- Non-food Packaging

- Pallet Wraps Market

Pallet Wraps Market Size, Share, and Growth Forecast, 2025 - 2032

Pallet Wraps Market by Material Type (Linear Low-Density Polyethylene (LLDPE), Low-Density Polyethylene (LDPE), High-Density Polyethylene (HDPE), Miscellaneous), Product Type (Stretch Films / Wraps, Shrink Films / Wraps), Industry (Food & Beverage, Pharmaceuticals & Healthcare, Automotive & Manufacturing, Consumer Goods, Others) and Regional Analysis for 2025 - 2032

Pallet Wraps Market Size and Trends Analysis

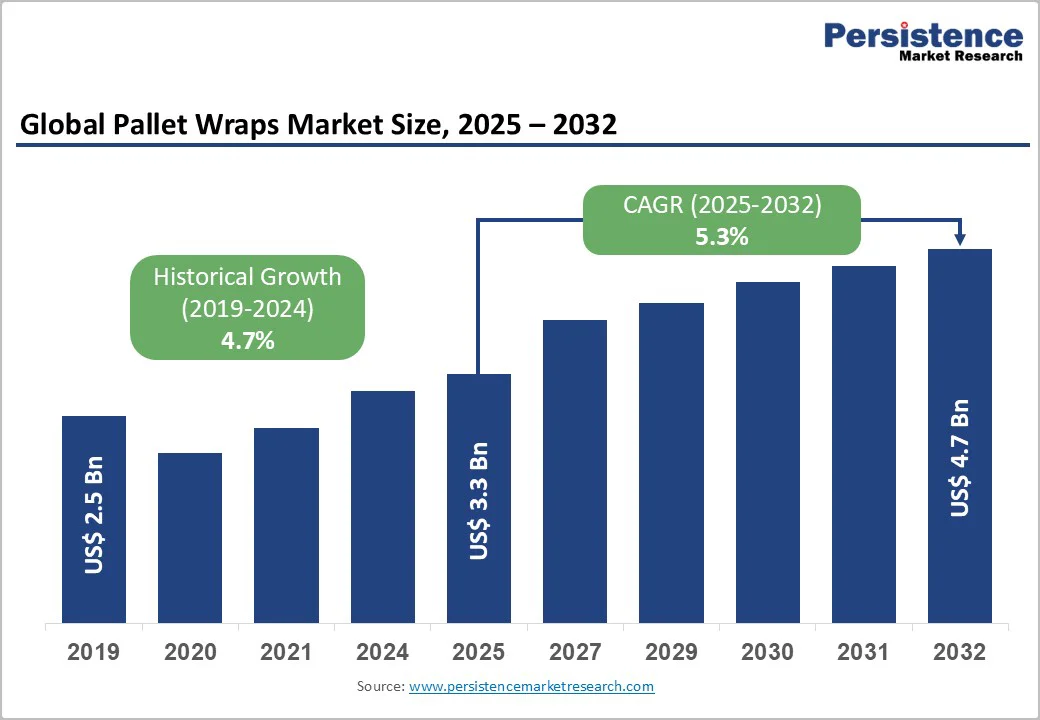

The global pallet wraps market size is valued at US$ 3.3 billion in 2025 and is projected to reach US$ 4.7 billion, growing at a CAGR of 5.3% between 2025 and 2032.

The market reflects substantial structural shifts driven by supply chain modernization, accelerating adoption of automated warehouse systems, and intensifying demand across multiple industrial sectors. The pallet wraps market is anchored in the logistics and manufacturing sectors, where load security, product protection, and operational efficiency form the foundation of competitive advantage.

Key Industry Highlights:

- Stretch films dominate the market with ~68.9% share in 2025, driven by automated warehousing adoption and superior load-containment performance.

