, customization, and change management, create financial barriers, particularly for smaller enterprises operating with constrained technology budgets. Vendor lock-in risks and concerns regarding the long-term total cost of ownership deter some organizations from pursuing AI-driven sales transformation initiatives. The complexity of integrating AI systems with legacy CRM platforms and existing sales technology stacks adds further implementation challenges and costs.

Opportunity - Expansion of Conversational Commerce and Voice-Enabled Sales Assistants

Conversational AI is one of the fastest-growing segments in the AI sales assistant software market, offering exceptional opportunities for vendors serving the retail, e-commerce, and B2B sectors. Natural language processing advancements enable AI sales assistants to conduct nuanced, context-aware conversations with customers across chat, SMS, voice, and social messaging platforms, achieving the sophistication previously required of human agents. Voice commerce and conversational shopping experiences are experiencing accelerated adoption, with consumers increasingly using voice assistants for product discovery and purchase decisions.

Major technology companies, including Google, Amazon, and Apple, are investing substantially in voice commerce capabilities, creating ecosystem opportunities for AI sales assistant software vendors to integrate with emerging voice-enabled retail platforms. The market for AI-powered chatbots and virtual sales assistants is projected to expand at a CAGR exceeding 27% through 2033, driven by consumer demand for frictionless, conversational commerce experiences and retailers’ emphasis on automation-driven cost reduction and revenue enhancement.

Industrial Vertical Expansion and Sector-Specific AI Solutions Development

Significant opportunities exist to develop industry-specific AI Sales Assistant Software solutions tailored to the unique requirements of the BFSI, healthcare, manufacturing, telecommunications, and professional services sectors. The BFSI sector presents particularly compelling opportunities, with financial institutions increasingly deploying AI-powered sales agents for customer onboarding, personalized financial advisory services, loan origination, policy recommendations, and cross-sell automation.

Retail and E-Commerce organizations are accelerating AI deployment to drive omnichannel growth, dynamic pricing optimization, and personalized customer engagement across physical stores and digital channels. In 2024, Walmart announced plans to scale AI and generative AI applications for creating hyper-personalized and immersive commerce experiences, exemplifying an enterprise-level commitment to AI-driven sales transformation.

Healthcare providers and life sciences organizations are exploring AI-powered sales enablement for pharmaceutical sales representatives and medical device companies, creating new addressable markets. Vertical-specific regulatory expertise, domain knowledge, and tailored feature sets create opportunities for differentiation for vendors developing specialized solutions. This fragmentation creates market opportunities for both established enterprises and innovative startups to capture customer segments with unique requirements and compliance frameworks.

Category-wise Analysis

Deployment Insights

Cloud-based deployment dominates the AI Sales assistant software market, commanding approximately 62% share in 2025, reflecting widespread enterprise adoption of Software-as-a-Service (SaaS) models and preference for scalable, cost-effective solutions without substantial infrastructure investment. Cloud deployment offers significant advantages, including rapid implementation timelines, automatic software updates, seamless scalability to accommodate growing user bases, and reduced capital expenditure requirements compared to on-premise deployments.

Major platform vendors, including Salesforce, HubSpot, and Microsoft Dynamics, have embedded native AI capabilities into cloud CRM offerings, accelerating cloud adoption. Small and medium-sized businesses particularly favor cloud-based solutions, as subscription-based pricing models eliminate prohibitive upfront capital requirements and provide flexibility to scale investments aligned with business growth trajectories.

Functionality Insights

Lead management and sales forecasting & analytics are the leading functionality segments, collectively commanding approximately 48% market share in 2025, reflecting the prioritization of demand generation and pipeline visibility by revenue-focused organizations. AI-powered lead management systems leverage machine learning algorithms to analyze vast customer datasets, identify high-potential prospects, automatically score leads by conversion probability, and route qualified leads to the most appropriate sales representatives.

