- Aerospace & Defense

- Thrust Reverser Actuation System Market

Thrust Reverser Actuation System Market Size, Share, and Growth Forecast, 2026-2033

Thrust Reverser Actuation System Market by Technology (Hydraulic, Electric, Pneumatic, Electro-Hydraulic, Mechanical), Application (Commercial Aircraft, Business Jets, Military Aircraft), and Regional Forecast for 2026-2033

Thrust Reverser Actuation System Market Share and Trends Analysis

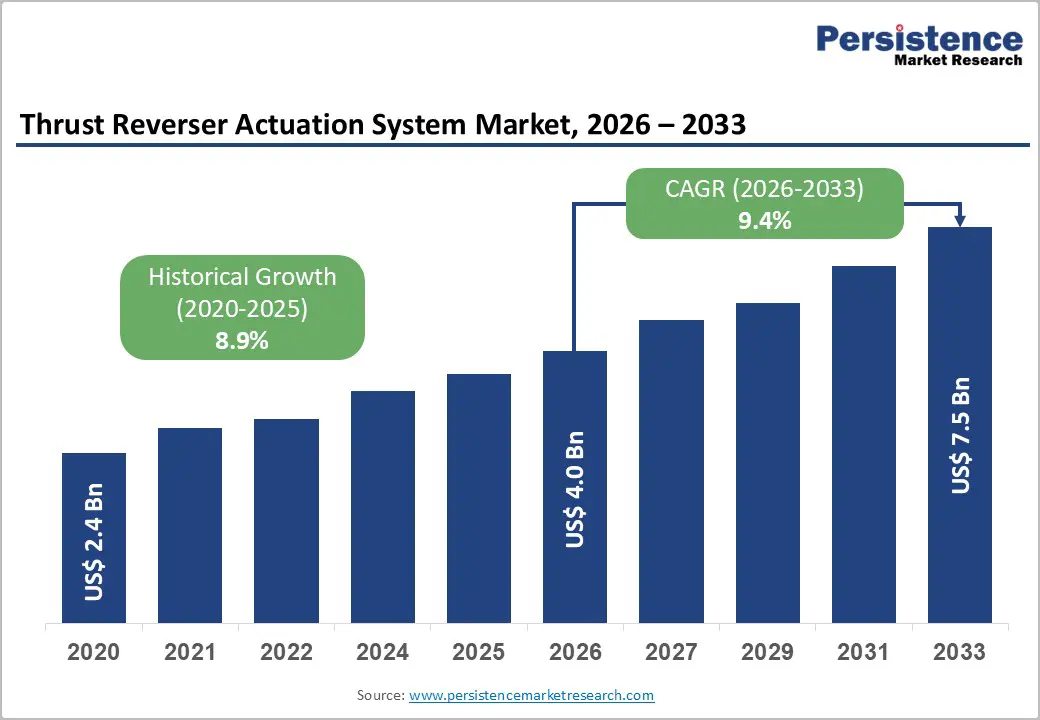

The global thrust reverser actuation system market size is likely to be valued at US$4.0 billion in 2026, and is projected to reach US$7.5 billion by 2033, growing at a CAGR of 9.4% during the forecast period 2026-2033.

Market expansion is being supported by rising aircraft deliveries, accelerated fleet modernization programs, and sustained replacement demand across aging aircraft platforms. Airlines and defense operators are increasingly prioritizing braking efficiency, landing safety, and operational reliability, which is reinforcing demand for advanced thrust reverser actuation systems across both new-build and retrofit programs.

Demand is continuing to strengthen across commercial aircraft, business jets, and military platforms, creating sustained growth opportunities for multiple actuation technologies. Hydraulic systems remain widely deployed due to their proven reliability, whereas electric and electro-hydraulic actuation systems are gaining traction as manufacturers focus on weight reduction, energy efficiency, and simplified maintenance. Pneumatic and mechanical actuation solutions are continuing to serve niche and legacy applications where cost control and design simplicity are critical. Technology adoption is increasingly shaped by trends in aircraft electrification, stricter performance standards, and lifecycle cost optimization.