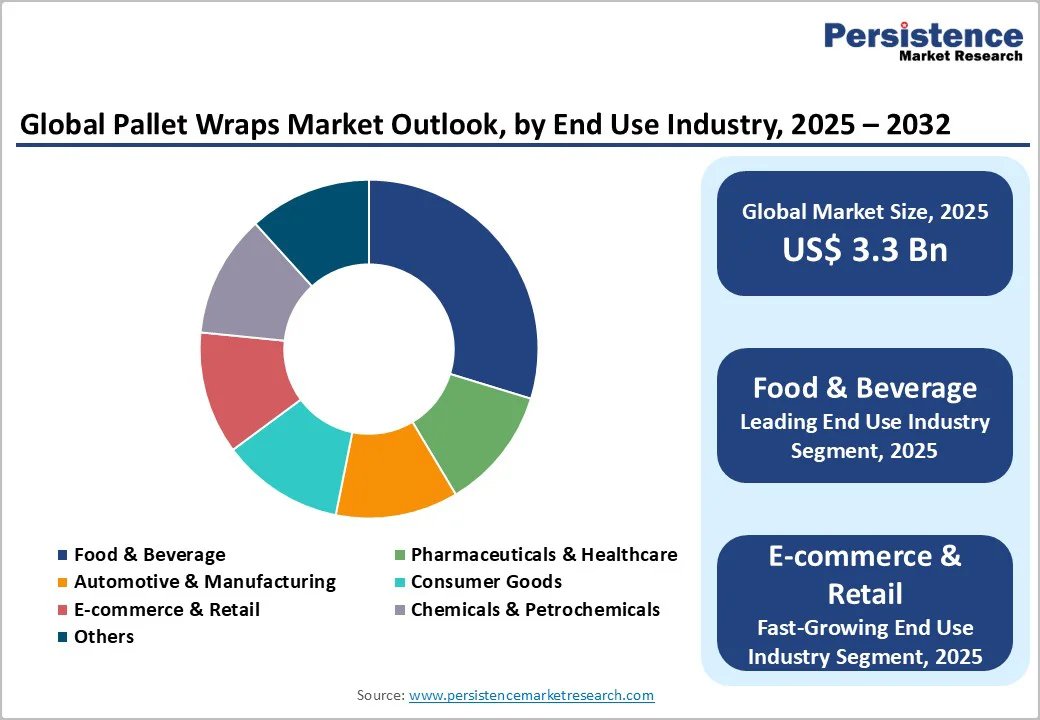

- Food & beverage is the leading end-use segment with ~32.3% market share, supported by stringent hygiene, cold-chain logistics, and rising global food exports.

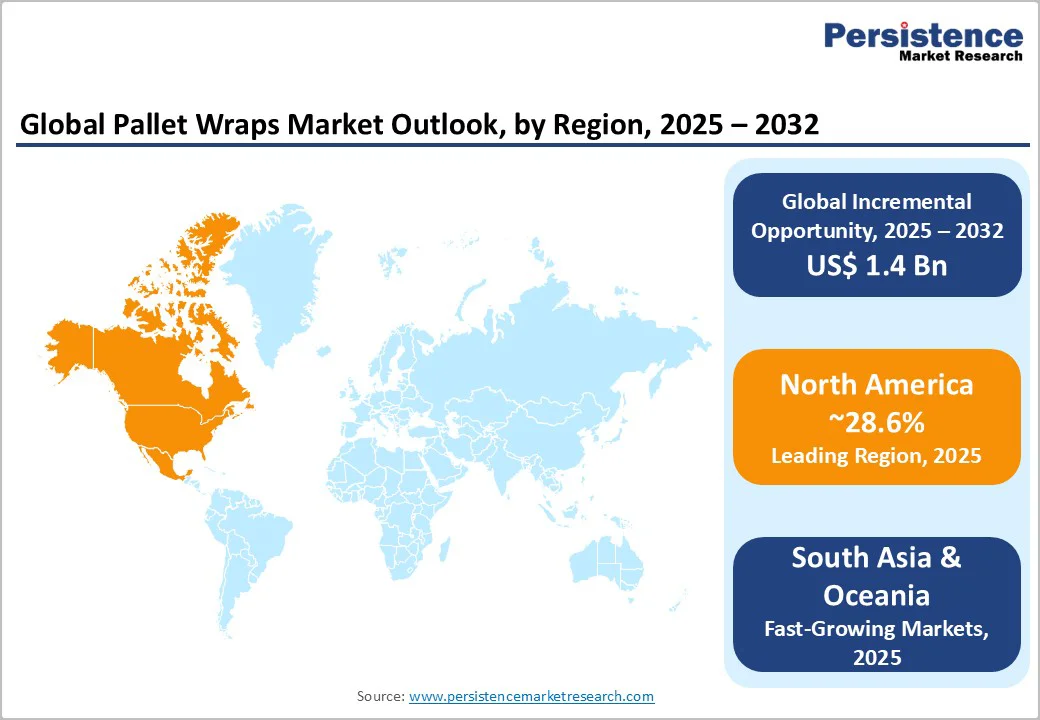

- North America remains the most mature regional market, characterised by high automation levels, advanced machine-grade films, and strong compliance-driven demand.

