- Biotechnology

- Rapid Influenza Diagnostic Tests (RIDTs) Market

Rapid Influenza Diagnostic Tests (RIDTs) Market Size, Share, and Growth Forecast, 2026 - 2033

Rapid Influenza Diagnostic Tests (RIDTs) Market by Product Type (Conventional RIDTs, Digital RIDTs), Test Type (Rapid Molecular Assays, Rapid Immunoassays, Others), End-user (Hospitals & Clinics, Others), and Regional Analysis for 2026 - 2033

Rapid Influenza Diagnostic Tests (RIDTs) Market Share and Trends Analysis

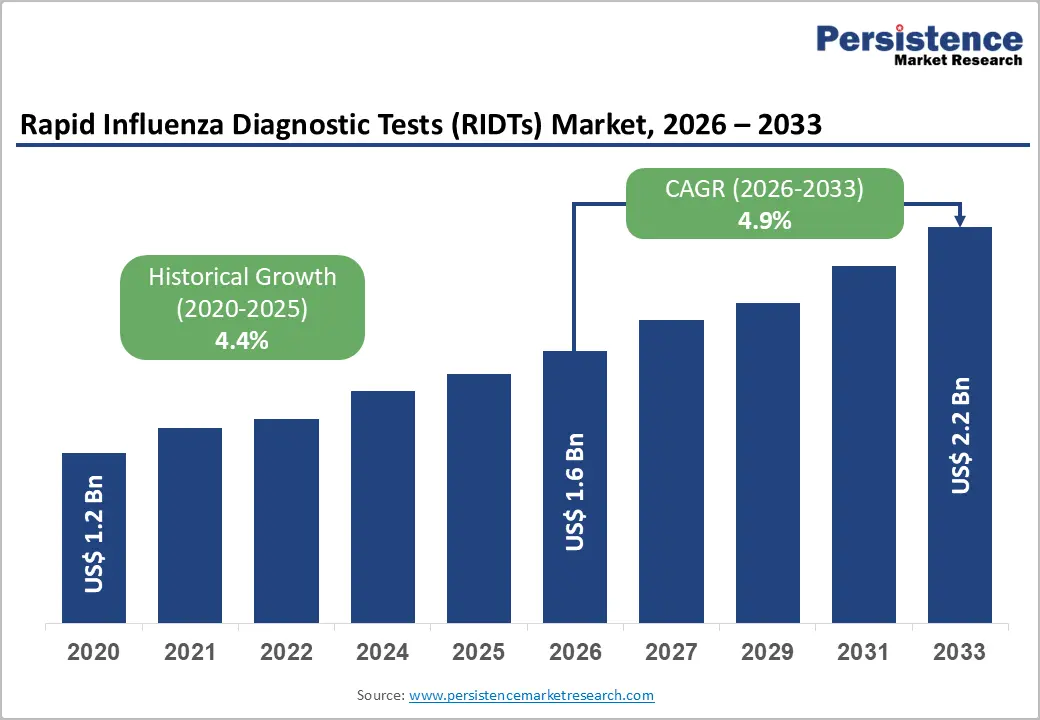

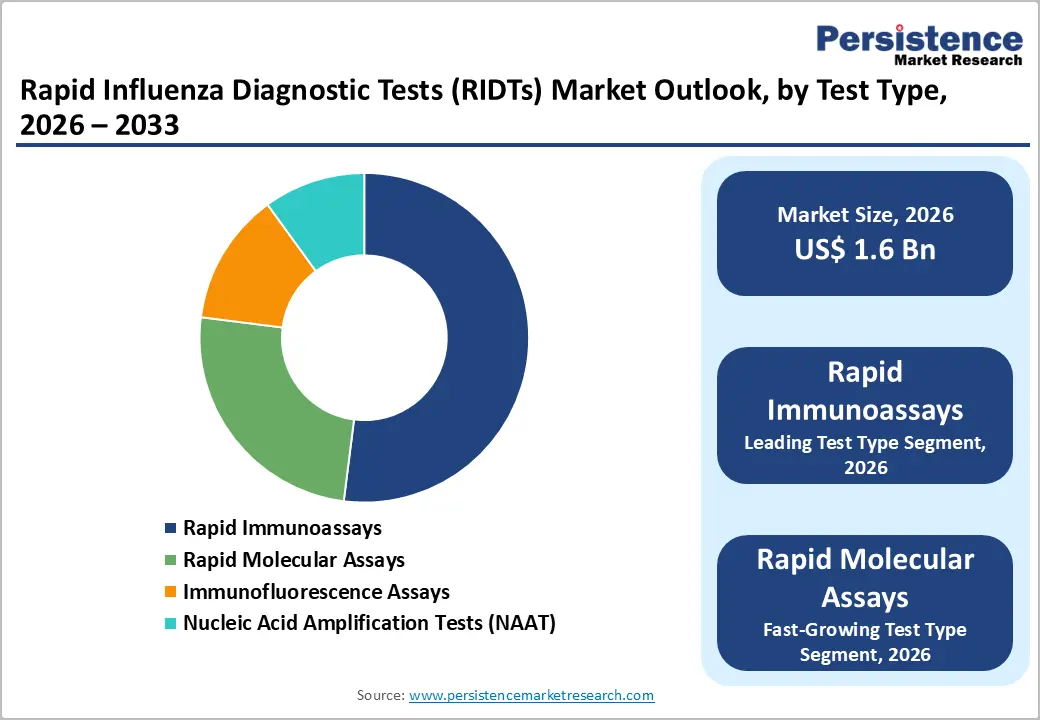

The global rapid influenza diagnostic tests (RIDTs) market size is likely to be valued at US$1.6 billion in 2026 and is estimated to reach US$2.2 billion by 2033, growing at a CAGR of 4.9% during the forecast period 2026 - 2033, driven by changing demographic patterns characterized by an aging global population highly susceptible to severe respiratory illnesses.

Stricter regulatory updates from bodies such as the United States Food and Drug Administration necessitate higher clinical sensitivity in diagnostic devices, accelerating the replacement of older testing methods. Rapid technological transition toward digital strip readers and decentralized molecular assays streamlines workflows across diverse clinical environments.

Key Industry Highlights:

- Leading Test Type: Rapid immunoassays are set to hold around 52% revenue share in 2026, driven by their rapid processing times that provide clear qualitative results within twenty minutes of sample exposure.

- Fastest-Growing Test Type: Rapid molecular assays are projected as the fastest-growing segment, supported by rising clinical demands for laboratory-grade diagnostic sensitivity directly at point-of-care locations.

- Leading End-user: Hospitals & clinics are estimated to hold roughly 42% revenue share in 2026, due to high emergency department patient volumes requiring immediate triaging decisions during seasonal outbreaks.

- Fastest-growing End-user: Point-of-care settings are forecast to record the fastest growth, driven by the ongoing decentralization of testing services away from central laboratories to urgent care centers.