Key Industry Highlights

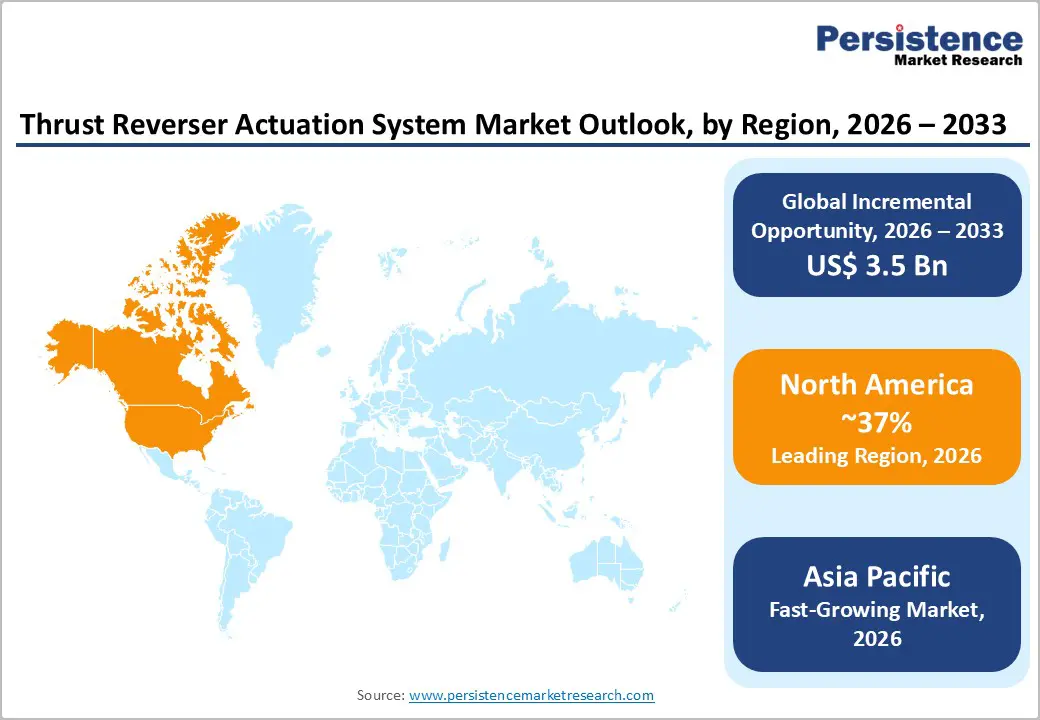

- Regional Leadership: North America is poised to lead with an estimated 37% share in 2026, while Asia Pacific is expected to record the fastest growth at 13.2% CAGR through 2033, fueled by expanding fleets and localized manufacturing.

