- Medical Devices

- Plastic Wound Retractor Market

Plastic Wound Retractor Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Plastic Wound Retractor Market by Product Type (Ring-Based, Prong-Based), Application (Abdominal Surgery, Cardiac Surgery, Spinal Surgery, Plastic Surgery, Dental Surgery, Brain Surgery, Thyroid Surgery, Others), Surgery Type (Minimally Invasive Surgery, Open Surgery), End-user (Hospitals, Ambulatory Surgical Centers), and Regional Analysis from 2026 - 2033

Plastic Wound Care Retractor Market Share and Trends Analysis

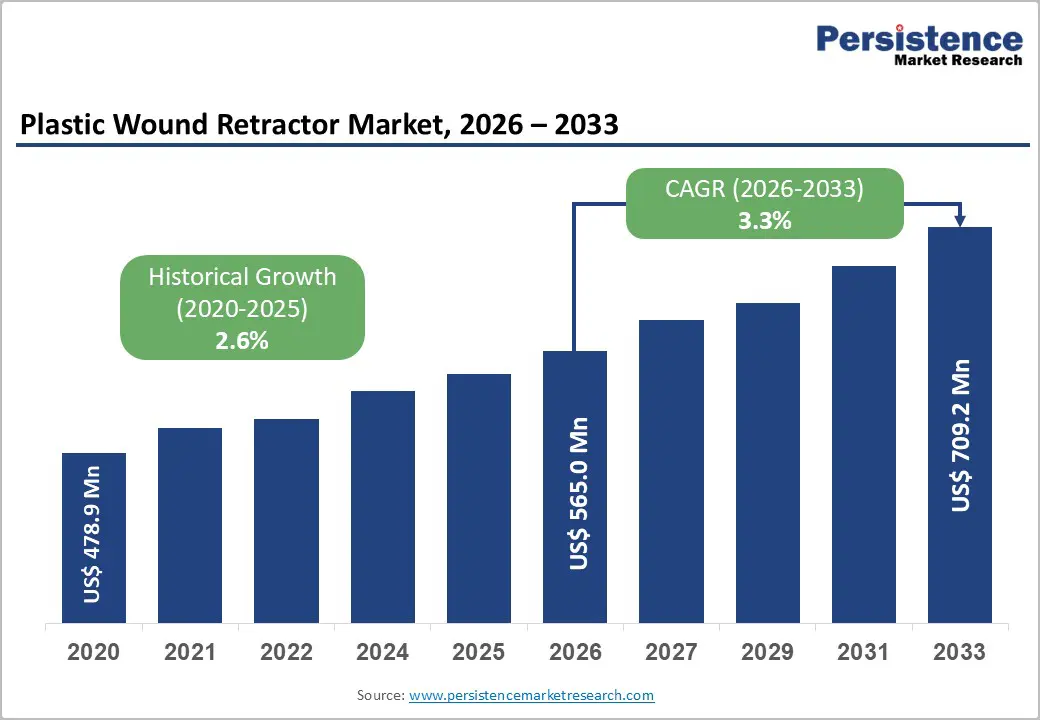

The global plastic wound retractor market is estimated to grow from US$ 565.0 million in 2026 to US$ 709.2 million by 2033. The market is projected to grow at a CAGR of 3.3% from 2026 to 2033.