- East Asia emerges as the fastest-growing region, propelled by massive e-commerce parcel volume, manufacturing scale, and logistics infrastructure modernisation.

- Shrink films represent the fastest-growing product type, supported by demand for tamper-evident, aesthetic, and high-clarity specialty packaging.

- Pharmaceuticals & healthcare is the fastest-growing application segment, fuelled by expanding cold-chain distribution and stringent sterility requirements.

- Europe leads in sustainability-led demand, driven by strict recyclability regulations, circular economy mandates, and rapid adoption of recycled-content pallet wraps.

| Key Insights | Details |

|---|---|

| Pallet Wraps Market Size (2025E) | US$3.3 Bn |

| Market Value Forecast (2032F) | US$4.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Dynamics

Drivers - E-Commerce Expansion and Omnichannel Distribution Requirements

E-commerce fulfilment operations have fundamentally transformed warehouse and logistics infrastructure globally. The expansion of direct-to-consumer distribution channels and the rapid deployment of regional fulfilment centres have created extraordinary demand for protective packaging materials that secure goods during last-mile delivery.

E-commerce platforms report handling 270 million online shoppers in India alone during 2024, with projections reaching 300 million by 2030. This volume trajectory translates directly into demand for pallet wraps, as distribution centres must process exponentially higher shipment volumes with consistent quality standards.

The pallet wraps market demonstrates direct correlation with e-commerce fulfilment expansion, as each order passing through distribution networks requires protective wrapping solutions.

Cross-border e-commerce volumes, particularly from China, at USD 331 billion in 2023, necessitate robust protective packaging ensuring product integrity across extended supply chains. The food and beverage sector, which accounts for approximately 33% of pallet wrap demand in 2025, has experienced growth through e-commerce channels, requiring specialised stretch film solutions that maintain product freshness during temperature-controlled transit.

Regulatory compliance requirements for food transportation, including sanitary standards and contamination prevention, mandate the utilisation of approved packaging materials, directly driving the adoption of high-performance pallet wraps within distribution operations.

Sustainability Requirements and Circular Economy Integration

Environmental regulations and corporate sustainability commitments have elevated material selection criteria throughout supply chains. Regulatory frameworks increasingly mandate recyclable or biodegradable packaging materials, with several markets implementing mandatory recycled content requirements.

India's April 2025 regulation requiring 30% recycled PET content in beverage bottles exemplifies this regulatory shift, influencing packaging material selection throughout downstream industries. The Pallet Wraps Market faces evolving material composition requirements, driving innovation in HDPE and LLDPE formulations incorporating post-consumer recycled content without sacrificing performance characteristics.

Sustainability certifications and transparency in material sourcing have become competitive differentiators, with major enterprises requiring suppliers to demonstrate reduced carbon footprints and circular economy alignment.

Biodegradable and compostable stretch film options are emerging as premium product categories, attracting buyers in highly regulated markets. Recycling infrastructure development, while still nascent in several geographies, creates long-term demand sustainability through increased material recirculation, extending material lifecycles and reducing virgin material requirements.

Companies investing in advanced recycling technologies and bio-based film formulations position themselves advantageously in markets implementing stringent environmental compliance frameworks.

Restraint - Volatile Raw Material Costs and Supply Chain Vulnerability

Polyethylene and other polymer feedstock pricing exhibits significant volatility driven by crude oil price fluctuations, geopolitical supply disruptions, and feedstock availability constraints. Producer costs for LLDPE, LDPE, and HDPE fluctuate substantially based on crude oil benchmarks, creating pricing pressure on manufacturers unable to pass incremental costs to price-sensitive customers.

Raw material cost spikes directly compress profit margins for pallet wrap manufacturers, particularly for commodity-grade products competing on price. Supply disruptions from major polymer-producing regions generate material shortages and delivery delays, disrupting production schedules and fulfilment commitments.

Manufacturers operating with limited inventory buffers experience acute vulnerability to supply volatility, constraining production flexibility during demand surges. This uncertainty complicates forward pricing and long-term customer contract negotiations, particularly for price-competitive applications in commodity logistics segments.

