- Food Ingredients & Additives

- Quinoa Market

Quinoa Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Quinoa Market by Product Type (Seeds, Flour Flakes, Puffs), by Nature (Conventional, Organic), by Distribution Channel, and Regional Analysis from 2026 - 2033

Quinoa Market Share and Trends Analysis

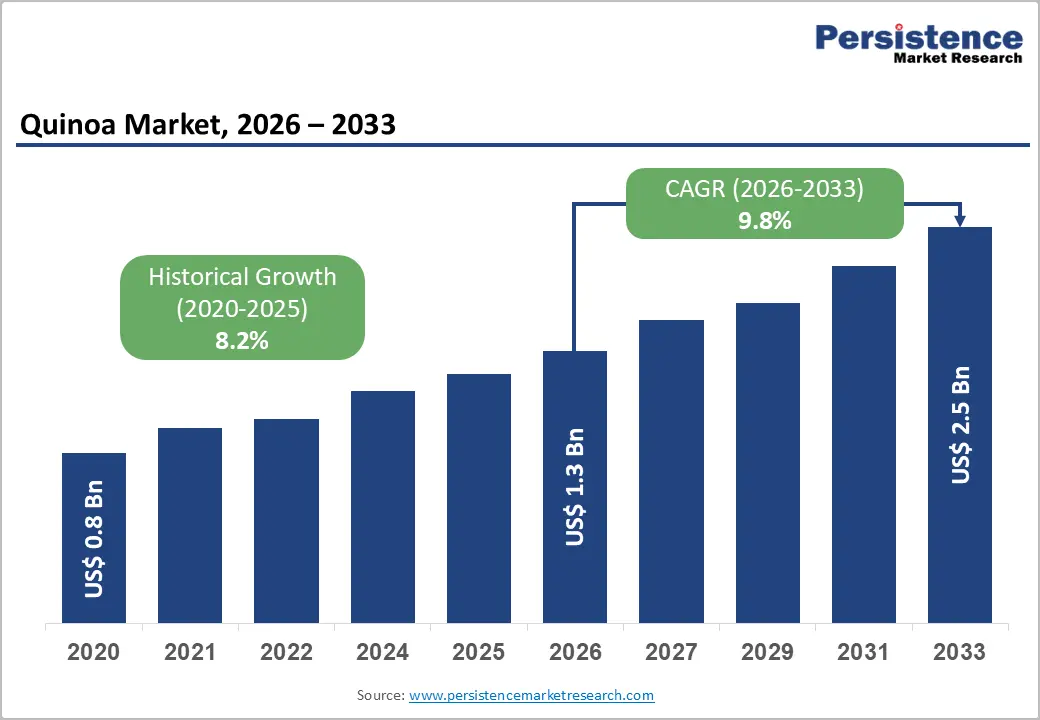

The global quinoa market size is likely to be valued at US$ 1.3 billion in 2026 to US$ 2.5 billion by 2033 growing at a CAGR of 9.8% during the forecast period from 2026 to 2033.

In recent years, the market experienced significant growth driven by increasing consumer demand for healthy and nutritious food options. Quinoa, a grain-like crop known for its high protein content and gluten-free properties, has become a versatile ingredient in various cuisines globally. Consumers are increasingly seeking organic and sustainably sourced food products. The organic quinoa industry is expected to grow significantly driven by the rising preference for chemical-free and environment-friendly agricultural practices. Quinoa's versatility as an ingredient has contributed to its growing popularity in the food industry. Growing awareness about quinoa's health benefits has fueled its demand among health-conscious consumers. All these quinoa market trends are expected to continue their growth trajectory in the coming years.

