- Pharmaceuticals

- Oncology Drugs Market

Oncology Drugs Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Oncology Drugs Market by Drug Class (Chemotherapy, Targeted Therapy, Immunotherapy, and Hormonal Therapy), Indication (Breast Cancer, Lung Cancer, Prostate Cancer, Multiple Myeloma, Colorectal Cancer, Non-Hodgkin's Lymphoma, Kidney Cancer, Chronic lymphocytic Leukaemia, Melanoma, and Others), Route of Administration, Distribution Channel, and Regional Analysis from 2025 to 2032

Oncology Drugs Market Share and Trends Analysis

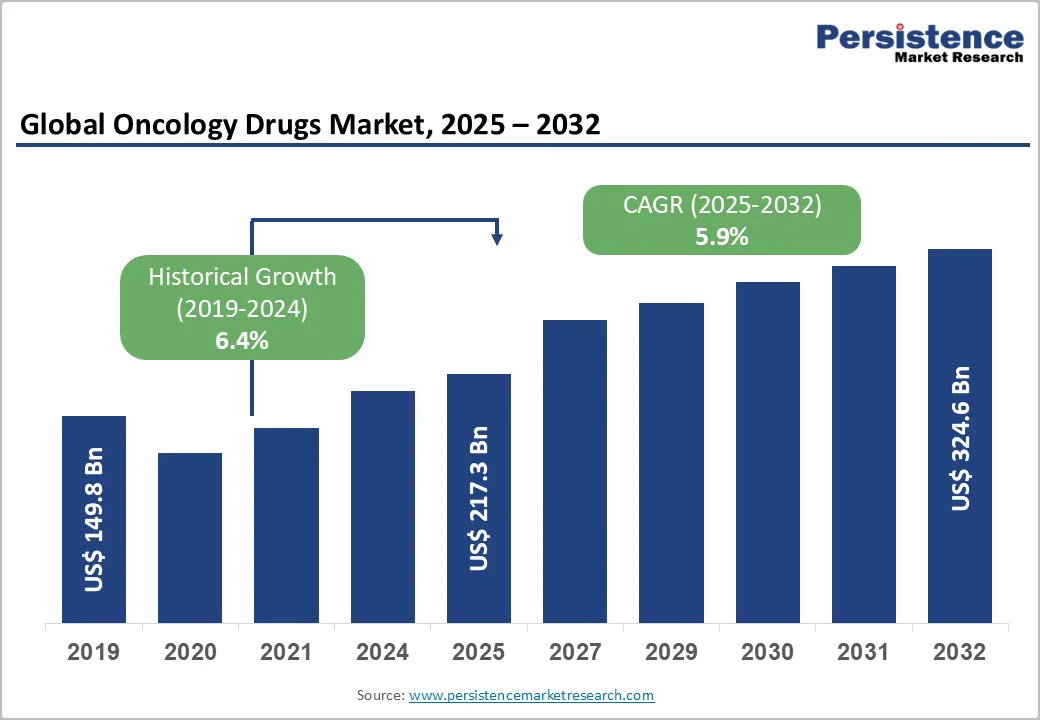

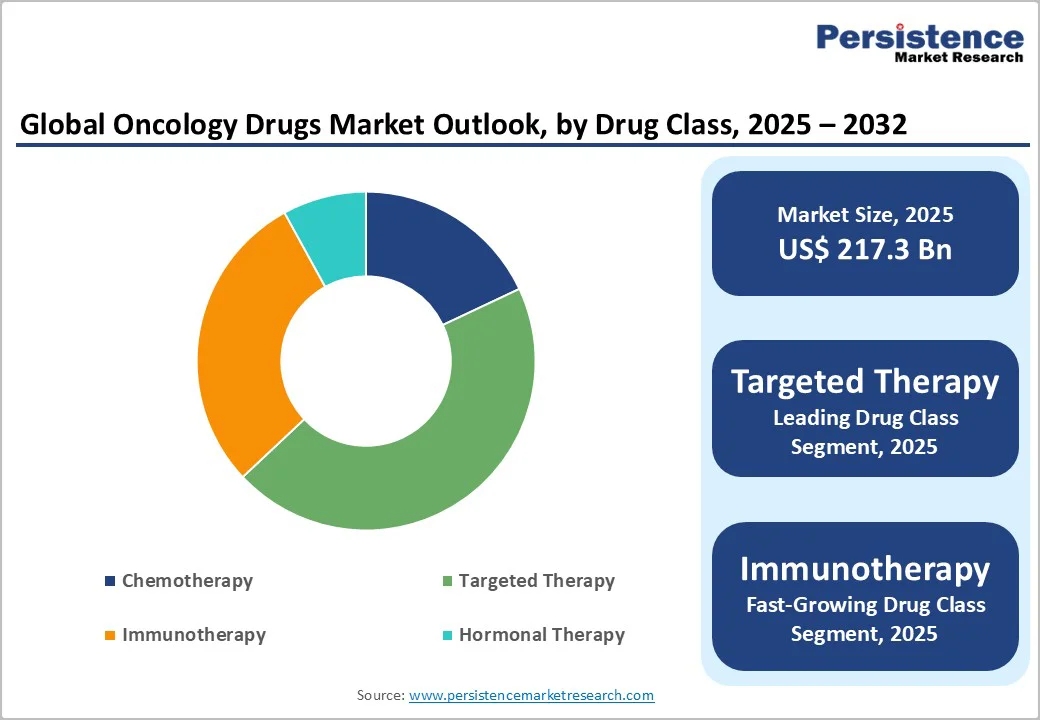

The global oncology drugs market size is valued at US$ 217.3 billion in 2025 and projected to reach US$ 324.6 billion growing at a CAGR of 5.9% during the forecast period from 2025 to 2032. The oncology drugs market is experiencing strong expansion driven by the rising global cancer burden and rapid progress in precision-based treatments.

Continued R&D investments, alongside the introduction of innovative biologics and combination regimens, are addressing long-standing unmet clinical needs and reshaping therapeutic approaches. Targeted therapies and immunotherapies are leading a paradigm shift, offering higher efficacy, improved survival outcomes, and more personalized treatment pathways.

These advances, supported by accelerated regulatory approvals in major markets, are enabling faster commercialization of novel molecules.

Key Industry Highlights:

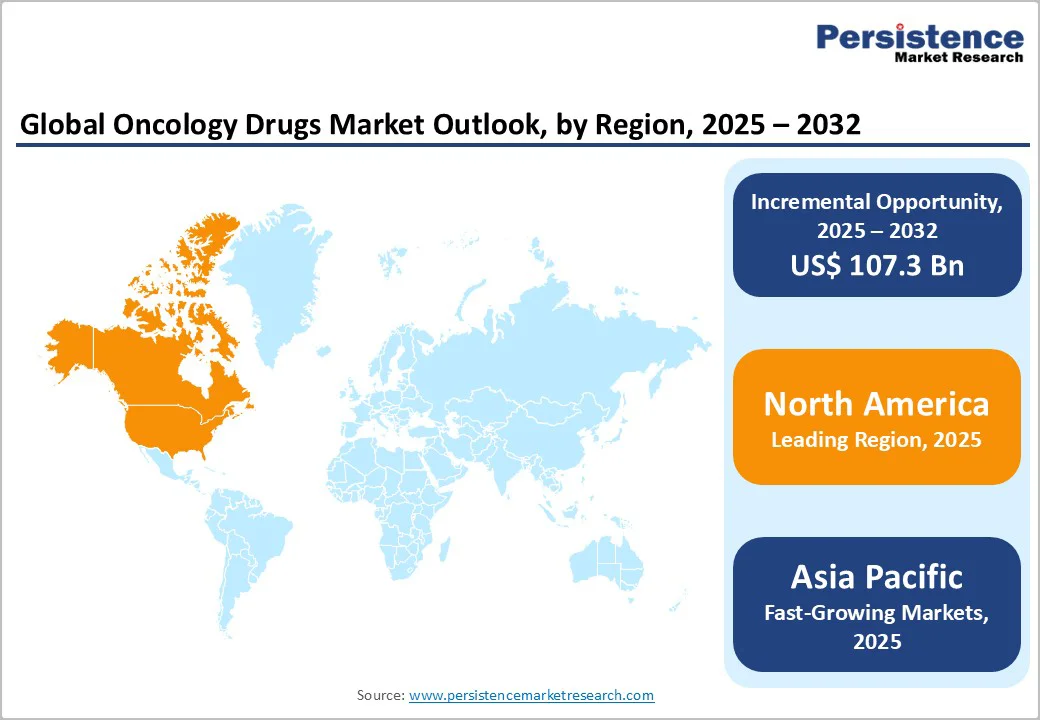

- Leading Region: North America continues to dominate the global oncology drugs market aided by robust regulatory support, innovation, and high patient access.

- Fastest Growing Region: Asia Pacific emerges as the fastest growing regional market, propelled by large patient populations, regulatory reforms, and manufacturing capacity expansion.

- Dominant Segment: Targeted therapy is the dominant drug class, holding a substantial 47% market share in 2024 due to its superior clinical outcomes and tolerability.

- Fastest Growing Segment: Immunotherapy is the fastest-growing segment, driven by advancements in immune checkpoint inhibitors and cell-based therapies.

| Key Insights | Details |

|---|---|

| Oncology Drugs Market Size (2025E) | US$ 217.3 Bn |

| Market Value Forecast (2032F) | US$ 324.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.4% |

Market Dynamics

Driver - Rising Incidence of Cancer Globally Driving Market Growth

The continuous rise in global cancer prevalence, has sharply enlarged the need for effective and accessible treatment options. According to the World Health Organization (WHO), more than 19.3 million new cancer cases were diagnosed in 2022, reflecting a rapidly expanding patient pool requiring timely therapeutic intervention.

This surge is further intensified by demographic and lifestyle shifts, including a growing aging population one of the highest-risk groups for cancer development and the widespread adoption of lifestyle factors such as obesity, tobacco consumption, excessive alcohol use, and sedentary behavior. These risk factors contribute significantly to the rising incidence of multiple cancer types worldwide.

Projections from the International Agency for Research on Cancer (IARC) indicate that the global cancer burden could reach 28.4 million new cases by 2040, marking nearly a 50% rise from current levels. Such an escalation places substantial pressure on healthcare systems, driving demand for advanced pharmacological solutions that can improve survival outcomes, reduce treatment toxicity, and enhance quality of life.

As a result, pharmaceutical companies are expanding research pipelines, accelerating drug development, and introducing novel targeted therapies, immunotherapies, and combination regimens. This sustained increase in prevalence directly fuels long-term market growth.

Restraints - High Cost of Oncology Drug Development and Treatment

The high cost associated with developing and delivering oncology drugs continues to be a significant barrier to market expansion. Advanced therapeutics such as biologics, monoclonal antibodies, CAR-T cell therapies, and next-generation immuno-oncology agents require extensive research, complex manufacturing, and long, multi-phase clinical trials.

These development pathways often span several years and demand substantial financial investment, driving up final treatment prices once the drugs reach the market. As a result, many newly approved cancer medicines enter healthcare systems at premium price points, placing considerable economic pressure on both patients and payers.

In low- and middle-income regions, affordability challenges are even more pronounced. Limited insurance coverage, restrictive reimbursement policies, and high out-of-pocket expenses prevent widespread access to cutting-edge therapies.

Patients frequently struggle to afford essential cancer treatments, resulting in delayed care, treatment interruptions, or complete non-utilization. Even in developed markets, rising oncology drug prices strain public health budgets and challenge long-term sustainability of cancer treatment programs.

Opportunity - Innovative Breakthroughs in Targeted & Immuno-Oncology Therapies

Rapid innovation in targeted therapy and immuno-oncology is creating one of the most compelling growth opportunities in the global oncology drugs market. Breakthroughs in PD-1/PD-L1 and CTLA-4 inhibitor classes, along with the expanding potential of CAR-T cell platforms, are redefining treatment standards by delivering superior clinical responses, longer survival, and improved patient quality of life.