Opportunity - Adoption of Smart Packing Technologies and IoT-Enabled Load Tracking

Integration of Internet of Things (IoT), artificial intelligence, and blockchain technologies into pallet wrapping operations represents a high-growth opportunity for the Pallet Wraps Market. Real-time tracking capabilities, temperature monitoring, and authenticity verification systems enhance supply chain transparency and reduce product loss from theft or damage.

Companies implementing AI-powered demand forecasting and predictive maintenance systems improve wrapping equipment utilisation rates and reduce unplanned downtime, creating measurable efficiency gains justifying continued investment in advanced solutions.

The convergence of physical pallet wraps with digital tracking infrastructure enables unprecedented supply chain visibility.

Organisations implementing RFID-enabled pallet systems report significant improvements in inventory accuracy and reduced loss rates, thereby justifying premium pricing for wrapping films incorporating smart technologies.

Emerging startups and established logistics providers across Asia Pacific are deploying telematics-based platforms and cloud-based supply chain systems that fundamentally depend on standardised pallet wrapping specifications and compatible film materials.

These technology adoption trajectories create pathways for pallet wraps market participants to develop value-added solutions incorporating connectivity, data collection, and intelligence capabilities. Companies developing films compatible with optical scanning systems and RFID tag embedding create differentiation opportunities and capture premium market segments.

Expansion of Bio-Based, Biodegradable, and Circular Economy Solutions

Sustainability-driven market opportunities within the Pallet Wraps Market are expanding as circular economy principles gain institutional traction and regulatory mandates evolve. Bio-based and biodegradable polymer materials represent innovative alternatives to conventional polyethylene-based wraps, aligning with corporate sustainability commitments and regulatory requirements for reduced environmental impact.

Agricultural applications, organic waste packaging, and compostable material development create opportunities for high-value pallet wrap solutions meeting stringent environmental specifications.

Emerging chemical and biological methods enabling "upcycling" of heterogeneous plastic waste into higher-quality materials support closed-loop packaging systems and reduce dependence on virgin polyethylene production. Companies investing in bio-based film development capitalise on growing consumer preferences and regulatory incentives favouring sustainable packaging.

Category-wise Analysis

Paper Type Insights

Stretch films and wraps represent the dominant product type within the Pallet Wraps Market, commanding approximately 68.9% of total market share in 2025. Stretch wrapping technology's compatibility with automated dispensing systems, superior load containment efficiency, and cost-effectiveness relative to alternative wrapping methodologies establish its preferred status across warehousing and logistics infrastructure globally.

The material's ability to conform precisely to pallet load geometry while maintaining consistent tension distribution prevents load shifting and damage throughout multi-modal transportation scenarios.

Industry Insights

The food and beverage industries represent the dominant application segment for pallet wraps, commanding approximately 32.3% of total market share in 2025. The sector's substantial demand derives from critical requirements for moisture protection, contamination prevention, and product preservation throughout global supply chains extending from manufacturing facilities through retailer distribution networks.

Packaged food exports, frozen product logistics, and beverage distribution networks depend fundamentally on reliable pallet wrapping specifications to maintain product quality and extend shelf life throughout extended transit durations.

The European food and drink industry, representing the continent's largest manufacturing sector with €1.2 trillion in annual turnover and employment of approximately 4.7 million people, generates continuous demand for high-performance protective packaging solutions.

Growth in international food trade, with the EU maintaining €182 billion in annual exports beyond the region, creates sustained demand for reliable containment systems throughout complex cross-border logistics networks.

Regional Insights and Trends

North America Pallet Wraps Market Trends

North America represents a mature, highly sophisticated pallet wraps market characterised by advanced warehouse automation adoption, stringent regulatory compliance requirements, and premium pricing for high-performance solutions.

The region's logistics infrastructure supports comprehensive integration of automated wrapping systems, with warehouse automation adoption projected to reach a 99% reduction in operational errors and 50% increase in storage capacity through deployed robotic systems.

The U.S. flexible packaging industry alone generated $41.5 billion in sales in 2022, representing 21% of the country's $180.3 billion packaging market, demonstrating substantial scale and sophistication.

North American manufacturers prioritise machine-grade films optimised for automated dispensing systems and equipped with data-enabled wrapping technology, facilitating predictive maintenance and downtime reduction.

East Asia Pallet Wraps Market Trend

East Asia represents the fastest-expanding regional market for pallet wraps, driven by manufacturing scale-up, intra-regional trade expansion, and logistics infrastructure modernisation across China, India, Japan, and Southeast Asian economies.