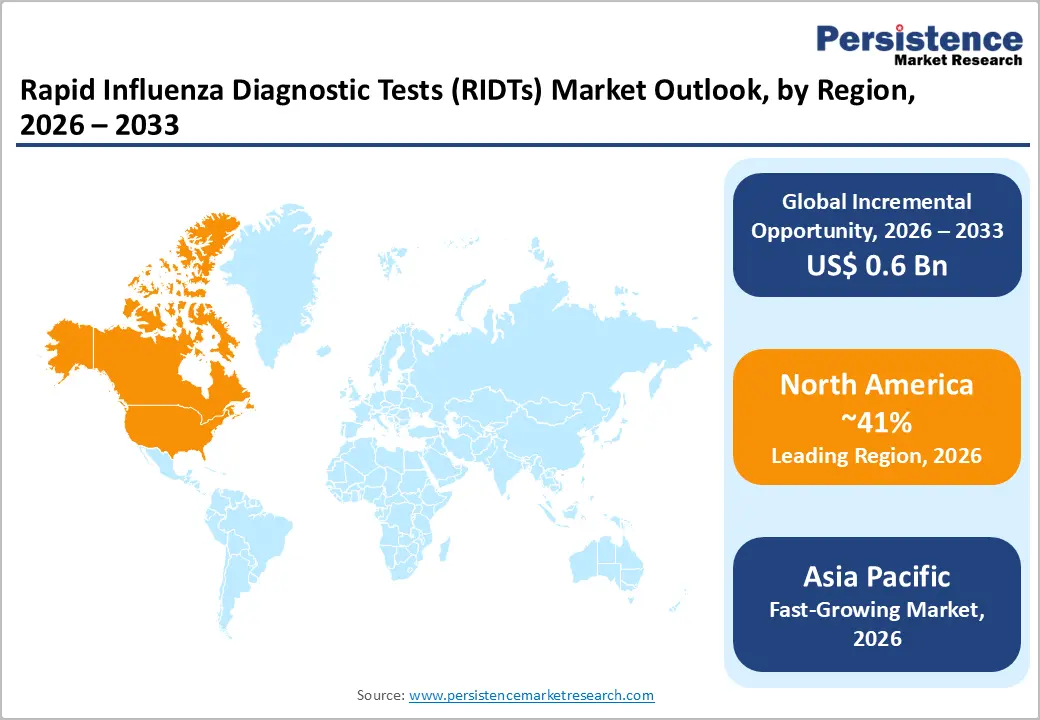

- Regional Leadership: North America is projected to capture roughly 41% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding healthcare infrastructure investments.

- Competitive Environment: The global environment is moderately fragmented, forcing key participants to utilize extensive distribution partnerships to protect their regional market positioning.

- Innovation Trends: Product development focuses on multiplex diagnostic designs, enabling the simultaneous detection of multiple viral pathogens from a single patient sample.

DRO Analysis

Driver - Escalating Geriatric Population and Respiratory Disease Burden

Demographic shifts toward an older average population age globally elevate the volume of clinical presentations requiring urgent differential diagnosis. Chronic conditions in older cohorts lower immune responses, transforming standard seasonal influenza infections into critical medical risks that demand immediate intervention. Rapid diagnostic intervention prevents prolonged institutional stays, driving high-volume procurement across acute care facilities.

Statistical data from the Centers for Disease Control and Prevention regarding the 2025-2026 respiratory season indicated approximately 29 million illnesses and 360,000 hospitalizations in the U.S. alone. This substantial disease volume strains emergency departments, forcing healthcare systems to deploy rapid testing methods to optimize patient triaging and bed management. Surging patient volumes accelerate clinical adoption rates, ensuring consistent market demand.

Restraint - Sensitivity Limitations of Conventional Rapid Tests

Conventional antigen-based influenza diagnostic platforms continue to face sensitivity limitations during early-stage infection detection. False-negative outcomes increase the requirement for confirmatory molecular testing, creating additional operational costs for healthcare providers. Lower diagnostic confidence can restrict adoption across critical care environments where clinical accuracy directly affects treatment pathways and patient isolation protocols.

Manufacturing cost pressures linked with regulatory compliance upgrades are also affecting scalability among smaller diagnostic suppliers. Performance validation standards introduced by regulatory authorities require continuous product optimization and quality monitoring. Increased expenditure on assay redesign, validation studies, and manufacturing adjustments can reduce operating margins across price-sensitive healthcare procurement environments.

Opportunity - Integration of Multiplex Testing Panels at Point-of-Care

Developing diagnostic panels that simultaneously identify multiple respiratory pathogens creates a clear pathway for commercial expansion. Co-circulating viruses present identical initial physical symptoms, requiring multi-pathogen screening from a single patient sample collection. Combining influenza detection with other seasonal respiratory targets improves institutional workflow efficiency.

Medical facilities derive higher economic value from single-sample multiplex assays, reducing the total volume of individual tests performed per patient. This clinical utility justifies higher procurement prices, expanding profit margins for manufacturing companies. Multiplex product development opens new high-value clinical avenues, driving substantial revenue growth.