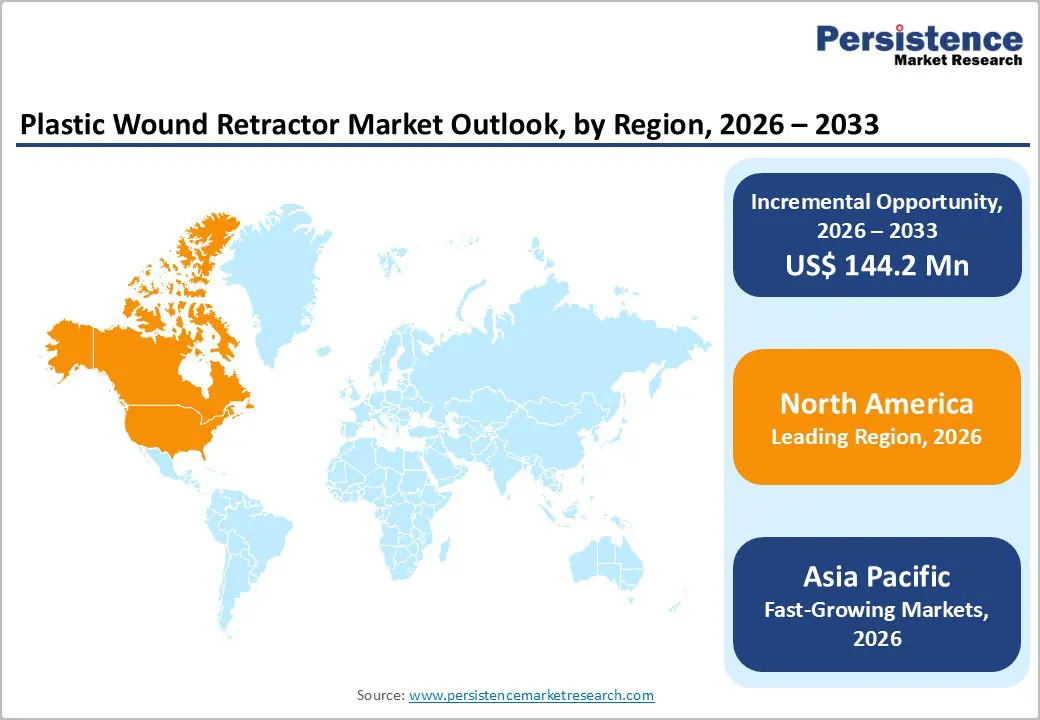

The plastic wound retractor industry is growing steadily, fueled by rising surgical volumes, increased minimally invasive procedures, and hospital infrastructure upgrades. North America leads due to advanced healthcare systems and high adoption of innovative surgical tools. Asia-Pacific is the fastest-growing region, driven by expanding healthcare facilities, higher procedure volumes, and rising investment in surgical infrastructure.