Chatbots and Virtual Assistants represent the fastest-growing functionality segment, expanding at a CAGR of approximately 26% between 2026 and 2033, driven by breakthrough advances in natural language processing, generative AI capabilities, and enterprise recognition of chatbot effectiveness in lead qualification and customer engagement. AI-powered virtual sales assistants can autonomously conduct initial discovery conversations, disqualify unsuitable prospects, schedule qualified leads with appropriate sales representatives, and provide 24/7 customer support.

End-user Insights

Retail and E-commerce represent the dominant end-user segment, capturing approximately 44% market share in 2025, reflecting the sector’s aggressive prioritization of omnichannel customer engagement, personalization, and automation-driven revenue optimization. Retail organizations are deploying AI-powered chatbots, product recommendation engines, and personalized customer relationship management systems to drive improvements in conversion rates, increase average order values, and enhance customer lifetime value across online and physical retail channels. Major retailers, including Nike and H&M, are leveraging AI recommendation engines to deliver personalized product suggestions, with Nike reporting a 35% increase in mobile conversion rates and H&M achieving a 20% reduction in product return rates through improved personalization.

Regional Insights

North America AI Sales Assistant Software Market Trends and Insights

North America maintains dominance in the global AI sales assistant software market, accounting for nearly 38% of the market in 2025, driven by substantial enterprise technology investments, advanced digital infrastructure, and a concentrated presence of leading AI software vendors. The United States is the largest individual country market, accounting for approximately 82% of the North American market value, fueled by venture capital investment exceeding $37 billion in generative AI in 2025 alone, according to Menlo Ventures analysis. Major technology companies, including Salesforce, HubSpot, Microsoft, and Google, maintain substantial research and development operations in the region, continuously advancing AI Sales Assistant Software capabilities and creating ecosystem advantages for local enterprises.

The region’s advantage extends to well-established original equipment manufacturer (OEM) partnerships, extensive integration ecosystems, and professional services infrastructure supporting complex AI implementations. Cloud infrastructure providers Amazon Web Services (AWS), Microsoft Azure, and Google Cloud offer enterprise-grade AI platforms enabling rapid development and deployment of AI Sales Assistant Software solutions. DocuSign, a major enterprise software vendor, announced in November 2025 its adoption of the Gong Revenue AI Operating System, underscoring its enterprise-level commitment to AI-driven sales transformation in North America.

Europe AI Sales Assistant Software Market Trends and Insights

Europe is emerging as the fastest-growing regional market for AI Sales Assistant Software, projected to expand at approximately 21.4% CAGR between 2026 and 2033, driven by accelerating digital transformation initiatives across regulated sectors, including BFSI, healthcare, and manufacturing. Germany,the United Kingdom, and France lead European adoption, with strong emphasis on data privacy compliance, regulatory harmonization, and responsible AI governance aligned with GDPR and emerging EU AI Act requirements. European enterprises prioritize AI solutions that offer transparency, explainability, and audit trails to satisfy stringent data governance requirements.

European vendors demonstrate competitive strength through partnerships with major global CRM platforms and the development of localized solutions addressing language diversity, regional compliance requirements, and sector-specific regulatory frameworks. The region’s emphasis on data sovereignty and local data residency requirements creates opportunities for vendors offering EU-compliant deployment options and regional data center infrastructure. Vertical-specific solutions tailored to European manufacturing sectors, automotive industry innovation ecosystems, and financial services regulatory requirements are driving market expansion.

Asia Pacific AI Sales Assistant Software Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected to grow at a CAGR of approximately 28% between 2026 and 2033, driven by rapid digital transformation, explosive growth in the e-commerce and retail sectors, and expanding adoption of cloud-based SaaS solutions among small and medium-sized businesses. China, accounting for approximately 30% of global vehicle production and significant e-commerce transaction volumes, is experiencing accelerated adoption of AI Sales Assistant Software across the telecommunications, financial services, retail, and technology sectors. Alibaba announced in July 2024 the adoption of its generative AI toolkit by approximately 500,000 merchants across Asia-Pacific and international markets, demonstrating regional scale and market opportunity magnitude.

