- Non-food Packaging

- Polypropylene Woven Bag and Sack Market

Polypropylene Woven Bag and Sack Market Size, Share, and Growth Forecast, 2026 - 2033

Polypropylene Woven Bag and Sack Market by Bag Type (Laminated, Uncoated, Others), Product Type (Valve Bags, Gusseted Bags, Others), Application, and Regional Analysis for 2026 - 2033

Polypropylene Woven Bag and Sack Market Size and Trends Analysis

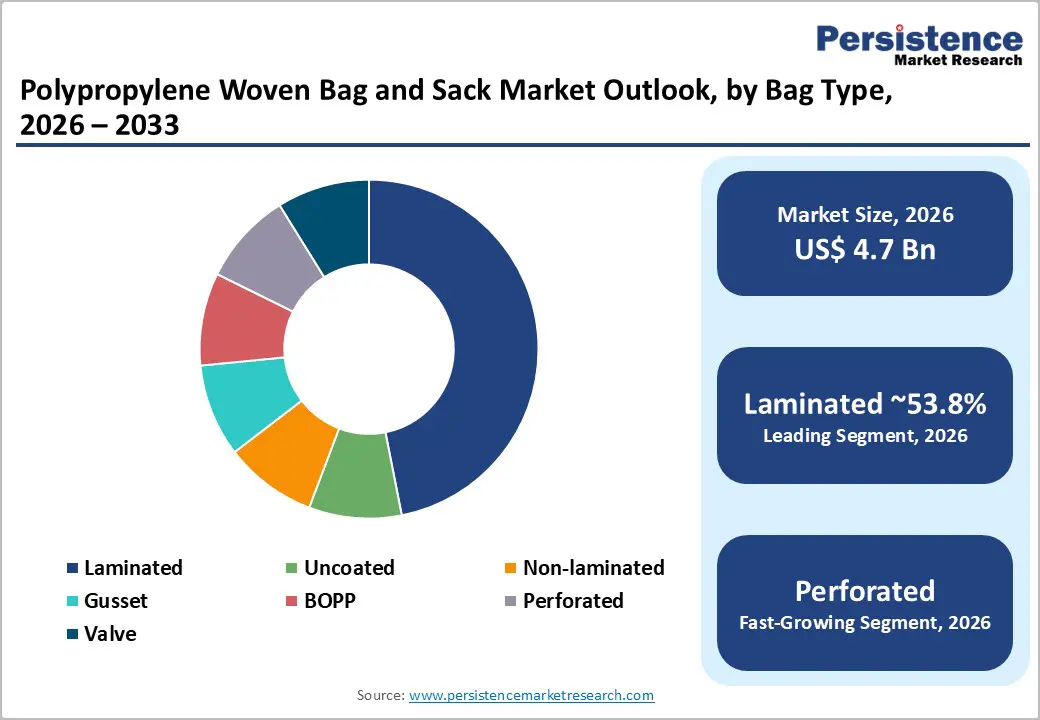

The global polypropylene woven bag and sack market size is likely to be valued at US$4.7 billion in 2026 and is expected to reach US$6.3 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033, driven by steady demand from agriculture, food distribution, and construction materials, along with increasing preference for durable, cost-effective bulk packaging solutions.

Product enhancements such as lamination, barrier liners, and the integration of recycled content are improving value realization. Although volatility in resin prices and rising regulatory compliance costs pose ongoing challenges, Asia-Pacific’s large-scale manufacturing base and expanding retail packaging requirements underpin long-term market stability and moderate growth.

Key Industry Highlights:

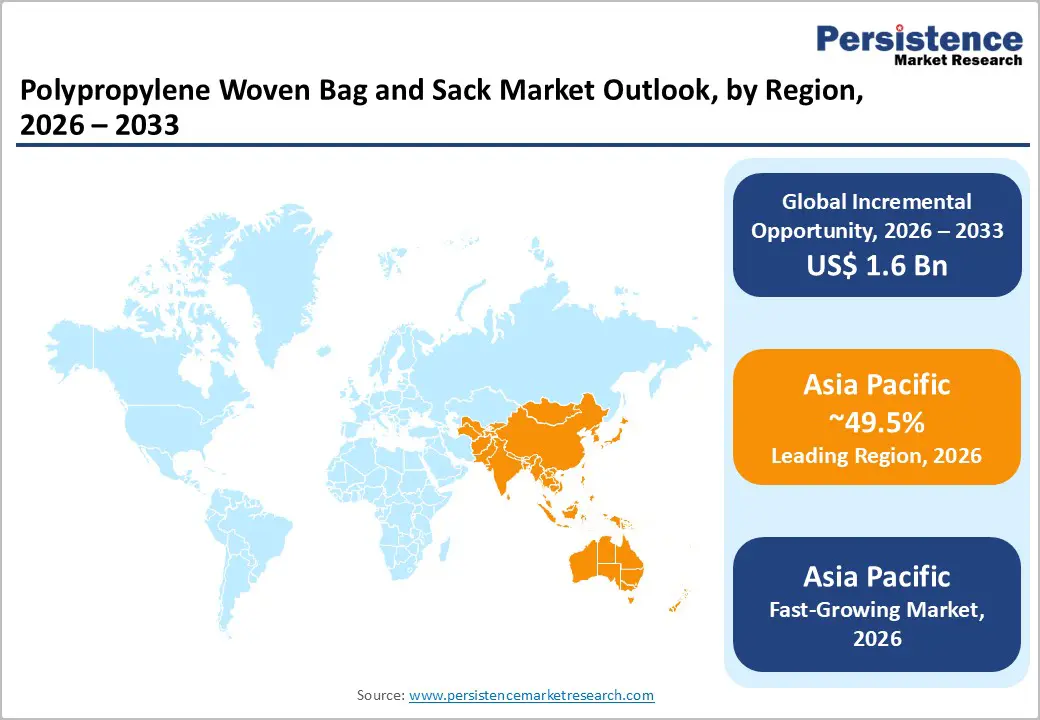

- Leading Region: Asia Pacific is projected to account for well over 49.5% of the market, driven by large-scale agricultural output, strong construction activity, and cost-efficient manufacturing hubs across China, India, and the ASEAN economies.

- Fastest-growing Region: Asia Pacific, supported by expanding fertilizer and grain packaging demand, infrastructure investments, and rising retail and e-commerce expansion.

- Investment Plans: Manufacturers are prioritizing lamination capacity expansion (≈approximately 10% incremental capacity in recent projects), integration of 10-20% post-consumer recycled (PCR) resin, automation of weaving and conversion lines, and adoption of digital printing and RFID-enabled packaging to support premiumization and supply-chain traceability.

- Dominant Bag Type: Laminated polypropylene woven bags is anticipated to hold approximately 53.8% of market share, due to superior moisture resistance, durability, and suitability for construction, food, and export packaging.

- Leading Application: Agriculture & allied is estimated to represent up to 41.3% of market share, underpinned by recurring demand for fertilizer, grain, sugar, and animal feed packaging across Asia Pacific, Africa, and emerging economies.

| Key Insights | Details |

|---|---|

| Polypropylene Woven Bag and Sack Market Size (2026E) | US$4.7 Bn |

| Market Value Forecast (2033F) | US$6.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Strong End-use Demand from Agriculture, Food, and Construction

Polypropylene (PP) woven bags and sacks remain essential for bulk transportation and storage of agricultural commodities, fertilizers, animal feed, sugar, grains, cement, sand, and chemical powders. Agriculture and allied applications collectively account for a significant share of total volume demand in multiple regional assessments, often representing one-third to nearly half of consumption depending on geography.

Fertilizer distribution programs and grain export flows require durable, tear-resistant packaging that can withstand mechanical handling and stacking. In parallel, the construction sector accounts for approximately 25-28% of total market demand, driven by cement and dry-mortar packaging requirements. Laminated woven sacks are particularly favored in cement packaging due to their moisture resistance and improved shelf life. These sectors represent recurring and high-volume consumption streams and provide a stable and predictable base for multi-year demand growth.

Technical Differentiation and Product Premiumization

Product innovation is reshaping the competitive landscape of the polypropylene woven bag and sack market. Manufacturers are increasingly differentiating their portfolios through advanced product configurations, including BOPP (Biaxially Oriented Polypropylene) lamination, integrated inner liners for food and chemical packaging, high-definition rotogravure printing, and recycled-content blends incorporating 10-20% post-consumer resin (PCR). These enhancements allow suppliers to address higher-margin use cases such as export packaging, branded food products, and retail-ready consumer sacks.

As a result, premium woven bag variants command average selling price (ASP) uplifts of 10-30% compared with standard non-laminated sacks. This transition from purely cost-based competition toward value-added differentiation is strengthening margin resilience and supporting sustainable profitability across the forecast period.

Asia Pacific Manufacturing Scale and Cost Efficiency

Asia Pacific is the largest global production and consumption hub for polypropylene woven bags and sacks, accounting for well over half of global supply and demand, according to aggregate estimates. The region benefits from established polymer-processing clusters, competitive labor costs, strong agricultural and construction demand, and export-oriented manufacturing ecosystems that collectively reinforce its cost leadership.

