- Medical Devices

- AI in Oncology Market

AI in Oncology Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

AI in Oncology Market by Product Type (Software Solutions, Hardware, Services), Cancer Type (Breast Cancer, Lung Cancer, Prostate Cancer, Colorectal Cancer, Brain Tumour, Others), Application (Chemotherapy, Immunotherapy, Radiotherapy, Others), End User (Hospitals, Biopharmaceutical Companies, Academic and Research Centers, Others), and Regional Analysis from 2026 to 2033

AI in Oncology Market Size and Trends Analysis

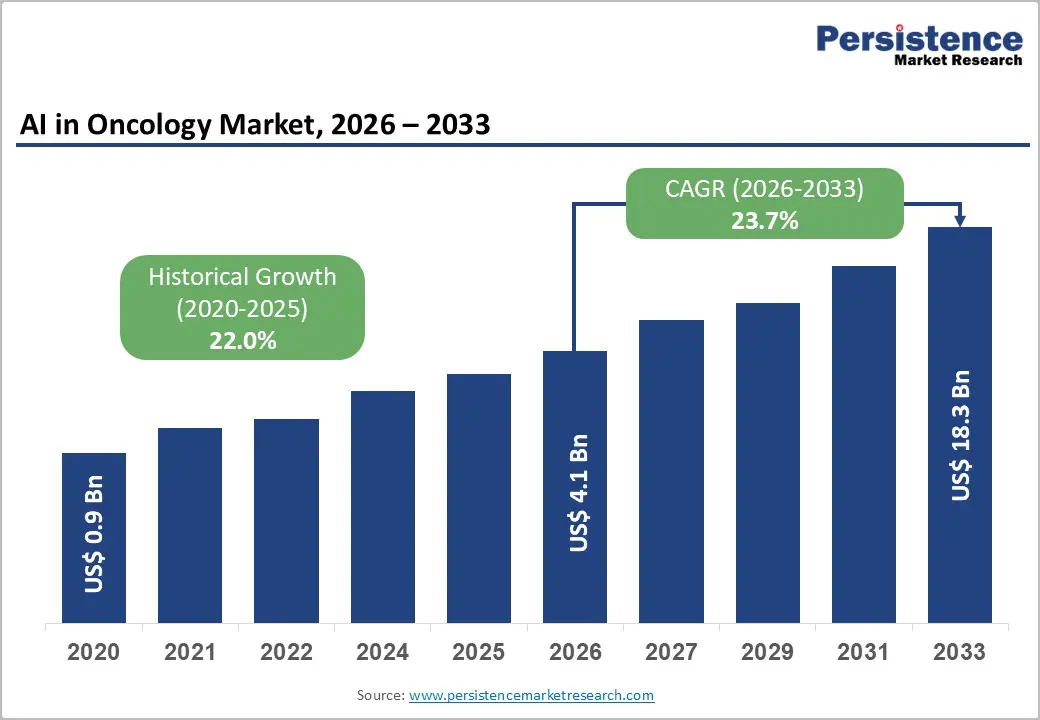

The global AI in oncology market is estimated to grow from US$ 4.1 Bn in 2026 to US$ 18.3 Bn by 2033. The market is projected to grow at a CAGR of 23.7% from 2026 to 2033.