China dominates regional logistics activity, with annual domestic parcels exceeding 130 billion units delivered in 2024, representing 10.3% annual growth and reflecting e-commerce expansion supporting pallet wrapping demand. Manufacturing concentration in production hubs throughout East Asia creates standardised demand for automated wrapping systems optimised for high-throughput production environments and complex supply chains.

Japan's advanced logistics technology and precision-based supply chain practices position the region as a technology leader within East Asia, with sophisticated e-commerce platforms including Rakuten and Amazon Japan driving warehouse automation adoption and premium product specification demand.

Europe Pallet Wraps Market Trend

Europe represents a mature, highly regulated market for pallet wraps emphasising sustainability, circular economy principles, and compliance with evolving packaging regulations. The European food and drink industry, the continent's largest manufacturing sector, generated €280.7 billion in value added in 2022, representing 37.8% growth from 2021 levels and demonstrating sector resilience and continued demand for protective packaging solutions.

European manufacturers prioritise closed-loop recovery systems and carbon footprint transparency, with regulatory frameworks mandating recyclable content requirements and microplastics elimination, creating competitive differentiation opportunities for sustainable product specifications.

The European Commission data demonstrates healthcare sector maturity, with 2022 healthcare expenditures ranging from €176 billion in Italy to €489 billion in Germany, supporting sophisticated pharmaceutical logistics requirements and premium pallet wrapping specifications.

Energy-efficient wrapping tunnel retrofits and technology partnerships supporting standardised test protocols advance operational efficiency and material performance optimisation across the region.

Competitive Landscape

The global pallet wrap market is moderately consolidated, with a handful of large players controlling a significant portion of the market while a long tail of regional suppliers competes on price and niche applications.

Key players include Berry Global, Sigma Plastics Group, Inteplast Group, AEP Industries, and Coveris. These companies lead through global scale, diversified product portfolios, and strong distribution networks. Smaller players focus on regional markets, specialised materials e.g., recycled content or paper-based wraps or tailor-made solutions, maintaining pressure on innovation and cost efficiency.

As materials costs and sustainability regulations intensify, competition is shifting toward high-performance films, recycled content, and integrated packaging solutions, making the market dynamic even within its consolidated structure.

Key Industry Developments:

- In Jan 2025, Smurfit Westrock launched a 100% paper-based pallet wrap made from Nertop® Stretch Kraft paper, offering a recyclable alternative to polyethylene stretch wraps. Innovation enhances supply chain sustainability, reduces CO2 emissions, and maintains high performance under humid conditions, marking a significant step in sustainable pallet wrapping solutions.

- In October, 2025, European Plastic Films (EuPF): EuPF welcomed the European Commission’s full exemption for pallet wrapping films and straps from the 100% reuse targets under Articles 29(2) and (3) of the PPWR, citing economic and logistical constraints, while advocating for a science-based approach to ensure future reuse obligations balance environmental benefits with operational efficiency.

- In April 2025, Springpack launched Armour Wrap ECO, a hand and machine-pallet wrap made from 100% post-consumer recycled content, offering tear resistance, superior cling, and reduced material usage. The fully recyclable wrap lowers virgin plastic consumption and Scope 3 emissions, targeting warehouses, distributors, and logistics operations.

Companies Covered in Pallet Wraps Market

- Berry Global

- Sigma Plastics Group

- Paragon Films

- Inteplast Group

- Coveris

- AEP Industries

- Intertape Polymer Group

- Clondalkin Group

- US Packing and Wrapping

- ULINE

- Seaman Paper

- Jhone Maye Company

- Green Spider Pallet Wraps

- Dara, Inc.

Frequently Asked Questions

The global pallet wraps market is projected to be valued at US$3.3 Bn in 2025.

The Linear Low-Density Polyethylene (LLDPE) segment is expected to hold around 48.9% market share by Material Type in 2025 in the Global Pallet Wraps Market.

The market is expected to witness a CAGR of 5.3% from 2025 to 2032.

The Pallet Wraps market is driven by surging e-commerce and omnichannel fulfilment needs coupled with rising sustainability mandates that push demand for recyclable, bio-based, and high-performance wrapping solutions.

The key market opportunities in the Pallet Wraps Market lie in smart packaging integration with IoT-enabled tracking and the rapid expansion of bio-based, biodegradable, and circular-economy film solutions that meet advanced automation and sustainability requirements.