Category-wise Analysis

Product Type Insights

Conventional RIDTs are expected to lead the rapid influenza diagnostic tests market, accounting for approximately 58% of revenue in 2026. These established testing systems offer low production costs and require minimal operator training across standard healthcare environments. The widespread availability of basic lateral flow strips in rural clinical settings sustains high shipment volumes globally. Low pricing structures support high-volume institutional purchasing protocols.

Digital RIDTs are likely to represent the fastest-growing segment, propelled by the medical necessity for higher diagnostic accuracy and automated data capture. Advanced digital optical readers eliminate subjective visual interpretation errors, elevating diagnostic precision during active clinical triaging. Incorporating automated benchtop analyzer units in community hospitals optimizes data entry workflows into institutional networks. Digital processing capabilities accelerate overall clinical testing adoption.

Test Type Insights

Rapid immunoassays are projected to lead the market, capturing around 52% of the revenue share in 2026. The widespread deployment of these tests depends on rapid processing times, yielding clear qualitative results within twenty minutes of sample exposure. Utilizing basic lateral flow cassettes during outpatient visits allows immediate treatment decisions without waiting for laboratory confirmation. Processing speed ensures dominant placement within emergency medical workflows.

Rapid molecular assays are likely to be the fastest-growing segment, fueled by the rising preference for laboratory-grade sensitivity at point-of-care locations. These compact testing systems utilize simplified isothermal nucleic acid amplification to deliver high accuracy within short timeframes. Implementing automated molecular workstations in decentralized testing locations improves diagnostic confidence without expanding laboratory space. High accuracy levels stimulate rapid clinical deployment.

End-user Insights

Hospitals & clinics are likely to be the leading segment with a projected 42% of the Rapid Influenza Diagnostic Tests market share in 2026 due to high emergency department patient volumes during seasonal outbreaks. These acute care centers require rapid diagnostic confirmation to guide immediate isolation decisions and antiviral prescriptions. Utilizing multi-tier triage systems in busy metropolitan emergency hubs requires large inventories of point-of-care testing kits. High patient density drives consistent bulk procurement activities.

Point-of-care settings are anticipated to be the fastest-growing segment, fueled by the ongoing decentralization of patient diagnostic services. Shifting testing protocols away from central laboratories directly to urgent care centers reduces total turnaround time. Operating compact standalone testing modules within retail clinics enables immediate diagnostic services during standard patient consultations. Decentralized diagnostic services accelerate decentralized testing demand.

Regional Insights

North America Rapid Influenza Diagnostic Tests (RIDTs) Market Trends

North America is anticipated to be the leading region, accounting for a market share of 41% in 2026, driven by strict regulatory standards established by the United States Food and Drug Administration regarding point-of-care diagnostic sensitivity. The presence of established healthcare networks facilitates rapid adoption of advanced digital and molecular testing devices. Extensive reimbursement coverage for diagnostic testing supports high utilization rates across healthcare systems.

U.S. Rapid Influenza Diagnostic Tests (RIDTs) Market Insights

The U.S. is expected to maintain high procurement levels due to the integration of digital diagnostic reporting with hospital electronic health networks. The presence of major industry innovators like QuidelOrtho Corporation and Becton, Dickinson and Company accelerates local technology transitions. National surveillance initiatives managed by public health agencies encourage widespread testing to monitor circulating viral strains.

Canada Rapid Influenza Diagnostic Tests (RIDTs) Market Insights

Canada is projected to experience steady market expansion driven by provincial healthcare investments aimed at improving diagnostic access in remote territories. Public procurement agencies prioritize decentralized testing equipment to lower seasonal burdens on urban emergency centers. Growing integration of diagnostic platforms within telehealth frameworks supports patient management in rural communities.