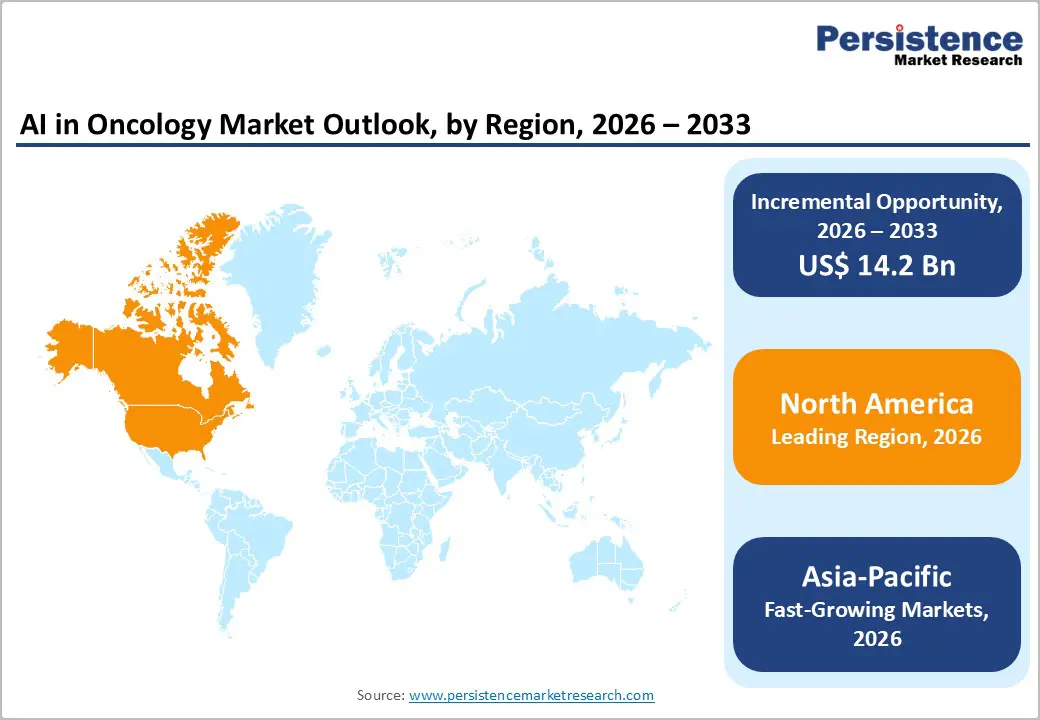

The global AI in oncology market is growing steadily, fueled by rising demand for digital healthcare, advanced analytics, and antiviral therapies. North America leads with robust infrastructure, strict regulations, and high-quality production. The Asia-Pacific region is the fastest-growing, driven by expanding healthcare facilities, government support, increased patient awareness, and investments in interoperable diagnostics and manufacturing solutions.