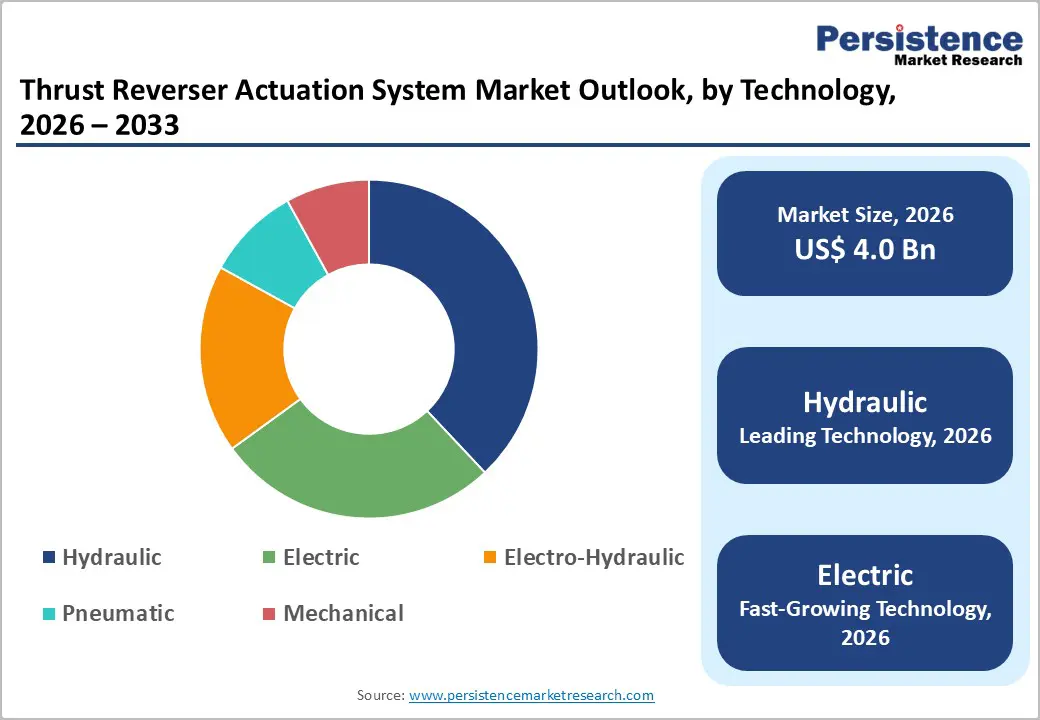

- Dominant Technology: Hydraulic actuation is projected to command around 38% revenue share in 2026, while electric actuation is expected to grow the fastest at about 12% CAGR through 2033, driven by the widening adoption of electric aircraft architectures.

- Leading Application: Commercial aircraft are expected to account for approximately 54% of revenues in 2026, while military and business jets are projected to grow the fastest over 2026–2033, reflecting fleet modernization.

- Advanced System Integration: Electro-hydraulic and smart integrated actuation systems are projected to achieve a 2026-2033 CAGR of approximately 11.3%, driven by predictive maintenance, sensor integration, and digital flight control systems.

- Competitive Environment: Strategic product launches, mergers and acquisitions (M&A), and aftermarket service expansion, aided by digitalization and predictive maintenance integration, are shaping competitive dynamics.

- January 2026: Bombardier announced a US$100 million investment in a new manufacturing hub in Quebec, enhancing production capacity for advanced components, including actuation hardware, through digital manufacturing.

| Key Insights | Details |

|---|---|

| Thrust Reverser Actuation System Market Size (2026E) | US$ 4.0 Bn |

| Market Value Forecast (2033F) | US$ 7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Fleet Expansion, Regulatory Compliance, and Technological Advancements

Original equipment manufacturers (OEMs) such as Boeing and Airbus are increasing production rates of narrow-body and wide-body aircraft, directly boosting demand for thrust reverser actuators. According to forecasts, the global commercial fleet is expected to grow by more than 20% by 2033, underpinning sustained demand for high-performance deceleration systems. These systems improve runway safety and reduce brake wear, particularly on long-haul, high-frequency routes. In 2025, Airbus delivered 793 jetliners, a 4% increase over the previous year, reflecting strong production momentum. Civil aviation regulatory bodies, such as the Federal Aviation Administration (FAA) and the International Civil Aviation Organization (ICAO), have intensified certification requirements for aircraft safety systems, including thrust-reverser actuation technologies. These mandates ensure responsive deployment and reliable performance. Environmental targets for noise and emissions reduction further drive adoption of efficient, lightweight systems.

Technological innovation is another key enabler of growth. The shift from hydraulic to electric and electro-hydraulic actuation reduces complexity, lowers maintenance requirements, and integrates more easily with digital flight controls. Smart sensors, embedded diagnostics, and predictive maintenance enhance reliability while minimizing operational downtime. These systems also optimize deceleration without excessive brake use, supporting fuel efficiency and environmental goals. Advances in materials and digital control technologies further improve aircraft performance and safety. Fleet expansion, regulatory compliance, and technological progress together create strong demand for thrust reverser actuation systems, making them essential across commercial, business, and military aircraft.

High Costs and Supply Chain Complexity Impact Market Expansion

The complexity of thrust reverser actuation systems drives elevated development, certification, and maintenance costs, particularly for advanced electric and hybrid configurations. Smaller aircraft platforms and budget carriers may delay investments in next-generation systems due to cost sensitivity, limiting short-term market expansion. High research & development (R&D) expenditures, rigorous safety certification processes, and long aircraft service lifecycles require suppliers to amortize costs over extended periods. Supply chain complexity, involving precision actuator components, servo controls, sensors, and electronics, adds further challenges. Boeing reported delays in the delivery of several 787 Dreamliner aircraft due to bottlenecks in actuator components. These disruptions highlight the operational difficulties that suppliers face.