India’s rapidly expanding software services industry, combined with aggressive digital adoption targets across retail and professional services sectors, is generating substantial demand for AI-powered sales solutions. Japan and South Korea maintain mature, established markets with high technology adoption rates and a strong emphasis on chatbot and conversational AI solutions. ASEAN nations, including Vietnam, Thailand, and Indonesia, are experiencing accelerating adoption driven by rising e-commerce penetration, expanding telecommunications sectors, and growing technology infrastructure investments.

Competitive Landscape

The AI sales assistant software market exhibits a moderately fragmented competitive structure characterized by dominant multinational software vendors alongside specialized technology companies and innovative startups. Major global platforms including Salesforce, HubSpot, and Microsoft Dynamics command significant market shares through extensive research and development investments, established enterprise customer relationships, and continuous integration of generative AI capabilities into core CRM platforms.

Specialized AI sales assistant software companies including Gong, Clari, Conversica, and Drift focus on conversation intelligence, pipeline management, and conversational commerce, achieving competitive differentiation through superior AI performance in specific use cases. Market consolidation trends reflect industry dynamics, as evidenced by Clari’s acquisition of Gong in October 2024, combining Gong’s conversation intelligence and real-time revenue intelligence with Clari’s predictive analytics and pipeline management capabilities. Emerging business models emphasize modular integration with existing CRM platforms, multi-channel deployment options, and transparent pricing structures transparent to mid-market customers.

Competitive differentiation strategies focus on developing vertical-specific solutions, integrating natural language processing and conversational AI advances into sales workflows, and demonstrating measurable revenue impact through customer case studies and performance metrics. Companies are increasingly offering transparent explainability features addressing enterprise concerns regarding AI decision-making processes and regulatory compliance.

Key Market Developments:

- December 2024: Gartner published research predicting that by 2027, approximately 95% of seller research workflows will initiate with AI, representing fundamental transformation in sales professional workflows and accelerating adoption of AI-powered research and intelligence tools across enterprise sales teams.

- November 2025: Docusign selected Gong Revenue AI Operating System to accelerate sales productivity and drive strategic growth initiatives, demonstrating enterprise-scale adoption of advanced AI conversation intelligence and revenue analytics platforms for optimizing go-to-market effectiveness.

- September 2024: Alibaba announced adoption of its generative AI toolkit by approximately 500,000 merchants across Asia-Pacific and international markets, reflecting significant market opportunity in retail and e-commerce segments and accelerating regional adoption of AI-powered sales and conversion optimization tools.

Companies Covered in AI Sales Assistant Software Market

- Salesforce

- HubSpot

- Zoho CRM

- Pipedrive AI Sales Assistant

- Clari

- Gong.io

- Conversica

- InsideSales.com

- Nutshell

- SugarCRM

- Scratchpad

- Yesware

- Qualified

- Apollo.io

- PandaDoc

- Drift

- X.ai

- SalesDirector.ai

- Troops

- Cien

- Saleswhale

- Zia

- Amplemarket

- Tact.ai

- Nudge.ai

Frequently Asked Questions

The global market is expected to reach US$ 3.2 billion in 2026 and expand to US$ 14.2 billion by 2033.

Demand is driven by enterprise digital transformation, the need for sales automation, measurable improvements in productivity and win rates, and rising expectations for personalized engagement.

North America is projected to maintain the largest share at approximately 38% in 2025 due to strong enterprise technology spending and advanced AI ecosystems.

Key opportunities include adoption of conversational and voice-enabled assistants, vertical-specific AI solutions, and expanding deployment in retail and e-commerce expected to grow at over 27% CAGR through 2032.

Key players include Salesforce, HubSpot, Zoho CRM, Gong.io, Clari, Conversica, Drift, Qualified, Apollo.io, and PandaDoc, supported by partnerships, R&D, and global platform capabilities.