China and India function as the primary production bases, supplying both domestic consumption and international export markets. Meanwhile, ASEAN countries such as Vietnam and Thailand are rapidly expanding their export capabilities, particularly in agricultural and food-grade packaging. The regional concentration of raw material sourcing, weaving, lamination, and printing infrastructure enables lower production costs, faster lead times, and supply-chain efficiencies, reinforcing Asia Pacific’s dominance in global trade flows.

Barrier Analysis - Feedstock Price Volatility and Margin Pressure

Polypropylene resin is the primary raw material for woven sack manufacturing, and fluctuations in resin pricing directly affect production costs and profitability. Historical price swings of 15-25% in polypropylene markets have materially compressed converter EBITDA margins, particularly during periods when cost increases could not be fully passed through to customers.

Agricultural and commodity buyers remain highly price-sensitive, limiting manufacturers' pricing flexibility. Volatility in freight costs, import duties, and foreign exchange rates further intensifies cost uncertainty. Converters with integrated resin sourcing or geographically diversified production footprints demonstrate stronger margin resilience, while smaller regional players are more exposed to intermittent margin compression during raw-material price spikes.

Regulatory Compliance and Sustainability Pressures

Packaging sustainability regulations, including Extended Producer Responsibility (EPR) frameworks and recycling mandates, are increasing compliance obligations across developed markets. Several jurisdictions are tightening definitions of single-use plastics and incentivizing the adoption of recycled or bio-based materials, directly influencing procurement and production strategies.

To maintain market access, manufacturers must invest in recycled-content validation, material traceability systems, laboratory testing and certification, and lifecycle reporting. For smaller producers, these compliance-related investments can raise unit production costs by approximately 1-3%, reducing competitiveness in price-sensitive commodity segments. In premium food and export applications, however, regulatory compliance is increasingly becoming a baseline requirement rather than a discretionary value-add.

Opportunity Analysis - Premium Laminated and Food-Grade Packaging

The ongoing transition from basic woven sacks to laminated and hygienic packaging formats presents a clear revenue expansion opportunity. Laminated products already account for approximately 53.8% of bag-type segmentation, and demand for certified food-grade and moisture-resistant packaging continues to rise across export and retail channels.

If 10-15% of conventional agricultural sack volumes migrate to laminated, printed, or liner-integrated formats, the market could unlock incremental revenue of hundreds of millions of dollars over the forecast period. Manufacturers investing in advanced barrier lamination, moisture protection, and high-resolution printing are well-positioned to capture export-oriented and retail-facing demand growth.

Circularity and Recycled-Content Integration

The incorporation of post-consumer recycled (PCR) resin into polypropylene woven sacks represents a strategic growth avenue aligned with sustainability mandates and buyer procurement criteria. Retailers and multinational brands are increasingly specifying recycled-content thresholds of 10-30% in packaging contracts.

If 20% of global woven sack volumes transition to validated recycled-content formulations by 2030, suppliers could access a premium sub-market valued in the tens to low hundreds of millions of dollars, while strengthening regulatory compliance and brand positioning. Key investment priorities include chain-of-custody certification, material traceability systems, partnerships with recycling operators, and quality-control measures to preserve mechanical strength and performance.

Category-wise Analysis

Bag Type Insights

Laminated polypropylene woven bags are anticipated to account for approximately 53.8% of market share, making them the dominant segment in the global market. Their leadership is driven by superior durability, enhanced protection against moisture and contamination, and strong branding capabilities. These bags are extensively used in cement packaging, export grain shipments, animal feed distribution, and industrial powder applications, where product integrity during long-distance transport is critical. Lamination significantly improves tensile strength, puncture resistance, and stacking performance, reducing product loss during handling and storage.

In cement and construction materials, laminated sacks help prevent moisture ingress, which can compromise material quality, while in agricultural exports, they protect grains and pulses from humidity. The ability to support high-quality multicolor printing further enhances brand visibility for manufacturers and distributors, enabling higher price realization. As a result, laminated woven bags consistently command premium prices and maintain strong adoption across industrial and construction markets.

Perforated woven bags are among the fastest-growing bag-type formats. Perforated woven sacks are widely used for fresh produce such as onions, potatoes, and fruits, where controlled airflow reduces condensation and spoilage during transit and storage. This makes them particularly relevant for agricultural export supply chains and domestic wholesale distribution.

These bags improve filling efficiency, reduce dust emissions, and support consistent weight control, which is critical in large-scale industrial operations. Growth in mechanized packaging lines and rising export volumes are accelerating adoption, allowing these specialized formats to outpace traditional open-mouth woven sacks.