Key Industry Highlights

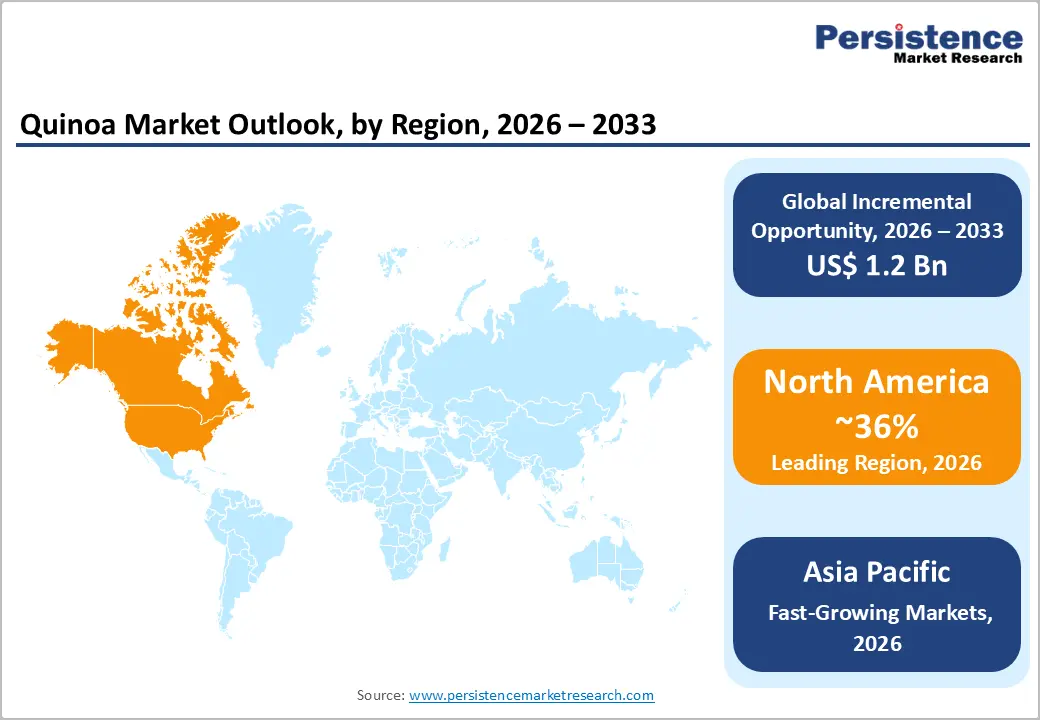

- Leading Region: North America leads the Quinoa Market, supported by high consumer awareness of health and wellness, increasing adoption of gluten-free and plant-based diets, and strong presence of organized retail and e-commerce platforms.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising demand for organic, fair-trade, and sustainably sourced quinoa, an expanding health-conscious consumer base, and government programs promoting climate-resilient crops.