Key Industry Highlights

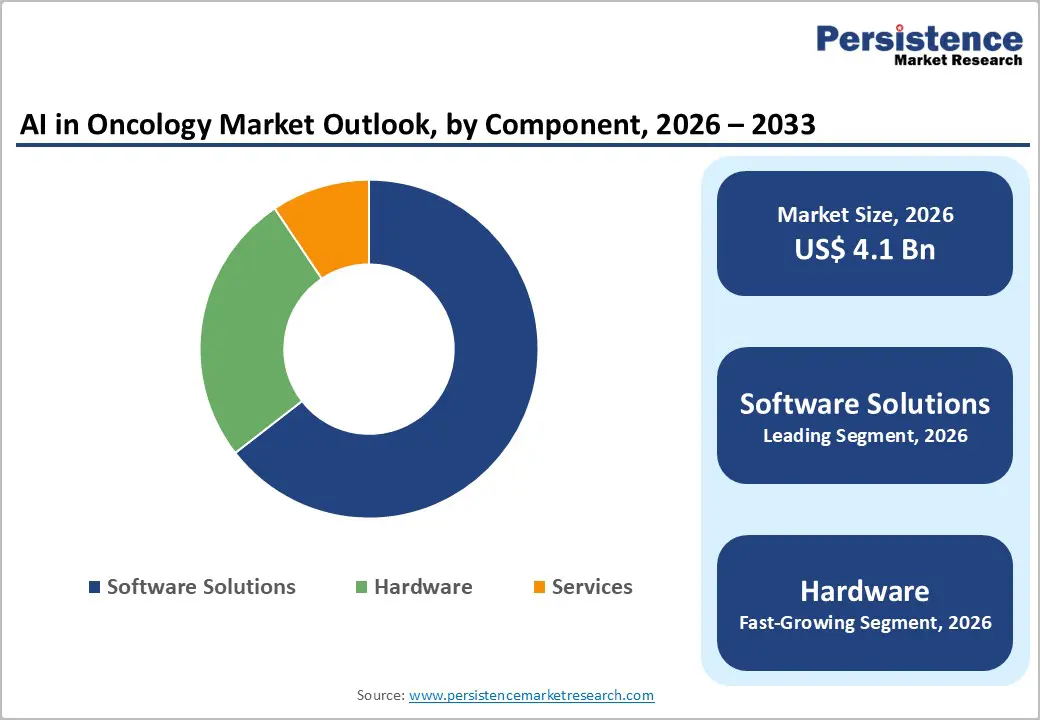

- Dominant Segment: AI-powered software solutions account for 64.5% of the market in 2025. Designed for precision oncology, predictive analytics, and treatment personalization, they enable accurate tumor detection, therapy planning, and patient monitoring. Integration with electronic health records and AI-based decision support systems ensures consistent, data-driven care, supports personalized medicine, optimizes clinical workflows, and enables next-generation oncology strategies.

- Dominant Region: North America leads with 46.7% share in 2025, supported by advanced healthcare infrastructure, regulatory rigor, and early adoption of AI-enabled oncology tools. Asia-Pacific is the fastest-growing region, driven by expanding hospitals and biotech facilities, government initiatives, rising R&D investments, and the adoption of scalable AI oncology solutions.

- Market Drivers: Increasing cancer prevalence, demand for personalized and precise therapies, technological advances in AI analytics, and rising biopharmaceutical investments are driving growth.

- Market Opportunity: Opportunities include AI-enabled predictive oncology, integration with personalized treatment pipelines, real-world data analytics, scalable AI platforms, and expansion into emerging healthcare and biotech markets.

| Global Market Attributes | Key Insights |

|---|---|

| Global AI in Oncology Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 18.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 23.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 22.0% |

Market Dynamics

Driver: Rising Cancer Prevalence and Early Diagnosis Demand

Cancer remains a leading global health challenge, with nearly 20 million new cases diagnosed worldwide in 2022 and about 9.7 million deaths attributed to the disease, according to the American Cancer Society’s Global Cancer Facts & Figures. Projections indicate that new annual cases could reach 35 million by 2050, driven by population ageing and lifestyle risk factors, underscoring the growing burden on healthcare systems. Early detection is critically linked to improved patient outcomes; for example, five-year survival for cancers like breast cancer can exceed 99 % when caught early, compared with much lower survival at advanced stages.

Against this backdrop, demand for AI technologies in oncology diagnostics and early screening is intensifying. AI algorithms can analyze imaging data (e.g., mammograms, CT scans) and electronic health records at scale, detecting subtle indicators of malignancy that might be missed by traditional methods. Pilot programs in clinical settings show AI use increases detection rates, for instance, one AI tool boosted cancer identification by 8% in general practice settings in England. This data-driven demand for earlier detection supports the AI in Oncology Market’s expansion, as providers and governments seek tools to reduce late-stage diagnoses, improve survival outcomes, and alleviate long-term treatment costs.

Restraints: High Implementation and Software Integration Costs

Integrating AI solutions into oncology workflows involves substantial financial investment, encompassing software licensing, data infrastructure, and clinician training. Reports on healthcare AI adoption indicate that deploying AI systems can cost millions of dollars per mid-sized hospital, factoring in high-performance computing, secure servers, continuous software updates, and expert personnel to manage and interpret model outputs. These costs are especially prohibitive for smaller hospitals and clinics, limiting AI uptake beyond large academic centers.