As oncology moves toward a precision-driven model, the demand for therapies guided by genetic and molecular biomarkers continues to rise. This shift is accelerating the adoption of targeted agents, many of which demonstrate higher efficacy and reduced toxicity compared to conventional chemotherapy.

Growing R&D investments, coupled with a surge in biomarker-based clinical trials, are opening avenues for highly personalized treatment regimens. Pharmaceutical companies are increasingly focusing on next-generation technologies such as bispecific antibodies, T-cell engagers, and novel checkpoint modulators, creating a rich pipeline of potential blockbuster drugs.

Regulatory agencies are also offering expedited pathways for breakthrough therapies, enabling faster market entry and wider patient access. With strong clinical validation and expanding applicability across solid tumors and hematologic malignancies, innovative targeted and immuno-oncology therapies represent a significant opportunity for sustained market growth over the coming decade.

Category-wise Analysis

By Drug Class Insights

Targeted therapy is the leading drug class in 2025 accounting for nearly 47% of the oncology drugs market as precision medicine continued to reshape cancer care. Its dominance stems from the strong clinical performance of monoclonal antibodies and small-molecule inhibitors, which offer higher specificity, reduced toxicity, and superior response rates compared to traditional chemotherapy.

Steady regulatory approvals, expansion into new indications, and robust R&D pipelines have further strengthened targeted therapy’s position as the preferred standard across multiple tumor types. The segment also benefits from growing biomarker testing and companion diagnostics, which support more accurate treatment selection and improved patient outcomes.

While targeted therapy leads in overall market share, immunotherapy stands out as the fastest-growing category. Checkpoint inhibitors, CAR-T cell therapies, and emerging modalities such as bispecific antibodies and T-cell engagers are driving rapid adoption due to their ability to generate durable responses, even in advanced or refractory cancers.

Rising clinical success, expanding trial activity, and broader application across solid tumors and hematologic malignancies are accelerating its growth trajectory. Continued advancements in immune engineering, personalized cell therapies, and combination regimens position immunotherapy as the most dynamic and transformative segment within the oncology drugs landscape.

By Indication Insights

Breast cancer continues to hold the dominant position in the global oncology drugs market, accounting for over 16% share in 2025. Its leading status is closely linked to the high disease burden worldwide; according to the International Agency for Research on Cancer (IARC), breast cancer recorded over 2.3 million new cases in 2022, making it the most frequently diagnosed cancer globally.

This substantial patient population drives sustained demand for effective pharmacological interventions.

The segment’s strength is reinforced by continuous progress in HER2-targeted therapies, CDK4/6 inhibitors, and emerging immunotherapy options that have significantly improved survival outcomes.

Pharmaceutical companies remain highly active in developing next-generation agents, including antibody-drug conjugates and personalized treatment combinations, further expanding therapeutic choices. Growing awareness programs, routine screening initiatives, and early detection efforts in both developed and developing regions also contribute to higher diagnosis rates and treatment uptake.

Additionally, broader access to newly approved therapies, improved reimbursement pathways, and increasing adoption of precision oncology approaches support breast cancer’s continued leadership within the oncology drug landscape. With ongoing innovation and expanding clinical pipelines, the segment is expected to maintain its strong market position over the forecast period.

Region-wise Insights

North America Oncology Drugs Market Trends

North America continues to command the largest share of the global oncology drugs market share for 36% in 2025. The region’s leadership is anchored in its advanced healthcare infrastructure, deep scientific expertise, and strong presence of major pharmaceutical innovators.

The U.S. continues to be the main center for cancer research, supported by extensive funding from public agencies, private investors, and academic-industry partnerships. This ecosystem consistently generates a rich pipeline of targeted therapies, immuno-oncology agents, and next-generation biologics.

A key strength of the region is the regulatory environment. The U.S. Food and Drug Administration (FDA) provide multiple accelerated pathways such as Fast Track, Breakthrough Therapy, and Priority Review, enabling quicker access to transformative cancer treatments.