Key Industry Highlights

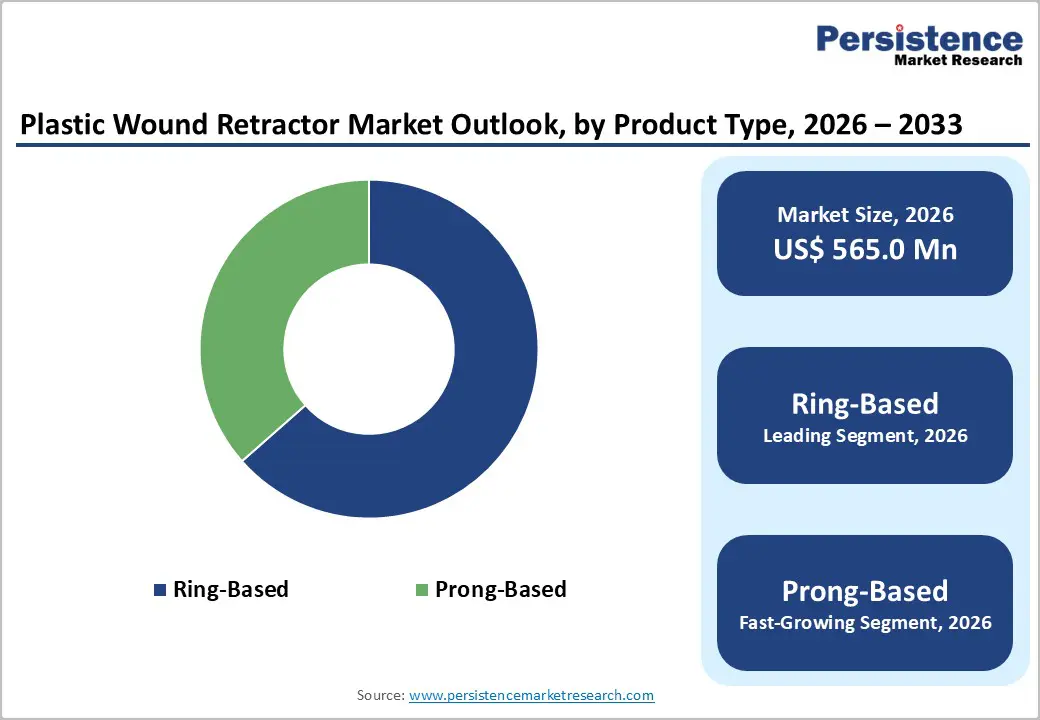

- Dominant Segment: Ring-based plastic wound retractors lead with 63.5% share in 2025, due to ease of use, stability, and broad surgical applicability. Prong-based retractors are the fastest-growing segment, driven by demand for precision, better tissue exposure, and adaptability across minimally invasive and complex procedures.

- Dominant Region: North America holds the largest share, around 38.9% in 2025, supported by advanced hospitals, high surgical volumes, and strong adoption of innovative surgical tools. Europe follows closely, while Asia-Pacific is the fastest-growing region due to rapid hospital expansion, rising procedure volumes, and healthcare investments.

- Market Drivers: Growth is fueled by increasing surgical procedures, rising minimally invasive surgeries, hospital modernization, demand for efficient operating room setups, and replacement of conventional retractors.

- Market Opportunity: Key opportunities include the adoption of disposable and smart retractors, growth in emerging markets, expansion of ambulatory surgical centers, integration with digital OR systems, and development of specialty retractors for complex surgeries.

| Key Insights | Details |

|---|---|

|

Plastic Wound Retractor Market Size (2026E) |

US$ 565.0 Mn |

|

Market Value Forecast (2033F) |

US$ 709.2 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

3.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.6% |

Market Dynamics

Driver - Rising volume of surgical procedures globally, especially elective and emergency surgeries

The global volume of surgical procedures is substantial and growing, providing a foundational driver for the plastic wound retractor market. Over 300 million major surgical operations are performed each year globally, involving incision, excision, manipulation, or suturing of tissue in an operating theatre under anesthesia. This reflects a significant increase from earlier estimates of approximately 234 million surgeries annually, indicating rising demand for surgical access and support tools. Such high absolute volumes underscore the consistent need for surgical devices that facilitate wound management and operative exposure, directly supporting demand for plastic wound retractors across diverse surgical specialties.

Increasing surgical volumes are not limited to emergency cases; elective procedures are also rising as populations age and access to medical care improves. In Australia and Europe, orthopaedic elective surgeries such as hip and knee replacements have risen markedly, with nearly 1 million hip and 680,000 knee replacements in EU countries in 2022, driven by demographic change and chronic musculoskeletal conditions. In India alone, an estimated 30 million surgeries are performed annually, with modeling studies suggesting that nearly 3,646 surgeries per 100,000 population are required to meet the national need. This growth in both emergency and elective surgeries expands the total addressable market for surgical consumables such as plastic wound retractors, reinforcing its steady expansion.

Restraints - High cost of advanced plastic wound retractors and surgical devices

The high cost of advanced surgical devices represents a significant restraint on the adoption of plastic wound retractors, particularly in resource-constrained healthcare systems. Hospitals across the United States reported that medical and surgical supply costs totaled more than $57 billion in 2023, highlighting that surgical instruments and devices consume a large portion of hospital budgets. These costs have risen steadily from $30.2 billion in 2017, reflecting a sustained increase in pricing pressures on surgical supplies. High upfront expenses for innovative and disposable surgical tools can limit hospitals’ ability to invest in newer wound retractors, slowing market growth and adoption in both developed and developing regions.