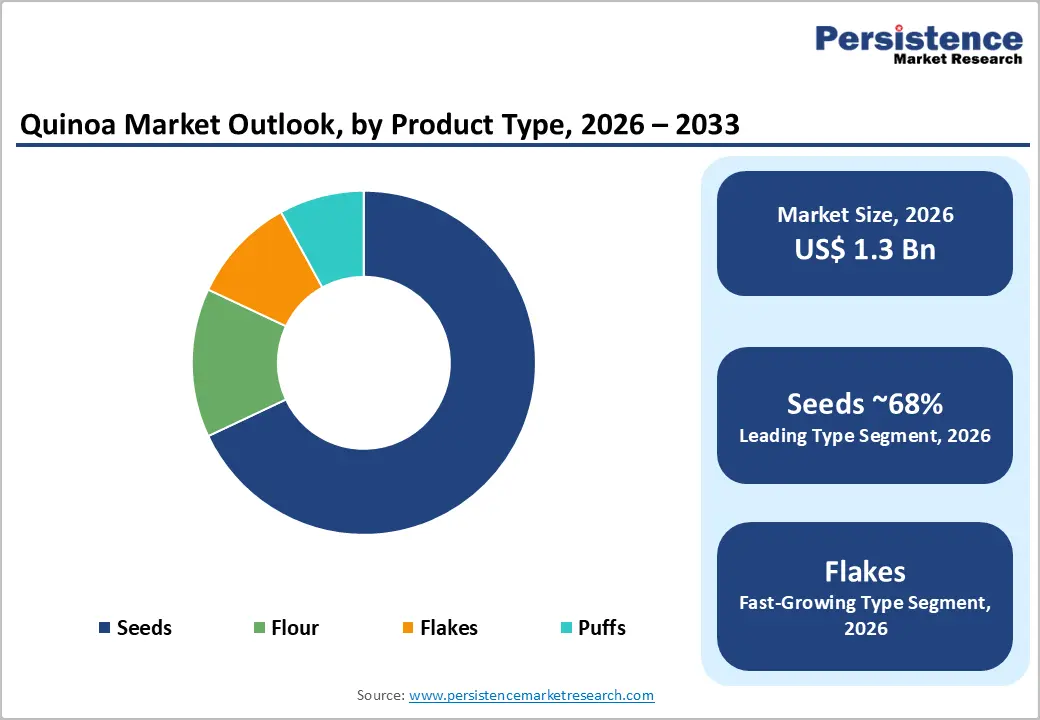

- Dominant Segment: Quinoa seeds dominate the market, owing to their versatility in home cooking, foodservice, and ready-to-eat meals, widespread consumer familiarity, and ability to retain full nutritional value with minimal processing.

- Fastest Growing Segment: Quinoa flakes are the fastest-growing product type, fueled by increasing adoption in convenient and ready-to-eat foods, breakfast cereals, snacks, and functional food products targeting health-conscious consumers.

| Key Insights | Details |

|---|---|

|

Quinoa Market Size (2026E) |

US$ 1.3 Bn |

|

Market Value Forecast (2033F) |

US$ 2.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.2% |

Market Dynamics

Driver - Rising Demand for Gluten-Free and High-Protein Foods

Growing prevalence of gluten intolerance, celiac disease, and lifestyle-driven gluten avoidance is a core driver of quinoa demand, as the grain is naturally gluten-free yet protein-dense. Clinical and nutritional reviews indicate that quinoa delivers around 14 g of protein per 100 g, along with higher fiber and micronutrient levels than common staples like rice or wheat, enabling formulators to enhance satiety and nutritional quality in gluten-free products. In North America and Europe, supermarket shelves feature an expanding range of quinoa-based breads, pastas, breakfast cereals, and snack bars, meeting consumer expectations for clean-label, minimally processed ingredients. In parallel, increased awareness of plant-based diets as recommended by organizations such as FAO for sustainability and health is steering both households and institutional buyers toward alternative grains such as quinoa.

Increasing Consumer Demand for Healthy and Nutritious Food

The growing consumer demand for healthy and nutritious food options is driving the quinoa market growth. Quinoa is known for its nutritional characteristics and health benefits including high protein content, essential amino acids, and dietary fiber. As consumers become health-conscious, the demand for quinoa as a nutritious alternative to traditional grains is rising.

With rising awareness about various dietary trends and health conditions such as gluten intolerance, celiac disease, and metabolic disorders, quinoa has gained traction. It is naturally gluten-free making it a valuable alternative for people with gluten sensitivities or those seeking to avoid gluten.

The broad movement toward whole and minimally processed foods have bolstered quinoa’s popularity. Consumers are seeking out foods that are less processed and more aligned with natural dietary practices. Quinoa fits well within this movement due to its whole-grain status and its minimal processing requirements.

Restraints - Price Volatility and Affordability Challenges

Despite its benefits, quinoa remains more expensive than staple grains, limiting adoption in price-sensitive markets. Global production, concentrated historically in Peru, Bolivia, and Ecuador, has experienced yield fluctuations tied to climate variability and agronomic constraints, driving price volatility at farm and retail levels. For low- and middle-income consumers, a price premium of often 2–3 times that of rice or wheat makes regular consumption difficult, while food manufacturers face higher input costs when using quinoa as a primary ingredient versus a minor fortification component.

Limited Variety Cultivation

The market growth is restricted due to the limited cultivation of certain quinoa varieties. Research suggests that a significant portion of quinoa production comes from only a few commercially viable types or cultivars out of the many varieties available. This limited variety of cultivation can hinder the market's potential for diversification and may restrict the availability of different quinoa types.

A lack of variety can reduce the appeal of quinoa to consumers who seek diverse options. For instance, different varieties may have distinct flavors, textures, or nutritional profiles. Limited variety could therefore restrict consumer choice and potentially limit market expansion.

Different quinoa varieties may be suited to different climates and soil conditions. Cultivating a limited range may restrict the geographical areas where quinoa can be effectively grown, limiting overall production capacity and market reach.