This has been especially evident in the rapid approval of checkpoint inhibitors, CAR-T therapies, and antibody-drug conjugates. Additionally, strong reimbursement mechanisms under Medicare, Medicaid, and commercial insurers ensure wide adoption once products are launched.

Patient advocacy groups and cancer networks play a vital role in driving awareness, improving clinical trial participation, and supporting early access programs.

The region also benefits from high diagnostic penetration, extensive genomic profiling, and widespread use of companion diagnostics, which further accelerates the uptake of precision-based oncology solutions. Together, these factors reinforce North America’s status as the world’s most influential oncology market, both in innovation and commercial performance.

Asia and Pacific Oncology Drugs Market Trends

Asia Pacific is emerging as the fastest-growing region in the global oncology drugs landscape, propelled by its large population base, rising cancer incidence, and ongoing investments in modern healthcare infrastructure. Countries such as China, Japan, South Korea, and India are shaping the region’s momentum through expanded screening programs, stronger treatment networks, and increased government focus on non-communicable diseases.

China remains a central force, supported by a robust domestic pharmaceutical industry and numerous collaborations with global drug developers. Regulatory reforms under agencies like the NMPA have shortened approval timelines, allowing faster entry of innovative oncology therapies, including targeted drugs and immunotherapies.

Japan continues to lead in technology adoption, particularly for precision diagnostics and advanced biologics. Meanwhile, India benefits from a growing generic and biosimilars sector, making many essential cancer treatments more affordable and accessible.

Across the region, rising awareness campaigns and improvements in early detection are contributing to higher treatment rates. The expansion of health insurance coverage in several Asia Pacific countries is also enabling more patients to access modern cancer therapies that were previously out of reach. Additionally, the rapid growth of clinical trial activity and increased foreign investments are strengthening research capabilities.

With its combination of unmet need, improving regulatory processes, and expanding healthcare access, Asia Pacific is positioned to remain the fastest-advancing oncology drugs market in the coming years.

Competitive Landscape

The oncology drugs market exhibits moderate concentration, with leading global pharmaceutical giants such as Pfizer Inc., Novartis AG, F. Hoffmann-La Roche Ltd, and AstraZeneca plc commanding sizable shares, and a broad base of emerging players contributing novel therapies.

Companies are increasingly pursuing M&A, collaborative research, and partnerships to broaden portfolios and access new technologies. A sharp focus on immuno-oncology and biomarker-guided drugs sets apart leaders, while the industry embraces digital health and real-world evidence as next-generation business model differentiators.

Key Industry Developments:

- In June 2025, AstraZeneca’s Camizestrant showed a 56% reduction in the risk of disease progression or death in advanced HR-positive breast cancer patients with an emergent ESR1 mutation, according to the SERENA-6 Phase III trial.

- In May 2025, Merck (MSD outside the U.S. and Canada) announced that new research spanning over 25 cancer types and multiple treatment settings from its broad portfolio and pipeline will be presented at the ASCO Annual Meeting.

Companies Covered in Oncology Drugs Market

- GlaxoSmithKline

- AstraZeneca plc

- AbbVie

- Pfizer Inc.

- Amgen Inc.

- Gilead Sciences, Inc.

- F. Hoffmann-La Roche Ltd

- Bristol-Myers Squibb Company (Celgene Corp)

- Novartis AG

- Johnson & Johnson

- Merck & Co.

- Eli Lilly and Company

- Sanofi S.A

- Bayer AG

- Others

Frequently Asked Questions

The global oncology drugs market is projected to be valued at US$ 217.3 Bn in 2025.

Rising cancer cases, rapid precision therapy advancements, strong R&D investments, and faster regulatory approvals collectively drive the global oncology drugs market.

The global market is poised to witness a CAGR of 5.9% between 2025 and 2032.

Breakthroughs in immunotherapy, targeted agents, personalized medicine, companion diagnostics, and expanding access in emerging markets create major growth opportunities.

Companies such as GlaxoSmithKline, AstraZeneca plc, AbbVie, Pfizer Inc., Amgen Inc., are some of the major players operating in the market.