Application Insights

Agriculture and allied industries are anticipated to remain the largest application segment for polypropylene woven bags, accounting for up to approximately 41.3% of market share. Fertilizers, grains, sugar, seeds, and animal feed rely extensively on woven sacks for bulk handling, storage, and transportation owing to their strength, reusability, and cost-effectiveness. Recurring agricultural production cycles ensure stable baseline demand throughout the year, particularly in major producing regions such as Asia Pacific and Latin America.

In markets such as India and Southeast Asia, woven sacks remain the preferred packaging format for the distribution of fertilizer and grain through government procurement programs and cooperative supply chains. Their resistance to tearing and suitability for rough handling further reinforce their dominance in agricultural logistics.

Retail and shopping applications represent the fastest-growing end-use segment. The expansion of e-commerce grocery platforms, increased use of reusable shopping bags, and rising consumer preference for durable, multi-use packaging are key growth drivers. Retailers and brand owners are increasingly adopting laminated and BOPP-printed woven bags for in-store and last-mile delivery applications, particularly in emerging urban markets.

These bags offer superior load-bearing capacity, extended reuse potential, and stronger visual branding than conventional plastic carry bags. The segment benefits directly from premium printing, lamination, and customization capabilities, positioning it as a high-value growth area within the overall polypropylene woven bag and sack market.

Regional Insights

North America Polypropylene Woven Bag and Sack Market Trends - Premium, Traceable, and Automation-Ready Industrial Packaging

North America is a significant revenue contributor to the global polypropylene woven bag and sack market, driven by higher average selling prices and strong demand for certified, specialty, and value-added packaging solutions. The U.S. dominates regional consumption, driven by construction materials, specialty chemicals, pet food, animal feed, and premium food packaging applications.

Infrastructure modernization programs and commercial renovation cycles continue to support steady cement and dry-mix packaging demand. Growth in residential construction and infrastructure rehabilitation has sustained the consumption of valve-type woven sacks used in cement distribution. Companies operating in the U.S. market increasingly emphasize performance reliability, compatibility with automation systems, and traceability. For example, Berry Global has expanded its sustainable flexible packaging portfolio, including recycled-content solutions, reinforcing the shift toward circular materials in industrial and food applications. Such developments strengthen premium positioning and support margin stability. Regulatory focus on sustainability, including state-level recycling mandates and corporate ESG commitments, has accelerated the adoption of post-consumer recycled (PCR) resin integration in woven sacks. Large agricultural and pet food brands are increasingly requesting traceable recycled content, pushing converters to invest in certification systems and quality validation processes.

Manufacturers across the region are investing in digital printing technologies to enhance branding flexibility and reduce minimum order quantities. RFID-enabled packaging solutions are also being piloted for industrial supply chains to improve logistics tracking and anti-counterfeit protection. Automated weaving and conversion lines are improving productivity and labor efficiency, reinforcing cost competitiveness.

Europe Polypropylene Woven Bag and Sack Market Trends - Regulation-Driven Sustainability and High-Performance Woven Solutions

Europe shows balanced demand across the commodity and premium woven packaging segments, with Germany, France, the U.K., Spain, and Italy as major consumption centers. Industrial packaging for cement, chemicals, and agricultural exports remains steady, while premium laminated and food-grade sacks are gaining market share. Regulatory harmonization under European Union packaging directives, including Extended Producer Responsibility (EPR) schemes and ambitious recycling targets, has significantly influenced market dynamics. These policies are driving demand for recyclable mono-material woven sacks and increased recycled-content incorporation. Companies such as Mondi have invested in sustainable industrial packaging innovations, including recyclable and high-performance paper-plastic hybrid alternatives, which influence competitive positioning within the broader industrial packaging landscape.

European converters are upgrading lamination lines to improve barrier properties while ensuring compatibility with mechanical recycling systems. The expansion of rotogravure printing has enabled higher-quality branding for agricultural exports and specialty food products. In countries such as Germany and France, food safety compliance standards are particularly stringent, prompting suppliers to enhance inner liner development for flour, sugar, and specialty ingredients. Strategic partnerships between packaging manufacturers and recycling firms are becoming more common. These collaborations ensure a consistent rPP feedstock supply and facilitate compliance with EU traceability requirements.

Export-focused production facilities near key ports in Spain and the Netherlands have reduced turnaround times for agricultural shipments to Africa and the Middle East. While compliance requirements elevate entry barriers for smaller producers, they create opportunities for technologically advanced suppliers capable of meeting certification, testing, and sustainability criteria. As a result, Europe remains a premium-value market with a strong emphasis on quality and regulatory alignment.