Opportunity - Expansion of Organic and Sustainable Quinoa Production

Growing consumer preference for organic, fair-trade, and sustainably produced foods is creating a strong opportunity for expansion in the global quinoa market. Health-conscious consumers are increasingly seeking clean-label grains with verified environmental and ethical credentials, driving demand for certified organic quinoa. International organizations such as the FAO, along with regional agricultural programs in Europe and North America, are actively promoting quinoa as a climate-resilient crop. These initiatives support pilot cultivation projects, research on adaptable seed varieties, and sustainable farming practices suited to non-Andean regions.

Organic quinoa continues to command a 30–50% price premium, making it attractive for both farmers and food manufacturers. It is increasingly used in baby foods, premium breakfast cereals, plant-based products, and specialty health-store assortments, particularly in markets such as Germany, France, and the United States. As farmers in Europe, North America, and parts of Asia adopt environmentally responsible cultivation methods, supply diversification is expected to reduce reliance on traditional Andean sources. This shift can help stabilize prices, improve supply security, and enable long-term sourcing agreements with multinational food companies that prioritize sustainability and traceability.

Category-wise Analysis

By Product Type

The global quinoa market is dominated by seeds, which account for approximately 68% of total market share in 2025. This leadership is primarily driven by strong consumer familiarity and the versatility of whole quinoa seeds across home cooking, foodservice, and ready-to-eat meals. Whole seeds are widely used as substitutes for rice, couscous, and other grains, enabling consumers to retain quinoa’s full nutritional value with minimal processing. Their broad acceptance across diverse cuisines and dietary patterns continues to support sustained demand.

Global quinoa production has expanded significantly since 2010, with major producing countries such as Peru and Bolivia focusing largely on seed cultivation for international markets. A considerable share of this production is sold through retail channels as packaged whole grain quinoa. Retailers strengthen seed dominance through clear packaging, preparation instructions, and nutrition-focused labeling that emphasizes protein content, fiber, and gluten-free benefits. In contrast, secondary product forms such as flour and flakes are mainly positioned as ingredients for processed foods rather than everyday staples. Consequently, whole quinoa seeds maintain a clear competitive advantage within the overall product mix.

By Distribution Channels

The B2C distribution channel dominates the global quinoa market, as quinoa is predominantly purchased for household consumption and direct use. Supermarkets, hypermarkets, specialty health food stores, and online platforms form the core retail outlets driving sales. In regions such as North America and Europe, quinoa has transitioned from a niche health product to a mainstream grain, now widely available in standard grocery aisles alongside rice and pasta. Private-label offerings and branded products further strengthen household penetration and repeat purchasing behavior.

Specialty and organic retailers play a key role in premium, organic, and fair-trade quinoa offerings, catering to health-conscious and sustainability-focused consumers. Meanwhile, e-commerce platforms in markets including the U.S., U.K., China, and India enable access to a wider product range, such as single-origin, organic, and value-added quinoa blends. Although B2B channels serving food manufacturers, foodservice operators, and institutions are expanding steadily, B2C remains the most influential channel. Its dominance is supported by strong retail visibility, branding initiatives, and direct engagement with end consumers prioritizing nutrition and wellness.

Region-wise Insights

North America Quinoa Market Trends

North America is poised to lead the quinoa market, propelled by a rising focus on health and a shift towards premium food options. As health awareness grows and consumers seek out high-quality, nutritious foods, quinoa is gaining significant traction across developed countries in the region. This surge in popularity underscores a broader commitment to adopting healthier eating habits and making more informed dietary choices.

Premium food options often emphasize health and nutrition. Quinoa, known for its high protein content, essential amino acids, and other nutrients, aligns well with these demands. As consumers become more health-conscious, they are more likely to choose quinoa over less nutritious alternative.

The broad health and wellness movement in North America emphasizes the importance of high-quality ingredients. Quinoa’s reputation for supporting a balanced diet and promoting overall well-being resonates with consumers who are willing to pay more for foods that contribute to their health goals.