Beyond upfront expenses, the complexity of AI integration with legacy electronic health record (EHR) systems further drives costs. Healthcare data is often siloed and unstandardized, requiring extensive preprocessing before AI can operate effectively. Fragmented workflows and interoperability issues between AI tools and existing clinical systems require hospitals to invest additional resources in customization and workflow redesign. Additionally, adherence to strict privacy regulations, such as the U.S. Health Insurance Portability and Accountability Act (HIPAA) or Europe’s General Data Protection Regulation (GDPR), requires robust security and compliance infrastructures, adding ongoing operational expenses.

These financial and technical burdens act as a restraint on the AI in Oncology Market, slowing adoption in resource constrained settings and delaying the widespread clinical deployment that would otherwise accelerate innovation and broaden clinical impact.

Opportunity: AI-Driven Predictive Oncology and Treatment Planning

One of the most promising opportunities in the AI in oncology market lies in predictive oncology, using AI to forecast disease progression, treatment response, and patient outcomes. Advanced machine learning models analyze vast datasets, including genomic sequences, imaging results, and clinical histories, to provide prognostic insights tailored to individual patients. Research indicates AI models can achieve up to 80% accuracy in predicting disease trajectories by interpreting unstructured electronic health data, and can augment risk stratification beyond traditional clinical indicators.

Moreover, studies demonstrate that AI-recommended treatment pathways can deliver meaningful clinical benefits, including 20% improvements in survival rates and extended progression-free survival for certain cancers when integrated into treatment planning. Predictive analytics also enhances clinical trial matching, helping identify patients most likely to benefit from experimental therapies and improving trial efficiency. The Cancer Moonshot and other national initiatives are promoting predictive models to tailor immunotherapy, chemotherapy, and targeted treatments, accelerating personalized oncology care.

These predictive capabilities represent a significant market opportunity as healthcare systems transition from reactive to proactive cancer management. AI-enabled treatment planning tools can reduce unnecessary interventions, optimize resource use, and improve patient outcomes, creating value for providers, payers, and patients alike.

Category-wise Analysis

By Component, Software Solutions Dominate the AI in Oncology Market

Software Solutions holds a 64.5% share of the global market in 2025, as they form the core layer that enables clinical interpretation, integration, and decision support across oncology workflows. These platforms incorporate machine learning, deep learning, and advanced analytics to process complex datasets, such as radiology images, pathology slides, and electronic health records, more quickly and accurately than manual methods. AI software can reduce diagnostic turnaround times by up to 30% and improve detection precision, enhancing clinical outcomes and operational efficiency in hospitals and cancer centers. Software’s scalability and compatibility with existing IT systems, particularly electronic health records, facilitate cross-departmental deployment without extensive hardware changes. Cloud-based delivery models further lower barriers by enabling on-demand compute and storage resources for analytics and AI model training.

By Cancer Type, Breast cancer leads AI oncology use due to high incidence, early detection needs, and imaging data

Breast cancer dominates AI oncology applications due to its very high global incidence and critical need for early detection and screening. According to the World Health Organization, an estimated 2.3 million new breast cancer cases occurred worldwide in 2022, making it the most commonly diagnosed cancer in women across most countries. Early diagnosis dramatically improves survival, so technologies that enhance imaging interpretation and risk prediction are in strong demand. AI systems applied to mammograms, MRI, and ultrasound can detect subtle abnormalities that might be overlooked by human observers, improving the sensitivity and consistency of screening outcomes. The sheer volume of imaging data generated in breast cancer screening also creates a favorable environment for software-based AI adoption, as these tools reduce workload for radiologists and support personalized treatment planning.

Regional Insights

North America AI in Oncology Market Trends

North America dominates the AI in oncology market, with a 46.7% share in 2025, driven by a mature healthcare ecosystem and deep investments in digital health infrastructure. The U.S. healthcare system has widely adopted electronic health records, facilitating AI applications in imaging, diagnostics, and treatment planning. Large datasets and research initiatives, such as the NIH’s All of Us Research Program with hundreds of thousands enrolled, provide critical real-world data to train and refine AI models. U.S. regulatory bodies like the FDA have cleared more than 50 AI/ML-enabled oncology tools, signaling robust clinical acceptance and pathway clarity that drives adoption. Leading tech and healthcare companies, extensive R&D funding, and early AI deployment across cancer centers further strengthen North America’s position.