Cost considerations are particularly acute in lower-income settings or smaller facilities, where capital for advanced equipment is limited. For example, while basic surgical wound retractors may be purchased at low per-unit rates, disposable and specialized versions that offer ergonomic design, infection control benefits, or improved visibility often cost substantially more. Budget constraints can lead facilities to prioritize essential services and general supplies, deferring investment in higher-priced devices. The combination of rising material costs, regulatory compliance expenses, and overall supply chain inflation is driving higher prices for advanced surgical instruments, further restraining the pace of adoption of premium plastic wound retractors worldwide.

Opportunity - Development of advanced materials (e.g., biodegradable or enhanced polymers) to improve performance and sustainability

The emergence of advanced biodegradable and enhanced polymer materials offers a compelling opportunity for the plastic wound retractor market by enabling devices that combine high performance with improved environmental sustainability. Biodegradable polymers such as polylactic acid (PLA), polyglycolic acid (PGA), PLGA, and polycaprolactone (PCL) are widely used in medical applications because they safely break down into non-toxic components after use. These materials are already employed in absorbable sutures, orthopedic implants, and drug delivery systems, demonstrating their reliability and biocompatibility in clinical settings. Adopting such materials for wound retractors can reduce medical waste and provide eco-friendly alternatives to conventional plastics in surgical consumables.

From a sustainability perspective, the broader healthcare sector is increasingly prioritizing environmentally responsible materials. Production of biodegradable plastics reached an estimated 2.22 million tons in 2022, with about 51% of that volume classified as biodegradable, illustrating a substantial and growing industrial capacity for these eco-friendly polymers. This trend reflects a shift toward materials that offer both clinical functionality and reduced long-term environmental impact, aligning with global sustainability goals and healthcare waste reduction efforts. Wound retractors manufactured from advanced biodegradable polymers can appeal to hospitals and surgical centers seeking to minimize their ecological footprint without compromising device performance, thereby expanding market opportunities.

Category-wise Analysis

By Product Type, Ring-Based Dominates the Plastic Wound Retractor Market

Ring-Based product type occupies 63.5% share of the global market in 2025, due to its ability to provide uniform, 360° retraction, ensuring better visibility and access to the surgical site compared with prong-based designs. Their flexible inner and outer rings can be deployed through small incisions and expanded to maintain consistent tension, reducing tissue trauma and enhancing operative efficiency. They are widely used in both open and minimally invasive surgeries, particularly abdominal procedures, where workflow efficiency and patient safety are critical. Single-use, sterile ring-based retractors also minimize infection risk and eliminate sterilization logistics, making them highly preferred in high-volume hospitals. Clinical studies indicate reduced surgical site infections and improved outcomes, further driving adoption.

By Application, Abdominal Surgery is gaining traction due to high procedure volumes, requiring effective exposure and wound protection

Abdominal surgery dominates the plastic wound retractor market because these procedures are among the most commonly performed worldwide, requiring reliable wound exposure and protection. High-volume surgeries such as cholecystectomies, with around 600,000 procedures annually in the U.S., and hernia repairs, totaling approximately 20 million operations globally each year, highlight the substantial clinical need for effective retractors. Abdominal surgeries include both emergency procedures like appendectomies and elective interventions, increasing overall demand. With over 300 million surgeries performed each year globally, a significant proportion involves abdominal procedures, making wound management critical. The consistent requirement for visibility, access, and tissue protection during these operations reinforces the preference for plastic wound retractors, establishing abdominal surgery as the leading application segment in the market.

Regional Insights

North America Plastic Wound Retractor Market Trends

North America dominates the plastic wound retractor market with a 38.9% share in 2025, driven by high surgical procedure volumes, advanced healthcare infrastructure, and strong adoption of modern surgical technologies. In the United States alone, nearly 50 million inpatient surgeries were performed annually prior to 2020, with millions more outpatient procedures requiring surgical access tools. The U.S. also spends over $1.4 trillion annually on hospital care, reflecting robust investment in medical technologies and supplies that improve surgical outcomes and efficiency. Canada and Mexico similarly maintain extensive surgical services supported by public and private health systems. High rates of minimally invasive procedures, strong hospital accreditation standards, and emphasis on infection control further encourage the use of single-use, advanced wound retractors. These factors combine to make North America the largest regional market for these devices.