Europe Quinoa Market Trends

Europe is a critical growth region for quinoa, with Germany, the U.K., France, and Spain at the forefront of demand. Rising adoption of plant-based diets and higher-than-average consumption of organic foods drive strong retail performance of quinoa across health-food chains and supermarkets. European consumers value sustainability and fair-trade attributes, leading to robust demand for certified organic and ethically sourced quinoa, often supported by partnerships with Andean smallholders.

Regulatory harmonization under European Union food law, including strict controls on pesticide residues and labeling, shapes the competitive landscape by favoring suppliers that can consistently meet EU MRLs. At the same time, agronomic initiatives in countries like Spain, France, and the U.K. are fostering local quinoa cultivation to reduce import dependence and improve supply-chain resilience. These developments, combined with widespread use of quinoa in bakery, breakfast cereals, meat analogues, and ready meals, position Europe as a structurally important and steadily expanding market for both conventional and organic quinoa.

Asia Pacific Quinoa Market Trends

Asia Pacific is emerging as one of the fastest-growing quinoa markets, driven by rising urbanization, income growth, and health awareness in China, India, Japan, and ASEAN countries. In China, quinoa imports and local cultivation have increased as consumers seek diversified grain options aligned with weight management and wellness diets, with some estimates showing double-digit annual growth in quinoa-based product launches. India has begun experimenting with domestic quinoa production in states such as Rajasthan and Andhra Pradesh, leveraging the crop’s tolerance to semi-arid conditions and its potential contribution to nutrition security.

The region benefits from manufacturing advantages such as lower processing costs and rapidly expanding modern retail and online grocery infrastructure. Japanese and Australian food companies incorporate quinoa into ready meals, bakery, and infant nutrition, while ASEAN markets are gradually adopting quinoa through premium retailers and hospitality segments. Government programs promoting crop diversification and healthier eating patterns in several Asia Pacific countries reinforce the long-term growth outlook, positioning the region as a key engine of incremental quinoa demand over the forecast period.

Competitive Landscape

The global quinoa market is moderately fragmented, featuring a mix of international grain handlers, large, branded food manufacturers, and specialized quinoa-focused companies. Major players such as Richardson International Limited, Avena Foods Limited, General Mills, Inc., and Nestlé SA leverage extensive sourcing networks and processing capabilities to incorporate quinoa into multi-category product portfolios, from breakfast cereals and snack bars to baby foods. Specialist firms like Andean Naturals Inc., NorQuin, and various seed companies focus on dedicated quinoa sourcing, milling, and distribution, often emphasizing organic, fair-trade, or region-specific varieties. Competitive strategies include vertical integration with Andean producers, investments in low-saponin and high-yield cultivars, expanded value-added offerings (flours, flakes, mixes), and direct-to-consumer e-commerce channels to capture premium health-conscious segments.

Key Industry Developments:

- February 2024, UK-based vegan dog food brand HOWND has introduced a new dry food in Pumpkin, Quinoa, and Moringa flavor, containing ingredients like sweet potato, cranberry, and Phytodroitin. The food is high in protein and low in fat and purines, providing a "digestive reset" for dogs with upset stomachs or allergies.

- March 2024, NIÚKE Foods has launched a range of plant-based condiments and milk alternatives, including quinoa milk and peanut milk. The NIÚKE Quinoa Milk is the first quinoa-based plant milk available in the US. The company also introduces two peanut-based milks, one plain and one combined with cacao using selenium-rich peanuts sourced from Argentina.

Companies Covered in Quinoa Market

- RICHARDSON INTERNATIONAL LIMITED

- Avena Foods Limited

- General Mills, Inc.

- Grain Millers

- Hancock seed company

- Andean Naturals Inc.

- Keen One Quinoa

- NorQuin

- Victory Seed Company

- Alter Eco

- Territorial Seed Company

- Adaptive Seeds spa

- Nestlé SA

- Blue Lake Milling

- Inca Organics

- Others

Frequently Asked Questions

The global quinoa market is projected to be valued at US$ 1.3 Bn in 2026.

Rising preference for chemical-free and environment-friendly agricultural practices is propelling market growth.

The global market is poised to witness a CAGR of 9.8% between 2026 and 2033.

Development and expansion of quinoa-based products provide a key opportunity for the market players.