Europe AI in Oncology Market Trends

Europe is a significant region for the AI in oncology market due to strong healthcare systems, coordinated digital health strategies, and supportive policy environments that encourage AI adoption. Countries such as Germany, the United Kingdom, and France are actively piloting and integrating AI tools in oncology workflows, including diagnostics and precision treatment planning. The European Union is also advancing digital health policies that aim for broad AI uptake across healthcare, balancing innovation with data protection and ethical standards. European health authorities emphasize AI’s role in optimizing hospital resource use, improving patient outcomes, and enabling predictive analytics in cancer care. These efforts, combined with public funding and cross-country research collaborations, make Europe a key growth and innovation region in oncology AI adoption.

Asia-Pacific AI in Oncology Market Trends

Asia Pacific is the fastest growing region in the ai in oncology market, driven by rapidly increasing cancer incidence, healthcare digitization, and expanding healthcare spending. Nations such as China, India, Japan, and South Korea are bolstering investments in oncology infrastructure, radiology, and genomics, creating fertile ground for AI implementation. Healthcare systems in the region are modernizing through government-led digital health initiatives and public-private partnerships that accelerate AI integration into cancer screening and treatment workflows. Large and aging populations further magnify demand for scalable, efficient cancer diagnostics and personalized care. This combination of rising patient volume, expanding digital health ecosystems, and proactive policy support translates to a high compound annual growth rate for AI adoption in oncology across the Asia Pacific, surpassing more mature markets.

Market Competitive Landscape

Leading AI in Oncology companies focus on advanced diagnostic and therapeutic software, scalable deployment, and regulatory compliance. Investments target AI-driven model development, predictive analytics, and workflow optimization. Strategic collaborations with hospitals, research institutions, and regulators, coupled with robust validation and integration with clinical systems, accelerate global adoption in cancer care and research.

Key Industry Developments:

- In January 2026, CancerIQ and Azra AI announced they had formed a strategic partnership to enhance lung cancer screening programs by combining risk-based patient identification with AI-powered imaging follow-up.

- CancerIQ’s platform helped healthcare providers identify high-risk individuals and guide appropriate scheduling of low-dose CT (LDCT) screening.

- In April 2025, Elekta and Azra AI announced a strategic partnership to enhance cancer registry operations through AI–powered automation. The collaboration combined Elekta’s Elekta ONE Registry Informatics software with Azra AI’s real-time patient identification and workflow automation tools to automate case finding, streamline data ingestion, and improve reporting accuracy.

Companies Covered in AI in Oncology Market

- Azra AI

- IBM

- Siemens Healthcare GmbH

- GE Healthcare

- NVIDIA Corporation

- Digital Diagnostics Inc.

- ConcertAI

- Median Technologies

- PathAI

- Berg (BPGbio Inc.)

- iCAD

- JLK Inspection

- Roche Diagnostics

- Zebra Medical Vision

- Illumina Inc.

- Envisionit DeepAI Ltd

- Others

Frequently Asked Questions

The global AI in oncology market is projected to be valued at US$ 4.1 Bn in 2026.

Rising cancer prevalence, early diagnosis demand, personalized therapies, AI adoption, and advanced analytics drive growth.

The global AI in oncology market is poised to witness a CAGR of 23.7% between 2026 and 2033.

Opportunities include predictive oncology, personalized treatment planning, AI-driven diagnostics, real-world data analytics, and emerging markets expansion.

Azra AI, IBM, Siemens Healthcare GmbH, GE Healthcare, NVIDIA Corporation, Digital Diagnostics Inc.