Asia Pacific Polypropylene Woven Bag and Sack Market Trends - Scale-Led Production with Export-Focused Premiumization

Asia-Pacific is the dominant regional market, accounting for 49.5% of the market. The region’s leadership stems from large-scale agricultural output, strong construction demand, cost-efficient manufacturing ecosystems, and dense polymer processing clusters. China represents the largest single producer and consumer, supported by robust cement production, chemical manufacturing, and agricultural packaging requirements. The country’s extensive base of woven sack manufacturing supports both domestic supply and export distribution. Chinese manufacturers have expanded laminated sack capacity to support export markets requiring higher barrier performance, strengthening the region’s influence in global trade flows.

India is another major hub, particularly in fertilizer and grain packaging. Government-supported fertilizer distribution programs and large agricultural procurement systems sustain recurring demand for woven sacks. Companies such as Uflex and Emmbi Industries have expanded value-added capabilities, including laminated and liner-integrated woven bags, positioning India as a competitive exporter to Africa and the Middle East. Growth in organized retail and e-commerce platforms is further accelerating demand for printed and branded small-format woven sacks. Manufacturers throughout Asia Pacific continue to expand lamination, BOPP coating, and high-definition printing capabilities to serve export markets in Europe, the Middle East, and Africa.

Integration across resin sourcing, weaving, printing, and finishing operations enables lower production costs and improved supply chain efficiency, reinforcing the region’s structural dominance. As sustainability awareness gradually increases across advanced Asian economies, larger converters are also piloting recycled-content woven sacks to maintain export competitiveness. This combination of scale, cost efficiency, and incremental premiumization ensures that Asia Pacific remains both the leading and fastest-growing regional market over the forecast period.

Competitive Landscape

The global polypropylene woven bag and sack market exhibits moderate fragmentation, characterized by the coexistence of large multinational packaging converters and a wide base of regional and local manufacturers. Competitive advantage in the current market environment is driven by stable resin sourcing, advanced lamination and high-definition printing capabilities, reliable delivery performance, and the ability to comply with evolving sustainability and regulatory requirements. Suppliers that combine these attributes are better positioned to secure long-term contracts with large agricultural, industrial, and retail buyers.

Leading players in the polypropylene woven bag and sack market are increasingly prioritizing product differentiation through lamination, liner integration, and functional enhancements. Sustainability initiatives, including recycled-content adoption and traceability systems, are becoming core strategic pillars rather than optional features. Geographic expansion within Asia Pacific remains a key growth lever, supported by manufacturing scale advantages, while digitalization and supply-chain integration enhance responsiveness and customer retention. Vertical collaboration with resin suppliers and recycling partners is also gaining momentum, strengthening material security and regulatory alignment across the value chain.

Key Industry Developments:

- In June 2025, Uflex Ltd. announced a strategic partnership with LC Packaging to co-develop and commercialize mono-material, recyclable woven PP bag solutions for food and agricultural applications, advancing the adoption of fully recyclable packaging formats.

Companies Covered in Polypropylene Woven Bag and Sack Market

- Mondi plc

- Berry Global Inc.

- LC Packaging International BV

- Uflex Ltd.

- Emmbi Industries Ltd.

- Muscat Polymers Pvt. Ltd.

- Rishi FIBC Solutions Pvt. Ltd.

- Shri Jagdamba Polymers Ltd.

- STP Group

- Gopinath Polyplast Pvt. Ltd.

- Al-Tawfiq Company

- Hanoi Plastic Bag JSC

- Bangkok Sacks Co., Ltd.

- United Bags, Inc.

- Bag Corp

- Polyweave Packaging Inc.

- Tianjin Brilliant Import & Export Co., Ltd.

- Green Bag Co. Ltd.

Frequently Asked Questions

The global polypropylene woven bag and sack market size is valued at US$4.7 billion in 2026.

By 2033, the polypropylene woven bag and sack market is expected to reach US$6.3 billion.

Key trends include product premiumization through lamination and BOPP coating, growing adoption of food-grade liners and hygienic packaging, increasing use of 10-20% recycled-content formulations, and rising demand for printed, retail-ready woven sacks driven by e-commerce and branded goods.

By bag type, laminated polypropylene woven bags lead the market, accounting for approximately 53.8% of market share, due to superior moisture resistance, durability, and print quality.

The polypropylene woven bag and sack market is projected to grow at a CAGR of 4.2% between 2026 and 2033.

Major players with strong and diversified portfolios include Mondi plc, Berry Global Inc., LC Packaging, Uflex Ltd., and Emmbi Industries.