Europe Rapid Influenza Diagnostic Tests (RIDTs) Market Trends

Europe is forecast to hold a substantial market share, supported by national health systems prioritizing early diagnostic screening to reduce seasonal hospital admission rates. Strict compliance with European Union In Vitro Diagnostic Medical Device Regulations drives product design updates among regional manufacturers. Growing collaboration between public health laboratories and private diagnostic providers enhances regional disease monitoring capabilities.

Germany Rapid Influenza Diagnostic Tests (RIDTs) Market Insights

Germany is expected to lead regional market expansion due to its highly developed laboratory network and swift adoption of point-of-care molecular technologies. The presence of established domestic suppliers like Siemens Healthineers AG supports local device placement and technical maintenance services. Statutory health insurance frameworks provide clear reimbursement pathways for rapid testing in outpatient settings, encouraging routine clinical use.

U.K. Rapid Influenza Diagnostic Tests (RIDTs) Market Insights

The U.K. is likely to expand its diagnostic capabilities through National Health Service initiatives focused on establishing community diagnostic hubs outside traditional hospital walls. Broad adoption of multiplex testing systems helps differentiate between influenza and other circulating seasonal pathogens. National procurement programs secure bulk quantities of lateral flow kits to manage seasonal spikes in healthcare demand.

Asia Pacific Rapid Influenza Diagnostic Tests (RIDTs) Market Trends

Asia Pacific is forecast to be the fastest-growing market for rapid influenza diagnostic tests, stimulated by expanding healthcare infrastructure investments and rising public awareness regarding infectious disease management. Growing populations and increasing healthcare spending across developing countries support high-volume procurement of point-of-care testing kits.

China Rapid Influenza Diagnostic Tests (RIDTs) Market Insights

China is projected to experience rapid market growth due to government initiatives aimed at strengthening primary healthcare clinics in rural provinces. Domestic manufacturing entities like Shanghai Fosun Pharmaceutical Industrial Development Co., Ltd. increase production capacity for low-cost, rapid test kits. Expanding clinical networks in growing urban centers require large quantities of rapid diagnostic tools for daily patient screening.

Japan Rapid Influenza Diagnostic Tests (RIDTs) Market Insights

Japan is expected to show stable market demand driven by its high density of elderly citizens and a deeply ingrained clinical culture of early viral testing. Well-developed distribution partnerships involving companies such as Sysmex Corporation ensure steady delivery of diagnostic products to community clinics. National health insurance systems provide complete coverage for rapid influenza diagnostic testing, encouraging immediate testing upon symptom presentation.

Competitive Landscape

The global rapid influenza diagnostic tests market is moderately fragmented, featuring a mix of large international medical device corporations and specialized diagnostic manufacturers. Established entities utilize extensive distribution networks and deep capital reserves to maintain leading market positions across major regions.

Smaller market entrants focus on developing specialized molecular technologies to compete in high-sensitivity market segments. Key industry participants shaping international competition include Abbott Laboratories, Becton, Dickinson and Company, QuidelOrtho Corporation, F. Hoffmann-La Roche Ltd, and Meridian Bioscience, Inc.

Companies Covered in Rapid Influenza Diagnostic Tests (RIDTs) Market

- Abbott Laboratories

- Becton, Dickinson and Company

- QuidelOrtho Corporation

- F. Hoffmann-La Roche Ltd

- Meridian Bioscience, Inc.

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific Inc.

- Sekisui Diagnostics

- Princeton BioMeditech Corporation

- SA Scientific, Ltd.

- Coris BioConcept

- Lumos Diagnostics, Inc.

Frequently Asked Questions

The RIDTs market is projected to reach US$1.6 billion in 2026.

Increasing seasonal influenza incidence, expanding point-of-care diagnostic adoption, and rising demand for rapid infectious disease screening are driving the RIDTs market.

The RIDTs market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Expansion of home-based influenza testing solutions and increasing adoption of multiplex molecular respiratory diagnostics are creating key growth opportunities in the RIDTs market.

Some of the key market players include Abbott Laboratories, Becton, Dickinson and Company, QuidelOrtho Corporation, F. Hoffmann-La Roche Ltd, and Meridian Bioscience, Inc.