The integration of advanced actuation systems across diverse aircraft platforms adds further complexity. Extensive validation, testing, and certification cycles increase lead times for OEMs and system suppliers. Maintaining system reliability while meeting stringent safety standards adds to lifecycle costs and operational challenges. Coordinating multiple suppliers across geographies also increases logistical and financial burdens. Combined with high upfront investment and cost-sensitive customer segments, these factors create structural barriers to rapid adoption. Strategic supplier partnerships and process optimization are critical to sustaining market momentum. These measures help mitigate constraints while supporting market stability.

Expanding Retrofit Demand and Smart Maintenance Integration

As airlines extend the service life of their fleets, retrofit thrust-reverser actuation systems are likely to experience surging demand, creating strong growth opportunities for market players. Upgrading legacy hydraulic systems to electric or hybrid configurations improves fuel efficiency, reduces maintenance downtime, and meets evolving safety standards. Retrofit demand is particularly strong in mature markets with gradual fleet renewal, thereby enabling aftermarket suppliers to capture recurring service revenue. Emerging markets in the Asia Pacific and Latin America are investing in aviation infrastructure and local manufacturing. Airlines in these regions are expanding their fleets with both new and refurbished aircraft, thereby increasing demand for advanced actuation systems. Localized production and joint ventures further enhance regional participation.

Integration with predictive maintenance and IoT-enabled platforms further strengthens growth prospects. Real-time health monitoring and sensor-driven analytics provide continuous feedback, enabling optimized maintenance schedules and failure prevention. In 2025, for instance, Korean Air partnered with Boeing to enhance predictive maintenance across its fleet, improving aircraft reliability and operational efficiency. These smart systems reduce unplanned downtime and support operational sustainability. Coupled with retrofit and regional market growth, digital integration strengthens supplier positioning in the aerospace ecosystem. Increasing adoption of connected maintenance systems drives differentiation and value creation. This convergence creates a favorable environment for the adoption of advanced actuation systems.

Category-wise Analysis

Technology Insights

Hydraulic actuation is expected to lead the market, accounting for approximately 38% of revenue in 2026, due to its high force capability and proven reliability. It dominates wide-body commercial jets and heavy military transports where robust performance is critical. Hydraulic systems benefit from a long certification history, reducing integration risk for OEMs and operators. Platforms such as the Airbus A330 rely on hydraulic systems to manage high load and braking performance. Established maintenance protocols and global service networks support operational uptime. These systems are integrated into both new builds and retrofit programs. The combination of reliability, certification, and service infrastructure secures hydraulic actuation’s market dominance.

Electric actuation is likely to be the fastest-growing segment, with an estimated 12% CAGR through 2033, driven by electrification trends and lightweight design requirements. These systems reduce weight, simplify maintenance, and integrate with digital flight controls. Collins Aerospace expanded electric thrust reverser production in the UK and France, scaling next-generation systems for narrow-body and business jets. Electro-hydraulic systems complement electrical solutions, delivering hybrid performance for versatile adoption, while embedded sensors and predictive diagnostics enhance reliability and reduce operational costs. OEMs increasingly adopt electric actuators for efficiency and integration benefits, positioning electric actuation as the primary growth driver in modern aircraft designs.

Application Insights

Commercial aircraft are expected to dominate the market for thrust reverser actuation systems, accounting for approximately 58% of total demand in 2026, driven by high aircraft delivery volumes and stringent safety requirements. Major OEMs are increasing production output to meet airline demand, as reflected by Embraer’s projection of an 18% rise in commercial jet deliveries during 2025. Narrowbody and widebody platforms, such as the Airbus A320 and A350 families, are integrating reliable thrust-reverser actuation systems to ensure safe landing performance and reduce brake wear in high-frequency operations. In parallel, retrofit and upgrade programs are expanding demand for both replacement systems and performance enhancements across in-service fleets. High utilization rates and well-established maintenance, repair, & overhaul (MRO) networks are reinforcing the long-term leadership of commercial aircraft within this application segment.