Europe Plastic Wound Retractor Market Trends

Europe is a key region in the plastic wound retractor market due to its well-established healthcare infrastructure, high surgical procedure volumes, and strong investment in medical technology. In 2024, over 63 million surgeries were performed across European countries, including general, minimally invasive, and specialty procedures, all of which require effective wound access and protection. Healthcare systems in Europe spend, on average, around 10% of GDP on health services, with a significant portion directed toward medical devices and surgical equipment. Countries such as Germany, France, and the United Kingdom lead in procuring advanced surgical tools, upgrading operating rooms, and adopting innovative technologies. This combination of high demand, infrastructure, and investment makes Europe an important market for plastic wound retractors.

Asia-Pacific Plastic Wound Retractor Market Trends

Asia-Pacific is the fastest-growing region in the plastic wound retractor market, driven by the rapid expansion of healthcare infrastructure, rising surgical volumes, and the growing adoption of advanced surgical techniques. Countries like China, India, Japan, and Southeast Asian nations are investing heavily in modern hospitals, new operating rooms, and specialized surgical centers to meet rising demand from aging populations and the prevalence of chronic diseases. Minimally invasive and complex surgeries are becoming more common, creating a higher demand for devices that ensure safe and efficient wound management. Additionally, increasing medical tourism in the region and government initiatives to improve healthcare accessibility contribute to faster adoption of innovative surgical tools, positioning the Asia-Pacific region as a leading growth region for plastic wound retractors.

Market Competitive Landscape

Leading companies in the plastic wound retractor market focus on innovative, ergonomic, and safe solutions, investing in advanced materials, improved design, and digital integration. R&D emphasizes durability, ease of use, and cost-effectiveness, while collaborations with hospitals and surgical centers support broader adoption, thereby enhancing surgical efficiency, patient safety, and operating room workflow worldwide.

Key Industry Developments:

- In August 2024, CooperCompanies acquired obp Surgical, expanding CooperSurgical’s portfolio of leading medical devices. The acquisition strengthened CooperSurgical’s offerings across various surgical and procedural areas, enhancing its ability to provide innovative medical solutions.

Companies Covered in Plastic Wound Retractor Market

- Applied Medical Resources Corp

- Betatech Medical

- Changzhou Ankang Medical Instruments Co Ltd

- Geister Medizintechnik GmbH

- HAKKO CO., LTD.

- Cooper Surgical

- Wecan Medicare

- Victor Medical Instruments Co., Ltd.

- Vaxcon Corporation

- PRESCIENT SURGICAL, INC

- SEJONG MEDICAL CO., LTD.

- SURKON MEDICAL CO., LTD

- Surgicore Co. Ltd.

- Swemac Innovation AB

- 3M Company

- Medtronic, Inc.

- Ethicon US, LLC

- Grena Limited

- MetroMed Healthcare Co. Ltd

- LOCAMED LIMITED

- Others

Frequently Asked Questions

The global plastic wound retractor market is projected to be valued at US$ 565.0 Mn in 2026.

Rising surgical volumes, minimally invasive procedures, hospital modernization, and demand for efficient, safe wound management drive growth.

The global plastic wound retractor market is poised to witness a CAGR of 3.3% between 2026 and 2033.

Adoption of advanced materials, disposable retractors, digital integration, emerging markets, and specialty surgical applications offer opportunities.

Applied Medical Resources Corp, Betatech Medical, Changzhou Ankang Medical Instruments Co Ltd, Geister Medizintechnik GmbH, HAKKO CO., LTD., Cooper Surgical.