Business jets and military aircraft are emerging as the fastest-growing applications, with a projected 2026-2033 CAGR of 10.8%, driven by increasing adoption of advanced actuation technologies. Business aviation is benefiting from the integration of lightweight electric and electro-hydraulic systems, as demonstrated by the delivery of next-generation platforms such as the Gulfstream G700 and G800, which are supporting higher performance and improved system efficiency. Military demand is strengthening through continued deliveries of transport aircraft such as the Lockheed Martin C-130J Super Hercules, where thrust reverser reliability is critical under demanding operational conditions. Fleet modernization programs, combined with smart diagnostics and electrification, are improving system efficiency and reducing maintenance requirements. These factors collectively drive faster growth in business jet and military applications than in the more mature commercial aircraft segment.

Regional Insights

North America Thrust Reverser Actuation System Market Trends

North America is expected to account for approximately 37% of the thrust reverser actuation system market in 2026, supported by a deeply integrated aerospace manufacturing and services ecosystem. The United States accounts for most regional demand, driven by strong commercial aircraft production and sustained defense procurement programs. A high concentration of OEMs and Tier-1 suppliers is accelerating the adoption of advanced actuation technologies across both civil and military platforms. Regulatory oversight by the FAA ensures strict safety, reliability, and performance standards, which reinforces demand for high-quality actuation systems. High fleet utilization rates are sustaining robust aftermarket demand for system upgrades, replacements, and servicing. Moog Inc. is expanding its aerospace actuation manufacturing footprint in New York, strengthening domestic production capacity and reinforcing regional leadership in safety-critical systems.

Long-term defense contracts provide demand stability across economic cycles and fluctuations in aircraft deliveries. Federal research and development incentives are continuing to support electrification initiatives and digital system integration across flight control and actuation platforms. A mature MRO ecosystem enables extended-lifecycle revenue opportunities beyond original equipment installations. Adoption of predictive maintenance tools is improving system reliability and operational efficiency for fleet operators. Clear certification pathways are reducing time to market for next-generation actuation solutions. Ongoing collaboration between suppliers, aerospace manufacturers, and government research institutions is sustaining innovation momentum, ensuring that North America will retain its dominant position in the global thrust reverser actuation system market over the forecast period.

Europe Thrust Reverser Actuation System Market Trends

Europe represents a major regional market for thrust reverser actuation systems, since it is home to well-established aerospace clusters across Germany, France, the U.K., and Spain. The region is benefiting from balanced demand across commercial aviation and military transport programs, with Airbus-led aircraft production anchoring sustained system integration. Harmonized regulatory oversight under the European Union Aviation Safety Agency (EASA) is ensuring consistency in certification, safety, and performance requirements across member states. Environmental priorities are increasingly shaping system design, as manufacturers are focusing on lighter, quieter, and more energy-efficient actuation solutions. Safran Nacelles is expanding smart manufacturing capabilities at its Le Havre facility, strengthening vertically integrated production of advanced actuation systems and reinforcing Europe’s emphasis on precision engineering.

Market growth in Europe is driven primarily by technology modernization, not by aircraft volume expansion alone. Regional suppliers are specializing in high-precision components and advanced system integration capabilities to meet evolving performance and sustainability requirements. Defense modernization initiatives are continuing to support steady demand for military transport aircraft, contributing to baseline market stability. Public and private collaboration frameworks are accelerating system testing, certification, and digital validation processes, reducing development risk for next-generation technologies. Regulatory focus on emissions reduction and noise control is encouraging wider adoption of electric and hybrid actuation architectures. Competitive dynamics are balancing established aerospace leaders with emerging specialist suppliers, which is sustaining innovation intensity and reinforcing Europe’s long-term competitiveness in thrust reverser actuation systems.

Asia Pacific Thrust Reverser Actuation System Market Trends

Asia-Pacific is projected to be the fastest-growing market for thrust reverser actuation systems, with an estimated 13.2% CAGR from 2026 to 2033. Rising passenger traffic is continuing to drive aggressive fleet expansion across major economies, while the growing penetration of low-cost carriers is increasing aircraft utilization rates. Governments across the region are actively promoting domestic aerospace manufacturing and system localization to reduce import dependence and strengthen supply chains. Demand is spanning both new aircraft deliveries and aftermarket services, as expanding fleets require ongoing maintenance and system upgrades. The increase in Commercial Aircraft Corporation of China (COMAC) C919 deliveries to domestic airlines is reinforcing regional demand for integrated actuation systems and is highlighting the Asia Pacific’s growing role in global aviation programs.

India and Southeast Asia are emerging as critical contributors to regional growth momentum, supported by expanding civil aviation networks and defense modernization initiatives. Military procurement programs are increasing the demand for robust and reliable actuation systems across transport and surveillance platforms. Regulatory frameworks are becoming more closely aligned with international safety standards, which is improving certification clarity and encouraging technology transfer. Global suppliers are forming targeted joint ventures with regional manufacturers to support localization strategies and accelerate market entry. Localized production is improving cost efficiency and service responsiveness, while aftermarket infrastructure is expanding in parallel with fleet growth.

Competitive Landscape

The global thrust reverser actuation system market structure is moderately consolidated, led by a small group of aerospace giants with deeply embedded relationships with OEMs. Companies such as Safran, Collins Aerospace, Liebherr Aerospace, and Parker Aerospace are maintaining leadership through long-term participation in both commercial and military aircraft programs. Their competitive strength is being reinforced by extensive certification expertise, vertically integrated manufacturing capabilities, and consistently high system reliability. Continuous investment in research and development is supporting the advancement of electric and hybrid actuation technologies, aligning product portfolios with aircraft electrification trends. Early involvement in aircraft design and development cycles is creating high switching costs for airframers, while comprehensive aftermarket support is further strengthening customer retention and long-term revenue stability.

Specialized suppliers such as Moog and Triumph Group are competing through high-precision actuation components, advanced control electronics, and lifecycle service offerings. These companies are focusing on platform-specific programs and aftermarket optimization rather than pursuing broad volume leadership across all aircraft categories. High regulatory requirements and complex system integration processes are continuing to limit new entrant participation in core actuation hardware. However, the growing adoption of digital health monitoring and predictive maintenance solutions is enabling collaboration with software-focused specialists. Competitive strategies are increasingly prioritizing long-term supply agreements, retrofit programs, and service-led revenue models.

Key Industry Developments

- In July 2025, Warburg Pincus and Berkshire Partners completed the acquisition of Triumph Group, transitioning the company to private ownership in a deal valued at approximately US$ 3 billion. The move is intended to accelerate growth across Triumph’s mission-critical aerospace systems portfolio, including actuation and structural components.

- In June 2025, Collins Aerospace opened a new engineering center in the U.K., dedicated to next-generation elecTRAS™ electric thrust reverser actuation systems, alongside a new final assembly line in France. The expansion supports the transition away from hydraulic systems, enabling lighter architectures and improved aircraft efficiency.

- In April 2025, Safran Nacelles signed a NacelleLife™ service agreement with Republic Airways covering maintenance and spare parts support for thrust reversers on Embraer 170/175 aircraft, supporting a fleet of over 200 aircraft. Services are delivered through Safran’s Indianapolis facility, focusing on advanced repairs and operational efficiency.

Companies Covered in Thrust Reverser Actuation System Market

- Triumph Group

- Woodward Inc

- Parker Hannifin

- Arkwin Industries

- Singapore Technologies Engineering

- Safran

- Spirit AeroSystems

- General Electric

- Collins Aerospace

- Honeywell

- Moog Inc

- UTC Aerospace

- Liebherr

Frequently Asked Questions

The global thrust reverser actuation system market is projected to reach US$ 4.0 billion in 2026.

Increasing aircraft production, stringent safety regulations, and increased emphasis on landing performance and operational reliability are the driving forces of the market.

The market is poised to witness a CAGR of around 9.4% from 2026 to 2033.

Key opportunities include electric and hybrid actuation adoption, retrofit demand from aging fleets, and integration of smart monitoring systems.

Safran, Collins Aerospace, Liebherr Aerospace, Parker Aerospace, and Moog are a few among the key players in the market.